Global Payments 2020-30 a Quantium Shift in the Next Decade Australia's Challenge

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wolfefintechforum DAY 1 AGENDA

#WolfeFinTechForum DAY 1 AGENDA - TUESDAY, MARCH 9, 2021 Opening Remarks 7:50-8:00am ET Wolfe Research – Darrin Peller, Managing Director, Payments, Processors, and IT Services Shift4 Payments 8:00-8:35am ET Jared Isaacman - CEO Fiserv 8:40-9:15am ET Frank Bisignano – President & CEO JP Morgan Chase 9:20-9:55am ET Max Neukirchen – CEO of Merchant Services Mastercard 10:00-10:35am ET Sachin Mehra - CFO B2B Payments: Living Through an Inflection Billtrust – Mark Shifke, CFO Discover Financial Services 10:40-11:15am ET MineralTree – Chris Sands, CFO John Greene – EVP & CFO Repay Holdings Corporation – Jake Moore, EVP Corporate Development & Strategy Fidelity National Information Services 11:20-11:55am ET Gary Norcross – President & CEO Woody Woodall - CFO PayPal 12:00-12:40pm ET Dan Schulman - CEO 12:40-1:00pm ET BREAK Square 1:00-1:35pm ET Amrita Ahuja - CFO Jack Henry & Associates, Inc. 1:40-2:15pm ET David Foss – President & CEO Synchrony 2:20-2:55pm ET Brian Wenzel, Sr – EVP & CFO Paychex, Inc. 3:00-3:35pm ET Efrain Rivera – Sr. VP, CFO & Treasurer Walker & Dunlop 3:40-4:15pm ET Willy Walker - CEO Cross-Border B2B: Still So Hard to Reach 4:20-4:55pm ET Credorax - Benny Nachman, Founder & Chairman of the Board Tipalti Inc. - Sarah D. Spoja, CFO COMPANIES HOSTING 1X1s ONLY – MARCH 9 Cielo S/A - Daniel Henrique de Sousa Diniz, Head of IR Coro Global Inc - David Dorr, Co-Founder & Mark Goode, CEO Finix Payments - Emanuel Pleitez, Head of Business Development FleetCor Technologies - Jim Eglseder, SVP, IR Global Blue Far Peak Acquisition Corporation - Thomas Farley, Chairman & CEO of Far Peak Acquisition Corporation Houlihan Lokey, Inc. -

Emerging Payments Trends

E M E R G I N G T R E N D S I N P A Y M E N T S I N N O V A T I O N M A5Y 2 0 2 0 real-time product and consumer insight on all competitors and new entrants Contact us at: pi-360@thefuturistgroup. com SECURITY INNOVATION CONSUMERS WANT Map every security feature on the market and 2 0 % identify innovation that drives product engagement r i s e i n f r a u d by consumer segment (e.g., GenZ, Millennials, 1 S T Q U A R T E R O F 2 0 2 0 Subprime, Prime, etc.). Virtual card #'s, biometrics, dynamic cvv, monitoring, alerts, protection insurance, etc. Mastercard | Visa | Apple | C apital One | Discover | Oberthur + more NEW PATH TO PROFITABILITY See shifting consumer needs and opportunity for 3 0 % driving long-term, profitable usage. D R O P I N Preferred reward constructs (tiered vs. flat etc.) C R E D I T S P E N D SWOT vs. competitors and their products a P R I L 2 0 2 0 Consumer data & insight on every innovative benefit deployed in response to COVID All Banks + Amazon| Instacart | Netflix| Zoom | DoorDash| SoFi + more FUTURE OF CONTACTLESS 4 0 % Understand near-term and longer-term i n c r e a s e i n opportunity for contactless communication & c o n t a c t l e S S innovation. Consumer insight data on every form a P R I L 2 0 2 0 of contactless including card plastic, mobile app, wearables, biometric, and connected car All Banks + Tappy | Fitbit | Apple | Samsung | Biohax | Connected Cars + more RISE OF DEBIT CARD REWARDS 2 . -

Visa's Annual Report

Annual Report 2017 Annual Report 2017 Mission Statement To connect the world through the most innovative, reliable and secure digital payment network that enables individuals, businesses and economies to thrive. Financial Highlights (GAAP) In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $7,199 $6,214 Operating income $9,064 $7, 883 $12,144 Net income $6,328 $5,991 $6,699 Stockholders' equity $29,842 $32,912 $32,760 Diluted class A common stock earnings per share $2.58 $2.48 $2.80 Financial Highlights (ADJUSTED)1 In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $5,060 $6,022 Operating income $9,064 $10,022 $12,336 Net income $6,438 $6,862 $8,335 Diluted class A common stock earnings per share $2.62 $2.84 $3.48 Operational Highlights² 12 months ended September 30 (except where noted) 2015 2016 2017 Total volume, including payments and cash volume³ $7.4 trillion $8.2 trillion $10.2 trillion Payments volume³ $4.9 trillion $5.8 trillion $7.3 trillion Transactions processed on Visa's networks 71.0 billion 83.2 billion 111.2 billion Cards⁴ 2.4 billion 2.5 billion 3.2 billion Stock Performance The accompanying graph and chart compares the cumulative total return on $350 Visa’s common stock with the cumulative total return on Standard & Poor’s 500 Index and the Standard & Poor’s 500 Data Processing Index from September 30, $300 2012 through September 30, 2016. -

WELLBEING, RESILIENCE and PROSPERITY for AUSTRALIA FINANCIAL SYSTEM INQUIRY March 2014

WELLBEING, RESILIENCE AND PROSPERITY FOR AUSTRALIA FINANCIAL SYSTEM INQUIRY March 2014 CBA0416 FSI Doc_Final.indd 1 31/03/14 5:46 PM COMMONWEALTH BANK’S SUBMISSION IS FOCUSED ON IMPROVING THE LONG-TERM WELLBEING OF AUSTRALIANS, CONSISTENT WITH OUR VISION TO SECURE AND ENHANCE THE FINANCIAL WELLBEING OF PEOPLE, BUSINESSES AND COMMUNITIES. COMMBANK CAN. CBA0416 FSI Doc_Final.indd 2 31/03/14 5:46 PM TABLE OF CONTENTS EXECUTIVE SUMMARY 6 SECTION IV: SAFEGUARDING SECTION I: AUSTRALIA’S RETIREMENT BUILDING ON SOLID WITH A SUSTAINABLE FINANCIAL SYSTEM SUPERANNUATION FOUNDATIONS 9 SYSTEM 72 CHAPTER 1: HOW THE FINANCIAL CHAPTER 10: IMPROVE THE EFFICIENCY SYSTEM HAS SUPPORTED OF THE SUPERANNUATION SYSTEM 72 ECONOMIC STABILITY 9 CHAPTER 11: FUND AUSTRALIA’S CHAPTER 2: A FREE MARKET RETIREMENT 79 PHILOSOPHY FOR AUSTRALIA’S FINANCIAL SYSTEM 24 SECTION V: CHAPTER 3: POSITIONING AUSTRALIA ENHANCING REGULATORY FOR A PROSPEROUS FUTURE 27 EFFICIENCY 87 SECTION II: CHAPTER 12: IMPROVE EFFICIENCY SUPPORTING A STRONG AND ADAPTABILITY OF THE REGULATORY SYSTEM 87 BANKING SYSTEM 33 CHAPTER 4: ENSURE SUSTAINABLE SECTION VI: FUNDING FOR AUSTRALIAN BANKS 34 ADDRESSING OTHER CHAPTER 5: ENABLE COMPARABILITY IMPORTANT ISSUES FOR OF AUSTRALIAN BANK CAPITAL CUSTOMERS 96 RATIOS TO INTERNATIONAL PEERS 42 CHAPTER 6: EMBED A SUPPORTIVE CHAPTER 13: IMPROVE FINANCIAL OPERATING FRAMEWORK FOR LITERACY 96 AUSTRALIAN BANKS 47 CHAPTER 14: FUND INFRASTRUCTURE CHAPTER 7: ENSURE AN APPROPRIATE DEVELOPMENT 102 FRAMEWORK FOR THE SHADOW CHAPTER 15: IMPROVE ACCESS BANKING SECTOR 52 TO -

Annual Report and Sustainability Update 2018/2019

Annual Report and Sustainability Update 2018–2019 “Our dedication to running an ethical and sustainable institution has been recognised with Teachers Mutual Bank Limited being named one of the World’s Most Ethical Companies for the sixth year running.” Contents Annual Report and Sustainability Update Our mission is to deliver quality financial products and services to workers and their families within the education, emergency services, and health communities. We will do this in an ethical, simple and friendly manner. Key financial performance 02 Chairperson and CEO’s report 04 Members 06 Social Responsibility 10 Community 14 Employees 18 Environment 22 Summary of Sustainability KPIs and targets 26 Directors’ report 28 Auditor’s independence declaration 32 Financial statements and notes 33 Statement of comprehensive income 34 Statement of changes in member equity 35 Statement of financial position 36 Statement of cash flows 37 Notes to the financial statements 38 Directors’ declaration 87 Independent auditor’s report 88 TEACHERS MUTUAL BANK LIMITED Telephone: 13 12 21 | Fax: (02) 9704 8205 Email: [email protected] | Address: 28-38 Powell Street Homebush NSW 2140 | PO Box: PO Box 7501 Silverwater NSW 2128 | ABN: 30 087 650 459 | AFSL/Australian Credit Licence: 238981 | Design: www.frescocreative.com.au 1 Key Financial Performance Our focus is to maintain sustainable growth to ensure we provide competitive products and services to enable our members to secure their financial futures. OVERVIEW Capital adequacy ratio Membership Capital adequacy is a ratio which protects depositors and Membership refers to all shareholders that are eligible to investors by indicating the strength of an institution. -

United States House of Representatives Financial Services Committee

United States House of Representatives Financial Services Committee Task Force on Financial Technology Is Cash Still King? Reviewing the Rise of Mobile Payments Testimony of Christina Tetreault Senior Policy Counsel Consumer Reports January 30, 2020 1 Introduction Chairman Lynch and Ranking Member Emmer and Members of the Financial Technology Task Force, thank you for the invitation to appear today. I am Christina Tetreault, senior policy counsel on Consumer Reports’ financial services policy team. Consumer Reports is an expert, independent, non-profit organization whose mission is to work for a fair, just, and safe marketplace for all consumers and to empower consumers to protect themselves. Consumers Reports works for pro-consumer policies in the areas of financial services and marketplace practices, antitrust and competition policy, privacy and data security, food and product safety, telecommunications and technology, travel, and other consumer issues in Washington, DC, in the states, and in the marketplace. Consumer Reports is the world’s largest independent product-testing organization, using its dozens of labs, auto test center, and survey research department to rate thousands of products and services annually. Founded in 1936, Consumer Reports has over 6 million members and publishes its magazine, website, and other publications. Consumer Reports (CR) has a long history of working to improve payments protections for consumers. In 2008, the then-leader of CR’s financial services policy team, Gail Hillebrand, published a comprehensive -

Die Zukunft Des (Mobilen) Zahlungsverkehrs 5

Aktuelle Themen Globale Finanzmärkte Die Zukunft des (mobilen) Zahlungsverkehrs 5. Februar 2013 Banken im Wettbewerb mit neuen Internet-Dienstleistern Autoren Seit geraumer Zeit gerät die Finanzbranche immer stärker unter Druck: Thomas F. Dapp Die rasante Entwicklung webbasierter Technologien stellt die klassischen Ban- +49 69 910-31752 [email protected] ken insbesondere in den Bereichen Einlagen und Zahlungsverkehr vor große Herausforderungen. Gleichzeitig sorgen schärfere regulatorische Auflagen und Antje Stobbe steigender Kostendruck dafür, dass viele Banken an Innovationskraft verlieren. +49 69 910-31847 [email protected] Der Markt für digitale (mobile) Bezahlsysteme steckt noch in den Kinder- schuhen. Selbst Unternehmen in den USA, die neben Japan Vorreiter sind, Patricia Wruuck +49 69 910-31832 arbeiten erst seit ein bis zwei Jahren an relevanten Geschäftsmodellen. [email protected] Viel Aufmerksamkeit richtet sich derzeit auf die Strategien neuer Wettbewerber Weitere Beiträge: wie Google, Apple, PayPal oder Amazon. Die Netzgiganten strecken verstärkt Bryan Keane ihre Fühler in Branchen außerhalb ihres bisherigen Kerngeschäfts aus, z.B. in Jason Napier den Markt für (mobile) Bezahlsysteme. Ashish Sabadra Yoshinobu Yamada Die Banken sind gut beraten, die großen Internetunternehmen, die Kreditkarten- sowie die Telekommunikationsunternehmen im Auge zu behalten. Vier in dieser Editor Studie erarbeitete Szenarien zeigen mögliche Entwicklungen im Bereich digitaler Bernhard Speyer (mobiler) Finanzdienstleistungen in den nächsten 3-5 Jahren: Das „Early-Bird“- Deutsche Bank AG Szenario ist gekennzeichnet durch eine hohe Akzeptanz digitaler Bezahlsyste- DB Research me, ein aktives Vorgehen der Banken und einen moderaten Verdrängungswett- Frankfurt am Main bewerb. Gelingt es den Banken jedoch nicht, adäquate webbasierte, mobile Fi- Deutschland E-Mail: [email protected] nanzdienste anzubieten, drohen Verluste bei den Marktanteilen („Nachzügler“- Fax: +49 69 910-31877 Szenario). -

How We Will Calculate Your Balance:We Use a Method Called “Average Daily Balance (Including New Purchases)”. Index and When

232 - 121144 Platinum Edition® Visa® Card T-GULF-2005 Cards are issued by First Bankcard®, a division of First National Bank of Omaha, which is referred to below as “we”, “us”, “our”, and “First Bankcard”. PLEASE NOTE: If you apply for a credit card, you may receive a Platinum Edition® Visa® Card, a Visa Signature® Card, or we may decline to open an account for you. Eligibility for card products depends on the information provided in your application and your credit card history. The card you are approved for will determine your Visa benefits. IMPORTANT RATE, FEE AND OTHER COST INFORMATION (SUMMARY OF CREDIT TERMS) Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 26.99% when you open your account. This APR will vary with the market based on the Prime Rate. APR for Balance Transfers 26.99% This APR will vary with the market based on the Prime Rate. APR for Cash Advances 25.24%. This APR will vary with the market based on the Prime Rate. Penalty APR and When it Applies None How to Avoid Paying Interest on Your due date is at least 21 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.1 Purchases Minimum Interest Charge If you are charged interest, the charge will be no less than $1.75. For Credit Card Tips from the To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at Consumer Financial Protection Bureau www.consumerfinance.gov/learnmore. -

Bow Credit Card Agreement

CREDIT CARD AGREEMENT (Personal Accounts) By requesting or accepting any Standard MasterCard, account. If we accept a payment from you in excess of your Standard Visa, Platinum MasterCard, Platinum Visa, outstanding balance, your available Credit Limit will not be Platinum Rewards MasterCard, or Platinum Rewards Visa increased by the amount of the overpayment nor will we be account (individually or collectively called “Credit Card required to authorize transactions for an amount in excess account” or “Account”) with Bank of the West, you agree to of your Credit Limit. be bound by all the terms of this Agreement. In this 3. Temporary Reduction of Credit Limit. Merchants, Agreement, the words “you” or “your” mean everyone who such as car rental companies and hotels, may request prior has requested or accepted a Credit Card account with us. credit approval from us for an estimated amount of your The words “we,” “us,” “our,” or “Bank” mean Bank of the Purchases, even if you ultimately do not pay by credit. If our West. If you do not accept this Agreement, you must notify approval is granted, your available Credit Limit will us in writing within 5 days after receipt. Use of your card or temporarily be reduced by the amount authorized by us. If any feature (including a balance transfer) of your Credit you do not ultimately use your Credit Card account to pay Card Agreement shall constitute acceptance of this for your Purchases or if the actual amount of Purchases Agreement. posted to your Credit Card account varies from the 1. Use. Your Standard MasterCard, Standard Visa, estimated amount approved by us, it is the responsibility of Platinum MasterCard, Platinum Visa, Platinum Rewards the merchant, not us, to cancel the prior credit approval MasterCard, or Platinum Rewards Visa card (individually or based on the estimated amount. -

General Contracting Terms and Conditions

K&H Bank Zrt. H–1095 Budapest, Lechner Ödön fasor 9. phone: +(36 1) 328 9000 fax: +(36 1) 328 9696 www.kh.hu • [email protected] GENERAL CONTRACTING TERMS AND CONDITIONS FOR BANKCARD AND CREDIT CARD SERVICES Effective dates: December 13, 2017, January 13, 2018 and February 13, 2018 Date of announcement: December 13, 2017 These GCTC are amended pursuant to Sections XIX.1 and XIX.2 hereof with the scope and effective dates specified below. Amended provisions in Section X.6 – effective date: December 13, 2017 (the effective date is referenced in the footnotes as well) Amendments due to amended legal regulations on payment services, or required for more precise and accurate wording of these GTC – effective date: January 13, 2018 Amended provisions in Sections IX.2 and XV.8 – effective date: February 13, 2018 (provisions becoming effective as of February 13, 2018 are specified also in the footnotes. TABLE OF CONTENTS I. TERMS: ................................................................................................................................................... 4 II. BANKCARD AGREEMENT AND ISSUING BANKCARDS ................................................................. 14 DETAILS OF THE EXTERIOR OF THE BANKCARD ....................................................................................................... 14 EXPIRY OF A BANKCARD ....................................................................................................................................... 14 APPLYING FOR A BANKCARD, CONTRACTING ........................................................................................................ -

Business Accounts and Payment Services

Business Accounts and Payment Services Fees and charges and how to minimise them. Terms and conditions, and general information. Effective: 13 September 2021 This booklet sets out the terms and conditions applying to our transaction and Part A: Fees and charges and how to minimise them ���������������������������������������������������6 savings accounts listed in Part A that are available for business customers. Business accounts: Features ������������������������������������������������������������������������������������������������������������������������������������ 10 Business accounts: Everyday banking fees and charges ����������������������������������������������������������������������� 12 Corporate accounts: Features ��������������������������������������������������������������������������������������������������������������������������������� 14 Different accounts have different features. The features that apply to our Corporate accounts: Everyday banking fees and charges ������������������������������������������������������������������� 16 accounts are set out in Part A. Specialist industry accounts – Statutory trust: Features ���������������������������������������������������������������������� 18 Separate terms and conditions apply to other banking services we offer, such as Internet and Phone Banking, Business Banking Online, or any linked Specialist industry accounts – Statutory trust: Everyday banking fees and charges ��������� 20 business lending facility. Specialist industry accounts – Society Cheque Account: Features -

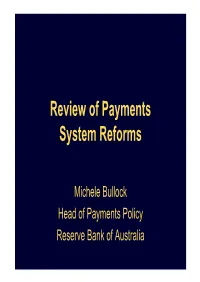

Presentation to Australian Smart Cards Summit 2007: Review of Payments System Reforms

Review of Payments System Reforms Michele Bullock Head of Payments Policy Reserve Bank of Australia Overview 1. Scope of the review 2. What issues are being addressed? 3. Developments since the reforms? 4. Progress on the studies 5. Where to from here? Scope Credit cards EFTPOS Scheme debit American Express/Diners Club BPAY ATMs The Issues Source: The Australian What are the Issues? Effects of the reforms? Alternatives to regulation? Changes to current regulations? Developments In the market? Overseas? Analysis? Non-cash Payments per Capita* Per year No No 60 60 Cheques Credit cards 50 50 Debit cards 40 40 Direct credits 30 30 20 20 Direct debits 10 10 BPAY 0 0 1994 19961998 2000 2002 2004 2006 *Debit and credit card data prior to 2002 have been adjusted for a break in the series due to an expansion in the coverage of the Retail Payments Statistics in 2002. Sources: ABS; APCA; BPAY; RBA Number of Card Payments Year-on-year growth %% 30 30 Credit 20 20 Debit 10 10 0 0 1997 1999 2001 2003 2005 2007 Source: RBA Market Shares of Card Schemes By value of purchases % Bankcard, MasterCard and Visa % 90 90 85 85 % American Express and Diners Club % 15 15 10 10 5 5 2002 2003 2004 2005 2006 2007 Source: RBA Merchants Surcharging Credit Cards* Per cent of surveyed merchants %% 12 12 Very large merchants Large merchants 8 8 Small merchants 4 4 Very small merchants 0 0 Jun 2005 Dec 2005 Jun 2006 Dec 2006 * Very large merchants are those with turnover greater than $340 million, large merchants $20 million to $340 million, small merchants $5 million to $20 million and very small merchants $1 million to $5 million.