Audited Appropriation Accounts 2004

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

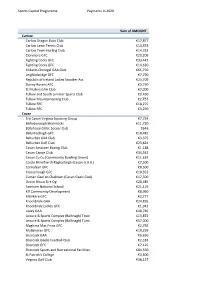

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow

Sports Capital Programme Payments in 2020 Sum of AMOUNT Carlow Carlow Dragon Boat Club €17,877 Carlow Lawn Tennis Club €14,353 Carlow Town Hurling Club €14,332 Clonmore GFC €23,209 Fighting Cocks GFC €33,442 Fighting Cocks GFC €14,620 Kildavin Clonegal GAA Club €61,750 Leighlinbridge GFC €7,790 Republic of Ireland Ladies Snooker Ass €23,709 Slaney Rovers AFC €3,750 St Mullins GAA Club €7,000 Tullow and South Leinster Sports Club €9,430 Tullow Mountaineering Club €2,757 Tullow RFC €18,275 Tullow RFC €3,250 Cavan 3rd Cavan Virginia Scouting Group €7,754 Bailieborough Shamrocks €11,720 Ballyhaise Celtic Soccer Club €646 Ballymachugh GFC €10,481 Belturbet GAA Club €3,375 Belturbet Golf Club €23,824 Cavan Amatuer Boxing Club €1,188 Cavan Canoe Club €34,542 Cavan Co Co (Community Bowling Green) €11,624 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) €7,500 Cornafean GFC €8,500 Crosserlough GFC €10,352 Cuman Gael an Chabhain (Cavan Gaels GAA) €17,500 Droim Dhuin Eire Og €20,485 Farnham National School €21,119 Kill Community Development €8,960 Killinkere GFC €2,777 Knockbride GAA €24,835 Knockbride Ladies GFC €1,942 Lavey GAA €48,785 Leisure & Sports Complex (Ballinagh) Trust €13,872 Leisure & Sports Complex (Ballinagh) Turst €57,000 Maghera Mac Finns GFC €2,792 Mullahoran GFC €10,259 Shercock GAA €6,650 Shercock Gaelic Football Club €2,183 Shercock GFC €7,125 Shercock Sports and Recreational Facilities €84,550 St Patrick's College €3,500 Virginia Golf Club €38,127 Sports Capital Programme Payments in 2020 Virginia Kayak Club €9,633 Cavan Castlerahan -

Killarney Outlook Sales: Des 087 659 3427 Or Email: [email protected]

Vol. 13 Edition 33: Friday 15th August 2014 : www.killarneyoutlook.com 15.08.14 1 Killarney Outlook Sales: Des 087 659 3427 or Email: [email protected] 2 15.08.14 Sales: Des 087 659 3427 or Email: [email protected] Killarney Outlook 15.08.14 3 NEWS DESK Editor: Aisling Crosbie 086 0400 958 or Email: [email protected] NEW SPIN ON THE RING LAUNCHED WRONG WAY AND HARD WAY ROUND CYCLES PLANNED FOR SEPTEMBER On Saturday, September 27 cycling enthusiasts from all over Ireland will travel to Killarney for the inaugural Wrong Way Round Killarney Cycling Festival where they will take on the stunning Ring of Kerry but in the opposite direction to the traditional anti-clockwise route. Cyclists will view the Ring like they have never seen it before as they head off from Killarney, before taking a right at Molls Gap and heading to Sneem. From there on the ON SATURDAY, SEPTEMBER 27 CYCLING ENTHUSIASTS FROM ALL OVER IRELAND WILL TRAVEL TO KILLARNEY FOR THE INAUGURAL WRONG WAY ROUND KILLARNEY CYCLING FESTIVAL. AT THE LAUNCH WERE FROM LEFT, PATRICK O’DONOGHUE, MD GLENEAGLE HOTEL, SEAN MULCHINOCK, FESTIVAL route is familiar, all be backwards, and takes AND EVENTS OPERATIONS MANAGER GLENEAGLE HOTEL, FIONNBAR WALSH, GRAND MARSHALL AND DENIS GEANEY. PHOTO: VALERIE O’SULLIVAN in Waterville, Cahersiveen, Glenbeigh and Killorglin. Then it’s the homeward stretch Cahersiveen. registration fees will be used to finance the along the foothills of the MacGillycuddy’s The festival is open to all levels of cyclists. There running of the event and any surplus made will Reeks through Beaufort. -

To Download Bray Wanderers V Athlone Town Matchday Programme 16.04.2021

Seagull Scene SSE Airtricity League First Division Season 2021 Vol. 37 No. 2 WELCOME TO THE CARLISLE BRAY WANDERERS FC I would like to welcome Adrian Carberry and his Athlone Town team and club officials to the Carlisle Grounds for this evening’s encounter. ROLL OF HONOUR FAI Cup Winners (2) Adrian has transformed the playing squad completely at Athlone Town this season including the additions of many 1990, 1999 familiar faces to Bray Wanderers fans with the arrival of First Division Champions (3) eight ex-Bray Wanderers players to their squad for this season. 1985/86, 1995/96, 1999/00 Athlone Town arrive at the Carlisle Grounds sitting top of First Division runners-up (2) the First Division and unbeaten after their opening three 1990/91, 1997/98 games with two wins and a draw. Shield Winners (1) Bray Wanderers are also unbeaten having drawn their 1995/96 three opening league games this season. Brandon Kavanagh produced a goal of the season contender National League B Division Champions (2) already with his magnificent second goal in the thrilling 3- 1991/92, 1998/99 3 draw away to Shelbourne a fortnight ago. Enda McGuill Cup (1) Goalkeeper Brian Maher was capped at under 21 level last 2005 month in a 2-1 away friendly win over Wales. Congratulations Brian! FAI Intermediate Cup Winners (2) 1955/56, 1957/58 Tonight we will get to see the new upgraded floodlights in the Carlisle grounds turned on for a match for the first time FAI Junior Cup Winners (2) which add to the recent improvements around the Carlisle 1955/56, 1957/58 Grounds. -

Grid Export Data

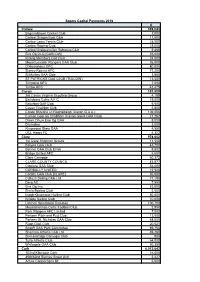

Sports Capital Payments 2018 € Carlow 389,043 Bagenalstown Cricket Club 7,000 Carlow Dragon Boat Club 11,500 Carlow Lawn Tennis Club 28,500 Carlow Rowing Club 18,000 Carlow/Graiguecullen Subaqua Club 9,468 Éire Óg CLG [CARLOW] 35,000 Killerig Members Golf Club 24,500 Mount Leinster Rangers GAA Club 36,000 O'Hanrahans GFC 80,000 Slaney Rovers AFC 71,250 St Mullins GAA Club 3,850 ST PATRICKS GAA CLUB (TULLOW) 13,500 Tinryland GFC 7,000 Tullow RFC 43,475 Cavan 183,809 3rd Cavan Virginia Scouting Group 4,189 Bailieboro Celtic A.F.C 19,000 Belturbet Golf Club 5,500 Cavan Triathlon Club 2,800 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) 109,686 Cuman Gael an Chabhain (Cavan Gaels GAA Club) 21,262 Droim Dhuin Eire Og GAA 9,000 Drumalee 3,500 Kingscourt Stars GAA 4,550 UCL Harps FC 4,322 Clare 978,602 1st Clare Shannon Scouts 11,500 Ballyea GAA Club 43,700 Banner GAA Club Ennis 9,602 Bridge United AFC 5,500 Clare Camogie 60,372 CLARE COUNTY COUNCIL 83,877 Clonlara GAA Club 54,000 CORBALLY UNITED 12,500 Corofin GAA Club [CLARE] 50,000 Cullaun Sailing Club Ltd 77,180 Derg AC 7,990 Eire Og Inis 53,000 Ennis Boxing Club 2,500 Inagh Kilnamona Hurling Club 50,000 Killaloe Sailing Club 10,000 Lahinch Sportsfield Comittee 100,700 Mountshannon Celtic Football Club 2,850 Park Rangers AFC Limited 7,000 Parteen Pitch and Putt Club 13,500 Parteen St. Nicholas GAA Club 68,000 Ruan GAA Club 20,621 Scariff GAA Park Committee 99,750 Shannon Athletic Club Ltd 39,260 Sixmilebridge Camogie Club 850 Tulla Athletic Club 64,000 Whitegate GAA Club 30,350 Cork 6,013,642 -

Official Handbook 2019/2020 Title Partner Official Kit Partner

OFFICIAL HANDBOOK 2019/2020 TITLE PARTNER OFFICIAL KIT PARTNER PREMIUM PARTNERS PARTNERS & SUPPLIERS MEDIA PARTNERS www.leinsterrugby.ie | From The Ground Up COMMITTEES & ORGANISATIONS OFFICIAL HANDBOOK 2019/2020 Contents Leinster Branch IRFU Past Presidents 2 COMMITTEES & ORGANISATIONS Leinster Branch Officers 3 Message from the President Robert Deacon 4 Message from Bank of Ireland 6 Leinster Branch Staff 8 Executive Committee 10 Branch Committees 14 Schools Committee 16 Womens Committee 17 Junior Committee 18 Youths Committee 19 Referees Committee 20 Leinster Rugby Referees Past Presidents 21 Metro Area Committee 22 Midlands Area Committee 24 North East Area Committee 25 North Midlands Area Committee 26 South East Area Committee 27 Provincial Contacts 29 International Union Contacts 31 Committee Meetings Diary 33 COMPETITION RESULTS European, UK & Ireland 35 Leagues In Leinster, Cups In Leinster 39 Provincial Area Competitions 40 Schools Competitions 43 Age Grade Competitions 44 Womens Competitions 47 Awards Ball 48 Leinster Rugby Charity Partners 50 FIXTURES International 51 Heineken Champions Cup 54 Guinness Pro14, Celtic Cup 57 Leinster League 58 Seconds League 68 Senior League 74 Metro League 76 Energia All Ireland League 89 Energia Womens AIL League 108 CLUB & SCHOOL INFORMATION Club Information 113 Schools Information 156 www.leinsterrugby.ie 1 OFFICIAL HANDBOOK 2019/2020 COMMITTEES & ORGANISATIONS Leinster Branch IRFU Past Presidents 1920-21 Rt. Rev. A.E. Hughes D.D. 1970-71 J.F. Coffey 1921-22 W.A. Daish 1971-72 R. Ganly 1922-23 H.J. Millar 1972-73 A.R. Dawson 1923-24 S.E. Polden 1973-74 M.H. Carroll 1924-25 J.J. Warren 1974-75 W.D. -

League Fixtures 2018 Season

Fri. 15 February Bohemians v Finn Harps Dalymount Park 7.45 pm Fri. 15 February Derry City v U.C.D. Ryan McBride Brandywell Stadium 7.45 pm Fri. 15 February Dundalk v Sligo Rovers Oriel Park 7.45 pm Fri. 15 February St. Patrick’s Athletic v Cork City Richmond Park 7.45 pm Fri. 15 February Waterford v Shamrock Rovers R.S.C. 7.45 pm Fri. 22 February Cork City v Waterford Turner’s Cross 7.45 pm Fri. 22 February Sligo Rovers v St. Patrick’s Athletic The Showgrounds 7.45 pm Fri. 22 February U.C.D. v Bohemians The UCD Bowl 7.45 pm Fri. 22 February Finn Harps v Dundalk Finn Park 8.00 pm Fri. 22 February Shamrock Rovers v Derry City Tallaght Stadium 8.00 pm Mon. 25 February Bohemians v Shamrock Rovers Dalymount Park 7.45 pm Mon. 25 February Derry City v Waterford Ryan McBride Brandywell Stadium 7.45 pm Mon. 25 February Dundalk v U.C.D. Oriel Park 7.45 pm Mon. 25 February St. Patrick’s Athletic v Finn Harps Richmond Park 7.45 pm Mon. 25 February Sligo Rovers v Cork City The Showgrounds 7.45 pm Fri. 1 March Cork City v Derry City Turner’s Cross 7.45 pm Fri. 1 March U.C.D. v St. Patrick’s Athletic The UCD Bowl 7.45 pm Fri. 1 March Waterford v Bohemians R.S.C. 7.45 pm Fri. 1 March Finn Harps v Sligo Rovers Finn Park 8.00 pm Fri. 1 March Shamrock Rovers v Dundalk Tallaght Stadium 8.00 pm Mon. -

Cloghroe, Blarney, Co. Cork. Cloghroe Pharmacy Tel: 021 438 2244 Congratulations to Our Christmas Hamper Winner Mrs Lil Healy

FREE January 2012 M USKERRY www.muskerrynews.biz NVolEWS 10, Issue 2 John O’Leary Autos Superior Servicing & Repairs carried out to all Blarney Auto Centre makes of cars, 4x4’s and light commercials The Square, Blarney MYLER INDUSTRIAL EST,, WEST VILLAGE, BALLINCOLLIG, CO. CORK. 021 4381528 MICHELINTYREAGENT Diagnostic Treat your car to Full mechanical checks available for a service at John services incl. all makes & models O'Leary Autos where brakes, clutches, from 1995 - 2009 personal service & FREE Winter checks suspension, Computerised print satisfaction is Lights, Wipers, Tyres, Fluids, Brakes, Tracking, Anti Freeze timing belts etc outs available guaranteed Serving the people of Blarney for 50 years For Booking contact John O’Leary @ 021 4870655 Mob: 087 2915551 Why not drop your doggie for grooming whilst you shop at Blackpool Shopping Centre? All Doggie New New New Hair Doo’s Full grooming service and Introducing new wash only available T: 021 4212394 Client Loyalty Cards M: 086 8478762 Don’t forget your Best Friend in 2012 Get one step closer to a fantastic All January clients will receive a offer with every visit. €5 off voucher off their next groom Wishing all our Clients a Mention this offer on arrival and Very Happy New Year receive a complimentary€ conditioning Selection of Clothing available to view LATE EVENING APPOINTMENTS AVAILABLE spray worth 15.90 (Offer valid until February 29th 2012) HairstylistJo's Edge Unit 6B, Woodfield, Station Road, Blarney. 4382739 086 8240422 Blarney DIY & Building Supplies Unit 1, Shean Lower, -

First Division Clubs in Europe 2014/15

CONTENTS | TABLE DES MATIÈRES | INHALTSVERZEICHNIS UEFA CLUB COMPETITIONS Calendar – 2014/15 UEFA CHAMPIONS LEAGUE 3 Calendar – 2014/15 UEFA EUROPA LEAGUE 4 UEFA MEMBER ASSOCIATIONS Albania | Albanie | Albanien 5 Andorra | Andorre | Andorra 7 Armenia | Arménie | Armenien 9 Austria | Autriche | Österreich 11 Azerbaijan | Azerbaïdjan | Aserbaidschan 13 Belarus | Belarus | Belarus 15 Belgium | Belgique | Belgien 17 Bosnia and Herzegovina | Bosnie-Herzégovine | Bosnien-Herzegowina 19 Bulgaria | Bulgarie | Bulgarien 21 Croatia | Croatie | Kroatien 23 Cyprus | Chypre | Zypern 25 Czech Republic | République tchèque | Tschechische Republik 27 Denmark | Danemark | Dänemark 29 England | Angleterre | England 31 Estonia | Estonie | Estland 33 Faroe Islands | Îles Féroé | Färöer-Inseln 35 Finland | Finlande | Finnland 37 France | France | Frankreich 39 Georgia | Géorgie | Georgien 41 Germany | Allemagne | Deutschland 43 Gibraltar / Gibraltar / Gibraltar 45 Greece | Grèce | Griechenland 47 Hungary | Hongrie | Ungarn 49 Iceland | Islande | Island 51 Israel | Israël | Israel 53 Italy | Italie | Italien 55 Kazakhstan | Kazakhstan | Kasachstan 57 Latvia | Lettonie | Lettland 59 Liechtenstein | Liechtenstein | Liechtenstein 61 Lithuania | Lituanie | Litauen 63 Luxembourg | Luxembourg | Luxemburg 65 Former Yugoslav Republic of Macedonia | ARY de Macédoine | EJR Mazedonien 67 Malta | Malte | Malta 69 Moldova | Moldavie | Moldawien 71 Montenegro | Monténégro | Montenegro 73 Netherlands | Pays-Bas | Niederlande 75 Northern Ireland | Irlande du Nord | Nordirland -

Official Handbook 2020/2021 Title Partner Offical Kit Partner

OFFICIAL HANDBOOK 2020/2021 TITLE PARTNER OFFICAL KIT PARTNER PREMIUM PARTNERS PARTNERS & SUPPLIERS MEDIA PARTNERS COMMITTEES & ORGANISATIONS www.leinsterrugby.ie 3 Contents Leinster Branch IRFU Past Presidents 4 COMMITTEES & ORGANISATIONS Leinster Branch Officers 5 Message from the President John Walsh 8 Message from Bank of Ireland 10 Leinster Branch Staff 13 Executive Committee 16 Branch Committees 22 Schools Committee 24 Womens Committee 25 Junior Committee 26 Youths Committee 27 Referees Committee 28 Metro Area Committee 30 Midlands Area Committee 32 North East Area Committee 33 North Midlands Area Committee 34 South East Area Committee 35 Provincial Contacts 39 International Union Contacts 42 Committee Meetings Diary 45 CLUB & SCHOOL INFORMATION Club Information 50 Inclusion Rugby 91 Touring Clubs / Youth Clubs 92 Schools Information 98 OFFICIAL HANDBOOK 2020/2021 COMMITTEES & ORGANISATIONS Leinster Branch IRFU Past Presidents 1920-21 Rt. Rev. A.E. Hughes D.D. 1972-73 A.R. Dawson 1921-22 W.A. Daish 1973-74 M.H. Carroll 1922-23 H.J. Millar 1974-75 W.D. Fraser 1923-24 S.E. Polden 1975-76 F.R. McMullen 1924-25 J.J. Warren 1976-77 P.F. Madigan 1925-26 E.M. Solomons M.A. 1977-78 K.D. Kelleher 1926-27 T.F. Stack 1978-79 I.B. Cairnduff 1927-28 A.D. Clinch M.D. 1979-80 P.J. Bolger 1928-29 W. G Fallon B.L. 1980-81 B. Cross 1929-30 W.H. Acton 1981-82 N.H. Brophy 1930-31 Mr. Justice Cahir Davitt 1982-83 E. Egan 1931-32 A.F. O’Connell 1983-84 P.J. -

2007 Sports Capital Programme Allocations

2007 Sports Capital Programme Allocations County Organisation Amount Allocated Carlow Askea Karate CLub €3,000 Carlow Ballinkillen Hurling Club €80,000 Carlow Carlow Gymnastics Club €10,750 Carlow Carlow Martial Arts Sanctuary €10,000 Carlow Carlow Town Hurling Club €50,000 Carlow County Carlow Football Club €70,000 Carlow Éire Óg CLG [CARLOW] €90,000 Carlow Myshall GAA Club €100,000 Carlow New Oak Boys Football Club €40,000 Carlow OLD LEIGHLIN GFC €100,000 Carlow Palatine GAA Club €80,000 Carlow ST PATRICKS GAA CLUB (TULLOW) €70,000 Cavan Active Virginians €3,500 Cavan Bailieborough Shamrocks GAA €100,000 Cavan Ballyjamesduff Soccer Club €60,000 Cavan Ballymachugh G.F.C. €140,000 Cavan Belturbet Row Boat Club €6,000 Cavan Butlersbridge Gaelic Football Club €100,000 Cavan Castlerahan Community Development Ltd €60,000 Cavan Cootehill Celtic GAA €90,000 Cavan Cootehill Harps AFC €90,000 Cavan Cornafean GFC €50,000 Cavan County Cavan Rugby Football Club €150,000 Cavan Drumalee €18,000 Cavan Drumlane Community Partnership Ltd €9,000 Cavan Drumlane GAA Club €12,000 Cavan Drumlin Equestrian €65,000 Cavan kill community development €40,000 Cavan Killeshandra Leaguers GFC €75,000 Cavan Kingscourt Harps AFC €50,000 Cavan Knockbride G F C €100,000 Cavan Lavey GAA Club €70,000 Cavan Loch Gowna G.A.A. Club €100,000 Cavan Mullahoran GFC €60,000 Cavan Ramor United GFc & Ramor Community Sports Park €130,000 Cavan Templeport Saint Aidans GAA Club €50,000 Clare Aughinish Diving Club €20,000 Clare Bodyke GAA Club €35,000 Clare CLARE COUNTY COUNCIL €130,000 Clare Clarecastle GAA Club €30,000 Clare Clonlara Leisure Athletic and Sports Centre €100,000 Clare Clooney Quin GAA Club €60,000 Clare Cooraclare GAA Club €90,000 Clare CORBALLY UNITED €10,000 Clare Corofin GAA Club [CLARE] €35,000 Clare County Clare Agricultural Show Society Limited €90,000 Clare Cratloe Tennis Club €20,000 Clare Crusheen G.A.A. -

Volunteer Recruitment Toolkit Developing the Strength of the GAA Volunteer Community

Volunteer Recruitment Toolkit Developing the strength of the GAA volunteer community www.gaa.ie Table of contents Introduction Why People Do and Do Not Volunteer Encouraging People to Volunteer Keeping New and Current Volunteers on Board Development of a Recruitment Strategy Other Points to Consider Provision of Training Appendices Introduction There is no organisation like the GAA. Nowhere in the world is there a to be asked, suggests strategies to keep those who are already there and lists national movement that has played such a positive role in the lives of its some approaches to attract those from outside the organisation who have citizens or has given such meaning and purpose to small communities, gifts and skills to offer the GAA. All of the ideas within have been tried and larger towns and the whole nation. GAA clubs with their wonderful found to succeed by clubs who helped us to create it. facilities are the jewel in the crown of the association and are its most important asset. Má usáideann coistí clubanna na smaointí seo, is dócha go mbeidh said abálta ní amhain fuil úr a mhealladh, a í a choinneáil chomh maith. It is the incredible work carried out by thousands of volunteers, young and old, male and female, from every single walk of life which drives this remarkable organisation and keeps it fresh, relevant and a critically important part of the lives of Irish people. Being involved in the GAA gives a sense of fulfilment which is unrivalled. It brings membership of the biggest club in Ireland, puts one right at the heart of Irish culture and provides a pastime for every member of the family. -

2020 U17 SSE Airtricity League First Division Fixture List

UNDER 17 SSE Airtricity League 2020 Season Fixture list Version 27TH FEBRUARY, 2020 2020 SSE AIRTRICITY National UNDER 17 LEAGUE Northern elite division FIXTURES WEEKEND ENDING SUNDAY 15th march 2020 – SERIES NO. 1 Sat, 14 Mar Derry City v Longford Town Ryan McBride 14:00 Brandywell Stadium Sat, 14 Mar Dundalk v Sligo Rovers Oriel Park 14:00 Sat, 14 Mar Athlone Town v Bohemians Athlone Town Stadium 14:00 Sat, 14 Mar Drogheda United v Shelbourne United Park 14:00 Sun, 15 Mar St. Patrick's Athletic v Finn Harps TU Dublin 14:00 Blanchardstown WEEKEND ENDING SUNDAY 22nd march 2020 – SERIES NO. 2 Sat, 21 Mar Bohemians v St. Patrick's Athletic St. Aidan's CBS 14:00 Sat, 21 Mar Sligo Rovers v Derry City The Showgrounds 14:00 Sun, 22 Mar Longford Town v Drogheda United Bishopsgate 14:00 Sun, 22 Mar Shelbourne v Athlone Town AUL Complex 14:00 Sun, 22 Mar Finn Harps v Dundalk The Curragh 14:00 WEEKEND ENDING SUNDAY 29th march 2020 – SERIES NO. 3 Sat, 28 Mar Athlone Town v Drogheda United Athlone Town Stadium 14:00 Sat, 28 Mar Longford Town v Sligo Rovers Bishopsgate 14:00 Sat, 28 Mar Derry City v Finn Harps Ryan McBride 14:00 Brandywell Stadium Sun, 29 Mar Dundalk v Bohemians Oriel Park 14:00 Sun, 29 Mar St. Patrick's Athletic v Shelbourne TU Dublin 14:00 Blanchardstown WEEKEND ENDING SUNDAY 5th april 2020 – SERIES NO. 4 Sat, 04 Apr Finn Harps v Longford Town The Curragh 14:00 Sat, 04 Apr Athlone Town v St.