How We Will Calculate Your Balance:We Use a Method Called “Average Daily Balance (Including New Purchases)”. Index and When

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Visa's Annual Report

Annual Report 2017 Annual Report 2017 Mission Statement To connect the world through the most innovative, reliable and secure digital payment network that enables individuals, businesses and economies to thrive. Financial Highlights (GAAP) In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $7,199 $6,214 Operating income $9,064 $7, 883 $12,144 Net income $6,328 $5,991 $6,699 Stockholders' equity $29,842 $32,912 $32,760 Diluted class A common stock earnings per share $2.58 $2.48 $2.80 Financial Highlights (ADJUSTED)1 In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $5,060 $6,022 Operating income $9,064 $10,022 $12,336 Net income $6,438 $6,862 $8,335 Diluted class A common stock earnings per share $2.62 $2.84 $3.48 Operational Highlights² 12 months ended September 30 (except where noted) 2015 2016 2017 Total volume, including payments and cash volume³ $7.4 trillion $8.2 trillion $10.2 trillion Payments volume³ $4.9 trillion $5.8 trillion $7.3 trillion Transactions processed on Visa's networks 71.0 billion 83.2 billion 111.2 billion Cards⁴ 2.4 billion 2.5 billion 3.2 billion Stock Performance The accompanying graph and chart compares the cumulative total return on $350 Visa’s common stock with the cumulative total return on Standard & Poor’s 500 Index and the Standard & Poor’s 500 Data Processing Index from September 30, $300 2012 through September 30, 2016. -

Global Payments 2020-30 a Quantium Shift in the Next Decade Australia's Challenge

McLean Roche Consulting Group Global Payments 2020-30 A quantium shift in the next decade Australia’s challenge – to keep up 1 Submission To RBA Payments Boards – Future of Payments – January 2020 McLean Roche Consulting Group AUSTRALIA’S PAYMENT CHALLENGE Australian payments will see more change in the next 10 years than the last 40 years combined. Australia has an expensive US/Anglo legacy based retail payments system which will be challenge by new technology, new data uses, new players and the need to protect consumer rights and data. Consumer retail payments total $975.7 billion in 2019 and will reach $3.2 trillion by 2030. A faster rate of expansion will occur in SME and Corporate payments. Payments are a very high volume, low margin business with even the smallest changes in revenues or margins delivering significant changes in actual dollars. Regulators around the globe will be challenged by forces of change and this requires all regulators and politicians to be aware of the scale of change and ensure the regulatory frame work changes and evolves quickly. 4 MYTHS DOMINATE THE NARRATIVE 1. CASH WILL DISAPPEAR – many including regulators keep predicting the death of cash. While bank notes may disappear, various forms of cash now dominate retail payments in Australia combining to total 71% share. 2. CREDIT CARDS DOMINATE LENDING – consumer credit cards are in decline having peaked 8 years ago. All the leading indicators are falling – average balance, average spend, revolve rate and number of cards. Corporate and Commercial cards are the only growth story. 3. DIGITAL PAYMENTS ARE THE FUTURE – many payment products use the ‘digital’ tag for marketing ‘glint’ however the reality is all payment products using Visa, MasterCard, Amex or eftpos payment networks are not digital. -

Bow Credit Card Agreement

CREDIT CARD AGREEMENT (Personal Accounts) By requesting or accepting any Standard MasterCard, account. If we accept a payment from you in excess of your Standard Visa, Platinum MasterCard, Platinum Visa, outstanding balance, your available Credit Limit will not be Platinum Rewards MasterCard, or Platinum Rewards Visa increased by the amount of the overpayment nor will we be account (individually or collectively called “Credit Card required to authorize transactions for an amount in excess account” or “Account”) with Bank of the West, you agree to of your Credit Limit. be bound by all the terms of this Agreement. In this 3. Temporary Reduction of Credit Limit. Merchants, Agreement, the words “you” or “your” mean everyone who such as car rental companies and hotels, may request prior has requested or accepted a Credit Card account with us. credit approval from us for an estimated amount of your The words “we,” “us,” “our,” or “Bank” mean Bank of the Purchases, even if you ultimately do not pay by credit. If our West. If you do not accept this Agreement, you must notify approval is granted, your available Credit Limit will us in writing within 5 days after receipt. Use of your card or temporarily be reduced by the amount authorized by us. If any feature (including a balance transfer) of your Credit you do not ultimately use your Credit Card account to pay Card Agreement shall constitute acceptance of this for your Purchases or if the actual amount of Purchases Agreement. posted to your Credit Card account varies from the 1. Use. Your Standard MasterCard, Standard Visa, estimated amount approved by us, it is the responsibility of Platinum MasterCard, Platinum Visa, Platinum Rewards the merchant, not us, to cancel the prior credit approval MasterCard, or Platinum Rewards Visa card (individually or based on the estimated amount. -

General Contracting Terms and Conditions

K&H Bank Zrt. H–1095 Budapest, Lechner Ödön fasor 9. phone: +(36 1) 328 9000 fax: +(36 1) 328 9696 www.kh.hu • [email protected] GENERAL CONTRACTING TERMS AND CONDITIONS FOR BANKCARD AND CREDIT CARD SERVICES Effective dates: December 13, 2017, January 13, 2018 and February 13, 2018 Date of announcement: December 13, 2017 These GCTC are amended pursuant to Sections XIX.1 and XIX.2 hereof with the scope and effective dates specified below. Amended provisions in Section X.6 – effective date: December 13, 2017 (the effective date is referenced in the footnotes as well) Amendments due to amended legal regulations on payment services, or required for more precise and accurate wording of these GTC – effective date: January 13, 2018 Amended provisions in Sections IX.2 and XV.8 – effective date: February 13, 2018 (provisions becoming effective as of February 13, 2018 are specified also in the footnotes. TABLE OF CONTENTS I. TERMS: ................................................................................................................................................... 4 II. BANKCARD AGREEMENT AND ISSUING BANKCARDS ................................................................. 14 DETAILS OF THE EXTERIOR OF THE BANKCARD ....................................................................................................... 14 EXPIRY OF A BANKCARD ....................................................................................................................................... 14 APPLYING FOR A BANKCARD, CONTRACTING ........................................................................................................ -

Presentation to Australian Smart Cards Summit 2007: Review of Payments System Reforms

Review of Payments System Reforms Michele Bullock Head of Payments Policy Reserve Bank of Australia Overview 1. Scope of the review 2. What issues are being addressed? 3. Developments since the reforms? 4. Progress on the studies 5. Where to from here? Scope Credit cards EFTPOS Scheme debit American Express/Diners Club BPAY ATMs The Issues Source: The Australian What are the Issues? Effects of the reforms? Alternatives to regulation? Changes to current regulations? Developments In the market? Overseas? Analysis? Non-cash Payments per Capita* Per year No No 60 60 Cheques Credit cards 50 50 Debit cards 40 40 Direct credits 30 30 20 20 Direct debits 10 10 BPAY 0 0 1994 19961998 2000 2002 2004 2006 *Debit and credit card data prior to 2002 have been adjusted for a break in the series due to an expansion in the coverage of the Retail Payments Statistics in 2002. Sources: ABS; APCA; BPAY; RBA Number of Card Payments Year-on-year growth %% 30 30 Credit 20 20 Debit 10 10 0 0 1997 1999 2001 2003 2005 2007 Source: RBA Market Shares of Card Schemes By value of purchases % Bankcard, MasterCard and Visa % 90 90 85 85 % American Express and Diners Club % 15 15 10 10 5 5 2002 2003 2004 2005 2006 2007 Source: RBA Merchants Surcharging Credit Cards* Per cent of surveyed merchants %% 12 12 Very large merchants Large merchants 8 8 Small merchants 4 4 Very small merchants 0 0 Jun 2005 Dec 2005 Jun 2006 Dec 2006 * Very large merchants are those with turnover greater than $340 million, large merchants $20 million to $340 million, small merchants $5 million to $20 million and very small merchants $1 million to $5 million. -

Visa Inc. V. Stoumbos

No. 15-____ IN THE Supreme Court of the United States VISA INC., ET AL., Petitioners, v. MARY STOUMBOS, ET AL., Respondents. On Petition for a Writ of Certiorari to the United States Court of Appeals for the District of Columbia Circuit PETITION FOR A WRIT OF CERTIORARI KENNETH A. GALLO ANTHONY J. FRANZE PAUL, WEISS, RIFKIND, Counsel of Record WHARTON & MARK R. MERLEY GARRISON LLP MATTHEW A. EISENSTEIN 2001 K STREET, NW ARNOLD & PORTER LLP WASHINGTON, DC 20006 601 MASSACHUSETTS AVENUE, (202) 223-7300 NW [email protected] WASHINGTON, DC 20001 (202) 942-5000 Counsel for Petitioners [email protected] MasterCard Incorporated and MasterCard International Counsel for Petitioners Visa Inc., Incorporated Visa U.S.A. Inc., Visa Interna- tional Service Association, and Plus System, Inc. i QUESTION PRESENTED Whether allegations that members of a business as- sociation agreed to adhere to the association’s rules and possess governance rights in the association, without more, are sufficient to plead the element of conspiracy in violation of Section 1 of the Sherman Act, 15 U.S.C. § 1, as the Court of Appeals held below, or are insufficient, as the Third, Fourth, and Ninth Circuits have held. ii PARTIES TO THE PROCEEDINGS Pursuant to Rule 14.1(b), the following list identi- fies all of the parties appearing here and before the United States Court of Appeals for the D.C. Circuit. The petitioners here and appellees below in both Stoumbos v. Visa Inc., et al., No. 1:11-cv-01882 (D.D.C.) (“Stoumbos”) and National ATM Council, et al. -

General Contracting Terms and Conditions

K&H Bank Zrt. H–1095 Budapest, Lechner Ödön fasor 9. phone: (36 1) 328 9000 fax: (36 1) 328 9696 www.kh.hu • [email protected] GENERAL CONTRACTING TERMS AND CONDITIONS FOR BANKCARD AND CREDIT CARD SERVICES Effective as of May 4, 2015 The GCTC has been amended pursuant to section XVII.2.a) herein in order to accommodate new services and to clarify regulations as necessary. TABLE OF CONTENTS TABLE OF CONTENTS .......................................................................................................................... 2 I. TERMS: ...................................................................................................................................... 3 II. BANKCARD AGREEMENT AND ISSUING THE BANKCARD ................................................ 9 III. HANDING OVER THE BANKCARD ........................................................................................ 10 IV. PIN (PERSONAL IDENTIFICATION NUMBER) CODE .......................................................... 13 V. ADDITIONAL (OR CO-) CARDS AND BUSINESS CARDS FOR ORGANISATIONS ........... 13 VI. CREDIT CARDS ....................................................................................................................... 14 VII. BANKCARD USE ..................................................................................................................... 19 VIII. BANKCARD USAGE AUTHORISATION, FINANCIAL COVERAGE ..................................... 24 IX. FEES, EXPENSES, COMMISSIONS AND INTEREST .......................................................... -

Bankcard Agreement for United Cardholders G17222 1

BANKCARD AGREEMENT FOR UNITED CARDHOLDERS G17222 1. DEFINITIONS – In this Agreement, the word “Card” means a single Card or two or more Cards we have issued applicable local, state or federal law. You agree to indemnify and save the Bank harmless from any liability the Bank may pursuant to this Agreement. The words “you” and “yours” mean each applicant or person to whom we have issued a incur or damage it may suffer by reason of use of the Card for any such improper purpose. Card. The words “us,” “our,” “we” and the “Bank” mean United Bank. The word “Account” means the MasterCard 14. CURRENCY CONVERSION – The exchange rate between the transaction currency and the billing currency used for or VISA Account for which you were issued a Card or Cards and Checks imprinted with your name and Account number. processing international transactions is a rate selected by Visa and MasterCard from a range of rates available in wholesale “Authorized User” means any person whom you have given permission to use your Account. If your spouse, or anyone currency markets for the applicable central processing date, which may vary from the rate that Visa and MasterCard itself else, desires the same type of credit card to be issued in his or her name, he or she must sign a credit card application receives or the government-mandated rate in effect for the applicable central processing date, plus 2 percent. requesting the same. “Checks” mean the checks provided to you with your Account, should your Account type provide 15. USE OF ACCOUNT FOR QUASI-CASH TRANSACTIONS – The Account may be utilized for payment of certain quasi-cash for Checks. -

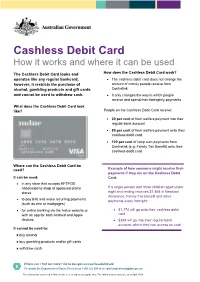

Cashless Debit Card How Does It Work

Cashless Debit Card How it works and where it can be used The Cashless Debit Card looks and How does the Cashless Debit Card work? operates like any regular bankcard, The cashless debit card does not change the however, it restricts the purchase of amount of money people receive from alcohol, gambling products and gift cards Centrelink and cannot be used to withdraw cash. It only changes the way in which people receive and spend their fortnightly payments What does the Cashless Debit Card look like? People on the Cashless Debit Card receive: 20 per cent of their welfare payment into their regular bank account 80 per cent of their welfare payment onto their cashless debit card 100 per cent of lump sum payments from Centrelink (e.g. Family Tax Benefit) onto their cashless debit card Where can the Cashless Debit Card be used? Example of how someone might receive their payments if they are on the Cashless Debit It can be used: Card: in any store that accepts EFTPOS nationwide to shop at approved online If a single person with three children aged under stores eight and renting receives $1,468 in Newstart Allowance, Family Tax Benefit and other to pay bills and make recurring payments payments every fortnight: (such as rent or mortgages) for online banking via the Indue website or $1,174 will go onto their cashless debit with an app for both Android and Apple card devices $294 will go into their regular bank account, which they can access as cash It cannot be used to: x buy alcohol x buy gambling products and/or gift cards x withdraw cash Where can I find out more? Go to dss.gov.au/cashlessdebitcard Or contact the Department of Social Services on 1800 252 604 or at [email protected] The information contained in this fact sheet is intended as a guide only. -

National Bankcard Melville, NY 11747 C R E D I T C a R D P R O C E S S I N G S O L U T I O N S Tel: (800) 991-2291 Fax: (800) 991-5591

538 Broadhollow Rd. Suite 213 National Bankcard Melville, NY 11747 C R E D I T C A R D P R O C E S S I N G S O L U T I O N S Tel: (800) 991-2291 Fax: (800) 991-5591 MERCHANT SERVICES PROGRAM TERMS AND CONDITIONS (PROGRAM GUIDE) IMPORTANT: PLEASE READ CAREFULLY AND RETAIN THIS DOCUMENT IN YOUR RECORDS AS IT FORMS PART OF YOUR MERCHANT PROCESSING AGREEMENT. PREFACE Thank You for selecting us for Your payment processing needs. Accepting numerous payment options provides a convenience to Your customers, increases Your customers’ ability to make purchases at Your establishment, and helps speed payment to Your account. Your Merchant Processing Application will indicate the types of payments and Services You have elected to accept. These Program Terms and Conditions (“the Program Guide”) presents terms governing the acceptance of Visa®, MasterCard®, Discover® Network Credit Card, Non-PIN Debit Card payments, and American Express® Card transactions related to Payment Services, and applicable Non-Bank Services. This Program Guide also sets forth general terms with respect to all Services to be performed whether or not Payment Services. This Program Guide, Your Merchant Processing Application and the schedules thereto (collectively, the “Agreement”), contains the terms and conditions under which We and/or Bank and/or third parties will provide the Services to You, which include the Payment Services and any Additional Services. We will not accept any alterations or strike-outs to the Agreement and, if made, any such alterations or strike-outs shall not apply. Please read this Program Guide completely as it contains important information. -

Card Processing Guide - MOI 2015.Qxp GP 07/09/2015 17:45 Page 1

JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 1 CARD PROCESSING GUIDE MERCHANT OPERATING INSTRUCTIONS SERVICE. DRIVEN. COMMERCE JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 2 CONTENTS SECTION PAGE Welcome 1 Global Payments 1 About This Document 1 An Introduction To Card Processing 3 The Anatomy Of A Card Payment 3 Transaction Types 4 Risk Awareness 4 Card Present (CP) Transactions 9 Cardholder Verified By PIN 9 Cardholder Verified By Signature 9 Cardholder Verified By PIN And Signature 9 Contactless Card Payments 10 Checking Cards 10 Examples Of Card Logos 13 Examples Of Cards And Card Features 14 Accepting Cards Using An Electronic Terminal 18 Authorisation 19 ‘Code 10’ Calls 24 Account Verification/Status Checks 25 Recovered Cards 26 Refunds 27 How To Submit Your Electronic Terminal Transactions 29 Using Fallback Paper Vouchers 30 Card Not Present (CNP) Transactions 33 Accepting Mail And Telephone Orders 33 Accepting Internet Orders 34 Authorisation Of CNP Transactions 36 Confirming CNP Orders 38 Delivering Goods 39 Collection Of Goods 39 Special Transaction Types 40 Bureau de Change 40 Dynamic Currency Conversion (DCC) 41 Foreign Currency Transactions 41 Gratuities 42 Hotel And Car Rental Transactions 42 Prepayments/Deposits/Instalments 44 Purchase With Cashback 44 Recurring Transactions 45 Global Iris 48 HomeCurrencyPay 50 An Introduction To HomeCurrencyPay 50 JM3150_Card Processing Guide - MOI 2015.qxp_GP 07/09/2015 17:45 Page 3 SECTION PAGE Card Present (CP) HomeCurrencyPay Transactions -

Cover Art-Outside

ANNUAL REPORT 2002 Cabcharge Australia Limited ABN 99 001 958 390 Contents 2 Results in Brief 4 Chairman’s Report 5 Highlights 10 Board of Directors 11 Annual Financial Report Annual General Meeting The 2002 Annual General Meeting of Shareholders of Cabcharge Australia Limited will be held at The Westin Sydney, Heritage Ballroom, No.1 Martin Place, Sydney NSW 2000 on Tuesday, 12 November 2002 at 11am. Cabcharge’s merger with Combined Communications Network (CCN) in January 2002 is already proving a success. CCN was the largest single contributor to the substantial increase in both revenue and profits during this turbulent year for businesses. Cabcharge now has an integrated array of state-of-the-art services for the Taxi Industry. Cabcharge remains committed to be the Australian leader in developing and applying new ideas and improved technology for even better efficiencies and service to customers. With increasing population and affluence likely to have a positive impact on the demand for taxis, Cabcharge is ideally placed to apply its expertise into new and exciting areas in the future. 1 RESULTS IN BRIEF * Pro-forma Actuals 2002 2002 2001 2000 Total revenue ($m) 609.5 588.1 545.4 481.1 Cabcharge operations 572.0 572.0 545.4 481.1 Communications (CCN) 37.5 16.1 - - Profit after tax ($m) 17.5 16.1 12.5 11.0 Cabcharge operations 14.0 14.0 12.5 11.0 Communications (CCN) 3.5 2.1 - - Earnings before interest, tax, depreciation and amortisation (EBITDA - $m) 29.3 25.7 20.2 16.9 Cabcharge operations 22.5 22.5 20.2 16.9 Communications (CCN) 6.8 3.2 - - Earnings per share (cents) 14.7 11.5 12.1 Dividend per share (cents) 10.0 8.0 7.5 Net tangible assets per share (cents) 90.4 85.8 80.4 * Pro-forma 2002 numbers are prepared on the hypothetical basis that CCN became a subsidiary of Cabcharge on 1 July 2001.