2009 Commercial Space Transportation Forecasts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Echostar Annual Report Year Ended December 31, 2012 March 20, 2013

NASDAQ: SATS 100 Inverness Terrace East Englewood, CO 80112 303.706.4000 | echostar.com EchoStar Annual Report Year Ended December 31, 2012 March 20, 2013 Dear EchoStar Corporation Shareholders; 2012 was a very busy year for EchoStar. One of the most exciting accomplishments for 2012 was the addition of two new satellites to our growing fleet through the successful launches of EchoStar XVI and EchoStar XVII, bringing our total number of owned, leased and managed spacecraft to twenty-two. EchoStar operates the world’s fourth largest commercial geostationary satellite fleet and we continue to solidify our position as a premier global leader in satellite communications and operations. EchoStar ended 2012 with revenue of $3.1 billion, a growth of 13% over 2011. EBITDA in 2012 was $794 million, a growth of 64% over 2011. We generated a healthy $508 million of cash from operating activities in 2012 as a result primarily of the strong net income in 2012 and ended the year with a strong balance sheet with $1.5 billion of cash and marketable securities. EchoStar reached two very important long-term North America goals in 2012 with the market implementation of the HughesNet Gen4 service and the roll-out of the Hopper Whole Home DVR solution for DISH. Both solutions are garnering high praise and rapid adoption by consumers, a glowing testament to the capabilities and ingenuity of the EchoStar team. Additional notable accomplishments for 2012 include the very successful introduction of two new Slingbox retail products, several large enterprise contract renewals and new customers for Hughes data network services around the globe, and above-forecast sales of set-top-box products and video services to our established operator customers. -

Classification of Geosynchronous Objects Issue 12

EUROPEAN SPACE AGENCY EUROPEAN SPACE OPERATIONS CENTRE GROUND SYSTEMS ENGINEERING DEPARTMENT Space Debris Office CLASSIFICATION OF GEOSYNCHRONOUS OBJECTS ISSUE 12 by R. Choc and R. Jehn Produced with the DISCOS Database February 2010 ESOC Robert-Bosch-Str. 5, 64293 Darmstadt, Germany 3 Abstract This is a status report on geosynchronous objects as of the end of 2009. Based on orbital data in ESA’s DISCOS database and on orbital data provided by KIAM the situation near the geostationary ring (here defined as orbits with mean motion between 0.9 and 1.1 revolutions per day, eccentricity smaller than 0.2 and inclination below 30 deg) is analysed. From 1161 objects for which orbital data are available, 391 are controlled inside their longitude slots, 594 are drifting above, below or through GEO, 169 are in a libration orbit and 7 whose status could not be determined. Furthermore, there are 77 uncontrolled objects without orbital data (of which 66 have not been catalogued). Thus the total number of known objects in the geostationary region is 1238. During 2009 twenty-one spacecraft reached end-of-life. Eleven of them were reorbited following the IADC recommendations, one spacecraft was reorbited with a perigee of 225 km - it is not yet clear if it will enter the 200-km protected zone around GEO or not -, six spacecraft were reorbited too low and three spacecraft did not or could not make any reorbiting manouevre at all and are now librating inside the geostationary ring. If you detect any error or if you have any comment or question please contact R¨udiger Jehn European Space Operations Center Robert-Bosch-Str. -

Thales Alenia Space Experience on Plasma Propulsion

Thales Alenia Space Experience on Plasma Propulsion IEPC-2007-301 Presented at the 30th International Electric Propulsion Conference, Florence, Italy September 17-20, 2007 Michel LYSZYK* and Laurent LECARDONNEL.† Thales Alenia Space, Cannes, 06150, France Abstract: Thales Alenia Space experience on plasma propulsion has been developed in the frame of Stentor, Astra 1K and GEI programs with plasma propulsion systems using SPT100 thrusters manufactured by Fakel and commercialized by Snecma . The PPS (plasma propulsion system) use in house equipments such as Power Processing Unit (PPU) manufactured by TAS-ETCA in Charleroi and the Thruster Orientation Mechanism (TOM) manufactured by TAS-France in Cannes . The PPS subsystem is used on board our SpaceBus satellite family to perform North-South station keeping. The on going activity on the XPS (Xenon Propulsion System) is devoted to the next European platform Alphabus currently under joint development by Thales Alenia Space and Astrium with CNES and ESA support. The XPS uses also the PPU manufactured by TAS-ETCA , the TOM manufactured by TAS-France and the Xe tank developed by TAS-Italy ; it use also the PPS1350 thruster under qualification by Snecma , a xenon regulator and a latch valve under development at Marotta Ireland. I. Introduction HIS document describes the Thales Alenia Space experience gained through Stentor , Astra 1K , GEI, T Spacebus and Alphabus programs on plasma Hall effect thrusters propulsion subsystems . For Spacebus application a description of the subsystem is given together with the general achieved performances . For Alphabus application a general status of the on going activities is given . * Head of electric propulsion section, Propulsion Department, [email protected]. -

The ASTRA Satellite System the ASTRA Satellite System at 19.2° East Services on ASTRA (September 2000)

Société Européenne des Satellites SES in brief (I) u Operator of ASTRA, the leading DTH satellite system in Europe u Satellite fleet: è 9 satellites in operation (7 at 19.2° East, 2 at 28.2° East) è 4 additional satellites until end of year 2001 u ASTRA carries more than 600 digital and analogue TV services and 389 radio services of leading European and international broadcasters for Europe's main language markets u ASTRA audience exceeds 79 million households in 22 European countries SES in brief (II) u Company listed on Luxembourg and Frankfurt Stock Exchanges èinstitutional and private shareholders èLuxembourg State holds 16.67 % of equity è33% of capital floated on Stock Exchange u Operating under a concession agreement with the Luxembourg State u 426 employees of 20 different nations u Turnover 1999: EUR 725.2 million H1 2000: EUR 403.0 million The ASTRA Satellite System The ASTRA Satellite System at 19.2° East Services on ASTRA (September 2000) 19.2° East u 85 analogue TV services for the German, English and pan- European market u 324 digital TV services for the French, German, More than -to-air Spanish, Dutch, Polish, Italian, Luxembourgish 75 free and pan-European market TV services u 313 analogue and digital radio services 28.2° East u 207 digital TV services for the UK and Ireland u 72 digital audio services for the UK and Ireland ASTRA coverage in Europe* (Mid Year 1992 to 2000) 90 80 70 60 50 40 30 20 ASTRA Households in Mill. 10 0 1992 1993 1994 1995 1996 1997 1998 1999 2000 DTH&SMATV 9.77 13.87 16.71 21.43 22.03 23.57 25.83 27.92 29.04 Cable 26.98 31.33 36.44 37.49 41.97 44.70 47.61 49.05 50.20 *22 European countries within the ASTRA footprint Source: SES/ASTRA, Satellite Monitors SES/ASTRA, Market Information Group, August 2000 Forecast of European DTH/SMATV Households 1997 – 2010 DTH/SMATV Households in Mill. -

SES Beam Magazine

BEAM MAGAZINE No. 01 | 2012 SATELLITES AND THE MEDIA The opportunities arising from ever-changing consumer demands TAKING THE LEAD Benefi tting from the varying markets of Europe EMERGING AUDIENCES The informed and increasingly a uent viewers of Asia TRANSMITTING MEDIA INNOVATION Keeping pace with the explosion in consumer devices EDITORIAL | BEAM NO. 01 STRENGTHENING PARTNERSHIPS DEAR READER, Partnering with our customers in order to support their de ve l- We are pushing for exciting, innovative satellite services and opment and growth plans: this is the core concept that drives our applications. Earlier this year, we unveiled SAT>IP: this ground- commitment to customer service. breaking technology allows satellite signals to be distributed in SES operates one of the world’s finest telecommunications the IP protocol to tablet computers, PCs and other smart devices. satellite fleets. With 51 satellites and a coverage area of 99% of the SAT>IP allows for mobile satellite reception on multiple screens world’s population, SES provides a major link in the global com- in the home. It represents a true breakthrough. And we are munications chain. moving closer to the launch of the O3b Networks constellation, This fleet, now featuring more than 1,400 transponders, is the which SES supports as a major strategic shareholder. This innova- world’s leading media broadcasting platform via satellite. Today, tive new medium earth orbit satellite system will provide highly we transmit more than 5,800 TV and radio channels – more than competitive high throughput broadband capacity for trunking, any other satellite system. Our spacecraft carry more than mobile backhaul and satellite applications in the maritime as 1,300 HDTV channels and our attractive satellite neighbour- well as the oil and gas sectors. -

2010 Commercial Space Transportation Forecasts

2010 Commercial Space Transportation Forecasts May 2010 FAA Commercial Space Transportation (AST) and the Commercial Space Transportation Advisory Committee (COMSTAC) HQ-101151.INDD 2010 Commercial Space Transportation Forecasts About the Office of Commercial Space Transportation The Federal Aviation Administration’s Office of Commercial Space Transportation (FAA/AST) licenses and regulates U.S. commercial space launch and reentry activity, as well as the operation of non-federal launch and reentry sites, as authorized by Executive Order 12465 and Title 49 United States Code, Subtitle IX, Chapter 701 (formerly the Commercial Space Launch Act). FAA/AST’s mission is to ensure public health and safety and the safety of property while protecting the national security and foreign policy interests of the United States during commercial launch and reentry operations. In addition, FAA/AST is directed to encourage, facilitate, and promote commercial space launches and reentries. Additional information concerning commercial space transportation can be found on FAA/AST’s web site at http://ast.faa.gov. Cover: Art by John Sloan (2010) NOTICE Use of trade names or names of manufacturers in this document does not constitute an official endorsement of such products or manufacturers, either expressed or implied, by the Federal Aviation Administration. • i • Federal Aviation Administration / Commercial Space Transportation Table of Contents Executive Summary . 1 Introduction . 4 About the CoMStAC GSo Forecast . .4 About the FAA NGSo Forecast . .4 ChAracteriStics oF the CommerCiAl Space transportAtioN MArket . .5 Demand ForecastS . .5 COMSTAC 2010 Commercial Geosynchronous Orbit (GSO) Launch Demand Forecast . 7 exeCutive Summary . .7 BackGround . .9 Forecast MethoDoloGy . .9 CoMStAC CommerCiAl GSo Launch Demand Forecast reSultS . -

2017 Annual Report

ANNUAL REPORT YEAR ENDING DECEMBER 31, 2017 A Nasdaq-100 Company 0DUFK 'HDU',6+1HWZRUN6KDUHKROGHU 6LQFHRXUVWDUWDVD&EDQGUHWDLOHULQZHKDYHVHUYHGDVDGLVUXSWLYHIRUFHFKDQJLQJWKHZD\SHRSOHDFFHVVDQGZDWFK 79',6+LVQRZD)RUWXQHFRPSDQ\LQODUJHSDUWEHFDXVHRIRXUDELOLW\WRDGDSWDQGUHLQYHQWRXUVHOYHVWRVHUYH FXVWRPHUVQRZDQGLQWKHIXWXUH 'XULQJZHIRFXVHGRQIXQGLQJRXUIXWXUHDQGHQGHGWKH\HDULQDSURILWDEOHSRVLWLRQZLWKVWURQJIUHHFDVKIORZ+LJKHU TXDOLW\FXVWRPHUVDQGLQQRYDWLRQVLQVHUYLFHGURYH',6+79FKXUQWRDPXOWL\HDUORZ6OLQJ79VXEVFULEHUVJUHZ SHUFHQW\HDURYHU\HDUHYHQDVQHZPDUNHWHQWUDQWVLQWHQVLILHG277FRPSHWLWLRQ ,QRUGHUWRGHYRWHPRUHWLPHWRRXUZLUHOHVVEXVLQHVV,SURPRWHG',6+YHWHUDQ(ULN&DUOVRQWRWKHUROHRI&(2(ULNKDV EHHQZLWKXVVLQFHZHDFTXLUHGRXUYHU\ILUVW',6+79FXVWRPHUDQGWKURXJKWKHODXQFKRI6OLQJ79+HLVDGLVFLSOLQHG RSHUDWRUDQGWKRXJKWIXOOHDGHUZKRZLOOFDSLWDOL]HRQWKHRSSRUWXQLWLHVLQSD\79:LWKWKLVFKDQJHZHDVVXPHGDQHZ JURXSVWUXFWXUHWRGHOLYHUYDOXHIRU',6+79DQG6OLQJ79E\DSSRLQWLQJH[HFXWLYHVWROHDGHDFKYLGHRVHUYLFH:HDOVR H[FKDQJHGFHUWDLQDVVHWVZLWK(FKR6WDU&RUSRUDWLRQJLYLQJXVWKHDELOLW\WRFRQWUROWKHIXOOFXVWRPHUH[SHULHQFHIRU6OLQJ 79DQG',6+79LQFOXGLQJWKHGHYHORSPHQWRIDSSOLFDWLRQVRIWZDUHDQGVHWWRSER[HV ,QDPDWXUHLQGXVWU\ZHUHPDLQHGGLVFLSOLQHGLQDWWUDFWLQJDQGUHWDLQLQJORQJWHUPSURILWDEOH',6+79VXEVFULEHUV:H FRQIURQWHGWKHLQGXVWU\¶VKLVWRULFDOO\ORZSD\79VDWLVIDFWLRQZLWK³7XQHG,Q7R<RX´D',6+79SURPLVHWROLVWHQWRDQG ILJKWIRUFXVWRPHUV:HLQWURGXFHGZKROHKRPHKDQGVIUHH79DVWKHILUVWSD\79SURYLGHUWRLQWHJUDWH$OH[DYRLFHFRQWURO $VWKH\HDUFORVHG',6+79ZDVUDQNHGLQ&XVWRPHU6HUYLFHQDWLRQDOO\E\-'3RZHUDQGRXUFXVWRPHUV 6OLQJ79ZDVWKHILUVWDQGUHPDLQVWKHOHDGLQJOLYHDQGRQGHPDQGVWUHDPLQJVHUYLFH:HEXLOWDGLIIHUHQWPRGHOWKDWJLYHV -

Astronomy 2008 Index

Astronomy Magazine Article Title Index 10 rising stars of astronomy, 8:60–8:63 1.5 million galaxies revealed, 3:41–3:43 185 million years before the dinosaurs’ demise, did an asteroid nearly end life on Earth?, 4:34–4:39 A Aligned aurorae, 8:27 All about the Veil Nebula, 6:56–6:61 Amateur astronomy’s greatest generation, 8:68–8:71 Amateurs see fireballs from U.S. satellite kill, 7:24 Another Earth, 6:13 Another super-Earth discovered, 9:21 Antares gang, The, 7:18 Antimatter traced, 5:23 Are big-planet systems uncommon?, 10:23 Are super-sized Earths the new frontier?, 11:26–11:31 Are these space rocks from Mercury?, 11:32–11:37 Are we done yet?, 4:14 Are we looking for life in the right places?, 7:28–7:33 Ask the aliens, 3:12 Asteroid sleuths find the dino killer, 1:20 Astro-humiliation, 10:14 Astroimaging over ancient Greece, 12:64–12:69 Astronaut rescue rocket revs up, 11:22 Astronomers spy a giant particle accelerator in the sky, 5:21 Astronomers unearth a star’s death secrets, 10:18 Astronomers witness alien star flip-out, 6:27 Astronomy magazine’s first 35 years, 8:supplement Astronomy’s guide to Go-to telescopes, 10:supplement Auroral storm trigger confirmed, 11:18 B Backstage at Astronomy, 8:76–8:82 Basking in the Sun, 5:16 Biggest planet’s 5 deepest mysteries, The, 1:38–1:43 Binary pulsar test affirms relativity, 10:21 Binocular Telescope snaps first image, 6:21 Black hole sets a record, 2:20 Black holes wind up galaxy arms, 9:19 Brightest starburst galaxy discovered, 12:23 C Calling all space probes, 10:64–10:65 Calling on Cassiopeia, 11:76 Canada to launch new asteroid hunter, 11:19 Canada’s handy robot, 1:24 Cannibal next door, The, 3:38 Capture images of our local star, 4:66–4:67 Cassini confirms Titan lakes, 12:27 Cassini scopes Saturn’s two-toned moon, 1:25 Cassini “tastes” Enceladus’ plumes, 7:26 Cepheus’ fall delights, 10:85 Choose the dome that’s right for you, 5:70–5:71 Clearing the air about seeing vs. -

Spotlight on Asia-Pacific

Worldwide Satellite Magazine June 2008 SatMagazine Spotlight On Asia-Pacific * The Asia-Pacific Satellite Market Segment * Expert analysis: Tara Giunta, Chris Forrester, Futron, Euroconsult, NSR and more... * Satellite Imagery — The Second Look * Diving Into the Beijing Olympics * Executive Spotlight, Andrew Jordan * The Pros Speak — Mark Dankburg, Bob Potter, Adrian Ballintine... * Checking Out CommunicAsia + O&GC3 * Thuraya-3 In Focus SATMAGAZINE JUNE 2008 CONTENTS COVER FEATURE EXE C UTIVE SPOTLIGHT The Asia-Pacific Satellite Market Andrew Jordan by Hartley & Pattie Lesser President & CEO The opportunities, and challenges, SAT-GE facing the Asia-Pacific satellite market 12 are enormous 42 FEATURES INSIGHT Let The Games Begin... High Stakes Patent Litigation by Silvano Payne, Hartley & Pattie by Tara Giunta, Robert M. Masters, Lesser, and Kevin and Michael Fleck and Erin Sears The Beijing Olympic Games are ex- Like it or not, high stakes patent pected to find some 800,000 visitors wars are waging in the global satel- 47 arriving in town for the 17-day event. 04 lite sector, and it is safe to assume that they are here to stay. Transforming Satel- TBS: Looking At Further Diversification lite Broadband by Chris Forrester by Mark Dankberg Internationally, Turner Broadcasting The first time the “radical” concept has always walked hand-in-hand with 54 of a 100 Gbps satellite was intro- the growth of satellite and cable – duced was four years ago, 07 and now IPTV. Here’s Looking At Everything — Part II by Hartley & Pattie Lesser The Key To DTH Success In Asia by Jose del Rosario The Geostationary Operational Envi- Some are eyeing Asia as a haven for ronmental Satellites (GOES) continu- economic safety or even economic ously track evolution of weather over growth amidst the current global almost a hemisphere. -

Asiasat and Globecast Distribute DW's New HD Channel on Asiasat 7

AsiaSat and Globecast distribute DW's New HD Channel on AsiaSat 7 Asia's leading satellite operator Asia Satellite Telecommunications Company Limited (AsiaSat) has reached an agreement with Globecast to deliver Deutsche Welle’s English-language program in HD to the Asia-Pacific region. DW in HD is an additional offering next to the existing TV channel in SD and radio services on AsiaSat 7. DW’s German-language program will continue its service across Asia via AsiaSat 5. For the past 20 years, AsiaSat and DW have partnered to bring German information and culture to Asia. The enhanced service offering demonstrates their commitment to providing more high-quality and relevant content to Asia. The AsiaSat fleet’s comprehensive access to Asian TV viewers has enabled DW to upgrade viewing experience as well as harness audience with different language interests. Sabrina Cubbon, AsiaSat's VP Marketing & Global Accounts: "I’m very pleased to extend our offerings of DW's programs through the Globecast partnership. Both are long-term clients of AsiaSat. Moving to HD will definitely improve viewer satisfaction and is a key tool to strengthen our success in a competitive market!" "For DW, 2017 will be a year of not only expansion but solidification as well," said DW's Director of Distribution and Sales Petra Schneider. "Content, brand and technological improvement will be more dynamic than ever before – the ability to constantly engage your audience in a consistent way and adapting to their technological watching habits remain our most important goals. The move towards HD is a step in the right direction." Biliana Pumpalovic, managing director at Globecast: "We are working in multiple markets to help broadcasters launch HD services and we're very pleased that DW has turned to us and AsiaSat. -

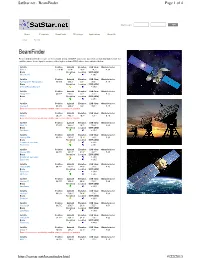

Beamfinder Page 1 of 4

SatStar.net - BeamFinder Page 1 of 4 Client Login: Home Footprints BeamFinder TV Listings Applications About Us Setup Tutorial BeamFinder Please find BeamFinder results for the C-band below. All EIRP values are based on official information from the satellite owner. Some signals can have either higher or lower EIRP values than indicated below. Satellite Position Azimuth Elevation LNB Skew Obstacle factor NSS 9 177.0°W 97.4° 19.0° -74.1° 0.34 Beam Reception Location EIRP (dBW) West hemi ≈ 39.5 Satellite Position Azimuth Elevation LNB Skew Obstacle factor AzerSpace 1/Africasat 1a 46.0°E 266.3° 5.7° 75.5° 0.10 Beam Reception Location EIRP (dBW) Central Asia & Europe ≈ 35.5 Satellite Position Azimuth Elevation LNB Skew Obstacle factor Yamal 202 49.0°E 265.5° 8.7° 75.2° 0.15 Beam Reception Location EIRP (dBW) C ≈ 40.5 Satellite Position Azimuth Elevation LNB Skew Obstacle factor Intelsat 5 50.2°E 265.2° 9.9° 75.1° 0.17 Beam information not provided by satellite owner or currently not available Satellite Position Azimuth Elevation LNB Skew Obstacle factor NSS 5 50.5°E 265.1° 10.2° 75.1° 0.18 Beam information not provided by satellite owner or currently not available Satellite Position Azimuth Elevation LNB Skew Obstacle factor NSS 12 57.0°E 263.3° 16.7° 74.4° 0.30 Beam Reception Location EIRP (dBW) Easthemi ≈ 40.0 Satellite Position Azimuth Elevation LNB Skew Obstacle factor Intelsat 904 60.0°E 262.4° 19.7° 74.0° 0.36 Beam Reception Location EIRP (dBW) Combined east zone ≈ 35.5 East hemi ≈ 38.5 Satellite Position Azimuth Elevation LNB Skew Obstacle -

Classification of Geosynchronous Objects

esoc European Space Operations Centre Robert-Bosch-Strasse 5 D-64293 Darmstadt Germany T +49 (0)6151 900 www.esa.int CLASSIFICATION OF GEOSYNCHRONOUS OBJECTS Produced with the DISCOS Database Prepared by T. Flohrer & S. Frey Reference GEN-DB-LOG-00195-OPS-GR Issue 18 Revision 0 Date of Issue 3 June 2016 Status ISSUED Document Type TN European Space Agency Agence spatiale europeenne´ Abstract This is a status report on geosynchronous objects as of 1 January 2016. Based on orbital data in ESA’s DISCOS database and on orbital data provided by KIAM the situation near the geostationary ring is analysed. From 1434 objects for which orbital data are available (of which 2 are outdated, i.e. the last available state dates back to 180 or more days before the reference date), 471 are actively controlled, 747 are drifting above, below or through GEO, 190 are in a libration orbit and 15 are in a highly inclined orbit. For 11 objects the status could not be determined. Furthermore, there are 50 uncontrolled objects without orbital data (of which 44 have not been cata- logued). Thus the total number of known objects in the geostationary region is 1484. In issue 18 the previously used definition of ”near the geostationary ring” has been slightly adapted. If you detect any error or if you have any comment or question please contact: Tim Flohrer, PhD European Space Agency European Space Operations Center Space Debris Office (OPS-GR) Robert-Bosch-Str. 5 64293 Darmstadt, Germany Tel.: +49-6151-903058 E-mail: tim.fl[email protected] Page 1 / 178 European Space Agency CLASSIFICATION OF GEOSYNCHRONOUS OBJECTS Agence spatiale europeenne´ Date 3 June 2016 Issue 18 Rev 0 Table of contents 1 Introduction 3 2 Sources 4 2.1 USSTRATCOM Two-Line Elements (TLEs) .