Appropriation Accounts 2005

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

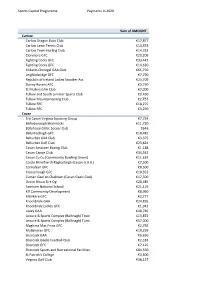

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow Carlow Dragon Boat Club €17,877 Carlow Lawn Tennis Club €14,353 Carlow Town Hurling Club €14,332 Clonmore GFC €23,209 Fighting Cocks GFC €33,442 Fighting Cocks GFC €14,620 Kildavin Clonegal GAA Club €61,750 Leighlinbridge GFC €7,790 Republic of Ireland Ladies Snooker Ass €23,709 Slaney Rovers AFC €3,750 St Mullins GAA Club €7,000 Tullow and South Leinster Sports Club €9,430 Tullow Mountaineering Club €2,757 Tullow RFC €18,275 Tullow RFC €3,250 Cavan 3rd Cavan Virginia Scouting Group €7,754 Bailieborough Shamrocks €11,720 Ballyhaise Celtic Soccer Club €646 Ballymachugh GFC €10,481 Belturbet GAA Club €3,375 Belturbet Golf Club €23,824 Cavan Amatuer Boxing Club €1,188 Cavan Canoe Club €34,542 Cavan Co Co (Community Bowling Green) €11,624 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) €7,500 Cornafean GFC €8,500 Crosserlough GFC €10,352 Cuman Gael an Chabhain (Cavan Gaels GAA) €17,500 Droim Dhuin Eire Og €20,485 Farnham National School €21,119 Kill Community Development €8,960 Killinkere GFC €2,777 Knockbride GAA €24,835 Knockbride Ladies GFC €1,942 Lavey GAA €48,785 Leisure & Sports Complex (Ballinagh) Trust €13,872 Leisure & Sports Complex (Ballinagh) Turst €57,000 Maghera Mac Finns GFC €2,792 Mullahoran GFC €10,259 Shercock GAA €6,650 Shercock Gaelic Football Club €2,183 Shercock GFC €7,125 Shercock Sports and Recreational Facilities €84,550 St Patrick's College €3,500 Virginia Golf Club €38,127 Sports Capital Programme Payments in 2020 Virginia Kayak Club €9,633 Cavan Castlerahan -

Killarney Outlook Sales: Des 087 659 3427 Or Email: [email protected]

Vol. 13 Edition 33: Friday 15th August 2014 : www.killarneyoutlook.com 15.08.14 1 Killarney Outlook Sales: Des 087 659 3427 or Email: [email protected] 2 15.08.14 Sales: Des 087 659 3427 or Email: [email protected] Killarney Outlook 15.08.14 3 NEWS DESK Editor: Aisling Crosbie 086 0400 958 or Email: [email protected] NEW SPIN ON THE RING LAUNCHED WRONG WAY AND HARD WAY ROUND CYCLES PLANNED FOR SEPTEMBER On Saturday, September 27 cycling enthusiasts from all over Ireland will travel to Killarney for the inaugural Wrong Way Round Killarney Cycling Festival where they will take on the stunning Ring of Kerry but in the opposite direction to the traditional anti-clockwise route. Cyclists will view the Ring like they have never seen it before as they head off from Killarney, before taking a right at Molls Gap and heading to Sneem. From there on the ON SATURDAY, SEPTEMBER 27 CYCLING ENTHUSIASTS FROM ALL OVER IRELAND WILL TRAVEL TO KILLARNEY FOR THE INAUGURAL WRONG WAY ROUND KILLARNEY CYCLING FESTIVAL. AT THE LAUNCH WERE FROM LEFT, PATRICK O’DONOGHUE, MD GLENEAGLE HOTEL, SEAN MULCHINOCK, FESTIVAL route is familiar, all be backwards, and takes AND EVENTS OPERATIONS MANAGER GLENEAGLE HOTEL, FIONNBAR WALSH, GRAND MARSHALL AND DENIS GEANEY. PHOTO: VALERIE O’SULLIVAN in Waterville, Cahersiveen, Glenbeigh and Killorglin. Then it’s the homeward stretch Cahersiveen. registration fees will be used to finance the along the foothills of the MacGillycuddy’s The festival is open to all levels of cyclists. There running of the event and any surplus made will Reeks through Beaufort. -

2010 League Presentations Dates for Your Diary GAA Email GAA Season

th Nuachtlitir Coiste Chontae Chorcaí: Vol. 2 No. 26, December 14 2010 Dates for Your 2010 League Presentations GAA Email Diary The presentation of cheques to the successful teams in Just a reminder: 16th December: Cork this year's RedFM Senior Hurling League took recently in where clubs have a GAA Clubs’ Draw, the RedFM Studios. In all, €11,000 was presented to change of secretary, Mitchelstown seven clubs - the top six, Midleton, Erin's Own, Sars, please ensure the th Killeagh, Na Piarsaigh and Glen Rovers, plus new secretary gets 20 December: Presentation of Bishopstown who completed their full league access to the GAA Munster Council programme and were thus entered into a draw for Email address. For Grants, time and €1000. County Chairman Jerry O'Sullivan and PRO any queries, contact venue tbc Gerard Lane both expressed their gratitude to Fiona [email protected] Darcy (CEO) and all at RedFM for their generous sponsorship of this competition. GAA Season 2011 Ticket 2011 Competitions The 2011 GAA The draws for the Season Ticket is now 2011 Evening Echo County Chairman Jerry O’Sullivan presents Midleton with their County on sale at a base price winners’ cheque. Also included are Fiona Darcy, Red FM CEO, and Pat of €75 (Juveniles Horgan, SHL Chairman. Championships €10). Rounds 1 and 2 were Cheques were also presented to the winners and made at Convention The Season Ticket th Scheme offers huge runners-up of all the other leagues at a recent function on December 12 – savings to fans, and is in Rochestown Park Hotel, where a total €29,725 was click here to view the available for either distributed between thirteen clubs. -

Central Statistics Office, Information Section, Skehard Road, Cork

Published by the Stationery Office, Dublin, Ireland. To be purchased from the: Central Statistics Office, Information Section, Skehard Road, Cork. Government Publications Sales Office, Sun Alliance House, Molesworth Street, Dublin 2, or through any bookseller. Prn 443. Price 15.00. July 2003. © Government of Ireland 2003 Material compiled and presented by Central Statistics Office. Reproduction is authorised, except for commercial purposes, provided the source is acknowledged. ISBN 0-7557-1507-1 3 Table of Contents General Details Page Introduction 5 Coverage of the Census 5 Conduct of the Census 5 Production of Results 5 Publication of Results 6 Maps Percentage change in the population of Electoral Divisions, 1996-2002 8 Population density of Electoral Divisions, 2002 9 Tables Table No. 1 Population of each Province, County and City and actual and percentage change, 1996-2002 13 2 Population of each Province and County as constituted at each census since 1841 14 3 Persons, males and females in the Aggregate Town and Aggregate Rural Areas of each Province, County and City and percentage of population in the Aggregate Town Area, 2002 19 4 Persons, males and females in each Regional Authority Area, showing those in the Aggregate Town and Aggregate Rural Areas and percentage of total population in towns of various sizes, 2002 20 5 Population of Towns ordered by County and size, 1996 and 2002 21 6 Population and area of each Province, County, City, urban area, rural area and Electoral Division, 1996 and 2002 58 7 Persons in each town of 1,500 population and over, distinguishing those within legally defined boundaries and in suburbs or environs, 1996 and 2002 119 8 Persons, males and females in each Constituency, as defined in the Electoral (Amendment) (No. -

2020 Season SSE Airtricity League Fixtures

SSE AIRTRICITY LEAGUE 2021 SEASON PREMIER DIVISION FIXTURE LIST VERSION 1st February 2021 SSE AIRTRICITY LEAGUE PREMIER DIVISION 2021 Presidents Cup Fri. 12 March 19:45 Shamrock Rovers Dundalk Tallaght Stadium Series 1 Fri. 19 March 19:45 Drogheda United Waterford United Park Fri. 19 March 20:00 Finn Harps Bohemians Finn Park Fri. 19 March 20:00 Shamrock Rovers St. Patrick's Athletic Tallaght Stadium Sat. 20 March 19:30 Longford Town Derry City Bishopsgate Sat. 20 March 19:45 Sligo Rovers Dundalk The Showgrounds Series 2 Fri. 26 March 19:45 Bohemians Longford Town Dalymount Park Fri. 26 March 19:45 Derry City Shamrock Rovers Ryan McBride Brandywell Stadium Fri. 26 March 19:45 Dundalk Finn Harps Oriel Park Fri. 26 March 19:45 St. Patrick's Athletic Drogheda United Richmond Park Fri. 26 March 19:45 Waterford Sligo Rovers Regional Sports Centre Series 3 Fri. 2 April 19:45 Drogheda United Finn Harps United Park Fri. 2 April 19:45 Derry City Waterford Ryan McBride Brandywell Stadium Fri. 2 April 19:45 Bohemians St. Patrick's Athletic Dalymount Park Fri. 2 April 20:00 Shamrock Rovers Dundalk Tallaght Stadium Sat. 3 April 19:30 Longford Town Sligo Rovers Bishopsgate Series 4 Fri. 9 April 20:00 Finn Harps Waterford Finn Park Fri. 9 April 19:45 Dundalk Bohemians Oriel Park Fri. 9 April 19:45 St. Patrick's Athletic Derry City Richmond Park Sat. 10 April 19:30 Longford Town Drogheda United Bishopsgate Sat. 10 April 19:45 Sligo Rovers Shamrock Rovers The Showgrounds Monday 12th/Tuesday 13th April - Reserve Date Series 5 Fri. -

Celebrating 101 Years

GAA Performance Analysis Seminar 4th February 2013 18:00 – 22:00 Mardyke Arena, University College Cork, Ireland Target Audience The Seminar aims to attract all key coaches/personnel involved in GAA clubs at all levels. The Seminar will highlight the significance of performance analysis within the game and the benefits it can bring to both teams and players. Proposed Program 18:00 – 18:30 Registration & Tea’s and Coffee’s 18:30 – 18:45 Opening/Welcome Address Overview of our facilities/services 18:45 – 19:45 Session 1: How Video Analysis is used to improve performance in both a Hurling & Football context? o Case Study: Going through all areas of analysis and highlighting the statistical report that is prepared and how this is used to improve performance. Speaker: Len Browne, Head of Performance Analysis, Mardyke Arena Speaker: Sean O’Donnell, Cork Senior Hurling Analyst 25 Minute Presentations & 10 Minutes Q& A 19:45 – 20:30 Session 2: The Benefits of Performance Analysis within a Team Environment: Coaches/Players Perspective 1. Billy Morgan, UCC Sigerson Head Coach & Ex Cork Senior Football Manager 2. Brian Cuthbert, Bishopstown G.A.A Head Coach/Cork Senior Football Selector 3. Ger Cunningham, UCC Fresher’s Hurling Head Coach & Ex Cork Senior Hurler 4. Noel Furlong, Carrigtwohill GAA Player 10 Minutes Presentations & 5 Minutes Q&A 1 GAA Performance Analysis Seminar 4th February 2013 18:00 – 22:00 Mardyke Arena, University College Cork, Ireland 20:30 – 21:30 Session 3: Active Recovery for Players: Demonstration on Hydrotherapy, Anti- Gravity Treadmills & Fitness Testing 20:30 – 20:50 Group A: Demo on Hydrotherapy Pool Group B: Demo on Anti-Gravity Treadmills Group C: Fitness Testing – Indoor Track 20:50 – 21:10 Group A: Demo on Anti-Gravity Treadmills Group B: Fitness Testing – Indoor Track Group C: Demo on Hydrotherapy Pool 21:10 – 21:30 Group A: Fitness Testing – Indoor Track Group B: Demo on Hydrotherapy Pool Group C: Demo on Anti-Gravity Treadmills 21:30 – 22:00 General Questions & Answers Session 2 . -

2007 Sports Capital Programme Allocations

2007 Sports Capital Programme Allocations County Organisation Amount Allocated Carlow Askea Karate CLub €3,000 Carlow Ballinkillen Hurling Club €80,000 Carlow Carlow Gymnastics Club €10,750 Carlow Carlow Martial Arts Sanctuary €10,000 Carlow Carlow Town Hurling Club €50,000 Carlow County Carlow Football Club €70,000 Carlow Éire Óg CLG [CARLOW] €90,000 Carlow Myshall GAA Club €100,000 Carlow New Oak Boys Football Club €40,000 Carlow OLD LEIGHLIN GFC €100,000 Carlow Palatine GAA Club €80,000 Carlow ST PATRICKS GAA CLUB (TULLOW) €70,000 Cavan Active Virginians €3,500 Cavan Bailieborough Shamrocks GAA €100,000 Cavan Ballyjamesduff Soccer Club €60,000 Cavan Ballymachugh G.F.C. €140,000 Cavan Belturbet Row Boat Club €6,000 Cavan Butlersbridge Gaelic Football Club €100,000 Cavan Castlerahan Community Development Ltd €60,000 Cavan Cootehill Celtic GAA €90,000 Cavan Cootehill Harps AFC €90,000 Cavan Cornafean GFC €50,000 Cavan County Cavan Rugby Football Club €150,000 Cavan Drumalee €18,000 Cavan Drumlane Community Partnership Ltd €9,000 Cavan Drumlane GAA Club €12,000 Cavan Drumlin Equestrian €65,000 Cavan kill community development €40,000 Cavan Killeshandra Leaguers GFC €75,000 Cavan Kingscourt Harps AFC €50,000 Cavan Knockbride G F C €100,000 Cavan Lavey GAA Club €70,000 Cavan Loch Gowna G.A.A. Club €100,000 Cavan Mullahoran GFC €60,000 Cavan Ramor United GFc & Ramor Community Sports Park €130,000 Cavan Templeport Saint Aidans GAA Club €50,000 Clare Aughinish Diving Club €20,000 Clare Bodyke GAA Club €35,000 Clare CLARE COUNTY COUNCIL €130,000 Clare Clarecastle GAA Club €30,000 Clare Clonlara Leisure Athletic and Sports Centre €100,000 Clare Clooney Quin GAA Club €60,000 Clare Cooraclare GAA Club €90,000 Clare CORBALLY UNITED €10,000 Clare Corofin GAA Club [CLARE] €35,000 Clare County Clare Agricultural Show Society Limited €90,000 Clare Cratloe Tennis Club €20,000 Clare Crusheen G.A.A. -

Rrec 26Nov10 E.Pdf

ISSUE ID: 2010/B/47 ANNUAL RETURNS RECEIVED BETWEEN 19-NOV-2010 AND 25-NOV-2010 INDEX OF SUBMISSION TYPES B1 - ANNUAL RETURN - NO ACCOUNTS B1AU - B1 WITH AUDITORS REPORT B1B - REPLACEMENT ANNUAL RETURN B1C - ANNUAL RETURN - GENERAL CRO GAZETTE, FRIDAY, 26th November 2010 3 ANNUAL RETURNS RECEIVED BETWEEN 19-NOV-2010 AND 25-NOV-2010 Company Company Document Date Of Company Company Document Date Of Number Name Receipt Number Name Receipt 2152 CLEVELAND INVESTMENTS B1AU 28/10/2010 18327 DOYLE HOTEL GROUP LIMITED B1C 27/10/2010 2857 QUILLS HOLDINGS LIMITED B1C 28/10/2010 18541 LANDENSTOWN ESTATES LIMITED B1C 28/10/2010 3394 CARRIGMAY LIMERICK, B1AU 28/10/2010 18543 BOART LONGYEAR LIMITED B1C 26/10/2010 3446 WATERFORD NEWS & STAR LIMITED B1C 26/10/2010 18571 NAVAN STEEL PRODUCTS LIMITED B1C 28/10/2010 3577 UNITED ARTS CLUB, DUBLIN, LIMITED B1C 16/11/2010 18749 EUROSNAX INTERNATIONAL LIMITED B1C 28/10/2010 4566 CORK BONDED WAREHOUSES, LIMITED B1C 28/10/2010 19044 NAT ROSS LIMITED B1C 28/10/2010 4784 J.W. GREEN & CO., (CORK) LIMITED B1C 28/10/2010 19054 WOOD - PRINTCRAFT LIMITED B1 28/10/2010 4966 WILLIS INSURANCE SERVICES (IRELAND) LIMITED B1C 27/10/2010 19308 LETT, DORAN & CO. LIMITED B1C 28/10/2010 7110 M & P SALES AND MARKETING LIMITED B1C 28/10/2010 19494 EXEL (EUROPEAN SERVICE CENTRE) B1C 27/10/2010 7138 ROBERT J. GOFF & CO. PUBLIC LIMITED B1C 13/10/2010 19741 JOHN O'DWYER LIMITED B1C 28/10/2010 COMPANY 19770 SHIRO B1AU 25/11/2010 7274 J. L. -

2020 Season SSE Airtricity League Fixtures

SSE AIRTRICITY LEAGUE 2021 SEASON PREMIER DIVISION FIXTURE LIST VERSION 1st February 2021 SSE AIRTRICITY LEAGUE PREMIER DIVISION 2021 Presidents Cup Fri. 12 March 19:45 Shamrock Rovers Dundalk Tallaght Stadium Series 1 Fri. 19 March 19:45 Drogheda United Waterford United Park Fri. 19 March 20:00 Finn Harps Bohemians Finn Park Fri. 19 March 20:00 Shamrock Rovers St. Patrick's Athletic Tallaght Stadium Sat. 20 March 19:30 Longford Town Derry City Bishopsgate Sat. 20 March 19:45 Sligo Rovers Dundalk The Showgrounds Series 2 Fri. 26 March 19:45 Bohemians Longford Town Dalymount Park Fri. 26 March 19:45 Derry City Shamrock Rovers Ryan McBride Brandywell Stadium Fri. 26 March 19:45 Dundalk Finn Harps Oriel Park Fri. 26 March 19:45 St. Patrick's Athletic Drogheda United Richmond Park Fri. 26 March 19:45 Waterford Sligo Rovers Regional Sports Centre Series 3 Fri. 2 April 19:45 Drogheda United Finn Harps United Park Fri. 2 April 19:45 Derry City Waterford Ryan McBride Brandywell Stadium Fri. 2 April 19:45 Bohemians St. Patrick's Athletic Dalymount Park Fri. 2 April 20:00 Shamrock Rovers Dundalk Tallaght Stadium Sat. 3 April 19:30 Longford Town Sligo Rovers Bishopsgate Series 4 Fri. 9 April 20:00 Finn Harps Waterford Finn Park Fri. 9 April 19:45 Dundalk Bohemians Oriel Park Fri. 9 April 19:45 St. Patrick's Athletic Derry City Richmond Park Sat. 10 April 19:30 Longford Town Drogheda United Bishopsgate Sat. 10 April 19:45 Sligo Rovers Shamrock Rovers The Showgrounds Monday 12th/Tuesday 13th April - Reserve Date Series 5 Fri. -

Audited Appropriation Accounts 2004

Audited Appropriation Accounts 2004 Appropriation Accounts of the Sums granted by the Oireachtas for Public Services for the year ended 31 December 2004 Presented pursuant to Section 3 (11) of the Comptroller and Auditor General (Amendment) Act, 1993 Baile Átha Cliath Arna fhoilsiú ag Oifig an tSoláthair Le ceannach díreach ón Oifig Dhíolta Foilseachán Rialtais, Teach Sun Alliance, Sráid Theach Laighean, Baile Átha Cliath 2 nó tríd an bpost ó Foilseacháin Rialtais, An Rannóg Post-Tráchta, 51 Faiche Stiabhna, Baile Átha Cliath 2 (Teil: 01-6476000, Fax: 01-4752760) nó trí aon díoltóir leabhar. Dublin Published by the Stationery Office To be purchased directly from the Government Publications Sales Office, Sun Alliance House, Molesworth Street, Dublin 2 or by mail order from Government Publications, Postal Trade Section, 51 St. Stephen’s Green, Dublin 2 (Tel: 01-6476000, Fax: 01-4752760) or through any bookseller. (Prn.A5/0039) Price €13.00 © Government of Ireland 2005 Table of Contents Page The Appropriation Accounts – An Introduction iii Duties of the Comptroller and Auditor General and Accounting Officers in relation to the Appropriation Accounts iii Statement of Accounting Policies and Principles v Statement by Accounting Officers on Internal Financial Control ix Summary of Appropriation Accounts xi Accounts President's Establishment 1 Department of the Taoiseach 7 Office of the Attorney General 14 Central Statistics Office 21 Office of the Comptroller and Auditor General 28 Office of the Minister for Finance 35 Superannuation and Retired -

STATUTORY INSTRUMENTS. SI No. 382 of 2021

STATUTORY INSTRUMENTS. S.I. No. 382 of 2021 ________________ HEALTH ACT 1947 (SECTION 31A - TEMPORARY RESTRICTIONS) (COVID-19) (NO. 2) (AMENDMENT) (NO. 8) REGULATIONS 2021 2 [382] S.I. No. 382 of 2021 HEALTH ACT 1947 (SECTION 31A - TEMPORARY RESTRICTIONS) (COVID-19) (NO. 2) (AMENDMENT) (NO. 8) REGULATIONS 2021 The Minister for Health, in exercise of the powers conferred on him by sections 5 and 31A (inserted by section 10 of the Health (Preservation and Protection and other Emergency Measures in the Public Interest) Act 2020 (No. 1 of 2020)) of the Health Act 1947 (No. 28 of 1947) and - (a) having regard to the immediate, exceptional and manifest risk posed to human life and public health by the spread of Covid-19 and to the matters specified in subsection (2) of section 31A, and (b) having consulted with the Minister for Foreign Affairs, the Minister for Housing, Local Government and Heritage, the Minister for Transport, the Minister for Enterprise, Trade and Employment, the Minister for Finance, the Minister for Justice and the Minister for Tourism, Culture, Arts, Gaeltacht, Sport and Media, hereby makes the following regulations: 1. These Regulations may be cited as the Health Act 1947 (Section 31A - Temporary Restrictions) (Covid-19) (No. 2) (Amendment) (No. 8) Regulations 2021. 2. These Regulations shall come into operation on the 24th day of July 2021. 3. The Health Act 1947 (Section 31A - Temporary Restrictions) (Covid-19) (No. 2) Regulations 2021 (S.I. No. 217 of 2021) are amended by the substitution of the Schedule to these Regulations for Schedule 3 to those Regulations. -

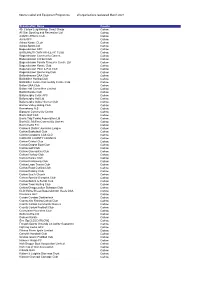

Grid Export Data

Sports Capital and Equipment Programme all organisations registered March 2021 Organisation Name County 4th Carlow Leighlinbrige Scout Group Carlow All Star Sporting and Recreation Ltd Carlow Ardattin Athletic Club Carlow Asca GFC Carlow Askea Karate CLub Carlow Askea Sports Ltd Carlow Bagenalstown AFC Carlow BAGENALSTOWN ATHLETIC CLUB Carlow Bagenalstown Community Games Carlow Bagenalstown Cricket Club Carlow Bagenalstown Family Resource Centre Ltd Carlow Bagenalstown Karate Club Carlow Bagenalstown Pitch & Putt Club Carlow Bagenalstown Swimming Club Carlow Ballinabranna GAA Club Carlow Ballinkillen Hurling Club Carlow Ballinkillen Lorum Community Centre Club Carlow Ballon GAA Club Carlow Ballon Hall Committee Limited Carlow Ballon Karate Club Carlow Ballymurphy Celtic AFC Carlow Ballymurphy Hall Ltd Carlow Ballymurphy Indoor Soccer Club Carlow Barrow Valley Riding Club Carlow Bennekerry N.S Carlow Bigstone Community Centre Carlow Borris Golf Club Carlow Borris Tidy Towns Association Ltd Carlow Borris/St. Mullins Community Games Carlow Burrin Celtic F.C. Carlow Carlow & District Juveniles League Carlow Carlow Basketball Club Carlow Carlow Carsports Club CLG Carlow CARLOW COUNTY COUNCIL Carlow Carlow Cricket Club Carlow Carlow Dragon Boat Club Carlow Carlow Golf Club Carlow Carlow Gymnastics Club Carlow Carlow Hockey Club Carlow Carlow Karate Club Carlow Carlow Kickboxing Club Carlow Carlow Lawn Tennis Club Carlow Carlow Road Cycling Club Carlow Carlow Rowing Club Carlow Carlow Scot's Church Carlow Carlow Special Olympics Club Carlow Carlow