Focused Positive Resilient

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

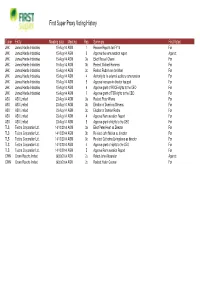

First Super Proxy Voting History

First Super Proxy Voting History Ticker Entity Meeting date Meeting Res. Summary First Voted JHX James Hardie Industries 15-Aug-14 AGM 1 Receive Reports for FY14 For JHX James Hardie Industries 15-Aug-14 AGM 2 Approve the remuneration report Against JHX James Hardie Industries 15-Aug-14 AGM 3a Elect Russell Chenu For JHX James Hardie Industries 15-Aug-14 AGM 3b Reelect Michael Hammes For JHX James Hardie Industries 15-Aug-14 AGM 3c Reelect Rudolf van der Meer For JHX James Hardie Industries 15-Aug-14 AGM 4 Authority to fix external auditors remuneration For JHX James Hardie Industries 15-Aug-14 AGM 5 Approve increase in director fee pool For JHX James Hardie Industries 15-Aug-14 AGM 6 Approve grant of ROCE rights to the CEO For JHX James Hardie Industries 15-Aug-14 AGM 7 Approve grant of TSR rights to the CEO For ASX ASX Limited 23-Aug-14 AGM 3a Reelect Peter Warne For ASX ASX Limited 23-Aug-14 AGM 3b Election of Domininc Stevens For ASX ASX Limited 23-Aug-14 AGM 3c Election of Damian Roche For ASX ASX Limited 23-Aug-14 AGM 4 Approve Remuneration Report For ASX ASX Limited 23-Aug-14 AGM 5 Approve grant of rights to the CEO For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3a Elect Peter Heart as Director For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3b Re-elect John Mullen as director For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3c Re-elect Catherine Livingstone as director For TLS Telstra Corporation Ltd. -

Annual Report 2016

ANNUAL REPORT 2016 GLOBAL DIVERSIFIED INDUSTRIAL CHEMICALS OUR OPERATIONS Ekati e Diavik e e Meadowbank CANADA Flin Flon e e Ishpeming Tumbler Ridge e North Bay Calgary a Maitland Biwabik e Boisbriand Tirana St Helens a e Ormstown Bucharest Barry i Simsbury Ankara Salt Lake City USA Cheyenne e a a Soma i e Donora TURKEY Carthage i e e Duffield CHINA Louisiana, Missouri a e Van Wyck i Linyi (Fabchem) PAKISTAN Waggaman, Louisiana e Brooksville New Delhi Dinamita i i Graham Hong Kong Gomez Palacios i Wolf Lake INDIA Guadalajara e MEXICO e Muara Tuhup e Tenggarong Batu Arang (TKEB) i e Berau PAPUA NEW GUINEA SOUTH Sibolga Tanjung Tabalong e e Papua New Guinea AFRICA Jakarta Batu Kajang e INDONESIA e a Moranbah Townsville Port Hedland e LATIN Mt Isa e Moura AMERICA Phosphate Hill (Queensland Nitrates) AUSTRALIA Gibson Island Kalgoorlie e i Helidon La Serena i Kooragang Island i Johannesburg (SASOL Dyno Nobel) Perth a Santiago Port Adelaide e Warkworth i Johannesburg (DetNet) Melbourne Portland Geelong Devonport Cover photograph: New IPL World Class Ammonia Plant, Louisiana USA VISION STATEMENT To be the best in our markets, delivering Zero Harm and outstanding business performance through our people, our culture and our customer focus. Ekati e Diavik e e Meadowbank CANADA Flin Flon e e Ishpeming Tumbler Ridge e North Bay Calgary a Maitland Biwabik e Boisbriand Tirana St Helens a e Ormstown Bucharest Barry i Simsbury Ankara Salt Lake City USA Cheyenne e a a Soma i e Donora TURKEY Carthage i e e Duffield CHINA Louisiana, Missouri a e Van Wyck -

For Personal Use Only Use Personal For

Office of the Company Secretary ABN 42 004 080 264 Registered Office: Level 8, 28 Freshwater Place Southbank Victoria 3006 Tel: (61 3) 8695 4400 Fax: (61 3) 8695 4419 25 November 2011 www.incitecpivot.com.au The Manager Company Announcements Office Australian Securities Exchange Level 45, South Tower Rialto 525 Collins Street MELBOURNE VIC 3000 Dear Sir or Madam Electronic Lodgement 2011 Annual Report In accordance with the listing rules, I attach a copy of Incitec Pivot Limited’s Annual Report for 2011 for release to the market. Yours faithfully Kerry Gleeson Company Secretary Attach. For personal use only 2011ANNUAL REPORT 2011 For personal use only STRATEGY ON TRACK AND DELIVERING CANADA Boisbriand Calgary North Bay Lausanne Louisiana Maitland Tirana St Helens Ormstown Bucharest Simsbury Ankara Salt Lake City USA Port Ewen Soma Cheyenne Donora TURKEY Carthage Duffield Wolf Lake CHINA Linyi (Fabchem) Savannah PAKISTAN Graham New Delhi Dinamita Hong Kong INDIA MEXICO TKEB PAPUA Arkon Binungan, Lati NEW GUINEA & Sambarata SOUTH Martabe AFRICA Adaro Lihir Jakarta INDONESIA Moranbah Port Hedland Townsville Mt Isa Moura (Queensland Nitrates) LATIN Phosphate Hill AMERICA AUSTRALIA Gibson Island Kalgoorlie Helidon La Serena Johannesburg (SASOL) Perth Kooragang Island Santiago Port Adelaide Johannesburg (DetNet) Melbourne Portland Geelong Devonport “Incitec Pivot’s strategy is Incitec Pivot Limited to leverage value from the Company Headquarters industrialisation and urbanisation Incitec Pivot Fertilisers Nitromak of Asia by positioning ourselves -

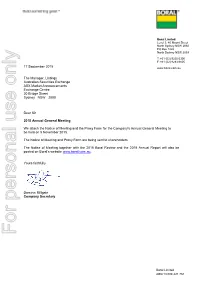

17 September 2018 the Manager, Listings Australian Securities

Boral Limited Level 3, 40 Mount Street North Sydney NSW 2060 PO Box 1228 North Sydney NSW 2059 T: +61 (02) 9220 6300 F: +61 (02) 9233 6605 17 September 2018 www.boral.com The Manager, Listings Australian Securities Exchange ASX Market Announcements Exchange Centre 20 Bridge Street Sydney NSW 2000 Dear Sir 2018 Annual General Meeting We attach the Notice of Meeting and the Proxy Form for the Company's Annual General Meeting to be held on 30 October 2018. The Notice of Meeting and Proxy Form are being sent to shareholders. The Notice of Meeting together with the 2018 Boral Review and the 2018 Annual Report will also be posted on Boral's website www.boral.com. Yours faithfully Dominic Millgate Company Secretary Boral Limited ABN 13 008 421 761 Boral Limited 2018 Annual General Meeting 17 SEPTEMBER 2018 2016 FERGUSON LA HELP ST Dear Shareholder ANDERSON ST It is my pleasure to invite you to attend the RAILWAY ST THE CONCOURSE 2018 Annual General Meeting of Boral Limited. e ENDEAVOUR ST The Meeting will be held at the Civic Pavilion, VICTORIA AVENUE erchang Transport Chatswood The Concourse, Chatswood on Tuesday, 30 October Int SPRING ST 2018 at 10.30am. Chatswood Mall We also invite you to join the Board and senior management of Boral for refreshments following the Meeting. This is an opportunity for you to learn more about VICTOR ST Boral’s operations from the executives who are running Westfield Shopping Centre Boral’s businesses. The map opposite shows the location of The Concourse. ALBERT AVENUE This will be my fifth AGM as a Director of Boral and my first AGM as Chairman. -

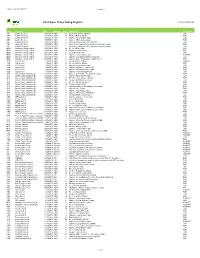

First Super Proxy Voting Register from Jul-18 to Oct-20

***Commercial in Confidence***# ***Public*** First Super Proxy Voting Register From Jul-18 to Oct-20 TickerCompany Date MeetingItemDescription First Voted AST AusNet Services 19/07/2018AGM 2aElect Alan Chan Heng Loon FOR AST AusNet Services 19/07/2018AGM 2bRe-elect Robert Milliner FOR AST AusNet Services 19/07/2018AGM 3 Approve remuneration report FOR AST AusNet Services 19/07/2018AGM 4 Approve CEO equity awards FOR AST AusNet Services 19/07/2018AGM 5 Issue of shares – Up to 10% pro rata FOR AST AusNet Services 19/07/2018AGM 6 Issue of shares pursuant to dividend reinvestment plan FOR AST AusNet Services 19/07/2018AGM 7 Issue of shares pursuant to employee incentive scheme FOR MQG Macquarie Group Limited 26/07/2018AGM 2aRe-elect Peter Warne FOR MQG Macquarie Group Limited 26/07/2018AGM 2bRe-elect Gordon Cairns FOR MQG Macquarie Group Limited 26/07/2018AGM 2cElect Glenn Stevens FOR MQG Macquarie Group Limited 26/07/2018AGM 3 Approve remuneration report AGAINST MQG Macquarie Group Limited 26/07/2018AGM 4 Approve CEO participation in equity plan FOR MQG Macquarie Group Limited 26/07/2018AGM 5 Approve issue of Macquarie Capital Notes 3 FOR ALQ ALS Limited 1/08/2018AGM 2i Re‐elect Bruce Phillips AGAINST ALQ ALS Limited 1/08/2018AGM 2ii Re‐elect Charlie Sartain FOR ALQ ALS Limited 1/08/2018AGM 3Approve remuneration report FOR ALQ ALS Limited 1/08/2018AGM 4 Approve director fee cap increase FOR ALQ ALS Limited 1/08/2018AGM 5 Approve CEO performance rights FOR ALQ ALS Limited 1/08/2018AGM 6Approve termination payments FOR JHX James Hardie Industries -

Annual Report 2012

Annual Report 2012 Building and renovations … it’s our business Alesco at a glance Alesco supplies innovative Contents branded products to trade Financial Overview 2-3 Chairman’s Report 4-5 customers in the Australian Managing Director’s Report 6-9 Divisional Reports 10 and New Zealand building - Garage Doors & Openers 11 - Cabinets, Windows & Appliances 12 products markets. - Construction Products & Equipment 13 Board of Directors 14-15 We operate through three divisions: Executive Team 16 Safety & Our People 17 Garage Doors & Openers Directors’ Report 18 Corporate Governance Statement 19 Cabinets, Windows & Appliances Remuneration Report 30 Financial Statements 65 Construction Products & Equipment 2012 Revenue1 Employees Listed on ASX $459.7m ~1380 ALS Group Financial Summary yeAR eNded 31 mAy 2012 2011 2010 2009 2008 Revenue ($ million) 459.7 478.8 483.6 512.7 561.9 2 NG 3 ui EBIT ($ million) 32.2 40.3 32.1 33.3 58.3 esses N N ti 3 N EBIT/Sales (%) 7.0 8.4 6.6 6.5 10.4 Busi Co Return on net operating assets4 (%) 7.0 8.5 6.7 6.7 11.7 Profit after tax($ million) -13.9 13.6 -124.3 -12.8 58.0 Return on equity (%) -3.3 3.2 -22.7 -2.2 11.2 oup Earnings per share (cents) -14.7 14.4 -132.8 -13.9 67.2 R G Dividend per share (cents) 18.0 14.0 7.0 7.0 67.0 Market capitalisation ($ million) 185.6 290.1 250.6 302.1 710.1 1. Continuing business only 2. -

For Personal Use Only Use Personal For

Boral Limited Level 3, 40 Mount Street North Sydney NSW 2060 PO Box 1228 North Sydney NSW 2059 T: +61 (02) 9220 6300 F: +61 (02) 9233 6605 17 September 2015 www.boral.com.au The Manager, Listings Australian Securities Exchange ASX Market Announcements Exchange Centre 20 Bridge Street Sydney NSW 2000 Dear Sir 2015 Annual General Meeting We attach the Notice of Meeting and the Proxy Form for the Company's Annual General Meeting to be held on 5 November 2015. The Notice of Meeting and Proxy Form are being sent to shareholders. The Notice of Meeting together with the 2015 Boral Review and the 2015 Annual Report will also be posted on Boral's website www.boral.com.au. Yours faithfully Dominic Millgate Company Secretary For personal use only Boral Limited ABN 13 008 421 761 BORAL LIMITED ANNUAL GENERAL MEETING 2015 17 SEPTEMBER 2015 FERGUSON LA HELP ST ANDERSON ST Dear Shareholder RAILWAY ST THE CONCOURSE It is my pleasure to invite you to attend the 2015 Annual General Meeting of Boral Limited. e ENDEAVOUR ST VICTORIA AVENUE erchang The Meeting will be held at The Civic Pavilion, Transport Chatswood Int The Concourse, Chatswood on Thursday, 5 November SPRING ST 2015 at 10.30am. The map opposite shows the location Chatswood Mall of The Concourse. The Notice of Meeting which follows, sets out the business to be dealt with at the Meeting. VICTOR ST Westeld Shopping Centre If you are able to attend the Meeting, please bring the enclosed Proxy Form with you to facilitate your registration. -

2012 Notice of Meeting

Boral Limited 2012 ABN 13 008 421 761 Annual General Meeting 17 September 2012 Dear Shareholder It is my pleasure to invite you to attend the 2012 Annual General Meeting of Boral Limited. The Meeting will be held in the City Recital Hall, Angel Place, Sydney on Thursday, 1 November 2012 at 10.30am. The plan opposite shows the location of the City Recital Hall. The Notice of Meeting which follows sets out the business to be dealt with at the Meeting. If you are able to attend the Meeting, please bring the enclosed Proxy Form with you to facilitate your registration. If you do not plan to attend the Meeting, you may wish to appoint a proxy to attend and vote on your behalf by completing and lodging the enclosed Proxy Form. Instructions on how to appoint a proxy and lodge the form are on the back of the form. Proxy Forms must be received by 10.30am on Tuesday, 30 October 2012 to be valid for the Meeting. The full AGM will be webcast live on the internet at location of AGM www.boral.com.au. The Chairman’s Address and the Chief Executive’s Address to the AGM will be placed on Boral’s website on the day of the Meeting. Yours sincerely BORAL Level 39, AMP Centre Dr Bob Every, AO 50 Bridge Street, Sydney Chairman GPO Box 910, Sydney NSW 2001 T (02) 9220 6300 F (02) 9233 6605 NOTICE OF MEETING Notice is given that the Annual General Item 5: Award of Rights to Mike Kane, Meeting of Shareholders of Boral Chief Executive Officer Designate Limited will be held in the City Recital To consider and, if thought fit, to pass the following resolution as an ordinary resolution: Hall, Angel Place, Sydney on Thursday, 1 November 2012 at 10.30am. -

27 September 2010 the Manager, Listings Australian Securities

27 September 2010 Boral Limited ABN 13 008 421 761 Level 39, 50 Bridge Street The Manager, Listings Sydney NSW 2000 T +61 2 9220 6300 Australian Securities Exchange F +61 2 9233 3725 Company Announcements Office www.boral.com.au Level 4 Exchange Centre 20 Bridge Street Sydney NSW 2000 Dear Sir 2010 Annual Report We attach the Company's 2010 Shareholder Review. We are separately forwarding to you the 2010 Annual Report (which includes the financial report). These documents are being sent to shareholders, other than those who have chosen to receive no reports, in accordance with choices made by them. Shareholders who have not made a choice will receive the Shareholder Review. The Shareholder Review and the Annual Report, together with the Notice of Meeting for the Company's 2010 Annual General Meeting will also be posted on Boral's website www.boral.com.au. Yours faithfully Margaret Taylor Company Secretary Boral Limited Shareholder Review 2010 LAYING THE FOUNDATIONS CONTENTS BORAL LIMITED Financial highlights 1 Boral Limited is an Group overview 2 Chairman’s review 4 international building Chief Executive’s review 6 and construction The building blocks of growth 10 materials group, Reinforcing the core 12 headquartered in Operational review 14 Financial review 22 Sydney, Australia. Sustainability in Boral 26 With leading market Board of directors 30 positions, Boral’s core Remuneration 32 businesses are Cement Financial calendar inside back cover and Construction Materials in Australia; Plasterboard in Australia and Asia; and Bricks, Roof -

Report of the Task Group on Emissions Trading

Report of the Task Group on Emissions Trading i REPORT OF THE TASK GROUP ON EMISSIONS TRADING © Commonwealth of Australia 2007 This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Commonwealth. Requests and inquiries concerning reproduction and rights should be addressed to the Commonwealth Copyright Administration, Attorney General’s Department, Robert Garran Offices, National Circuit Barton ACT 2600 or posted at http://www.ag.gov.au/cca Published by: The Department of the Prime Minister and Cabinet, One National Circuit, Barton ACT 2600 Australia ISBN 978-0-9803115-4-9 (paperback) ISBN 978-0-9803115-5-6 (PDF) The Department of the Prime Minister and Cabinet website, http://www.pmc.gov.au Editorial, design and layout by WHH Publishing. Original concept and cover art by Octavo Printed by Pirion, Canberra i ii REPORT OF THE TASK GROUP ON EMISSIONS TRADING Contents Introduction 1 Executive summary 5 1. Climate change – a global challenge 14 1.1 Overview 14 1.2 The global context 14 1.3 Global trends in emissions 17 2. Australia’s circumstances and current policies 25 2.1 Overview 25 2.2 Structure of Australia's economy and emissions profile 26 2.3 Australia’s emissions trajectory 31 2.4 The challenge of reducing emissions 34 2.5 Current policies and measures to reduce greenhouse gases 37 3. Achieving least-cost emissions reductions 44 3.1 Overview 44 3.2 Abatement options 44 3.3 Comparing market-based approaches 48 3.4 Preferred approach 49 4. -

Boral Limited 2018 Annual General Meeting

Boral Limited 2018 Annual General Meeting 17 SEPTEMBER 2018 2016 FERGUSON LA HELP ST Dear Shareholder ANDERSON ST It is my pleasure to invite you to attend the RAILWAY ST THE CONCOURSE 2018 Annual General Meeting of Boral Limited. e ENDEAVOUR ST The Meeting will be held at the Civic Pavilion, VICTORIA AVENUE erchang Transport Chatswood The Concourse, Chatswood on Tuesday, 30 October Int SPRING ST 2018 at 10.30am. Chatswood Mall We also invite you to join the Board and senior management of Boral for refreshments following the Meeting. This is an opportunity for you to learn more about VICTOR ST Boral’s operations from the executives who are running Westfield Shopping Centre Boral’s businesses. The map opposite shows the location of The Concourse. ALBERT AVENUE This will be my fifth AGM as a Director of Boral and my first AGM as Chairman. I look forward to welcoming those shareholders who can attend. I would also like to take this opportunity to welcome Peter Alexander to what will be his first AGM as a Director, and to thank Catherine Brenner for her considerable and valuable contribution to Boral since she joined the Board in 2010. Catherine retires by rotation at the 2018 AGM and has decided not to stand for re-election. Catherine has been an outstanding Non-executive Director of our Board for 8 years. She has made a great contribution and leaves the Board with our thanks and enormous respect. We wish her the very best. The Notice of Meeting which follows sets out the business to be dealt with at the Meeting. -

SPDR® S&P®/ASX 200 Fund Proxy Voting Record

1 July 2018 to 30 June 2019 SPDR® S&P®/ASX 200 Fund Proxy Voting Record Vote Summary Report Date range covered: 07/01/2018 to 06/30/2019 Location(s): State Street Global Advisors, State Street Global Advisors 1412 Institution Account(s): SPDR S&P/ ASX 200 Fund AusNet Services Limited Meeting Date: 07/19/2018 Country: Australia Primary Security ID: Q0708Q109 Record Date: 07/17/2018 Meeting Type: Annual Ticker: AST Primary CUSIP: Q8604X102 Primary ISIN: AU000000AST5 Primary SEDOL: BPXR7J0 Proposal Votable Voting Vote Number Proposal Text Proponent Proposal Mgmt Rec Policy Rec Instruction 2a Elect Alan Chan Heng Loon as Director Mgmt Yes For Against Against 2b Elect Robert Milliner as Director Mgmt Yes For For For 3 Approve the Remuneration Report Mgmt Yes For For For 4 Approve Grant of Equity Awards to Nino Ficca Mgmt Yes For For For 5 Approve the Issuance of Shares Mgmt Yes For For For 6 Approve the Issuance of Shares Pursuant to Mgmt Yes For For For the Dividend Reinvestment Plan 7 Approve the Issuance of Shares Pursuant to Mgmt Yes For For For an Employee Incentive Scheme Macquarie Group Limited Meeting Date: 07/26/2018 Country: Australia Primary Security ID: Q57085286 Record Date: 07/24/2018 Meeting Type: Annual Ticker: MQG Primary CUSIP: Q57085104 Primary ISIN: AU000000MQG1 Primary SEDOL: B28YTC2 Proposal Votable Voting Vote Number Proposal Text Proponent Proposal Mgmt Rec Policy Rec Instruction 2a Elect Peter H Warne as Director Mgmt Yes For For For 2b Elect Gordon M Cairns as Director Mgmt Yes For For For 2c Elect Glenn R Stevens