World Bank Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mozambique Zambia South Africa Zimbabwe Tanzania

UNITED NATIONS MOZAMBIQUE Geospatial 30°E 35°E 40°E L a k UNITED REPUBLIC OF 10°S e 10°S Chinsali M a l a w TANZANIA Palma i Mocimboa da Praia R ovuma Mueda ^! Lua Mecula pu la ZAMBIA L a Quissanga k e NIASSA N Metangula y CABO DELGADO a Chiconono DEM. REP. OF s a Ancuabe Pemba THE CONGO Lichinga Montepuez Marrupa Chipata MALAWI Maúa Lilongwe Namuno Namapa a ^! gw n Mandimba Memba a io u Vila úr L L Mecubúri Nacala Kabwe Gamito Cuamba Vila Ribáué MecontaMonapo Mossuril Fingoè FurancungoCoutinho ^! Nampula 15°S Vila ^! 15°S Lago de NAMPULA TETE Junqueiro ^! Lusaka ZumboCahora Bassa Murrupula Mogincual K Nametil o afu ezi Namarrói Erego e b Mágoè Tete GiléL am i Z Moatize Milange g Angoche Lugela o Z n l a h m a bez e i ZAMBEZIA Vila n azoe Changara da Moma n M a Lake Chemba Morrumbala Maganja Bindura Guro h Kariba Pebane C Namacurra e Chinhoyi Harare Vila Quelimane u ^! Fontes iq Marondera Mopeia Marromeu b am Inhaminga Velha oz P M úngu Chinde Be ni n è SOFALA t of ManicaChimoio o o o o o o o o o o o o o o o gh ZIMBABWE o Bi Mutare Sussundenga Dondo Gweru Masvingo Beira I NDI A N Bulawayo Chibabava 20°S 20°S Espungabera Nova OCE A N Mambone Gwanda MANICA e Sav Inhassôro Vilanculos Chicualacuala Mabote Mapai INHAMBANE Lim Massinga p o p GAZA o Morrumbene Homoíne Massingir Panda ^! National capital SOUTH Inhambane Administrative capital Polokwane Guijá Inharrime Town, village o Chibuto Major airport Magude MaciaManjacazeQuissico International boundary AFRICA Administrative boundary MAPUTO Xai-Xai 25°S Nelspruit Main road 25°S Moamba Manhiça Railway Pretoria MatolaMaputo ^! ^! 0 100 200km Mbabane^!Namaacha Boane 0 50 100mi !\ Bela Johannesburg Lobamba Vista ESWATINI Map No. -

Zambia USADF Country Portfolio

Zambia USADF Country Portfolio Overview: Country program established in 1984 and reopened in U.S. African Development Foundation Partner Organization: Keepers Zambia 2004. USADF currently manages a portfolio of 23 projects and one Country Program Coordinator: Guy Kahokola Foundation (KZF) Cooperative Agreement. Total active commitment is $2.9 million. Suite 103 Foxdale Court Office Park Program Manager: Victor Makasa Agricultural investments total $2.6 million. Youth-led enterprise 609 Zambezi Road, Roma Tel: +260 211 293333 investments total $20,000. Lusaka, Zambia Email: [email protected] Email: [email protected] Country Strategy: The program focuses on support to agricultural enterprises, including organic farming as Zambia has been identified as a Feed the Future country. In addition, there are investments in off-grid energy and youth led-enterprises. Enterprise Duration Grant Size Description Mongu Dairy Cooperative Society 2012-2017 $152,381 Sector: Agriculture (Dairy) Limited Town/City: Mongu District in the Western Province 2705-ZMB Summary: The project funds will be used to increase the production and sales of milk through the purchase of improved breed cows, transportation, and storage equipment. Chibusa Home Based Care 2013-2018 $187,789 Sector: Agriculture (Food Processing) Association Town/City: Mungwi District in the Northern Province of Zambia 2925-ZMB Summary: The project funds will be used to provide working capital for purchasing grains, increase milling capacity, build a storage warehouse, and provide funds to improve marketing. Ushaa Area Farmers Association 2013-2018 $94,960 Sector: Agriculture (Rice) Limited Town/City: Mongu District in the Western Province of Zambia 2937-ZMB Summary: The project funds will be used to provide working capital for purchasing rice, build a storage warehouse, and provide funds to improve marketing. -

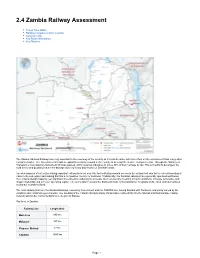

2.4 Zambia Railway Assessment

2.4 Zambia Railway Assessment Travel Time Matrix Railway Companies and Consortia Capacity Table Key Route Information Key Stations The Zambia National Railways are very important to the economy of the country as it is a bulk carrier with less effect on the environment than many other transport modes. The Government intends to expand its railway network in the country to develop the surface transport sector. Through the Ministry of Transport, a new statutory instrument (SI) was passed, which requires industries to move 30% of their carriage by rail. This is in a bid to decongest the road sector and possibly reduce the damage done by heavy duty trucks on Zambian roads. The development of rail routes linking important exit points is not only vital for facilitating smooth access to the outside but also for the overall boosting of trade in the sub-region and making Zambia a competitive country for business. Traditionally, the Zambian railways have generally operated well below their original design capacity, yet significant investment is underway to increase their volumes by investing in track conditions, increase locomotive and wagon availability and increase operating capital. The rail network remains the dominant mode of transportation for goods on the local and international routes but is under-utilized. The main railway lines are the Zambia Railways, owned by Government and the TAZARA line, linking Zambia with Tanzania, and jointly owned by the Zambian and Tanzanian governments. The opening of the Chipata-Mchinji railway link provides connectivity into the Malawi and Mozambique railway network and further connects Zambia to the port of Nacala. -

National Investment Plan to Reduce Deforestation and Forest Degradation (2018-2022)

Republic of Zambia Ministry of Lands and Natural Resources National Investment Plan to Reduce Deforestation and Forest Degradation (2018-2022) November 2017 -i- Executive Summary Zambia has approximately 49.9 million hectares of forest, representing approximately 66 percent of its total land mass and is subsequently one of the most forested countries in southern Africa. However, deforestation is a major problem, with annual rates estimated at around 250,000 to 300,000 hectares. Such numbers amount to the potential loss of 10 million hectares of forest in the next 30 years (IDLO, 2014). The key drivers of deforestation and forest degradation in Zambia are agricultural expansion (commercial and subsistence), heavy reliance on wood fuel – energy demand (charcoal and firewood), unsustainable timber extraction (both legal and illegal) and infrastructure development (e.g., mining and other large infrastructural developments). A study by UN-REDD, (2015) on the economic value of Zambia’s forest ecosystems showed that the direct and indirect values of forests are estimated to make a direct contribution equivalent to about 4.7% of gross domestic product (GDP) or US$957.5 million (using 2010 figures). However, when the multiplier effects of forestry and tourism-related activities on other sectors are considered, the overall or economy-wide contribution of forests to GDP is estimated to be at least 6.3% or US$1,277 million (Table 1). Forests are estimated to provide at least 1.4 million jobs, supporting 60% of rural Zambian households, heavily dependent upon the use of natural resources to supplement or sustain their livelihoods (UN-REDD., 2015). -

Mwami Adventist Hospital, Zambia Photo Courtesy of Moses M

Mwami Adventist Hospital, Zambia Photo courtesy of Moses M. Banda. Mwami Adventist Hospital MOSES M. BANDA Moses M. Banda , M.A. (Zambia Open University, Lusaka, Zambia), B.A. in theology (Rusangu University), serves as president of East Zambia Field of Seventh-day Adventists. He is an ordained minister and has served in various positions for 20 years. He is married to Eness with whom he has two children. Mwami Adventist Hospital is a medical institution of the Southern Zambia Union Conference of Seventh-day Adventists. Developments that Led to the Establishment of the Institution As early as 1913, C. Robinson yearned to secure a foothold in north-east Rhodesia; somewhere near Fort Jameson (now Chipata).1 On October 2, 1925, G. A. Ellingworth of Malamulo Mission acquired a farm of 3,035 acres, on which Mwami Mission station was established.2 Between 1925 and 1927, Samuel Moyo served as the mission station director. He was respected and regarded as one of God’s gentlemen. In 1927, the final transaction for the tract of the farmland situated between Fort Manning and Fort Jameson was concluded. The farm had three streams, good soil, and pastureland that could support a small herd. It had previously been a tobacco farm, with many old brick buildings. The unusable buildings were still valuable in that they contained 200,000 good bricks, needed for mission buildings.3 Mwami Adventist Hospital was established as an extension of medical missionary work conducted at Malamulo Mission in Malawi.4 Mwami is 480 kilometers from Malamulo, and 30 kilometers southeast of Chipata, the provincial capital city of the Eastern Province of Zambia, in the Luangeni constituency along Vubwi Road.5 The mission was named after the Mwami stream, which flows through the mission farm.6 The Mwami stream originates from the eastern side of Mkwabe mountain, then deviates northwards through the Mwami Dam until it crosses Vubwi Road near Lufazi Village. -

Food Security Research Project

FOOD SECURITY RESEARCH PROJECT LEVIES ON AGRICULTURAL COMMODITIES: WHO BENEFITS? A RAPID ASSESSMENT By Billy Mwiinga Julius Shawa T.S. Jayne James Shaffer WORKING PAPER No. 12 FOOD SECURITY RESEARCH PROJECT LUSAKA, ZAMBIA APRIL 2005 (Downloadable at: http://www.aec.msu.edu/agecon/fs2/zambia/index.htm ) ACKNOWLEDGMENTS The Food Security Research Project is a collaboration between the Agricultural Consultative Forum (ACF), the Ministry of Agriculture, Food and Fisheries (MAFF), and Michigan State University's Department of Agricultural Economics (MSU). We wish to acknowledge the financial and substantive support of the United States Agency for International Development (USAID) in Lusaka. Research support from the Global Bureau, Office Agriculture and Food Security, and the Africa Bureau, Office of Sustainable Development at USAID/Washington also made it possible for MSU researchers to contribute to this work. This study was conceived and carried out under the auspices of the Ministry of Agriculture and Cooperatives (MACO). Comments and questions should be directed to the In-Country Coordinator, Food Security Research Project, 86 Provident Street, Fairview, Lusaka; tel: 234539; fax: 234559; email: [email protected]. ii FOOD SECURITY RESEARCH PROJECT TEAM MEMBERS The Zambia FSRP field research team is comprised of Jones Govereh, Stephen Kabwe, Billy Mwiinga, Jan Nijhoff, Misheck Nyembe and Ballard Zulu. MSU-based researchers in the Food Security Research Project are Antony Chapoto, Cynthia Donovan, Thomas Jayne, David Tschirley, and Michael -

Republic of Malawi Diagnostic Trade Integration Study (DTIS) Update

Report No: ACS7534 Public Disclosure Authorized Republic of Malawi Diagnostic Trade Integration Study (DTIS) Update Public Disclosure Authorized Reducing trade costs to promote competitiveness and inclusive growth March 25, 2014 Public Disclosure Authorized AFTP1 AFRICA Public Disclosure Authorized Standard Disclaimer: This volume is a product of the staff of the International Bank for Reconstruction and Development/ The World Bank. The findings, interpretations, and conclusions expressed in this paper do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Copyright Statement: The material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. The International Bank for Reconstruction and Development/ The World Bank encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly. For permission to photocopy or reprint any part of this work, please send a request with complete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, http://www.copyright.com/. All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Publisher, The World Bank, 1818 H Street NW, Washington, DC 20433, USA, fax 202-522-2422, e-mail [email protected]. -

Terms of Reference for Chipata/Mchinji Dry and Liquid Port

LOT N° 2: REQUEST N° SPECIFIC TERMS OF REFERENCE FEASIBILITY FOR THE DEVELOPMENT OF AN INTERMODAL DRY PORT IN CHIPATA, ZAMBIA 1. BACKGROUND 1.1 Sugar Reform The sugar industry plays a crucial role in the Zambian economy. The industry provides an important source of income ands employment in rural areas, as well as foreign exchange, thanks to the sale of large proportion of the industry's output to export destinations, including the EU. In Zambia, the sugar sector contributes to 3-4% of the GDP and 6% of the National Export Earnings1. As a low cost producer, the sugar industry has the potential to increase its contribution to Zambia's socio- economic development. The 2006 EU sugar sector reform has involved a reduction of EU sugar prices and has required significant adjustment in ACP countries signatories to the Sugar Protocol, which was providing duty free access for sugar, at a guaranteed price. In the light of the reform, Zambia has initiated a reorientation and restructuring of its sugar industry. An adaptation strategy for the Sugar Industry in Zambia has been developed in 2006. It sets out relevant projects that will consolidate and improve the future competitiveness of the Sugar Industry in Zambia. The main areas of intervention include: • The expansion of sugar production through Outgrower Schemes; • A diversification strategy: particularly based on ethanol production for fuel blending and gel fuel, and encouragement of the co-generation of electricity; • The facilitation of improvements to and cost reductions on sugar trade routes; • The development of a sugar trade policy. On this basis, the European Commission has allocated €562,000 to Zambia as "Accompanying measures 2006 for Sugar Protocol Countries". -

Works Contract for the Construction of the Mwami/Mchinji One Stop Border Post (Osbp): Works Package 2: Zambia Osbp Facilities - Rda/Icb/Ce/004/18

REPUBLIC OF ZAMBIA ROAD DEVELOPMENT AGENCY (RDA) WORKS CONTRACT FOR THE CONSTRUCTION OF THE MWAMI/MCHINJI ONE STOP BORDER POST (OSBP): WORKS PACKAGE 2: ZAMBIA OSBP FACILITIES - RDA/ICB/CE/004/18 SPECIFIC PROCUREMENT NOTICE INVITATION FOR BIDS Date: 18th May, 2018 Loan No: 2100150030793 IFB No: RDA/ICB/CE/004/18 1. This Invitation for Bids follows the General Procurement Notice (GPN) for this project that appeared on UNDB online of 15th March, 2012 and on the African Development Bank Group’s Internet Website. 2. The Government of the Republic of Zambia has received Financing from the African Development Bank in various currencies towards the cost of Nacala Road Development Project Phase IV. It is intended that part of the proceeds of this loan will be applied to eligible payments under the Works Contract for the Construction of the Mwami/Mchinji One Stop Border Post (OSBP): Works Package 2: Zambia OSBP Facilities. 3. The Road Development Agency (RDA) now invites sealed bids from eligible bidders for the execution of the works: The scope of works consists of both building and civil works that include but will not be limited to: ▪ Construction of 3 x 2 storey blocks (combined floor area of approximately 6,000m2), ▪ Construction of 5 single storey blocks ▪ Construction of roads linking the Mwami and Mchinji one stop border facilities between Zambia and Malawi. This shall also include related access roads, parking areas for up to 70 trucks as well as staff car parking with circulating roads. The Project shall be executed in Chipata District, Eastern Province. -

Vulnerability and Resilience of Social-Ecological Systems Research Institute for Humanity and Nature

Working Paper on Social-Ecological Resilience Series No. 2009-010 Resilience of Rural Households and Communities to Economic Shocks, HIV/AIDS and Recurrent Droughts: The Case of Households and Communities in the Mwami Area, Chipata, Zambia By Chileshe L. Mulenga Visiting Fellow, Research Institute for Humanity and Nature December 2009 Vulnerability and Resilience of Social-Ecological Systems RIHN Research Project E-04 Research Institute for Humanity and Nature (RIHN) Inter-University Research Institute Corporation, National Institutes for the Humanities 大学共同利用機関法人 人間文化研究機構 総合地球環境学研究所 Working Paper on Social-Ecological Resilience Series No. 2009-010 Resilience of Rural Households and Communities to Economic Shocks, HIV/AIDS and Recurrent Droughts: The Case of Households and Communities in the Mwami Area, Chipata, Zambia By Chileshe L. Mulenga Visiting Fellow, Research Institute for Humanity and Nature E-mail: [email protected] December 2009 Vulnerability and Resilience of Social-Ecological Systems RIHN Research Project E-04 Research Institute for Humanity and Nature (RIHN) Inter-University Research Institute Corporation, National Institutes for the Humanities 大学共同利用機関法人 人間文化研究機構 総合地球環境学研究所 Table of Contents Acknowledgements Abstract 1.0 Introduction ...………………………………………………………………………….. 1 1.1 Approaches to the Study ……………………………………………………………... 3 1.2 Organization of the Paper ……………………………………………………………. 3 2.0 Conceptual Framework ……………………………………………………………….. 5 3.0 Political Economy of Agriculture and Rural Development in Zambia …………….. 7 3.1 Responses to the New Political Economy of Agriculture and Rural Development ….. 14 4.0 HIV/AIDS and Responses of Households and Communities in the Mwami Area … 19 4.1 HIV/AIDS Prevalence and Policy Responses in Zambia ……………………………. 19 4.2 Knowledge and Attitudes to HIV/AIDS among Young People …………………….. -

Republic of Zambia Report of the Committee on Parastatal Bodies on the Examination of the Annual Reports for the Tanzania Zambia

REPUBLIC OF ZAMBIA REPORT OF THE COMMITTEE ON PARASTATAL BODIES ON THE EXAMINATION OF THE ANNUAL REPORTS FOR THE TANZANIA ZAMBIA RAILWAY AUTHORITY FOR THE YEARS ENDED 2017 AND 2018 FOR THE FOURTH SESSION OF THE TWELFTH NATIONAL ASSEMBLY APPOINTED ON 21ST SEPTEMBER, 2017 Printed by the National Assembly of Zambia REPORT OF THE COMMITTEE ON PARASTATAL BODIES ON THE EXAMINATION OF THE ANNUAL REPORTS FOR THE TANZANIA ZAMBIA RAILWAY AUTHORITY FOR THE YEARS ENDED 2017 AND 2018 FOR THE FOURTH SESSION OF THE TWELFTH NATIONAL ASSEMBLY APPOINTED ON 21ST SEPTEMBER, 2017 Table of Contents 1.0 Composition of the Committee ...................................................................................................... 1 2.0 Functions of the Committee ........................................................................................................... 1 3.0 Meetings of the Committee ............................................................................................................ 2 4.0 Procedure Adopted by the Committee ........................................................................................... 2 5.0 Arrangement of the Report ............................................................................................................ 2 PART I .......................................................................................................................................................... 2 Consideration of the Topical Issue: Examination of the Annual Reports of the Tanzania-Zambia Railway Authority, for the -

Zambia Non-Motorised Transport Strategy

Zambia Non-Motorised Transport Strategy Ministry of Transport and Communications United Nations Environment Programme Institute for Transportation and Development Policy July 2019 Contents 1. Introduction ...................................................................................................................................... 3 2. Emerging urban mobility challenges ................................................................................................ 3 3. Assessment of walking & cycling environment ............................................................................... 5 3.1 Footpaths ............................................................................................................................... 5 3.2 Cycle facilities ....................................................................................................................... 7 3.3 Pedestrian crossings ............................................................................................................... 7 3.4 Parking management ............................................................................................................. 8 3.5 Street lighting ........................................................................................................................ 9 3.6 Storm water management .................................................................................................... 10 3.7 Building design ...................................................................................................................