PDF File Generated From

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Shrimp Fishing in Mexico

235 Shrimp fishing in Mexico Based on the work of D. Aguilar and J. Grande-Vidal AN OVERVIEW Mexico has coastlines of 8 475 km along the Pacific and 3 294 km along the Atlantic Oceans. Shrimp fishing in Mexico takes place in the Pacific, Gulf of Mexico and Caribbean, both by artisanal and industrial fleets. A large number of small fishing vessels use many types of gear to catch shrimp. The larger offshore shrimp vessels, numbering about 2 212, trawl using either two nets (Pacific side) or four nets (Atlantic). In 2003, shrimp production in Mexico of 123 905 tonnes came from three sources: 21.26 percent from artisanal fisheries, 28.41 percent from industrial fisheries and 50.33 percent from aquaculture activities. Shrimp is the most important fishery commodity produced in Mexico in terms of value, exports and employment. Catches of Mexican Pacific shrimp appear to have reached their maximum. There is general recognition that overcapacity is a problem in the various shrimp fleets. DEVELOPMENT AND STRUCTURE Although trawling for shrimp started in the late 1920s, shrimp has been captured in inshore areas since pre-Columbian times. Magallón-Barajas (1987) describes the lagoon shrimp fishery, developed in the pre-Hispanic era by natives of the southeastern Gulf of California, which used barriers built with mangrove sticks across the channels and mouths of estuaries and lagoons. The National Fisheries Institute (INP, 2000) and Magallón-Barajas (1987) reviewed the history of shrimp fishing on the Pacific coast of Mexico. It began in 1921 at Guaymas with two United States boats. -

Sea Level Rise and Land Use Planning in Barbados, Trinidad and Tobago, Guyana, and Pará

Water, Water Everywhere: Sea Level Rise and Land Use Planning in Barbados, Trinidad and Tobago, Guyana, and Pará Thomas E. Bassett and Gregory R. Scruggs © 2013 Lincoln Institute of Land Policy Lincoln Institute of Land Policy Working Paper The findings and conclusions of this Working Paper reflect the views of the author(s) and have not been subject to a detailed review by the staff of the Lincoln Institute of Land Policy. Contact the Lincoln Institute with questions or requests for permission to reprint this paper. [email protected] Lincoln Institute Product Code: WP13TB1 Abstract The Caribbean and northern coastal Brazil face severe impacts from climate change, particularly from sea-level rise. This paper analyses current land use and development policies in three Caribbean locations and one at the mouth of the Amazon River to determine if these policies are sufficient to protect economic, natural, and population resources based on current projections of urbanization and sea-level rise. Where policies are not deemed sufficient, the authors will address the question of how land use and infrastructure policies could be adjusted to most cost- effectively mitigate the negative impacts of climate change on the economies and urban populations. Keywords: sea-level rise, land use planning, coastal development, Barbados, Trinidad and Tobago, Guyana, Pará, Brazil About the Authors Thomas E. Bassett is a senior program associate at the American Planning Association. He works on the Energy and Climate Partnership of the Americas grant from the U.S. Department of State as well as the domestic Community Assistance Program. Thomas E. Bassett 1030 15th Street NW Suite 750W Washington, DC 20005 Phone: 202-349-1028 Email: [email protected]; [email protected] Gregory R. -

Observations of Pelagic Seabirds Wintering at Sea in the Southeastern Caribbean William L

Pp. 104-110 in Studies in Trinidad and Tobago Ornithology Honouring Richard ffrench (F. E. Hayes and S. A. Temple, Eds.). Dept. Life Sci., Univ. West Indies, St. Augustine, Occ. Pap. 11, 2000 OBSERVATIONS OF PELAGIC SEABIRDS WINTERING AT SEA IN THE SOUTHEASTERN CARIBBEAN WILLIAM L. MURPHY, 8265 Glengarry Court, Indianapolis, IN 46236, USA ABSTRACT.-I report observations, including several the educational cruise ship Yorktown Clipper between significant distributional records, of 16 species of Curaçao and the Orinoco River, traversing seabirds wintering at sea in the southeastern Caribbean approximately 2,000 km per trip (Table 1). Because during cruises from Bonaire to the Orinoco River (5-13 the focus was on visiting islands as well as on cruising, January 1996, 3-12 March 1997, and 23 December many of the longer passages were traversed at night. 1997 - 1 January 1998). A few scattered shearwaters While at sea during the day, fellow birders and I (Calonectris diomedea and Puffinus lherminieri) were maintained a sea watch, recording sightings of bird seen. Storm-Petrels (Oceanites oceanicus and species and their numbers. Oceanodroma leucorhoa), particularly the latter species, were often seen toward the east. Most The observers were all experienced birders with tropicbirds (Phaethon aethereus) and gulls (Larus binoculars, some of which were image-stabilised. The atricilla) were near Tobago. Boobies were common; number of observers at any given time ranged from Sula leucogaster outnumbered S. sula by about 4:1 and one to 15, averaging about five. Observations were S. dactylatra was scarce. Frigatebirds (Fregata made from various points on three decks ranging from magnificens) were strictly coastal. -

Experimental Investigations Into Manufacturing Processes

K. Hall and G. Shrivastava.: Marine Current Power Generation in Trinidad: A Case Study 15 ISSN 0511-5728 The West Indian Journal of Engineering Vol.39, No.2, January 2017, pp.15-24 Marine Current Power Generation in Trinidad: A Case Study Kashawn Hall a,Ψ, and Gyan Shrivastavab Department of Civil and Environmental Engineering, Faculty of Engineering, The University of the West Indies, St. Augustine Campus, Trinidad and Tobago, West Indies; aE-mail: [email protected] b E-mail: [email protected] Ψ Corresponding Author (Received 19 April 2016; Revised 22 August 2016; Accepted 6 December 2016) Abstract: Development of alternative energy sources has attracted worldwide interest given the adverse effects of fossil fuels on the global climate as well as its unsustainability. It is in this context that this report examines the feasibility of marine power generation at the 14 km wide Serpent’s Mouth in Trinidad. It is part of the narrow Columbus Channel which lies between Trinidad and Venezuela. At this location, depth varies between 30 - 48 m and a marine current of approximately 1.5 m/s suggests the possibility of generating power through submerged turbines.The conditions are similar to those at Strangford Lough in the Irish Sea, where the world’s first marine current turbine was installed in 2008 for generating 2 MW of power. After taking into account the technical, environmental, and economic factors, this paper concludes it is feasible to use The Serpent’s Mouth location for Power Generation. Keywords: Columbus Channel, Marine Current Turbines (MCTs), Power Generation, Marine Renewable Energy (MRE) 1. -

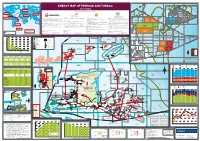

View the Energy Map of Trinidad and Tobago, 2017 Edition

Trinidad and Tobago LNG export destinations 2015 (million m3 of LNG) Trinidad and Tobago deepwater area for development 60°W 59°W 58°W Trinidad and Tobago territorial waters ENERGY MAP OF TRINIDAD AND TOBAGO 1000 2000 m m 2017 edition GRENADA BARBADOS Trinidad and Tobago 2000m LNG to Europe A tlantic Ocean 2.91 million m3 LNG A TLANTIC Caribbean 2000m 20 Produced by Petroleum Economist, in association with 00 O CEAN EUROPE Sea m Trinidad and Tobago 2000m LNG to North America NORTH AMERICA Trinidad and Tobago 5.69 million m3 LNG LNG to Asia 3 GO TTDAA 30 TTDAA 31 TTDAA 32 BA 1.02 million m LNG TO Trinidad and Tobago OPEN OPEN OPEN 12°N LNG to MENA 3 1.90 million m LNG ASIA Trinidad and Tobago CARIBBEAN TRINIDAD AND TOBAGO 2000m LNG to Caribbean Atlantic LNG Company profile Company Profile Company profile Company Profile 3 Established by the Government of Trinidad and Tobago in August 1975, The National Gas Company of Trinidad and Tobago Limited (NGC) is an BHP Billiton is a leading global resources company with a Petroleum Business that includes exploration, development, production and marketing Shell has been in Trinidad and Tobago for over 100 years and has played a major role in the development of its oil and gas industry. Petroleum Company of Trinidad and Tobago Limited (Petrotrin) is an integrated Oil and Gas Company engaged in the full range of petroleum 3.84 million m LNG internationally investment-graded company that is strategically positioned in the midstream of the natural gas value chain. -

Hydrographic Data As Indicators of Physical Development on the Trinidad West Coast

Hydrographic Data as Indicators of Physical Development on the Trinidad West Coast David NEALE, Republic of Trinidad and Tobago Key words: Coastal Area Planning, Hydrography, and Environmental Assessment. SUMMARY In Trinidad, physical development is concentrated on the west coast along the Gulf of Paria. The development pattern includes a wide range of use including towns and villages, oil and gas development, manufacturing and commercial ports. In order to satisfy the country’s need to document the state of its environment, including the marine environment, all available data were reviewed to ascertain the potential of these data to describe, monitor and predict environment change. Hydrographic data are among the data sets reviewed. These data collected mainly by private sector enterprises are generally concentrated on areas of high physical development. They include bathymetry, ship traffic and coastal circulation. While the collection of these data are not designed for or specific to environmental monitoring, they serve to indicate in spatial terms, areas of marine development activity. For the 156km-long Trinidad West Coast, the review revealed three (3) areas of special attention. The identification of these ‘special attention areas’ allows the State to direct limited resources, such as obtains in Small Island Developing States like the Republic of Trinidad and Tobago, towards surveys that can be managed to include specific data collection and reporting regulations. Workshop – Hydro 1/11 WSH2 – Marine Cadastre / CZM David Neale WSH2.3 Hydrographic Data as Indicators of Physical Development on the Trinidad West Coast FIG Working Week 2004 Athens, Greece, May 22-27, 2004 Hydrographic Data as Indicators of Physical Development on the Trinidad West Coast David NEALE, Republic of Trinidad and Tobago 1. -

Studies in Trinidad and Tobago Ornithology Honouring Richard Ffrench

STUDIES IN TRINIDAD AND TOBAGO ORNITHOLOGY HONOURING RICHARD FFRENCH Edited by Floyd E. Hayes and Stanley A Temple Occasional Paper # 11 Department of Life Sciences, University of the West Indies, St. Augustine, Trinidad STUDIES IN TRINIDAD AND TOBAGO ORNITHOLOGY HONOURING RICHARD FFRENCH Editors: FLOYD E. HAYES Department ofLife Sciences, University of the West Indies, St. Augustine, Trinidad and Tobago STANLEY A. TEMPLE Department of Wildlife Ecology, University of Wisconsin, Madison, WI 53706, USA Occasional Paper #11 Department of Life Sciences University of the West Indies, St. Augustine Trinidad 2002 OCCASIONAL PAPERS OF THE DEPARTMENT OF LIFE SCIENCES, UNIVERSITY OF THE WEST INDIES, ST. AUGUSTINE, TRINIDAD This series has been established for the publication of major papers on the natural history of Trinidad and Tobago. Initiated in 1978 as 'Occasional Papers of the Department of Zoology, University of the West Indies, St. Augustine, Trinidad', the change in name reflects the merger of the Departments of Zoology, Plant Sciences and Biochemistry in 1996. Correspondence concerning manuscripts for publication in the series should be sent to the series editor, Mary Alkins-Koo, Department of Life Sciences, University of the West Indies, St. Augustine, Trinidad and Tobago. Inquiries regarding availability and purcl1ase of publications, listed below, should be addressed to the Secretary, Department of Life Sciences, University of the West Indies, St. Augustine, Trinidad and Tobago. 1. BACON, P. R .. 1978. An annotated bibliography to the fauna (excluding insects) of Trinidad and Tobago 1817-1977.177 pp. 2. ALKlNS, M. E. 1979. The mammals of Trinidad. 75 pp. 3. MOOTOOSlNGH, S. N. 1979. The growth of conservation awareness in Trinidad and Tobago (1765-I 979). -

Trinidad and Tobago National Report

NATIONAL REPORT ON Integrating The Management of Watersheds and Coastal Areas in Trinidad and Tobago Prepared by The Water Resources Agency for The Ministry of the Environment Eric Williams Financial Complex Independence Square, Port of Spain March 2001 WRA/MIN. Env: Integrating the Management of Watersheds and Coastal Areas in Trinidad and Tobago i EXECUTIVE SUMMARY The Republic of Trinidad and Tobago is an archipelagic state located at the southern end of the Caribbean island chain. The islands have a tropical wet climate of the monsoonal type. Rainfall that averages 2,200 millimetres, is seasonal with a wet season from June to November and a dry season from December to May. Temperatures range from 25 to 27 °C, humidity ranges between 50 to 100% and wind speed averages between 20 and 28 km/hr. Trinidad's landscape is characterised by steep mountains, undulating hills and plains. Tobago's landscape is however, characterised by a highland area, which runs through the island and a small coastal plain. The islands are endowed with extremely varied coastlines, a fair share of wetlands and richly diverse flora and fauna. The population is estimated at 1.25 million with an annual growth rate of 1.2 percent. Trinidad's population is concentrated in urban areas along the west coastal areas and at the foothills of its northerly located mountain range. On the other hand, Tobago's population is concentrated in the southwest part of the island. Relative to the rest of the Caribbean islands the country is highly industrialised with a petroleum based economy and a small but rapidly growing tourism industry concentrated mainly in Tobago. -

Submission to the Commission on the Limits of the Continental Shelf

SUBMISSION TO THE COMMISSION ON THE LIMITS OF THE CONTINENTAL SHELF PURSUANT TO ARTICLE 76, PARAGRAPH 8 OF THE UNITED NATIONS CONVENTION ON THE LAW OF THE SEA Republic of Trinidad and Tobago PART I: EXECUTIVE SUMMARY Trinidad and Tobago Continental Shelf Submission Executive Summary TABLE OF CONTENTS 1. INTRODUCTION...............................................................................................................................................................1 2. TRINIDAD AND TOBAGO AS A STATE PARTY TO UNCLOS ............................................................................................3 3. TIMELINESS OF THE SUBMISSION....................................................................................................................................4 4. MEMBERS OF THE CLCS WHO PROVIDED ADVICE IN THE PREPARATION OF THE SUBMISSION ........................................4 5. FULL SUBMISSION ..........................................................................................................................................................5 6. STATE BODIES RESPONSIBLE FOR THE PREPARATION OF THE SUBMISSION ....................................................................5 7. EXTERNAL EXPERTS AND ORGANIZATIONS INVOLVED IN THE PREPARATION OF THE SUBMISSION................................5 8. RELEVANT BASELINES....................................................................................................................................................6 9. UNIQUE TREATY-BASED COMPETENCE OF THE CLCS.....................................................................................................8 -

By Kevin Jeanville

Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION By Kevin Jeanville Edited by: Shenelle L. Jeanville B.Sc. (Chemistry) Caribbean Tutorial Publishing Company Limited i Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION Caribbean Tutorial Publishing Company Limited Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission of the copyright owner. ©Kevin Jeanville First Printed 2015 Printed and Published by: Caribbean Tutorial Publishing Company Limited Pointe-à-Pierre Road, San Fernando Trinidad, West Indies. Telephone: +1(868) 653-1166 Agent: Mohammed’s Book Store (1988) Ltd. Marc Street, Chaguanas – (868) 665-2959 High Street, Princes Town – (868) 655-2915 Penal Junction – (868) 647-4786 Also Michael Mohammed’s Book Store Pointe-à-Pierre Road, San Fernando – (868) 653-1166 ii Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION PREFACE “Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION”, has been designed for pupils to achieve the objectives of the new Social Studies Syllabus in accordance with the requirements of the Secondary Entrance Assessment (S.E.A.) Examination. The text reflects Trinidad and Tobago’s trend toward standards based curricula and the author takes the position on what I believe constitutes the key issue. The text aims at culturally responsive teaching with a focus on enhanced quality of instruction for diverse learners. “Trinidad & Tobago Social Studies for Primary School: Standard 3 PCR EDITION”, has three overarching goals: 1. -

By Shenelle L. Jeanville

By Shenelle L. Jeanville Caribbean Tutorial Publishing Company Limited Trinidad & Tobago Social Studies for Primary School: Standard 3 Workbook – PCR Edition Caribbean Tutorial Publishing Company Limited Trinidad & Tobago Social Studies for Primary School: WORKBOOK 3 - PCR Edition All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission of the copyright owners. ©Shenelle L. Jeanville First Printed 2016 Printed and Published by: Caribbean Tutorial Publishing Company Limited Pointe-à-Pierre Road, San Fernando Trinidad West Indies. Telephone: +1(868) 653-1166 Agent: Mohammed’s Book Store (1988) Ltd. Marc Street, Chaguanas – (868) 665-2959 High Street, Princes Town – (868) 655-2915 Penal Junction – (868) 647-4786 Also Michael Mohammed’s Book Store Pointe-à-Pierre Road, San Fernando – (868) 653-1166 Trinidad & Tobago Social Studies for Primary School: Standard 3 Workbook – PCR Edition Preface The aim of the “Trinidad & Tobago Social Studies Workbook for Primary School: Workbook 3 – PCR Edition” is to challenge students in their understanding of the objectives of the new Social Studies Syllabus, which aligns with the Secondary Entrance Assessment (S.E.A.) Examination. It also aims to cultivate the twenty-first (21st) century skills in students, as prescribed by the Ministry of Education, that are needed to mould future leaders, inclusive of Aesthetic Expression, Technological Competency, Citizenship and Communication. In conjunction with the “Trinidad & Tobago Social Studies for Primary School: Workbook 3”, this workbook is able to reach pupils via two (2) main learning styles: visual and kinaesthetic, thus honing their cognitive faculties, such as reasoning, judgement and perception, within a local context. -

The Contribution of Trinidad and Tobago to the Development of the Regime of the Continental Shelf

THE CONTRIBUTION OF TRINIDAD AND TOBAGO TO THE DEVELOPMENT OF THE REGIME OF THE CONTINENTAL SHELF Anthony A. Lucky It is both a privilege and honor to have this article included in the Liber Amicorum for a distinguished scholar, jurist, professor of law and judge of the International Tribunal for the Law of the Sea. Th e paper exam- ines the development of the regime of the continental shelf from an historical perspective. It considers the beginning of the legal aspects of the regime emanating from the Gulf of Paria Treaty 1942. Th e paper then assesses the development and contribution to the regime by Trinidad and Tobago, a country which recognizes that the commercial production of oil and gas is inevitably subject to laws and regulations, nationally and internationally, because of the value and eff ect this resource has on the economy of any oil producing country; moreso, where a very large percentage of oil and gas is extracted from its conti- nental shelf. A. Introduction Rapid global development of the regime of the continental shelf may not have been easily envisaged in the 1930s when the exploration for oil and gas had extended to the sub-marine areas of some coastal states. Th e literature and articles on legal aspects of the regime are volumi- nous as national and international jurists continue to examine and consider new developments in science and technology as they relate to global submarine exploitation. In examining the contribution of Trinidad and Tobago in the devel- opment of the regime of the continental shelf, an historical perspec- tive of the twin island Republic has to be viewed.