Trinity Mills Station Market Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bringing Regional Rail Service to the Historic Cotton Belt Corridor DART Current and Future Rail Services

SILVER LINE REGIONAL RAIL GROUNDBREAKING COMMEMORATIVE EDITION Bringing Regional Rail Service to the Historic Cotton Belt Corridor DART Current and Future Rail Services NW PLANO PARK & RIDE PLANO PARKER ROAD To Denton JACK HATCHELL DOWNTOWN PLANO TRANSIT CTR. Preside SHILOH nt G 12TH STREET ROAD e sh Turnpike (future) o r g e Bu Dallas North Tollway CITYLINE/BUSH NORTH CARROLLTON/FRANKFORD UT DALLAS GALATYN PARK TRINITY MILLS CARROLLTON ADDISON KNOLL TRAIL RICHARDSON ARAPAHO CENTER Map Legend DOWNTOWN CARROLLTON ADDISON CYPRESS WATERS TRANSIT CTR. DFW (DALLAS) SPRING VALLEY MapTo FortLegendBlue Worth Line AIRPORT FARMERS NORTH BRANCH Red Line DOWNTOWN Blue Line FARMERS BRANCH GARLAND GARLAND LBJ/CENTRAL Map LegendGreenDFW Line DFW DOWNTOWN Red Line ROWLETT AIRPORT AIRPORT FOREST LANE FOREST/JUPITER OrangeBlueTerminal Line B Line Terminal A Green Line HIDDEN ROYAL LANE LBJ/SKILLMAN Orange Line BELT LINE ROWLETT Red Line RIDGE Map Legend LAKE HIGHLANDS Weekdays Peak Only (future) WALNUT OrangeDFW Line IRVING CONVENTION WALNUT HILL/DENTON HILL TrinityGreen RailwayLine Express CENTER Blue Line (No Sunday Service) PARK LANE Lake Ray Orange Line NORTH LAKE LAS COLINAS S. GARLAND Hubbard Orange Line COLLEGE Red Line TRANSIT CTR. TEXRailWeekdays (Trinity Peak Metro) Only URBAN CENTER UNIVERSITY WHITE ROCK LOVERS A-Train (DCTA) Green Line BACHMAN OrangeTrinity Line Railway Express UNIVERSITY OF DALLAS PARK LANE Weekdays Peak Only (No Sunday Service) LOVE FIELD White Rock M-Line Trolley VIA BUS 524 HIGHLAND LAKE RAY Orange Line Lake TrinityTEXRail Railway (Trinity Express Metro)Inset Map LOOP 12 BURBANK PARK HUBBARD Dallas(No Sunday Streetcar Service) (future) INWOOD/LOVE FIELD SMU/MOCKINGBIRD TRANSIT CTR. -

Richland Hills Trinity Railway Express (TRE) Station Transit Oriented Development Plan R ICHLAND H ILLS TRE S TATION TOD P LAN

RICHLAND HILLS TRINITY RAILWAY EXPRESS (TRE) STATION TRANSIT ORIENTED DEVELOPMENT PLAN R ICHLAND H ILLS TRE S TATION TOD P LAN Richland Hills Trinity Railway Express (TRE) Station Transit Oriented Development (TOD) Plan June 2009 R ICHLAND H ILLS TRE S TATION TOD P LAN ACKNOWLEDGEMENTS North Central Texas Council of Governments Ronny Region, Commissioner st Karla Weaver, AICP, Senior Transportation Planner Greg Klarich, 1 Alternate nd Alma Martinez, Transportation Planner Kellie Starnes, 2 Alternate Staron Faucher, Transportation Planner Fort Worth Transportation Authority Natalie Bettger, Senior Program Manager Curvie Hawkins, Director of Planning Emily Beckham, Grants Coordinator Ken Frost, Vice President, Project Management City of Richland Hills City Administration Consultant Team Mayor David L. Ragan URS Transit and Urban Design Studio: James W. Quin, City Manager Tim Baldwin, AICP, URS Corporation Michael H. Barnes, P.E., Public Works Director Mark Leese, AIA, AICP, URS Corporation Denice Thomas, Planning Director Krista Kahle, AICP, URS Corporation Matthew Shaffstall, Economic Development Jennifer Hall, AICP, URS Corporation City of Richland Hills City Council Jennifer McNeil, AICP, URS Corporation Mayor Pro Tem Jeff Ritter, Council Place 1 Shari Frank, AICP, URS Corporation Council Member Kenney Davis, Council Place 2 Andrea Snyder, URS Corporation Council Member Phil Heinze, Council Place 3 Lonnie Blaydes, Lonnie E. Blaydes Consulting Council Member Don Acker , Council Place 4 Dennis Wilson, Townscape, Inc. Council Member Larry -

KIRK MILLICAN, AIA, LEED AP Senior Vice President | Principal-In-Charge

KIRK MILLICAN, AIA, LEED AP Senior Vice President | Principal-In-Charge EDUCATION Since joining HOK in 1979, Kirk has had a varied background as project designer, manager, Washington University and architect for a broad range of project types including architectural and urban design, Bachelor of Architecture, 1973 transportation, regional and campus planning, justice design and interior design. As Principal-in-Charge and Project Manager, Kirk has managed multiple transportation, public, Washington University educational, institutional and justice projects. Master of Architecture, 1976 PROFESSIONAL REGISTRATIONS EXPERIENCE Architect - Texas; Interior Design - Texas; Fort Worth Urban Villages - Southwest Houston METRO Downtown Transit Center LEED Accredited Professional Cluster Station Fort Worth, Texas Houston, Texas MEMBERSHIPS American Institute of Architects Dallas Area Rapid Transit (DART) Houston METRO Museum District Station Interiors Committee, 1990-1994 Light Rail Station Prototypical Design Houston, Texas Interiors Committee National Chairman, Dallas, Texas 1994 Fort Worth Transportation Authority (FWTA) DART Cedars Station Downtown Commuter Rail Corridor Texas Society of Architects Dallas, Texas Fort Worth, Texas Interior Architecture Committee Chairman, 1986-1991 DART Union Station FWTA Intermodal Transportation Center Dallas, Texas Fort Worth, Texas City of Fort Worth Downtown Design Review Board, 2007-2009; Chairman, 2009 DART Convention Center Station FWTA T&P Station Dallas, Texas Fort Worth, Texas Arts Council of Fort Worth and Tarrant County, Board of Directors, 1995-2001; Ex DART Mockingbird Station FWTA Alarm Supply Building Preservation Officio, 2007-2009 Dallas, Texas Fort Worth, Texas City of Fort Worth Art Commission, Vice DART Commuter Rail Maintenance Facility 600 Las Colinas Area Personal Transit Chair, 2003-2006; Chair, 2007-2009 Irving, Texas Station Las Colinas, Texas James L. -

Northwest Corridor

NORTHWEST CORRIDOR NORTHWEST CORRIDOR AT A GLANCE tunnel miles elevated miles 13,900 48,000 2004-10 12 at-grade Weekday Riders Jobs Within 1/2 Mile of Stations Phased Openings Total Stations 17.4 0.3 41minutes 1 $700m 17.4 miles 8.4 Downtown Dallas to Airport Connection at Federal Funding for Combined Downtown Dallas to 8.7 N Carrollton/Frankford Station Inwood/Love Field Station NW/SE Project N Carrollton/Frankford Station 0% 48% MILES AT-GRADE 50% 8.7 DAILY STATION RIDERSHIP**Average Weekday FY18 MILES ELEVATED 3,000 8.4 2,500 2,000 MILES 1,500 BELOW-GRADE 0.3 1,000 500 0 MARKET VICTORY INWOOD/ BURBANK CENTER BACHMAN DENTON ROYAL LANE DOWNTOWN LOVE FIELD WALNUT HILL/ TRINITY MILLS FRANKFORD SMD/PARKLAND CARROLLTON FARMERS BRANCH N. CARROLLTON/ PROJECT TIMELINE SERVICE CHARACTERISTICS FEBRUARY NOVEMBER NORTHWEST 2000 2004 LOCALLY PREFERRED FIRST 1.2 MILES GREEN LINE 7.5-MINUTE COMBINED ALTERNATIVE OPENS TO VICTORY 15-MINUTE PEAK HEADWAY APPROVED STATION PEAK (GREEN/ORANGE) HEADWAY SOUTH OF BACHMAN ORANGE LINE BUS INTERFACE AT 15-MINUTE ALL STATIONS 2010 PEAK HEADWAY 2000 2003 2004 2006 TO PARKER RD STATION OCTOBER JULY DECEMBER ORANGE LINE JUNCTION 2003 2006 2010 20-30 MINUTE AT BACHMAN STATION FEIS PUBLISHED FTA AWARDS GREEN LINE OFF-PEAK $700M GRANT FOR OPENS HEADWAY COMBINED NW/SE PROJECT TRE AT VICTORY STATION DID YOU KNOW? The Northwest Corridor provides direct access to Parkland Hospital and serves the largest medical district in the DFW region, UTSW Medical District. REV. 03/19 STATION HIGHLIGHTS VICTORY • AMERICAN AIRLINES CENTER • PEROT MUSEUM OF NATURE & SCIENCE A-Train to Denton (operated by DCTA) NW PLANO PARK & RIDE PLANO MARKET CENTER • DALLAS MARKET CENTER P • INFOMART PARKER ROAD JACK HATCHELL TRANSIT CTR. -

Doug Allen-Dallas

The DART Perspective Doug Allen Executive Vice President Program Development Dallas Area Rapid Transit Why DART? • Growing Mobility Problems • “World Class” Image • Vision 9 Fixed Guideway 9 Multi-modal 9 Regional Mobility History • DART was created to implement a vision 9 Fixed Guideway 9 Multi-modal • We had some problems along the way 9 Local economy 9 Public input 9 Political support 9 Credibility 9 Failure of Bond Referendum History • 1983 – DART established • 1988 – Bond referendum failure • 1989 – New Directions System Plan campaign • 1992 – Rail construction begins • 1996 – Opening of LRT Starter System • 2000 – Long term debt package passed • 2001-02 – Opening of extensions • 2006 – $700 Million FFGA The Mission To build and operate a safe, efficient and effective transportation system that, within the DART Service Area, provides mobility, improves the quality of life, and stimulates economic development. FY 2006 Ridership by Mode 36.1 Million 18.6 Million 18% 36% 44% 2% 2.4 Million 44.3 Million System Overview THE DART SYSTEM BUS • Provides area-wide coverage 9 700 square miles 9 Over 100 routes • Flexible 9 Local 9 Express 9 Crosstown 9 Feeders 9 Paratransit 9 Innovative services • Carries 44.3 million riders/year (FY ’06) System Overview THE DART SYSTEM Light Rail • Provides high capacity, quality transit within busiest corridors 9 20 mile Starter System 9 Additional 25 miles in 2002-3 9 Another 48 miles in planning & design • Benefits include 9 Service Reliability 9 Consistent time savings 9 Attracts new users 9 Stimulates -

DFW Industrial Marketview

MARKETVIEW Dallas/Fort Worth Industrial, Q4 2018 Demand tops 20 million sq. ft. for third consecutive year. 6.0% 14,513,927 SF 8,273,325 SF 7,108,176 SF Figure 1: DFW Industrial Market *Arrows indicate trend from previous quarter. MSF Vacancy Rate (%) 30 7 25 20 15 6 10 5 0 5 2013 2014 2015 2016 2017 2018 Total Net Absorption Delivered Construction Construction Starts Total Vacancy Source: CBRE Research, Q4 2018. SUPPLY AND DEMAND REMAIN BALANCED PRODUCT PIPELINE CONTRACTS SUBSTANTIALLY MARKET-WIDE VACANCY RATE REMAINS SNUG Q4 2018 CBRE Research © 2019 CBRE, Inc. | 1 MARKETVIEW DALLAS/FORT WORTH INDUSTRIAL Figure 2: DFW Industrial Market Snapshot Net Direct Total Q4 2018 Q4 2018 2018 Avail. Direct Total Rentable Available Vacancy Vacancy Direct Net Total Net Total Market Rate Vacancy Vacancy Area (SF) Rate Rate Absorption Absorption Absorption (%) (SF) (SF) (SF) (%) (%) (SF) (SF) (SF) DFW Airport 76,537,446 7,143,995 9.3 4,981,889 6.5 5,496,992 7.2 1,021,613 1,093,964 2,816,521 East Dallas 36,711,061 3,247,617 8.8 1,640,650 4.5 1,674,582 4.6 455,405 421,473 323,735 Northeast Dallas 98,857,581 7,721,313 7.8 4,920,189 5.0 5,634,661 5.7 749,356 666,538 1,314,114 Northwest Dallas 110,278,941 6,873,465 6.2 4,158,527 3.8 4,433,034 4.0 360,646 333,645 1,007,725 South Dallas 77,278,616 13,465,000 17.4 12,086,981 15.6 12,226,952 15.8 1,206,291 1,254,279 5,847,155 South Stemmons 116,757,096 7,800,940 6.7 4,460,334 3.8 4,759,216 4.1 (375,470) (376,688) (1,290,388) Great SW/Arlington 111,266,798 8,018,274 7.2 5,043,620 4.5 5,140,768 4.6 2,566,998 2,601,478 7,293,671 North Ft. -

Tarrant County New Construction & Proposed Multifamily Project

Tarrant County New Construction & Proposed Multifamily Project ID PROJECT NAME UNITS 61 Viridian II 343 1 Elan Crockett Row 380 62 The Carter 275 2 Shelby at Northside 300 63 Haven at Mansfield 257 3 Magnolia at University Heights 117 64 Ballpark Lofts 280 4 The Palmer 46 65 Talos Holdings Development 200 5 The Chisholm at Tavolo Park 387 66 Bridgeview Real Estate Development 320 6 Alta Champions Circle 286 67 The Kent 248 7 The Silverlake 371 68 The Holston II 255 10 8 The Preserve 399 9 The Dylan I 227 10 Trophy Ridge 88 11 Alleia at Presidio 231 12 Cortland Riverside 374 13 Domain at Founders Parc 285 14 Aura Benbrook 301 15 26 @ City Point 270 16 The Trails at Summer Creek 240 17 Rocklyn 274 18 The Cooper 390 19 Presidio at River East 140 20 35 West at Champions Circle 300 6 21 Broadstone Southside 179 20 22 The Westhouse 318 23 Standard at River District 293 24 The Jameson 387 68 25 62 25 Wallis & Baker 432 29 26 Ramble & Rose 285 57 7 27 The George 397 22 59 28 Gates at Meadows Place 208 33 29 The Holston I 265 11 30 Hangar 19 351 38 8 31 Jefferson River East 400 32 The Jackson 340 12 34 33 Presidium Revelstoke 408 40 41 13 34 The Millennium at HomeTown 306 15 30 61 35 CoHo 54 55 36 The Truman Arlington Commons 358 32 37 Broadway Chapter 242 44 38 Avilla Fossil Creek 112 53 23 36 39 Burnett Lofts 245 4 43 64 40 Iron Horse Heights 328 28 41 The Stream at High Pointe I 270 42 60 42 Metro West 282 45 27 65 2 43 The Mark at Weatherford 355 19 44 Jefferson North Collins 346 14 24 31 45 The Elm at River Park 293 17 46 The Julian at South -

Learn More About Ray Mach by Scanning the QR Code!

RAY MACH - ACTIVITY LAST 12 MONTHS Area Listing Price Address Agency Date McKinney $450,000 8305 Desert Dunes Trl Buying Agent 8/19/21 Downtown/Uptown $949,999 2011 Cedar Springs Rd #307 Buying Agent 8/6/21 Frisco $2,505,000 12310 Harvest Meadow Dr Buying Agent 7/29/21 Plano $396,678 4520 Miami Dr Buying Agent 7/26/21 Frisco $399,900 4241 Armistice Dr Buying Agent 7/19/21 Uptown $195,000 4241 Buena Vista St #18 Listing Agent 7/14/21 Northwood Hills $700,000 6720 Mossvine Pl Listing Agent 7/9/21 Northwest Dallas $315,000 4310 Rosser Sq Listing Agent 7/2/21 Northwest Dallas $575,000 4065 Deep Valley Dr Listing Agent 6/30/21 Northwest Dallas $3,250 4064 Boca Bay Dr Lease Listing Agent 6/30/21 Ray Mach x Lantana $425,000 1080 Noble Ave Referral Agent 6/11/21 CEO, Founder, Broker & Realtor© Northwest Dallas $355,000 3220 Dothan Ln Buying Agent 6/11/21 America’s Top 100 Real Estate Agents - Top 1% McKinney $264,900 2613 Mountain View Dr Buying Agent 6/8/21 (2020-2021) North Dallas $225,000 5565 Preston Oaks #237 Buying Agent 6/3/21 North Dallas $225,000 5565 Preston Oaks #237 Listing Agent 6/3/21 TOP 100 MOST INFLUENTIAL AGENTS IN TEXAS 2017 Celina $450,000 717 Corner Post Path Listing Agent 5/28/21 TOP 100 MOST INFLUENTIAL AGENTS IN N TEXAS 2016 East Dallas $2,750 6418 E Lovers Ln Tenant Agent 5/25/21 PLATINUM PRODUCER, TOP PRODUCER, East Dallas $2,750 6418 E Lovers Ln Lease Listing Agent 5/25/21 “VOTED ONE OF DALLAS’ BEST” Preston Hollow $1,395 10753 Villager Rd Apt A Tenant Agent 5/25/21 Preston Hollow $1,395 10753 Villager Rd Apt A Lease -

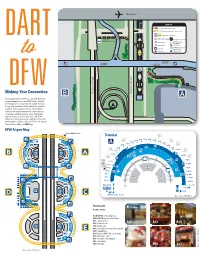

Making Your Connection

DART Rail System Map DOWNTOWN ROWLETT DFW AIRPORT STATION Open 2014 Irving Convention Center Belt Line Making Your Connection During peak times (4:30-7 a.m. and 2:15-5:30 p.m. weekday departures from DFW Airport Station), the Orange Line travels from the station through Irving, into downtown Dallas and to the northern terminus of the system at Parker Road Station in Plano. Off-peak, it follows the same path but terminates at LBJ/Central Station. Select late- night Orange Line trains will travel from DFW Exploring Airport Station to downtown; from there they will Popular Destinations go through Deep Ellum and end at Fair Park Station. Check out schedules at DART.org. DART DFW Airport Map Convention Center District. One of the largest in the nation, the Kay Bailey Hutchison (Dallas) Convention Center hosts major national and international conventions, meetings, antique and Exit to DART Station Terminal auto shows, and other events. The Omni Dallas Hotel is connected to it via sky bridge. Convention Center Station Fair Park. The largest collection of Art Deco exhibit buildings in the U.S., Fair Park is a historical treasure that plays host to the State Fair of Texas®. Other attractions include the Heart of Dallas Bowl football game and year-round museums. Fair Park Station Dallas Arts District. The Dallas Arts District is the largest arts district in the nation, spanning 68 acres and comprising Entry numerous venues of cultural as well as architectural from distinction. Pearl/Arts District Station DART Omni Dallas Hotel Station NorthPark Center. Shoppers from all over the world are drawn to NorthPark’s one-of-a-kind collection of luxury and fashion-forward retailers. -

History of Mass Transit

A NEW WAY TO CONNECT TO TRAVEL Ryan Quast Figure 1.1 A NEW WAY TO CONNECT TO TRAVEL A Design Thesis Submitted to the Department of Architecture and Landscape Architecture of North Dakota State University By Ryan Quast In Partial Fulfillment of the Requirements for the Degree of Master of Architecture Primary Thesis Advisor Thesis Committee Chair May 2015 Fargo, North Dakota List of Tables and Figures Table of Contents Figure 1.1 Train entering COR station 1 Cover Page................................................................................................1 Taken by author Signature Page....................................................................................... ...3 Figure 1.2 Northstar commuter train 13 Table of Contents......................................................................................4 www.northstartrain.org Tables and Figures....................................................................................5 Thesis Proposal.....................................................................................10 Figure 2.1 Render of The COR 15 Thesis Abstract............................................................................11 coratramsey.com/node/23 Narrative of the Theoretical Aspect of the Thesis..................12 Figure 2.2 Development plan for COR 15 Project Typology.........................................................................13 coratramsey.com/sites/default/files/COR-Development-Plan-6.0.pdf Typological Research (Case Studies)...................................................14 -

DART Rail Expansion: Orange Line

1 Timothy H. McKay, P.E. Executive Vice President, Growth and Regional Development Dallas Area Rapid Transit American Society of Civil Engineers of Dallas November 12, 2012 Opened July 30: Orange Line •5 miles • 3 stations • University of Dallas • Las Colinas Urban Center • Irving Convention Center • Design/Build Contract DART Rail Expansion: Orange Line • 9 miles • 3 stations • Orange Line to North Lake College and Belt Line opens Dec. 2012 • Orange Line to DFW Airport opens 2014 DFW Station DFW Station Architectural DFW Station Pedestrian Concept Walkway $8 Billion in Current, Planned & Projected TOD Mockingbird Station Cedars Station Downtown Plano Victory Station Station New CNG Buses Safety & Security Campaign “On the Go, In the Know” New Tools For Riders of All Modes DART Rail Expansion: Blue Line • Extension south to University of North Texas at Dallas • 3 miles • Planned for 2016 Future Dallas Streetcar Line Dallas is building a 1.6- mile streetcar line that will be expanded to serve neighborhoods around the city center. source: Dallas 360 Plan 14 Project Overview • 1.7 mile Single Track • Design/Build Delivery • Off-wire operation across bridge • Connection to DART LRT near Union Station • Vehicles compatible with DART LRT System Union Station to Oak Cliff Streetcar Tiger Project Unique Partnership – City of Dallas: Project Owner – NCTCOG: Federal Grantee – DART: Owner’s Technical Representative – Federal Transit Administration (Federal Partner) – Design-Build Team • Stacy Witbeck / Carcon – Vehicle Manufacturer Union Station -

System Map 551 829 HOPKINS R DFW AIRPORT STATION @ 500 LEWISVILLE 987

LAKE LEWISVILLE 346 348 EXCHANGE PKWY 348 LEGACY DR PARKWOOD SH 121 SHOPS AT 452 348 452 LEGACY 346346 LEGACY DR TENNYSON 347 P 183 451 208 NORTH PLANO NORTHWEST PLANO DART ON-CALL ZONE PARK AND RIDE 183, 208, 346, 347, PRESTON RD 348, 451, 452 SPRING CREEK PKWY 452 SPRING CREEK PKWY 829 LAKESIDE US-75 N. CENTRAL EXPWY. COLLIN COUNTY MARKET COMMUNITY 350 COLLEGE JUPITER RD 350 TEXAS HEALTH 451 PLANO RD PRESBYTERIAN HOSPITAL PLANO PARKER RD 452 R RD COMMUNICATIONS 347 PARKER RD PARKER ROAD STATION PARKE 350, 410, 452 183 PRESTON RD. DART ON-CALL, TI Shuttle, Texoma Express 410 CUSTER RD SHOPS AT RD COIT PARK BLVD INDEPENDENCE PARK BLVD CREEK WILLOWBEND 410 ALMA ARBOR 531 347 PARK BLVD PARK BLVD CHEYENNE 870 451 BAYLOR MEDICAL CTR. 18TH 870 AT CARROLLTON HEBRON PLANO DOWNTOWN PLANO STATION MEDICAL CENTER 870 FLEX 208 OF PLANO 15TH 15TH OHIO 14TH IN T PARKWOOD E 350 R 13TH 870 N A PLANO PKWY TI 210 COLLIN CREEK MALL ON JACK HATCHELL TRANSIT CENTER FM 544 AL P KWY 841 210, 350, 451, 452, 841 FLEX SH-121 347 210 BAYLOR REGIONAL 870 MEDICAL CTR. K AVE 843 843 ROSEMEADE PKWY 534 841 PLANO PKWY PLANO PKWY HEBRON to Denton (operated by DCTA) 841 531 347 841 MARSH LUNA 350 410 WAL-MART 883 Fri/Sun 841841 ROUND GROVE NPIKE NORTH STAR RD TIMBERGREEN H TUR NORTH CARROLLTON/FRANKFORD STATION P S BUSH TURNPIKE STATION 333 U 883 UTD Shuttle, 841-843 FLEX PEAR RIDGE PEAR B IH-35E STEMMONS FRWY.