Outoftheblue

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Leinster GAA Convention Report 2013-2014 1

Leinster GAA Convention Report 2013-2014 1 The proudest man in Croke Park last Summer was Na Fianna’s Jimmy Gray when he was called on to present the Bob O’Keeffe Cup to Dublin Hurling Captain, Johnny McCaffrey, after their victory over Galway. In 1961 Jimmy played in goal for Dublin when they defeated Wexford in their last Dublin Captain Stephen Cluxton, raises the Leinster Senior Hurling Championship Final win. Little did anyone know then that it Delaney Cup in triumph at Croke Park in July 2013 would be a long 52 years before the Dubs would repeat that victory. Well worth waiting for, Jimmy! Dublin Leinster Senior Hurling Champions 2013 Dublin Leinster Senior Football Champions 2013 Back L-R: Conor McCormack, Liam Rushe, Conal Keaney, Eamon Dillon, Mark Schutte, Martin Quilty, Joseph Boland, Niall Corcoran, Back L-R: Kevin Nolan, Shane Supple, Nicky Devereaux, James McCarthy, Ciaran Kilkenny, Paul Mannion, Darren Daly, Michael Ryan O’Dwyer, Peter Kelly, Michael Carton, Stephen Hiney, Simon Lambert, Niall McMorrow, Paul Ryan, Shane Durkin. Darragh Macauley, Cian O’Sullivan, Bernard Brogan, Kevin O’Brien, Michael Fitzsimons, Shane Carthy, Denis Bastick, Philly McMahon, Kevin McManamon. Front L-R:2 DavidLeinster Treacy, GAA Ruairi Convention Trainor, JohnnyReport McCaffrey2013-2014 (C), Paul Schutte, Gary Maguire, Danny Sutcliffe, David O’Callaghan, Alan Nolan, Oisin Gough, Maurice O’Brien. Front L-R: Dean Rock, Johnny Cooper, Ger Brennan, Cormac Costello, Stephen Cluxton (C), Diarmuid Connolly, Paul Flynn, Rory O’Carroll, Jack McCaffrey, Bryan Cullen. The proudest man in Croke Park last Summer was Na Fianna’s Jimmy Gray when he was called on to present the Bob O’Keeffe Cup to Dublin Hurling Captain, Johnny McCaffrey, after their victory over Galway. -

LGAA Conv Book 04

Comhairle Laighean C.L.G. Tionolfar Comhdháil Cinn Bliana 2003 - 2004 In Jury’s Hotel, Ballsbridge Ar an hAoine, 27ú Feabhra 2004 6.15 pm 2 Kilkenny - Leinster Minor Hurling Champions 2003 Back L-R: S.Prendergast, N Delahunty, R Maher, P Doheny, D Prendergast, P Hartley, D Cody, J Tennyson, M Fennelly, J Dalton, R Wall, B Beckett, D McCormack. Front L-R: D Fogarty, A Murphy, P O'Donovan, M Nolan, E Guinan, R Power, S Cadogan, C Grant, E McGrath, A Healy, J Fitzpatrick, E O'Donoghue. Clár 6.15pm Registration 6.30pm High Tea 7.30pm (1) Convention Opens (2) Address by Cathaoirleach Coisde Co. Áth Cliath C.L.G. 7.45pm (1) Minutes of 2003 Convention (2) Discussion of Report of Chief Executive (3) Discussion of Sub-Committee Reports 8.10pm Ballot (Cisteoir) 8.15pm Review of Accounts of Comhairle Laighean C.L.G. 8.30pm Ballot (P.R.O.) 8.40pm Address by An Cathaoirleach 9.00pm Election of Officers 9.15pm Guest Speakers 9.30pm Na Rúin 9.40pm Tea/Coffee – Convention Closes Each county is entitled to the following Delegate representation at Convention, in addition to its two representatives on the Provincial Council: Ceatharloch 5 Cill Mhantain 6 Iarmhi 5 An Mhí 6 An Lú 5 Longphort 5 Cill Dara 6 Uibh Fháilí 6 Cill Chainnigh 5 Laois 6 Áth Cliath 6 Loch Garman 6 A brief meeting of the incoming Leinster Council will be held immediately after Convention, at which only urgent business to hand will be considered. NOTE 1. Slip on Admission Card to be handed to Hotel Management for High Tea (6.30pm) 2. -

Na Fianna Nuacht

Na Fianna Nuacht Club and Individual Team Fundraiser 2019 Next Leaders Unveiled This week saw the unveiling of the next group of Leaders of Na Fianna’s Operation Transformation. Congratulations to Colm O’Driscoll representing the Junior 8 Footballers, Dermot Moran representing Senior Hurlers, Ciara Purdy from Senior Ladies Footballers, Ryan O’Flaherty Senior Footballers and Mary O’Connell representing the Minor and U-16 Hurlers. Well done all for stepping up. But we need more leaders…..read on. Na Fianna Nuacht 24ú Nollaig 2018 1 Na Fianna Nuacht Leaders Required – No Experience Necessary Fundraising opportunity for your Team and Club Entries by 18th Jan 2019 First Weigh in starts 19th Jan Start Date: 8th Feb 2019 End Date: 19th April 2019 – Finale Night with Special Guests Contact: email [email protected] Paul McCarville 0872835005 Gerard Keane 0862548027 Philip O Brien 0868259287 Anne Barrett 0863168230 Art Fitzpatrick 0868118395 Raise much needed funds for Na Fianna and your Individual Teams Leaders can be mentors, parents, aunt, uncle or grandparents basically anyone the Team want to nominate and get behind in a fundraising drive. This is about the promotion of Club, Community, Health and Wellbeing for 2019. It is for all members of the Club from Senior Teams down to the Nursery and is a great opportunity to get involved in a very positive fundraiser for your Club and your individual Teams. Initially we need 20 Leaders up for the challenge. This week’s new five leaders now join our first three announced last week – Roisin O’Donoghue Senior Camogie, Maurice Grehan & Philip O’Brien under 13 Boys More Leaders to be announced straight after Christmas – keep an eye out to see who else will be joining our leaders – limited spaces available so get in quick and join us on this journey. -

Grid Export Data

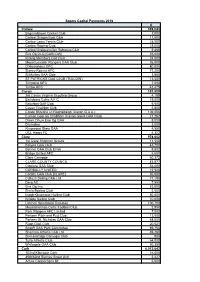

Sports Capital Payments 2018 € Carlow 389,043 Bagenalstown Cricket Club 7,000 Carlow Dragon Boat Club 11,500 Carlow Lawn Tennis Club 28,500 Carlow Rowing Club 18,000 Carlow/Graiguecullen Subaqua Club 9,468 Éire Óg CLG [CARLOW] 35,000 Killerig Members Golf Club 24,500 Mount Leinster Rangers GAA Club 36,000 O'Hanrahans GFC 80,000 Slaney Rovers AFC 71,250 St Mullins GAA Club 3,850 ST PATRICKS GAA CLUB (TULLOW) 13,500 Tinryland GFC 7,000 Tullow RFC 43,475 Cavan 183,809 3rd Cavan Virginia Scouting Group 4,189 Bailieboro Celtic A.F.C 19,000 Belturbet Golf Club 5,500 Cavan Triathlon Club 2,800 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) 109,686 Cuman Gael an Chabhain (Cavan Gaels GAA Club) 21,262 Droim Dhuin Eire Og GAA 9,000 Drumalee 3,500 Kingscourt Stars GAA 4,550 UCL Harps FC 4,322 Clare 978,602 1st Clare Shannon Scouts 11,500 Ballyea GAA Club 43,700 Banner GAA Club Ennis 9,602 Bridge United AFC 5,500 Clare Camogie 60,372 CLARE COUNTY COUNCIL 83,877 Clonlara GAA Club 54,000 CORBALLY UNITED 12,500 Corofin GAA Club [CLARE] 50,000 Cullaun Sailing Club Ltd 77,180 Derg AC 7,990 Eire Og Inis 53,000 Ennis Boxing Club 2,500 Inagh Kilnamona Hurling Club 50,000 Killaloe Sailing Club 10,000 Lahinch Sportsfield Comittee 100,700 Mountshannon Celtic Football Club 2,850 Park Rangers AFC Limited 7,000 Parteen Pitch and Putt Club 13,500 Parteen St. Nicholas GAA Club 68,000 Ruan GAA Club 20,621 Scariff GAA Park Committee 99,750 Shannon Athletic Club Ltd 39,260 Sixmilebridge Camogie Club 850 Tulla Athletic Club 64,000 Whitegate GAA Club 30,350 Cork 6,013,642 -

Na Fianna Nuacht

Na Fianna Nuacht Chairman’s New Year’s Greetings It's that time of year again when hopefully we are all well rested after a peaceful Christmas and New Year. The batteries have been re-charged and thoughts inevitably drift forward. Several teams have already come out of hibernation and are making plans for the playing season ahead. A lot of work has gone into next weekend's Coaching Forum which will take place on Saturday afternoon January 17th at 1pm in the Mobhi Suite. Please ensure that you can attend as it is the perfect way to throw in the ball for the new season. 2015 promises to be an eventful year in the life of our club. It marks the 60th anniversary of the club's foundation so we will be celebrating a diamond anniversary. Plans are afoot to celebrate this landmark date appropriately. On the pitch the club will be fielding a record number of teams across our four unrivalled sports of hurling, football, camogie and ladies' football. Our handballers will continue to hold court and are growing in numbers. Our musicians, dancers and players are making their presence felt in Scór at county, provincial and national level. The club's Nursery continues to be the 'jewel in the crown' and is a wonderful testament to the commitment and dedication of our club volunteers. Recent club success at senior, minor and Under 21 level can be traced back directly to the wonderful work done in the club Nursery by so many around the turn of the century. -

2007 Sports Capital Programme Allocations

2007 Sports Capital Programme Allocations County Organisation Amount Allocated Carlow Askea Karate CLub €3,000 Carlow Ballinkillen Hurling Club €80,000 Carlow Carlow Gymnastics Club €10,750 Carlow Carlow Martial Arts Sanctuary €10,000 Carlow Carlow Town Hurling Club €50,000 Carlow County Carlow Football Club €70,000 Carlow Éire Óg CLG [CARLOW] €90,000 Carlow Myshall GAA Club €100,000 Carlow New Oak Boys Football Club €40,000 Carlow OLD LEIGHLIN GFC €100,000 Carlow Palatine GAA Club €80,000 Carlow ST PATRICKS GAA CLUB (TULLOW) €70,000 Cavan Active Virginians €3,500 Cavan Bailieborough Shamrocks GAA €100,000 Cavan Ballyjamesduff Soccer Club €60,000 Cavan Ballymachugh G.F.C. €140,000 Cavan Belturbet Row Boat Club €6,000 Cavan Butlersbridge Gaelic Football Club €100,000 Cavan Castlerahan Community Development Ltd €60,000 Cavan Cootehill Celtic GAA €90,000 Cavan Cootehill Harps AFC €90,000 Cavan Cornafean GFC €50,000 Cavan County Cavan Rugby Football Club €150,000 Cavan Drumalee €18,000 Cavan Drumlane Community Partnership Ltd €9,000 Cavan Drumlane GAA Club €12,000 Cavan Drumlin Equestrian €65,000 Cavan kill community development €40,000 Cavan Killeshandra Leaguers GFC €75,000 Cavan Kingscourt Harps AFC €50,000 Cavan Knockbride G F C €100,000 Cavan Lavey GAA Club €70,000 Cavan Loch Gowna G.A.A. Club €100,000 Cavan Mullahoran GFC €60,000 Cavan Ramor United GFc & Ramor Community Sports Park €130,000 Cavan Templeport Saint Aidans GAA Club €50,000 Clare Aughinish Diving Club €20,000 Clare Bodyke GAA Club €35,000 Clare CLARE COUNTY COUNCIL €130,000 Clare Clarecastle GAA Club €30,000 Clare Clonlara Leisure Athletic and Sports Centre €100,000 Clare Clooney Quin GAA Club €60,000 Clare Cooraclare GAA Club €90,000 Clare CORBALLY UNITED €10,000 Clare Corofin GAA Club [CLARE] €35,000 Clare County Clare Agricultural Show Society Limited €90,000 Clare Cratloe Tennis Club €20,000 Clare Crusheen G.A.A. -

The Edition, 25Th October, 2017

Technological University Dublin ARROW@TU Dublin Student Publications Dublin Institute of Technology 2017-10-25 The Edition, 25th October, 2017 DIT News Society Follow this and additional works at: https://arrow.tudublin.ie/ditoth Recommended Citation Dublin Institute of Technology News Society; The Edition, 25 October 2017. Dublin, DIT, 2017 This Article is brought to you for free and open access by the Dublin Institute of Technology at ARROW@TU Dublin. It has been accepted for inclusion in Student Publications by an authorized administrator of ARROW@TU Dublin. For more information, please contact [email protected], [email protected]. This work is licensed under a Creative Commons Attribution-Noncommercial-Share Alike 4.0 License Wednesday 25 October 2017 THE EDITION@edition_ie edition.ie www.edition.ie Supported by DIT News Society DIT counsellingHumans Of waiting DIT - Pg list 8 - Pg 3 VolleyballBack to facilitiesStars Hollow a must- - Pg Pg 9 24 GetDoctor to know Strange your Review Socities - -Pg Pg 15 15 Grangegorman Canteen’s - Page prices 4 under scrutiny - Page 5 DIT to introduce Student Levy By John Patrick Kierans DIT are planning to introduce a to get to that point,” he added. student levy of up to €150 to pay “We hope the levy will include so- for a number of student services in cial and recreational space, which Grangegorman. would be on the ground floor of The long awaited campus, which the student accommodation and is not expected to be fully com- a new build in the first phase of a plete until 2022, will see students new sports hall. -

Grid Export Data

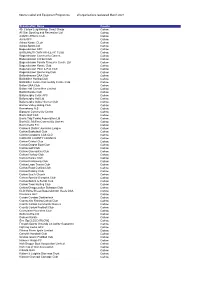

Sports Capital and Equipment Programme all organisations registered March 2021 Organisation Name County 4th Carlow Leighlinbrige Scout Group Carlow All Star Sporting and Recreation Ltd Carlow Ardattin Athletic Club Carlow Asca GFC Carlow Askea Karate CLub Carlow Askea Sports Ltd Carlow Bagenalstown AFC Carlow BAGENALSTOWN ATHLETIC CLUB Carlow Bagenalstown Community Games Carlow Bagenalstown Cricket Club Carlow Bagenalstown Family Resource Centre Ltd Carlow Bagenalstown Karate Club Carlow Bagenalstown Pitch & Putt Club Carlow Bagenalstown Swimming Club Carlow Ballinabranna GAA Club Carlow Ballinkillen Hurling Club Carlow Ballinkillen Lorum Community Centre Club Carlow Ballon GAA Club Carlow Ballon Hall Committee Limited Carlow Ballon Karate Club Carlow Ballymurphy Celtic AFC Carlow Ballymurphy Hall Ltd Carlow Ballymurphy Indoor Soccer Club Carlow Barrow Valley Riding Club Carlow Bennekerry N.S Carlow Bigstone Community Centre Carlow Borris Golf Club Carlow Borris Tidy Towns Association Ltd Carlow Borris/St. Mullins Community Games Carlow Burrin Celtic F.C. Carlow Carlow & District Juveniles League Carlow Carlow Basketball Club Carlow Carlow Carsports Club CLG Carlow CARLOW COUNTY COUNCIL Carlow Carlow Cricket Club Carlow Carlow Dragon Boat Club Carlow Carlow Golf Club Carlow Carlow Gymnastics Club Carlow Carlow Hockey Club Carlow Carlow Karate Club Carlow Carlow Kickboxing Club Carlow Carlow Lawn Tennis Club Carlow Carlow Road Cycling Club Carlow Carlow Rowing Club Carlow Carlow Scot's Church Carlow Carlow Special Olympics Club Carlow Carlow -

Cuntais Leithreasa Iniúchta 2005

Cuntais Leithreasa Iniúchta 2005 Cuntais Leithreasa de na Suimeanna arna ndeonú ag an Oireachtas le haghaidh Seirbhísí Poiblí don bhliain dar chríoch 31 Nollaig 2005 Arna dtíolacadh faoi réir Alt 3(10) den Acht Ard-Reachtaire Cuntas agus Ciste (Leasú), 1993 Baile Átha Cliath Arna fhoilsiú ag Oifig an tSoláthair Le ceannach díreach ón Oifig Dhíolta Foilseachán Rialtais, Teach Sun Alliance, Sráid Theach Laighean, Baile Átha Cliath 2 nó tríd an bpost ó Foilseacháin Rialtais, An Rannóg Post-Tráchta, 51 Faiche Stiabhna, Baile Átha Cliath 2 (Teil: 01-6476000, Fax: 01-4752760) nó trí aon díoltóir leabhar. (Prn. A6/0431) Praghas €13.00 © Rialtas na hÉireann 2006 Clár Ábhair Leathanach Na Cuntais Oiriúnacha – Tabhairt Isteach iii Dualgais an Ard-Reachtaire Cuntas agus Ciste agus na n-Oifigeach Cuntasóireachta i leith na gCuntas Oiriúnaigh. iii Ráiteas Polasaithe agus Prionsabal Cuntasóireachta v Ráiteas ag Oifigigh Cuntasóireachta ar Smacht Airgeadúil Inmheánach ix Achomair de Chuntais Oiriúnacha xi Cuntais Teaghlachas an Uachtaráin 1 Roinn an Taoisigh 6 Oifig an Ard-Aighne 14 An Phríomh-Oifig Staidrimh 21 Oifig an Ard-Reachtaire Cuntas agus Ciste 28 Oifig an Aire Airgeadais 35 Aoisliúntas agus Liúntais Scoir 44 Oifig na gCoimisinéirí Achomhairc 48 Oifig na gCoimisinéirí Ioncaim 52 Oifig na nOibreacha Poiblí 58 An tSaotharlann Stáit 70 Rúnseirbhís 77 Oifig an Phríomh-Aturnae Stáit 80 Oifig an Stiúrthóra Ionchúiseamh Poiblí 87 An Oifig Luachála 92 i An tSeirbhís um Cheapachain Phoiblí 98 Oifig an Choimisiúin um Cheapacháin Serbhíse Poiblí 105 Oifig -

Na Fianna Nuacht 070619

Na Fianna Nuacht Fancy Winning €19,000! Club lotto jackpot still hasn’t been won which means that next Monday night’s jackpot will be a cool €19,000. Be sure to get your ticket in the Club this weekend, tickets on sale in members bar. Alternatively, by signing up for the direct debit option, you could win the jackpot every week! See details here Mobhi Road Parking Please note that due to the presence of a film crew in the club car park Mobhi Road, parking in Mobhi Road will be tight until Monday. Members attending games over the weekend are asked, where possible, to consider leaving cars at home. Thanks to all for your cooperation. Na Fianna Nuacht 7ú Meitheamh 2019 1 Na Fianna Nuacht New Sponsors For Our Senior Ladies Ballygall Credit Union recently announced a sponsorship arrangement with Na Fianna’s Senior Ladies Football team. Pictured above is Aislinn Daly of Ballygall Credit Union with team captain Aoife Caffrey. Pictured below at the recent sponsorship presentation are members of the Senior Ladies with Aislinn Daly of Ballygall Credit Union. Sincere thanks to all at Ballygall Credit Union for their generous support. Na Fianna Nuacht 7ú Meitheamh 2019 2 Na Fianna Nuacht This year the annual Dermot McNulty Memorial Tournament was held on the June Bank Holiday Sunday and moved up from u11 to u12 age group. Now in its thirteenth year, this hurling blitz, held in memory of founding member Dermot McNulty, showcases the juvenile set up of CLG Na Fianna, our wonderful facilities and the importance that events like this have for the club, community and hurling. -

Property Development Department, Civic Offices. the Chairman And

Property Development Department, Civic Offices. The Chairman and Members of North West Area Committee Meeting: 17th October 2017 Item No: 12 With reference to the Development Department Property Section Community Group Lettings/Licences Historical Background One of the functions of the City Council is to provide community facilities to the various community organisations such as Sports Clubs, Residents Associations, Youth Clubs etc. within its functional area so that they can carry out their various activities. In the late 1960s and early 70s in particular and possibly as a result of the expansion of the suburbs the City Council began disposing of sites to community organisations on long term leases. In general the disposals were made by way of a Building Agreement and subsequent lease i.e. the Council provided the land and the community organisations through fundraising and in some cases grant aid from Dublin City Council and others built the premises. In return for this the Council gave the groups in question a long term lease (usually 99 years) subject to an open market rent but abated to a nominal rent so long as the premises was used for a specific community purpose. Usually there were two bands of abatement. If there was a covenant in the lease prohibiting the organisation from selling alcohol on the premises then they were charged either €33.00 (£25.00) or €127 (£100). However if there was no such prohibition in the lease then that group were charged an abated rent of €1,270 (£1,000). As these are leases and so long as the groups abide by the covenants therein there is no scope to increase rent on these properties. -

List of Sporting Bodies Who Have Been Granted Tax Exemption @2Nd

List of sporting bodies who have been granted tax exemption @ 30th November 2015 under Section 235 Taxes Consolidation Act, 1997 and their county. Queries to: Games & Sports Exemption Section, Revenue Commissioners, Government Offices, Nenagh,Co. Tipperary LoCall: 1890 666 333 Phone: 067 63377 GS Number Name County 646 Abbey Boxing Club Limerick 2220 Abbeydorney GAA Club Kerry 384 Abbeyfeale Community Leisure Ltd. Limerick 1071 Abbeyknockmoy Hurling Club Galway 2420 Abbeylara GAA Club Longford 2353 Abbeyleix Park Development Laois 2797 Abbeyleix Tennis Club Laois 2775 Abbeyside / Ballinacourty GAA Club Waterford 2095 Abbeyside Parish & GAA CE Scheme Ltd Waterford 2286 Abbeyside United AFC Waterford 1372 Adamstown/St Abban's GAA Club Wexford 607 Adare Manor Golf Club Limerick 1302 Adrigole GAA Football Club Cork 621 Aer Lingus Bowls Club Dublin 3174 Affane Cappoquin GAA Waterford 2856 Aghabullogue Camogie Club Cork 3046 Aghabullogue GAA Club Cork 1088 Aghada GAA Club Cork 1179 Aghamore GAA Club Mayo 1208 Ahascragh-Fohenagh GAA Club Galway 2747 Aherlow GAA Club Tipperary 254 AIB Golfing Society Dublin 1951 Aisling Annacotty AFC Limited Limerick 2656 Ajax Orienteering Club Dublin 12 All Ireland Polo Club Dublin 1689 Allen Gaels GAA Club Leitrim 3270 Allenwood G F C Kildare 1280 Alpha Dive Meath 1294 An Creagan/Maigh Locha Galway 1971 An Riocht Stadium Limited Kerry 1210 An Tochar GAA Club Wicklow 2323 Angling Council of Ireland Dublin 1491 Annaduff GAA Club Leitrim 2081 Annagh Water Sports & Leisure Limited Longford 2824 Annaghdown GAA Club