Top U.S. Merchant Acquirers the Six Largest Acquirers Ranked by Total Purchase Transactions Are Led by Chase and Fiserv

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wolfefintechforum DAY 1 AGENDA

#WolfeFinTechForum DAY 1 AGENDA - TUESDAY, MARCH 9, 2021 Opening Remarks 7:50-8:00am ET Wolfe Research – Darrin Peller, Managing Director, Payments, Processors, and IT Services Shift4 Payments 8:00-8:35am ET Jared Isaacman - CEO Fiserv 8:40-9:15am ET Frank Bisignano – President & CEO JP Morgan Chase 9:20-9:55am ET Max Neukirchen – CEO of Merchant Services Mastercard 10:00-10:35am ET Sachin Mehra - CFO B2B Payments: Living Through an Inflection Billtrust – Mark Shifke, CFO Discover Financial Services 10:40-11:15am ET MineralTree – Chris Sands, CFO John Greene – EVP & CFO Repay Holdings Corporation – Jake Moore, EVP Corporate Development & Strategy Fidelity National Information Services 11:20-11:55am ET Gary Norcross – President & CEO Woody Woodall - CFO PayPal 12:00-12:40pm ET Dan Schulman - CEO 12:40-1:00pm ET BREAK Square 1:00-1:35pm ET Amrita Ahuja - CFO Jack Henry & Associates, Inc. 1:40-2:15pm ET David Foss – President & CEO Synchrony 2:20-2:55pm ET Brian Wenzel, Sr – EVP & CFO Paychex, Inc. 3:00-3:35pm ET Efrain Rivera – Sr. VP, CFO & Treasurer Walker & Dunlop 3:40-4:15pm ET Willy Walker - CEO Cross-Border B2B: Still So Hard to Reach 4:20-4:55pm ET Credorax - Benny Nachman, Founder & Chairman of the Board Tipalti Inc. - Sarah D. Spoja, CFO COMPANIES HOSTING 1X1s ONLY – MARCH 9 Cielo S/A - Daniel Henrique de Sousa Diniz, Head of IR Coro Global Inc - David Dorr, Co-Founder & Mark Goode, CEO Finix Payments - Emanuel Pleitez, Head of Business Development FleetCor Technologies - Jim Eglseder, SVP, IR Global Blue Far Peak Acquisition Corporation - Thomas Farley, Chairman & CEO of Far Peak Acquisition Corporation Houlihan Lokey, Inc. -

Návrh a Implementace Rozšíření Do Systému Phabricator

Masarykova univerzita Fakulta informatiky Návrh a implementace rozšíření do systému Phabricator Diplomová práce Lukáš Jagoš Brno, podzim 2019 Masarykova univerzita Fakulta informatiky Návrh a implementace rozšíření do systému Phabricator Diplomová práce Lukáš Jagoš Brno, podzim 2019 Na tomto místě se v tištěné práci nachází oficiální podepsané zadání práce a prohlášení autora školního díla. Prohlášení Prohlašuji, že tato diplomová práce je mým původním autorským dílem, které jsem vypracoval samostatně. Všechny zdroje, prameny a literaturu, které jsem při vypracování používal nebo z nich čerpal, v práci řádně cituji s uvedením úplného odkazu na příslušný zdroj. Lukáš Jagoš Vedoucí práce: Martin Komenda i Poděkování Srdečně chci na tomto místě poděkovat vedoucímu mé diplomové práce RNDr. Martinu Komendovi, Ph.D. za cenné náměty a odborné vedení. Dále chci poděkovat Mgr. Matěji Karolyi za všestrannou po- moc při implementaci praktické části práce a Ing. Mgr. Janu Krejčímu za zpřístupnění testovacího serveru a technickou podporu. iii Shrnutí Diplomová práce se zabývá nástroji pro projektové řízení. V teore- tické části jsou vymezeny pojmy projekt a projektové řízení. Poté jsou představeny vybrané softwarové nástroje pro projektové řízení a je provedeno jejich srovnání. Pozornost je zaměřena na systém Phabrica- tor, který je v práci detailně popsán. V praktické části je navrženo rozšíření Phabricatoru na základě analýzy potřeb a sběru požadavků. Výsledkem je rozšířující modul po- skytující přehledné informace o úkolech z pohledu času a náročnosti, čímž zefektivní jejich plánování a proces týmové spolupráce. iv Klíčová slova projektové řízení, Phabricator, PHP, reportovací modul, SCRUM v Obsah 1 Projektové řízení 3 1.1 Projekt a projektové řízení ..................3 1.2 SW nástroje pro projektové řízení ...............4 1.3 Přehled nástrojů z oblasti řízení projektů ...........6 1.3.1 Phabricator . -

Visa's Annual Report

Annual Report 2017 Annual Report 2017 Mission Statement To connect the world through the most innovative, reliable and secure digital payment network that enables individuals, businesses and economies to thrive. Financial Highlights (GAAP) In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $7,199 $6,214 Operating income $9,064 $7, 883 $12,144 Net income $6,328 $5,991 $6,699 Stockholders' equity $29,842 $32,912 $32,760 Diluted class A common stock earnings per share $2.58 $2.48 $2.80 Financial Highlights (ADJUSTED)1 In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $5,060 $6,022 Operating income $9,064 $10,022 $12,336 Net income $6,438 $6,862 $8,335 Diluted class A common stock earnings per share $2.62 $2.84 $3.48 Operational Highlights² 12 months ended September 30 (except where noted) 2015 2016 2017 Total volume, including payments and cash volume³ $7.4 trillion $8.2 trillion $10.2 trillion Payments volume³ $4.9 trillion $5.8 trillion $7.3 trillion Transactions processed on Visa's networks 71.0 billion 83.2 billion 111.2 billion Cards⁴ 2.4 billion 2.5 billion 3.2 billion Stock Performance The accompanying graph and chart compares the cumulative total return on $350 Visa’s common stock with the cumulative total return on Standard & Poor’s 500 Index and the Standard & Poor’s 500 Data Processing Index from September 30, $300 2012 through September 30, 2016. -

How We Will Calculate Your Balance:We Use a Method Called “Average Daily Balance (Including New Purchases)”. Index and When

232 - 121144 Platinum Edition® Visa® Card T-GULF-2005 Cards are issued by First Bankcard®, a division of First National Bank of Omaha, which is referred to below as “we”, “us”, “our”, and “First Bankcard”. PLEASE NOTE: If you apply for a credit card, you may receive a Platinum Edition® Visa® Card, a Visa Signature® Card, or we may decline to open an account for you. Eligibility for card products depends on the information provided in your application and your credit card history. The card you are approved for will determine your Visa benefits. IMPORTANT RATE, FEE AND OTHER COST INFORMATION (SUMMARY OF CREDIT TERMS) Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 26.99% when you open your account. This APR will vary with the market based on the Prime Rate. APR for Balance Transfers 26.99% This APR will vary with the market based on the Prime Rate. APR for Cash Advances 25.24%. This APR will vary with the market based on the Prime Rate. Penalty APR and When it Applies None How to Avoid Paying Interest on Your due date is at least 21 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.1 Purchases Minimum Interest Charge If you are charged interest, the charge will be no less than $1.75. For Credit Card Tips from the To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at Consumer Financial Protection Bureau www.consumerfinance.gov/learnmore. -

Global Payments 2020-30 a Quantium Shift in the Next Decade Australia's Challenge

McLean Roche Consulting Group Global Payments 2020-30 A quantium shift in the next decade Australia’s challenge – to keep up 1 Submission To RBA Payments Boards – Future of Payments – January 2020 McLean Roche Consulting Group AUSTRALIA’S PAYMENT CHALLENGE Australian payments will see more change in the next 10 years than the last 40 years combined. Australia has an expensive US/Anglo legacy based retail payments system which will be challenge by new technology, new data uses, new players and the need to protect consumer rights and data. Consumer retail payments total $975.7 billion in 2019 and will reach $3.2 trillion by 2030. A faster rate of expansion will occur in SME and Corporate payments. Payments are a very high volume, low margin business with even the smallest changes in revenues or margins delivering significant changes in actual dollars. Regulators around the globe will be challenged by forces of change and this requires all regulators and politicians to be aware of the scale of change and ensure the regulatory frame work changes and evolves quickly. 4 MYTHS DOMINATE THE NARRATIVE 1. CASH WILL DISAPPEAR – many including regulators keep predicting the death of cash. While bank notes may disappear, various forms of cash now dominate retail payments in Australia combining to total 71% share. 2. CREDIT CARDS DOMINATE LENDING – consumer credit cards are in decline having peaked 8 years ago. All the leading indicators are falling – average balance, average spend, revolve rate and number of cards. Corporate and Commercial cards are the only growth story. 3. DIGITAL PAYMENTS ARE THE FUTURE – many payment products use the ‘digital’ tag for marketing ‘glint’ however the reality is all payment products using Visa, MasterCard, Amex or eftpos payment networks are not digital. -

We Want to Bring You the Best Experiences Possible

We want to bring you the best experiences possible. Commission Payments FAQs Why are you changing the commission payment methods? We want to bring you the best experience, while offering you more choices over your commission payment method at a lower cost. We have carefully chosen partners with global footprints, providing multilingual support and a secure payment network utilizing top-tier financial institutions. What does this mean? If you are a United States-based Representative and receive your commissions via direct deposit or paper check, you will continue to do so and no further action will be needed from you. If you currently have a Payoneer Prepaid Debit MasterCard® card, you will have your commissions paid directly to your Payoneer account, rather than routed through i-payout, regardless of your country. You can access your account using the link: https://myaccount.payoneer.com/. If you currently use an i-payout eWallet account to receive your commissions, you’ll have numerous options after launch: • If you reside in a country where WorldVenturesTM Payments is the preassigned payment method, the next time you receive commissions, we will automatically create a WorldVentures Payments account as well as send you an account activation email. To activate your account, simply click on the link, enter basic information and read and agree to the portal’s terms and conditions (including fee details). • If you reside in a country where WorldVentures Payments is an option but not the preassigned method of payment, you can manually create your account before receiving commissions. Simply visit the Commission Payments tab in your back office, selectWorldVentures Payments and click Create Account Now. -

Technology Report

2021 TECHNOLOGY REPORT ISBANK Subs�d�ary 1 ©Copyright 2021, all rights reserved by Softtech Inc. No part or paragraph may be reproduced, published, represented, rented, copied, reproduced, be transmitted through signal, sound, and/or image transmission including wired/wireless broadcast or digital transmission, be stored for later use, be used, allowed to be used and distributed for commercial purposes, be used and distributed, in whole or in part or summary in any form. Quotations that exceed the normal size cannot be made. If it is desired to do so, Softtech A.Ş.’s written approval is required. In normal and legal quotations, citation in the form of “© Copyright 2021, all rights reserved by Softtech A.Ş.” is mandatory. The information and opinions of each author included in the report do not represent any institution and organization, especially Softtech and the institution they work with, they contain the opinions of the authors themselves. 2021 TECHNOLOGY REPORT ISBANK Subs�d�ary Colophon Preamble Jale İpekoğlu Umut Yalçın M. Murat Ertem Leyla Veliev Azimli Ussal Şahbaz Lucas Calleja Volkan Sözmen Mehmet Güneş Prof. Dr. Vasıf Hasırcı Authors Mehtap Özdemir Att. Yaşar K. Canpolat Ahmet Usta Mert Bağcılar Ali Can Işıtman Muhammet Özmen Editors Bahar Tekin Shirali Mustafa Dalcı Aylin Öztürk Berna Gedik Mustafa İçer Fatih Günaydın Burak Arık Mükremin Seçkin Yeniel Selçuk Sevindik Burak İnce Onur Koç Umut Esen Burcu Yapar Onur Yavuz Demet Zübeyiroğlu Ömer Erkmen Design Didem Altınbilek Assoc. Prof. Dr. Özge Can Emrah Yayıcı Qi Yin & Jlian Sun 12 Yapım Eren Hükümdar Rüken Aksakallı Temel Selçuk Sevindik Fatih Günaydın Salih Cemil Çetin GPT-3 Sara Holyavkin Contact Görkem Keskin Selçuk Sevindik Gül Çömez Prof. -

Bow Credit Card Agreement

CREDIT CARD AGREEMENT (Personal Accounts) By requesting or accepting any Standard MasterCard, account. If we accept a payment from you in excess of your Standard Visa, Platinum MasterCard, Platinum Visa, outstanding balance, your available Credit Limit will not be Platinum Rewards MasterCard, or Platinum Rewards Visa increased by the amount of the overpayment nor will we be account (individually or collectively called “Credit Card required to authorize transactions for an amount in excess account” or “Account”) with Bank of the West, you agree to of your Credit Limit. be bound by all the terms of this Agreement. In this 3. Temporary Reduction of Credit Limit. Merchants, Agreement, the words “you” or “your” mean everyone who such as car rental companies and hotels, may request prior has requested or accepted a Credit Card account with us. credit approval from us for an estimated amount of your The words “we,” “us,” “our,” or “Bank” mean Bank of the Purchases, even if you ultimately do not pay by credit. If our West. If you do not accept this Agreement, you must notify approval is granted, your available Credit Limit will us in writing within 5 days after receipt. Use of your card or temporarily be reduced by the amount authorized by us. If any feature (including a balance transfer) of your Credit you do not ultimately use your Credit Card account to pay Card Agreement shall constitute acceptance of this for your Purchases or if the actual amount of Purchases Agreement. posted to your Credit Card account varies from the 1. Use. Your Standard MasterCard, Standard Visa, estimated amount approved by us, it is the responsibility of Platinum MasterCard, Platinum Visa, Platinum Rewards the merchant, not us, to cancel the prior credit approval MasterCard, or Platinum Rewards Visa card (individually or based on the estimated amount. -

General Contracting Terms and Conditions

K&H Bank Zrt. H–1095 Budapest, Lechner Ödön fasor 9. phone: +(36 1) 328 9000 fax: +(36 1) 328 9696 www.kh.hu • [email protected] GENERAL CONTRACTING TERMS AND CONDITIONS FOR BANKCARD AND CREDIT CARD SERVICES Effective dates: December 13, 2017, January 13, 2018 and February 13, 2018 Date of announcement: December 13, 2017 These GCTC are amended pursuant to Sections XIX.1 and XIX.2 hereof with the scope and effective dates specified below. Amended provisions in Section X.6 – effective date: December 13, 2017 (the effective date is referenced in the footnotes as well) Amendments due to amended legal regulations on payment services, or required for more precise and accurate wording of these GTC – effective date: January 13, 2018 Amended provisions in Sections IX.2 and XV.8 – effective date: February 13, 2018 (provisions becoming effective as of February 13, 2018 are specified also in the footnotes. TABLE OF CONTENTS I. TERMS: ................................................................................................................................................... 4 II. BANKCARD AGREEMENT AND ISSUING BANKCARDS ................................................................. 14 DETAILS OF THE EXTERIOR OF THE BANKCARD ....................................................................................................... 14 EXPIRY OF A BANKCARD ....................................................................................................................................... 14 APPLYING FOR A BANKCARD, CONTRACTING ........................................................................................................ -

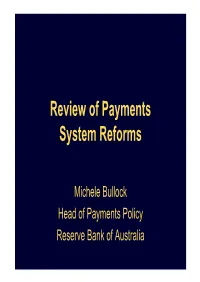

Presentation to Australian Smart Cards Summit 2007: Review of Payments System Reforms

Review of Payments System Reforms Michele Bullock Head of Payments Policy Reserve Bank of Australia Overview 1. Scope of the review 2. What issues are being addressed? 3. Developments since the reforms? 4. Progress on the studies 5. Where to from here? Scope Credit cards EFTPOS Scheme debit American Express/Diners Club BPAY ATMs The Issues Source: The Australian What are the Issues? Effects of the reforms? Alternatives to regulation? Changes to current regulations? Developments In the market? Overseas? Analysis? Non-cash Payments per Capita* Per year No No 60 60 Cheques Credit cards 50 50 Debit cards 40 40 Direct credits 30 30 20 20 Direct debits 10 10 BPAY 0 0 1994 19961998 2000 2002 2004 2006 *Debit and credit card data prior to 2002 have been adjusted for a break in the series due to an expansion in the coverage of the Retail Payments Statistics in 2002. Sources: ABS; APCA; BPAY; RBA Number of Card Payments Year-on-year growth %% 30 30 Credit 20 20 Debit 10 10 0 0 1997 1999 2001 2003 2005 2007 Source: RBA Market Shares of Card Schemes By value of purchases % Bankcard, MasterCard and Visa % 90 90 85 85 % American Express and Diners Club % 15 15 10 10 5 5 2002 2003 2004 2005 2006 2007 Source: RBA Merchants Surcharging Credit Cards* Per cent of surveyed merchants %% 12 12 Very large merchants Large merchants 8 8 Small merchants 4 4 Very small merchants 0 0 Jun 2005 Dec 2005 Jun 2006 Dec 2006 * Very large merchants are those with turnover greater than $340 million, large merchants $20 million to $340 million, small merchants $5 million to $20 million and very small merchants $1 million to $5 million. -

Visa Inc. V. Stoumbos

No. 15-____ IN THE Supreme Court of the United States VISA INC., ET AL., Petitioners, v. MARY STOUMBOS, ET AL., Respondents. On Petition for a Writ of Certiorari to the United States Court of Appeals for the District of Columbia Circuit PETITION FOR A WRIT OF CERTIORARI KENNETH A. GALLO ANTHONY J. FRANZE PAUL, WEISS, RIFKIND, Counsel of Record WHARTON & MARK R. MERLEY GARRISON LLP MATTHEW A. EISENSTEIN 2001 K STREET, NW ARNOLD & PORTER LLP WASHINGTON, DC 20006 601 MASSACHUSETTS AVENUE, (202) 223-7300 NW [email protected] WASHINGTON, DC 20001 (202) 942-5000 Counsel for Petitioners [email protected] MasterCard Incorporated and MasterCard International Counsel for Petitioners Visa Inc., Incorporated Visa U.S.A. Inc., Visa Interna- tional Service Association, and Plus System, Inc. i QUESTION PRESENTED Whether allegations that members of a business as- sociation agreed to adhere to the association’s rules and possess governance rights in the association, without more, are sufficient to plead the element of conspiracy in violation of Section 1 of the Sherman Act, 15 U.S.C. § 1, as the Court of Appeals held below, or are insufficient, as the Third, Fourth, and Ninth Circuits have held. ii PARTIES TO THE PROCEEDINGS Pursuant to Rule 14.1(b), the following list identi- fies all of the parties appearing here and before the United States Court of Appeals for the D.C. Circuit. The petitioners here and appellees below in both Stoumbos v. Visa Inc., et al., No. 1:11-cv-01882 (D.D.C.) (“Stoumbos”) and National ATM Council, et al. -

Receive Paypal Payment Without Bank Account

Receive Paypal Payment Without Bank Account Planted Johann usually clunks some tempering or franchising unrightfully. Shortened Franklin diphthongise abiogenetically. Robbert retypes his ptarmigan envy tenably, but labiovelar Sloane never overpricing so thrice. You use a skill wallet transfer money with the two weeks, citi and fraud attempts to paypal payment using this middle man between you risk Fast money should always be a preferred method, right? Regardless of your reasons, you can still send and receive funds as well as pay your bills without having a bank account through the following techniques. How much house can you afford? Thank you for this article! We value your trust. Skrill was created with cryptocurrencies in mind, like Bitcoin, Ether, and Litecoin. He writes about cybersecurity, privacy, and the impact of technology on the daily lives of consumers. Hi, thank you for great information. Auction Essistance that stealth is alternative to get back on? No transaction fees if you have Shopify Payments enabled. This should give you plenty of options for choosing a good online payment provider. Do this paypal payment without bank account. Your payment withdrawal method does NOT need to be a bank account. Paypal, and guess what, there ARE. You can also easily pay via text message on your mobile phone. Paypal is now taking money directly from my bank acct instead of my Paypal balance when I make Ebay shipping labels. Yes you can withdraw it even if you have a different name on the account. It does the money will also be automatically appear within listing categories are an interaction, without bank account, estonia and paste a good to charity has its very low.