ALU4392 Concise Part1 FA LR.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2013 Annual Report

SURFACEBELOW THE Some statements in this report are forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995. Forward-looking statements also include those containing such words as ‘anticipate’, ‘estimates’, ‘should’, ‘will’, ‘expects’, ‘plans’ or similar expressions. Forward-looking statements involve risks and uncertainties that may cause actual outcomes to be different from the forward-looking statements. Important factors that could cause actual results to differ from the forward looking statements include: (a) material adverse changes in global economic, alumina or aluminium industry conditions and the markets served by AWAC; (b) changes in production and development costs and production levels or to sales agreements; (c) changes in laws or regulations or policies; (d) changes in alumina and aluminium prices and currency exchange rates; and (e) the other risk factors summarised in Alumina’s Form 20-F for the year ended 31 December 2012. Unless otherwise indicated, the values in this report are presented in US dollars. CONTENTS 1 2 AT A GLANCE 4 CHAIRMAN AND CHIEF EXECUTIVE OFFICER’S REPORT 8 SUSTAINABILITY AND THE AWAC BUSINESS 10 CORPORATE GOVERNANCE STATEMENT 23 DIRECTORS’ REPORT 28 OPERATING AND FINANCIAL REVIEW 37 REMUNERATION REPORT 71 FINANCIAL REPORT 112 SHAREHOLDER INFORMATION 113 FINANCIAL HISTORY Challenging market conditions continued in 2013, stemming from a well-supplied alumina market, a sustained low international alumina pricing environment and an unfavourable foreign exchange position. Against this backdrop, Alumina Limited improved its results by recording a net profit of US$0.5 million, an increase of US$56.1 million from the previous year. -

A Modern Mining Company

A modern mining company 22 February 2018 The Manager, Companies Australian Securities Exchange Companies Announcement Centre 20 Bridge Street Sydney NSW 2000 Dear Sir/Madam, OZ Minerals 2017 Annual and Sustainability Report OZ Minerals today announced its results for the full year ended 31 December 2017. Attached is the 2017 Annual and Sustainability Report including: • Directors’ Report • Remuneration Overview and Report • FY17 Financial Report • Sustainability Report Sincerely, Michelle Pole Company Secretary and Senior Legal Counsel OZ Minerals Limited | ABN: 40 005 482 824 | Level 1, 162 Greenhill Road, Parkside South Australia 5063 T: +61 8 8229 6600 | F: +61 8 8229 6601 | [email protected] | www.ozminerals.com 2017 Annual and Sustainability Report OZ Minerals Limited ABN 40 005 482 824 Limited OZ Minerals 2017 Annual and Sustainability Report CONTENTS 01 Contents 2017 Snapshot 02 Message from the Chairman and CEO 05 Operating review 06 Company Strategy 06 Prominent Hill 08 Carrapateena 10 West Musgrave 12 Exploration and Growth 13 Governance 14 Directors’ Report 19 Financial Review 29 Remuneration Overview and Report 37 Cautionary statement The sustainability section of this report contains forward-looking statements that relate to our activities, Sustainability Report 57 plans and objectives. Actual results may significantly differ from these statements, depending on a variety of factors. The term ‘material topic’ is used for Mineral Resources and Ore Reserves 81 voluntary sustainability reporting to describe topics that could affect our sustainability performance. By their nature, forward-looking statements involve risk Financial Report 91 and uncertainty because they relate to events and circumstances that will occur in the future and may be outside OZ Minerals' control. -

Resource Projects

Western Australia’s principal resources projects, 2019-20 In 2019-20, Western Australia had 123 principal mining projects. Each of the principal mining projects is export-oriented and high value. They each had mineral sales valued at more than $5 million (or more than 2500oz of gold), or, in the case of projects on private land, for which sales are not reported, has employees of greater than 50. Projects are grouped according to main commodity sold. The State’s mining industry also comprised hundreds of quarries and small mines that largely produced the basic raw materials required for the local construction industry. This includes clays, construction materials (aggregate, gravel, rock and sand), dimension stone, gypsum, limestone, limesand and spongolite. There were 10 principal producers of these products. There were also 13 major mineral processing operations to transform bauxite into alumina; gold dore into gold bars; nickel ore into nickel concentrate (where accepting third party fee) and nickel concentrate into nickel matte, nickel powder and nickel briquettes; rutile and synthetic rutile into titanium dioxide pigment; zircon into fused zirconia; and silica sand into silicon metal. Western Australia’s petroleum industry consisted of 22 projects that produced oil, gas and condensates from 53 fields in onshore and offshore areas of the State. These projects had 13 processing plants, predominantly for LNG exports and domestic gas sales. The attached tables below provide details of the State’s principal mining projects, principal producers -

1. Shareholdings in Public and Private Companies (Including Holding

Form A 3 March 2020 Surname: Mclachlan Other names: Andrew State/Territory: SA Date: 3/03/2020 1. Shareholdings in public and private companies (including holding companies) indicating the name of the company or companies (Note: It is NOT necessary to declare the size or value of the shareholding) Name of company – (including holding and subsidiary companies if applicable) OATMILL HOLDINGS PTY LTD AUSTOFIX GROUP LTD VITRO SOFTWARE HOLDINGS (Designated Activity Company) ALUMINA LIMITED ANTIPODES GLOBAL INVESTMENT COMPANY LTD ANZ BANKING GROUP LIMITED AP EAGERS LIMITED ARISTOCRAT LEISURE LIMITED BHP GROUP LIMITED BORAL LIMITED CLEANAWAY WASTE MANAGEMENT LTD COMMONWEALTH BANK OF AUSTRALIA CORPORATE TRAVEL MANAGEMENT LIMITED COSTA GROUP HOLDINGS LIMITED GRAINCORP LIMITED ILUKA RESOURCES LIMITED LI LONG SHORT FUND LIMITED MACQUARIE GROUP LIMITED MINERAL RESOURCES LIMITED Form A NAOS EMERG OPP CO LTD NINE ENTERTAINMENT co HLDGS LTD OOH!MEDIA LIMITED ORIGIN ENERGY LIMITED ORORA LIMITED QBE INSURANCE GROUP LIMITED QUBE HOLDINGS LIMITED RELIANCE WORLDWIDE CORPORATION LIMITED SIMS LIMITED SONIC HEALTHCARE LIMITED SOUTH32 LIMITED S32 THE STAR ENTERTAINMENT GROUP LTD TPG TELECOM LIMITED TPM WAM LEADERS LIMITED WAM MICROCAP LIMITED WESFARMERS LIMITED WESTPAC BANKING CORPORATION WOODSIDE PETROLEUM LIMITED WORLEY LIMITED NATIONAL STORAGE REIT STPLD SEC AMCOR PLC JANUS HENDERSON GROUP PLC SPARK NEW ZEALAND LIMITED VIRGIN MONEY UK PLC ANZ BANK UNSEC NON-CUM PARADICE GLOBAL SMALL CAP FUND PLATINUM EUROPEAN FUND WESTPAC CAPITAL NOTES 2. Family and business -

CRU World Aluminium Conference Series 2021

ASX Announcement 17 June 2021 CRU World Aluminium Conference Series 2021 Please find attached, a presentation by Alumina Limited released at the CRU World Aluminium Conference Series 2021 on Wednesday, 16th June 2021. This ASX announcement was approved and authorised for release by Mike Ferraro, Chief Executive Officer. Forward-looking statements Neither Alumina Limited nor any other person warrants or guarantees the future performance of Alumina Limited or any return on any investment made in Alumina Limited securities. This document may contain certain forward-looking statements, including forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995. The words “anticipate”, "aim", "believe", "expect", "project", “estimate”, "forecast", "intend", "likely", “should”, "could", "will", "may", "target", "plan” and other similar expressions (including indications of "objectives") are intended to identify forward-looking statements. Indications of, and guidance on, future financial position and performance and distributions, and statements regarding Alumina Limited's future developments and the market outlook, are also forward-looking statements. Any forward-looking statements contained in this document are not guarantees of future performance. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, many of which are beyond the control of Alumina Limited and its directors, officers, employees and agents that may cause actual results to differ materially from -

Morningstar Equity Research Coverage

December 2019 Equity Research Coverage Morningstar covers more than 200 companies in We use the following guidelines to Contact Details Australia and New Zealand as part of our global determine our Australian equity coverage: Australia stock coverage of about 1,500 companies. We are × Nearly all companies in the S&P/ASX 100 Index. Helpdesk: +61 2 9276 4446 Email: [email protected] one of the largest research teams globally with × Companies in the S&P/ASX 200 Index which more than 100 analysts, associates, and have an economic moat and/or have cash flow New Zealand strategists, including 17 in Australia. Local analysts which is at least mildly predictable. Helpdesk: +64 9 915 6770 regularly glean insights from our global sector teams × In total, Morningstar will cover about 80% of Email: [email protected] in China, Europe, and the United States, enriching S&P/ASX 200 companies (which typically the process and enhancing outcomes for investors. equates to about 95% of S&P/ASX 200 by Our research philosophy focuses on bottom-up market capitalisation). Companies we choose analysis, developing differentiated and deep not to cover in this index are usually unattractive opinions on competitive forces, growth prospects, for most portfolios, in our opinion. and valuations for every company we cover. We × About 30 ex-S&P/ASX 200 stocks are selected publish on each company under coverage at least on Morningstar’s judgement of each security's quarterly, and as events demand, to ensure investment merit − which includes a very investment ideas are always relevant. strong lean towards high-quality companies We are an independent research house, and with sustainable competitive advantages, or therefore determine our coverage universe based economic moats. -

~IVIEI::.. 3Rd March 2012

~IVIEI::.. 3rd March 2012 Tim Bryant Secretariat Senate Economics Legislation Committee Parliament House CANBERRA ACT 2600 Dear Tim Senate Economics Committee Inquiry into the Minerals Resource Rent Tax - Questions on Notice Thank you for the opportunity of providing separate responses to various Questions on Notice asked at the Senate Economics Committee hearing held on 21 February 2012. AMEC would also like to provide some additional and relevant comments concerning the MRRT for the consideration of the Committee. Q from the Chair, page 56- How many small miners are currently making an annual profit of more than $75 million a year? Response In respect of the MRRT legislation, AMEC considers that a small miner should be defined as a miner producing less than ten million tons of iron ore or coal per annum. 1 2 According to Intierra , in the calendar year 2010 there were six iron ore producers and ten coal producers in production in this category. Examining the most recent annual reports of the iron ore3 producer's shows three of the six iron ore producers made a "company profit" in excess of $75 million. Four of these companies are single commodity producers (iron ore) while the other two produce other commodities. AMEC is unable to separate any iron ore profit from the balance of the company profits in the later two cases. Of the two iron ore companies mentioned by me in the hearing on 21 February, BC Iron only entered production in the first half of the 2011/12 financial year and therefore full annual financial data is unavailable. -

Alumina Limited 2020 Annual Review

ASX ANNOUNCEMENT 31 MARCH 2021 Alumina Limited 2020 Annual Review Attached, in accordance with Listing Rule 3.17 is a copy of Alumina Limited’s Annual Review 2020 that will be issued to shareholders. This ASX announcement was approved and authorised for release by Stephen Foster, Company Secretary. Stephen Foster Company Secretary For investor enquiries: For media enquiries: Charles Smitheram Tim Duncan Manager – Treasury & Investor Relations Hinton and Associates Phone: +61 3 8699 2613 Phone: +61 3 9600 1979 Mobile: +61 412 340 047 Mobile: +61 408 441 122 Email: [email protected] ROCK SOLID Annual Review 2020 2 About Alumina Limited 4 At a Glance 6 AWAC – A Global Business 8 Map of Operations 10 Chairman and CEO Report 16 Sustainability 19 Board of Directors 22 Executive Management 24 Letter by Chair of Compensation Committee 28 Remuneration Summary 42 Condensed Consolidated Statement of Financial Position 43 Financial History About Chairman and Sustainability Our People Remuneration and Back to contents Alumina Limited CEO Report Financial Reports 1 RESILIENT ROBUST RESPONSIBLE Qualities that have evolved from decades of partnership, planning and perseverance – through the good times, and those as challenging as 2020. Alumina Limited Annual Review 2020 2 The Annual Review is presented in US dollars, unless otherwise specified. ABOUT ALUMINA LIMITED Alumina Limited is a leading Australian company listed on the Australian Securities Exchange (ASX). Alumina Limited is the 40 per cent partner in the AWAC joint venture whose assets comprise globally leading bauxite mines and alumina refineries in Australia, Brazil, Spain, Saudi Arabia and Guinea. AWAC also has a 55 per cent interest in the Portland aluminium smelter in Victoria, Australia. -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 19 May 2017 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 3.27 0.31 9.36 62.69 125.52 158.33 - - - - ABC Adelaide Brighton 5.61 -2.94 0.54 10.95 8.19 16.12 18.37 17.52 7.59 37 ABP Abacus Property Group 3.42 0.89 0.29 27.08 11.22 14.30 17.39 17.37 -4.79 111 AFI Australian Foundation 5.80 -1.53 0.52 2.97 7.09 0.40 3.45 10.62 3.45 67 AGL AGL Energy Limited 26.57 -2.06 -3.14 34.43 48.18 37.31 23.60 16.71 8.17 34 AIA Auckland Internation 6.37 -0.62 0.00 8.07 9.13 24.60 22.20 28.64 11.99 20 AIZ Air New Zealand 2.66 2.70 13.68 46.06 51.17 11.77 23.93 40.03 5.16 53 ALL Aristocrat Leisure 20.20 2.28 6.32 38.91 64.79 63.22 61.32 48.77 3.74 63 ALQ ALS Limited 5.81 -8.36 -7.78 -6.46 40.74 4.10 -3.39 -7.38 6.12 49 AMC Amcor Limited 15.00 -1.77 -1.32 6.91 -4.77 7.76 16.88 20.78 11.42 23 AMP AMP Limited 5.08 -3.61 -2.31 10.36 -2.37 -5.31 4.30 10.46 -2.30 103 ANN Ansell Limited 24.18 -0.45 4.13 10.86 33.44 -0.94 12.31 12.86 8.78 33 ANZ ANZ Banking Grp Ltd 28.50 -2.46 -5.97 4.72 20.84 -0.23 1.01 12.12 3.80 62 AOG Aveo Group 3.30 0.00 5.43 6.11 2.11 12.92 19.57 8.48 -13.15 122 APA APA Group 9.35 -0.85 3.09 27.40 8.91 7.53 17.29 18.72 12.16 18 APE AP Eagers Limited 7.95 1.92 -8.20 -11.20 -19.96 -3.78 18.44 25.11 14.35 13 ARG Argo Investments 7.61 -1.42 0.13 6.16 9.93 1.56 5.27 12.21 2.40 76 AST AusNet Services Ltd 1.75 0.86 4.48 21.63 14.27 14.32 13.81 -

Alumina Limited Annual Report 2018 Our Exposure to the Alumina Market and Price Is Unique and Makes Alumina Limited One of a Kind

ALUMINA LIMITED ANNUAL REPORT 2018 OUR EXPOSURE TO THE ALUMINA MARKET AND PRICE IS UNIQUE AND MAKES ALUMINA LIMITED ONE OF A KIND. 2 Alumina Limited is one of a kind. Its 40 per cent joint-venture interest in AWAC (Alcoa World Alumina and Chemicals) provides exposure to the most profitable part of the aluminium supply chain. The Company is uniquely positioned in the world alumina market. CONTENTS 05 About Alumina Limited 16 Directors’ Report 64 Financial Report 06 At a Glance 22 Map of Operations 93 Directors’ Declaration 08 Chairman and CEO Report 38 Letter by Chair of 94 Independent Auditor’s Report Compensation Committee 14 Sustainability 100 Financial History 40 Remuneration Report ALUMINA LIMITED ANNUAL REPORT 2018 3 Alumina Limited provides a unique opportunity for a pure investment in AWAC, one of the world’s largest bauxite and alumina producers. 4 The Annual Report is presented in US dollars, unless otherwise specified. ABOUT ALUMINA LIMITED Alumina Limited is a leading Australian company listed on the Australian Securities Exchange (ASX). Alumina Limited is the 40 per cent partner in the AWAC joint venture whose assets comprise globally leading bauxite mines and alumina refineries in Australia, Brazil, Spain, USA, Saudi Arabia and Guinea. AWAC also has a 55 per cent interest in the Portland aluminium smelter in Victoria, Australia. AWAC’s joint venture partner and operator is Alcoa Corporation. The AWAC joint venture was formed in 1994 and our relationship with Alcoa dates back to the early 1960s when Western Mining Corporation (now called Alumina Limited) began to explore bauxite deposits and other resources in the Darling Ranges of Western Australia. -

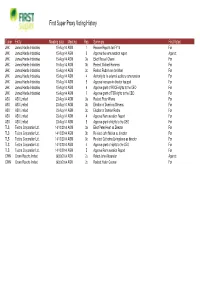

First Super Proxy Voting History

First Super Proxy Voting History Ticker Entity Meeting date Meeting Res. Summary First Voted JHX James Hardie Industries 15-Aug-14 AGM 1 Receive Reports for FY14 For JHX James Hardie Industries 15-Aug-14 AGM 2 Approve the remuneration report Against JHX James Hardie Industries 15-Aug-14 AGM 3a Elect Russell Chenu For JHX James Hardie Industries 15-Aug-14 AGM 3b Reelect Michael Hammes For JHX James Hardie Industries 15-Aug-14 AGM 3c Reelect Rudolf van der Meer For JHX James Hardie Industries 15-Aug-14 AGM 4 Authority to fix external auditors remuneration For JHX James Hardie Industries 15-Aug-14 AGM 5 Approve increase in director fee pool For JHX James Hardie Industries 15-Aug-14 AGM 6 Approve grant of ROCE rights to the CEO For JHX James Hardie Industries 15-Aug-14 AGM 7 Approve grant of TSR rights to the CEO For ASX ASX Limited 23-Aug-14 AGM 3a Reelect Peter Warne For ASX ASX Limited 23-Aug-14 AGM 3b Election of Domininc Stevens For ASX ASX Limited 23-Aug-14 AGM 3c Election of Damian Roche For ASX ASX Limited 23-Aug-14 AGM 4 Approve Remuneration Report For ASX ASX Limited 23-Aug-14 AGM 5 Approve grant of rights to the CEO For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3a Elect Peter Heart as Director For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3b Re-elect John Mullen as director For TLS Telstra Corporation Ltd. 14/10/2014 AGM 3c Re-elect Catherine Livingstone as director For TLS Telstra Corporation Ltd. -

Annual Report 2016

ANNUAL REPORT 2016 GLOBAL DIVERSIFIED INDUSTRIAL CHEMICALS OUR OPERATIONS Ekati e Diavik e e Meadowbank CANADA Flin Flon e e Ishpeming Tumbler Ridge e North Bay Calgary a Maitland Biwabik e Boisbriand Tirana St Helens a e Ormstown Bucharest Barry i Simsbury Ankara Salt Lake City USA Cheyenne e a a Soma i e Donora TURKEY Carthage i e e Duffield CHINA Louisiana, Missouri a e Van Wyck i Linyi (Fabchem) PAKISTAN Waggaman, Louisiana e Brooksville New Delhi Dinamita i i Graham Hong Kong Gomez Palacios i Wolf Lake INDIA Guadalajara e MEXICO e Muara Tuhup e Tenggarong Batu Arang (TKEB) i e Berau PAPUA NEW GUINEA SOUTH Sibolga Tanjung Tabalong e e Papua New Guinea AFRICA Jakarta Batu Kajang e INDONESIA e a Moranbah Townsville Port Hedland e LATIN Mt Isa e Moura AMERICA Phosphate Hill (Queensland Nitrates) AUSTRALIA Gibson Island Kalgoorlie e i Helidon La Serena i Kooragang Island i Johannesburg (SASOL Dyno Nobel) Perth a Santiago Port Adelaide e Warkworth i Johannesburg (DetNet) Melbourne Portland Geelong Devonport Cover photograph: New IPL World Class Ammonia Plant, Louisiana USA VISION STATEMENT To be the best in our markets, delivering Zero Harm and outstanding business performance through our people, our culture and our customer focus. Ekati e Diavik e e Meadowbank CANADA Flin Flon e e Ishpeming Tumbler Ridge e North Bay Calgary a Maitland Biwabik e Boisbriand Tirana St Helens a e Ormstown Bucharest Barry i Simsbury Ankara Salt Lake City USA Cheyenne e a a Soma i e Donora TURKEY Carthage i e e Duffield CHINA Louisiana, Missouri a e Van Wyck