Annual Report & Accounts 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Na Fianna Nuacht

Na Fianna Nuacht Inter Ladies – Champions! Wednesday 22nd August 2018 Junior C Championship Final will be remembered by the Na Fianna Ladies Inter team for all the right reasons. In what was described before the final by the DLGFA as “Expect a Cracker” certainly lived up to everybody’s expectations. A panel of 29 consisting of adult, minor and U16 players started preparation for Championship back in June. Right from the first training session we spoke about “giving this a real go” and the plan of playing a total of 6 matches to become Junior C Champions. That we did. Championship consisted of 2 groups of 5 teams with the top 2 from each group contesting the semi-finals. 1 of 6. We were away to Clontarf B. Great game played on probably one of the best surfaces in Dublin – St Anne’s pitch 35. We won 3-9 to 1-2. 2 of 6. We’re away again this time to St Brendan’s in Longmeadow’s. Little did we know then that we would be meeting them in the final a month later! A very difficult game with both sides very evenly matched. We won 3-10 to 2-9 3 of 6. Our first home game, Crumlin on back pitch. Game was played with great pace from our girls and we put up a strong score. We won 5-11 to 1-7. Na Fianna Nuacht 25ú Lúnasa 2018 1 Na Fianna Nuacht 4 of 6. Our second home fixture v Naomh Olaf this time on the best pitch in Dublin – front pitch Mobhi Rd. -

Annual Activity Report 2017

FINGAL LEADER PARTNERSHIP Annual Activity Report 2017 1 Contents 1. Introduction 3 2. Rural Dublin LEADER (DRL) 4 3. Tús Programme 13 4. Jobs Club 21 5. Organisation Development 23 6. Board of Directors 26 7. Staff 28 2 1. Introduction 2017 has been another very successful year for Fingal Leader Partnership. The Dublin Rural LEADR programme got off to a very strong start with project targets being met and, in some cases, exceeded. The Tús Programe has seen the successful placement of over 200 participants with over 130 participating non-profit organisations, assisting them to deliver much needed services for our local communities. The Care and Repair and the new Computer Home Support services operated under the Tús programme continues to go from strength to strength. The Jobs Club ensured that over half of all clients during the year either successfully regained employment or went on to further education. 2017 also saw the very successful move to our new offices and the integration of services into our new premises at DSV House in Swords Business Park. In February 2017 we appointed our new CEO, Dr. Chris O’Malley who, over the past year, has been successfully planning, formulating and managing the change process within the company. On behalf of the board I would like to take this opportunity to thank him for his guidance, direction, hard work and commitment to the company since his appointment. I would also like to take this opportunity to sincerely thank our Deputy CEO, Phil Moore, for her hard work and dedication to the company over the past number of years. -

LGAA Conv Book 04

Comhairle Laighean C.L.G. Tionolfar Comhdháil Cinn Bliana 2003 - 2004 In Jury’s Hotel, Ballsbridge Ar an hAoine, 27ú Feabhra 2004 6.15 pm 2 Kilkenny - Leinster Minor Hurling Champions 2003 Back L-R: S.Prendergast, N Delahunty, R Maher, P Doheny, D Prendergast, P Hartley, D Cody, J Tennyson, M Fennelly, J Dalton, R Wall, B Beckett, D McCormack. Front L-R: D Fogarty, A Murphy, P O'Donovan, M Nolan, E Guinan, R Power, S Cadogan, C Grant, E McGrath, A Healy, J Fitzpatrick, E O'Donoghue. Clár 6.15pm Registration 6.30pm High Tea 7.30pm (1) Convention Opens (2) Address by Cathaoirleach Coisde Co. Áth Cliath C.L.G. 7.45pm (1) Minutes of 2003 Convention (2) Discussion of Report of Chief Executive (3) Discussion of Sub-Committee Reports 8.10pm Ballot (Cisteoir) 8.15pm Review of Accounts of Comhairle Laighean C.L.G. 8.30pm Ballot (P.R.O.) 8.40pm Address by An Cathaoirleach 9.00pm Election of Officers 9.15pm Guest Speakers 9.30pm Na Rúin 9.40pm Tea/Coffee – Convention Closes Each county is entitled to the following Delegate representation at Convention, in addition to its two representatives on the Provincial Council: Ceatharloch 5 Cill Mhantain 6 Iarmhi 5 An Mhí 6 An Lú 5 Longphort 5 Cill Dara 6 Uibh Fháilí 6 Cill Chainnigh 5 Laois 6 Áth Cliath 6 Loch Garman 6 A brief meeting of the incoming Leinster Council will be held immediately after Convention, at which only urgent business to hand will be considered. NOTE 1. Slip on Admission Card to be handed to Hotel Management for High Tea (6.30pm) 2. -

Grid Export Data

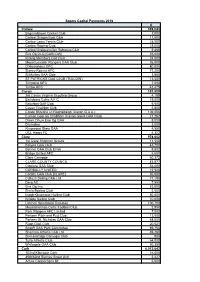

Sports Capital Payments 2018 € Carlow 389,043 Bagenalstown Cricket Club 7,000 Carlow Dragon Boat Club 11,500 Carlow Lawn Tennis Club 28,500 Carlow Rowing Club 18,000 Carlow/Graiguecullen Subaqua Club 9,468 Éire Óg CLG [CARLOW] 35,000 Killerig Members Golf Club 24,500 Mount Leinster Rangers GAA Club 36,000 O'Hanrahans GFC 80,000 Slaney Rovers AFC 71,250 St Mullins GAA Club 3,850 ST PATRICKS GAA CLUB (TULLOW) 13,500 Tinryland GFC 7,000 Tullow RFC 43,475 Cavan 183,809 3rd Cavan Virginia Scouting Group 4,189 Bailieboro Celtic A.F.C 19,000 Belturbet Golf Club 5,500 Cavan Triathlon Club 2,800 Coiste Bhreifne Uí Raghaillaigh (Cavan G.A.A.) 109,686 Cuman Gael an Chabhain (Cavan Gaels GAA Club) 21,262 Droim Dhuin Eire Og GAA 9,000 Drumalee 3,500 Kingscourt Stars GAA 4,550 UCL Harps FC 4,322 Clare 978,602 1st Clare Shannon Scouts 11,500 Ballyea GAA Club 43,700 Banner GAA Club Ennis 9,602 Bridge United AFC 5,500 Clare Camogie 60,372 CLARE COUNTY COUNCIL 83,877 Clonlara GAA Club 54,000 CORBALLY UNITED 12,500 Corofin GAA Club [CLARE] 50,000 Cullaun Sailing Club Ltd 77,180 Derg AC 7,990 Eire Og Inis 53,000 Ennis Boxing Club 2,500 Inagh Kilnamona Hurling Club 50,000 Killaloe Sailing Club 10,000 Lahinch Sportsfield Comittee 100,700 Mountshannon Celtic Football Club 2,850 Park Rangers AFC Limited 7,000 Parteen Pitch and Putt Club 13,500 Parteen St. Nicholas GAA Club 68,000 Ruan GAA Club 20,621 Scariff GAA Park Committee 99,750 Shannon Athletic Club Ltd 39,260 Sixmilebridge Camogie Club 850 Tulla Athletic Club 64,000 Whitegate GAA Club 30,350 Cork 6,013,642 -

2007 Sports Capital Programme Allocations

2007 Sports Capital Programme Allocations County Organisation Amount Allocated Carlow Askea Karate CLub €3,000 Carlow Ballinkillen Hurling Club €80,000 Carlow Carlow Gymnastics Club €10,750 Carlow Carlow Martial Arts Sanctuary €10,000 Carlow Carlow Town Hurling Club €50,000 Carlow County Carlow Football Club €70,000 Carlow Éire Óg CLG [CARLOW] €90,000 Carlow Myshall GAA Club €100,000 Carlow New Oak Boys Football Club €40,000 Carlow OLD LEIGHLIN GFC €100,000 Carlow Palatine GAA Club €80,000 Carlow ST PATRICKS GAA CLUB (TULLOW) €70,000 Cavan Active Virginians €3,500 Cavan Bailieborough Shamrocks GAA €100,000 Cavan Ballyjamesduff Soccer Club €60,000 Cavan Ballymachugh G.F.C. €140,000 Cavan Belturbet Row Boat Club €6,000 Cavan Butlersbridge Gaelic Football Club €100,000 Cavan Castlerahan Community Development Ltd €60,000 Cavan Cootehill Celtic GAA €90,000 Cavan Cootehill Harps AFC €90,000 Cavan Cornafean GFC €50,000 Cavan County Cavan Rugby Football Club €150,000 Cavan Drumalee €18,000 Cavan Drumlane Community Partnership Ltd €9,000 Cavan Drumlane GAA Club €12,000 Cavan Drumlin Equestrian €65,000 Cavan kill community development €40,000 Cavan Killeshandra Leaguers GFC €75,000 Cavan Kingscourt Harps AFC €50,000 Cavan Knockbride G F C €100,000 Cavan Lavey GAA Club €70,000 Cavan Loch Gowna G.A.A. Club €100,000 Cavan Mullahoran GFC €60,000 Cavan Ramor United GFc & Ramor Community Sports Park €130,000 Cavan Templeport Saint Aidans GAA Club €50,000 Clare Aughinish Diving Club €20,000 Clare Bodyke GAA Club €35,000 Clare CLARE COUNTY COUNCIL €130,000 Clare Clarecastle GAA Club €30,000 Clare Clonlara Leisure Athletic and Sports Centre €100,000 Clare Clooney Quin GAA Club €60,000 Clare Cooraclare GAA Club €90,000 Clare CORBALLY UNITED €10,000 Clare Corofin GAA Club [CLARE] €35,000 Clare County Clare Agricultural Show Society Limited €90,000 Clare Cratloe Tennis Club €20,000 Clare Crusheen G.A.A. -

Audited Appropriation Accounts 2004

Audited Appropriation Accounts 2004 Appropriation Accounts of the Sums granted by the Oireachtas for Public Services for the year ended 31 December 2004 Presented pursuant to Section 3 (11) of the Comptroller and Auditor General (Amendment) Act, 1993 Baile Átha Cliath Arna fhoilsiú ag Oifig an tSoláthair Le ceannach díreach ón Oifig Dhíolta Foilseachán Rialtais, Teach Sun Alliance, Sráid Theach Laighean, Baile Átha Cliath 2 nó tríd an bpost ó Foilseacháin Rialtais, An Rannóg Post-Tráchta, 51 Faiche Stiabhna, Baile Átha Cliath 2 (Teil: 01-6476000, Fax: 01-4752760) nó trí aon díoltóir leabhar. Dublin Published by the Stationery Office To be purchased directly from the Government Publications Sales Office, Sun Alliance House, Molesworth Street, Dublin 2 or by mail order from Government Publications, Postal Trade Section, 51 St. Stephen’s Green, Dublin 2 (Tel: 01-6476000, Fax: 01-4752760) or through any bookseller. (Prn.A5/0039) Price €13.00 © Government of Ireland 2005 Table of Contents Page The Appropriation Accounts – An Introduction iii Duties of the Comptroller and Auditor General and Accounting Officers in relation to the Appropriation Accounts iii Statement of Accounting Policies and Principles v Statement by Accounting Officers on Internal Financial Control ix Summary of Appropriation Accounts xi Accounts President's Establishment 1 Department of the Taoiseach 7 Office of the Attorney General 14 Central Statistics Office 21 Office of the Comptroller and Auditor General 28 Office of the Minister for Finance 35 Superannuation and Retired -

Grid Export Data

Sports Capital and Equipment Programme all organisations registered March 2021 Organisation Name County 4th Carlow Leighlinbrige Scout Group Carlow All Star Sporting and Recreation Ltd Carlow Ardattin Athletic Club Carlow Asca GFC Carlow Askea Karate CLub Carlow Askea Sports Ltd Carlow Bagenalstown AFC Carlow BAGENALSTOWN ATHLETIC CLUB Carlow Bagenalstown Community Games Carlow Bagenalstown Cricket Club Carlow Bagenalstown Family Resource Centre Ltd Carlow Bagenalstown Karate Club Carlow Bagenalstown Pitch & Putt Club Carlow Bagenalstown Swimming Club Carlow Ballinabranna GAA Club Carlow Ballinkillen Hurling Club Carlow Ballinkillen Lorum Community Centre Club Carlow Ballon GAA Club Carlow Ballon Hall Committee Limited Carlow Ballon Karate Club Carlow Ballymurphy Celtic AFC Carlow Ballymurphy Hall Ltd Carlow Ballymurphy Indoor Soccer Club Carlow Barrow Valley Riding Club Carlow Bennekerry N.S Carlow Bigstone Community Centre Carlow Borris Golf Club Carlow Borris Tidy Towns Association Ltd Carlow Borris/St. Mullins Community Games Carlow Burrin Celtic F.C. Carlow Carlow & District Juveniles League Carlow Carlow Basketball Club Carlow Carlow Carsports Club CLG Carlow CARLOW COUNTY COUNCIL Carlow Carlow Cricket Club Carlow Carlow Dragon Boat Club Carlow Carlow Golf Club Carlow Carlow Gymnastics Club Carlow Carlow Hockey Club Carlow Carlow Karate Club Carlow Carlow Kickboxing Club Carlow Carlow Lawn Tennis Club Carlow Carlow Road Cycling Club Carlow Carlow Rowing Club Carlow Carlow Scot's Church Carlow Carlow Special Olympics Club Carlow Carlow -

Nuachtlitirmárta 2016

MARCH 2016 NUACHTLITIR MÁRTA 2016 FOR NEWS, VIDEOS AND FIXTURES www.gaa.ie Football Hurling Club General GAA DEFIBRILLATOR SAVED MY LIFE by Cian Murphy t was a Thursday night kick around people suffering instances of cardiac with the lads just like any other. But arrest continue to cause shock among the events of October 11, 2010 would communities around Ireland. change Seaghan Kearney’s life forever. I It’s estimated that every year in Ireland He was playing indoor football in Dublin’s there are 80 such instances which happen St Oliver Plunkett’s Eoghan Ruadha with to people in the 14-35 year-old bracket. club mates when his life was suddenly Only last month Leitrim U21 footballer Alan and scarily turned upside down as this McTigue suffered a cardiac incident and apparently fit and healthy 30 year-old was thankfully survived. Sadly there have been floored by a massive heart attack. many more instances where the results have not been as positive. The quick thinking of his team mates was crucial but, ultimately, it was the presence Initially when Seaghan Kearney dropped of a GAA approved defibrillator on the to the ground his friends thought he had premises, and the availability of a trained slipped. But they soon realised something person who could use it, ensured that this more serious was at play. shocking event didn’t become much more tragic. What happened in the next few critical minutes was where fortune came to “On a Monday night a few of the lads Seaghan’s salvation. would meet and play five a side in the hall in Plunkett’s and that night was the same Working in the club that night as a as any other - only in the middle of the volunteer in the bar was Terry O’Brien – a game my heart stopped and I had a massive trained Paramedic. -

LEGISLATIVE RESOLUTION Honoring Larry Mccarthy Upon the Occasion of His Designation for Special Recognition by the Rockland Gaelic Athletic Association

LEGISLATIVE RESOLUTION honoring Larry McCarthy upon the occasion of his designation for special recognition by the Rockland Gaelic Athletic Association WHEREAS, It is the sense of this Legislative Body to recognize that the quality and character of life in the communities across New York State are reflective of the concerned and dedicated efforts of those organiza- tions and individuals who would devote themselves to the welfare of the community and its citizenry; and WHEREAS, Attendant to such concern, and in full accord with its long- standing traditions, this Legislative Body is justly proud to honor Larry McCarthy upon the occasion of his designation for special recogni- tion by the Rockland Gaelic Athletic Association on Saturday, November 7, 2009; and WHEREAS, Larry McCarthy was born in Cork, Ireland, and holds a Ph.D. in Sports Management from Ohio State University; currently, he is an associate professor of management at the W. Paul Stillman School of Business at Seton Hall University where he teaches in the Center for Sports Management, and also serves as the Director of the Institute of International Business; and WHEREAS, Previously, Larry McCarthy was the Graduate Sports Management Program coordinator in the Department of Recreation & Sports Management at Georgia Southern University; he earned an M.A. degree from New York University (NYU), and a B.Ed. degree from the National University of Ireland (NUI); and WHEREAS, Larry McCarthy has published research articles in national and international journals for professional sports -

March Newsletter 2006.Lnk

Email: [email protected] www.castleknock.net Cumann Báire agus Peile Chaisleán Cnucha Castleknock Hurling & Football Club VOLUME 4, ISSUE 3 NEWSLETTER MARCH 2006 Blanchardstown Renault sponsor Car for Castleknock Hurling and Football Club Many thanks to John Quilter (Blanchardstown Renault) and Rory Doogan (Renault Ireland) who sponsored a car for Castleknock Hurling & Football Club. Pictured to the left are: (L-R) Daire O'Neill (GPO), John Quilter (Blanchardstown Renault), Rory Doogan (Renault Ireland & Junior Footballer), Mick Lynch (CHFC Club Chairman) & Eamonn Connor (Juvenile Chairman). U9 BOYS ENJOY TRIP TO CROKE PARK The U9 Squad had a great day out in Croke Park where they had a guided tour of the Stadium. They started in the tunnel underneath the Cusack Stand and ended up in the top tier. The tour included the dressing rooms and the Corporate boxes and the lads learned lots of interesting facts about the history and construction of Croke Park. Next they stopped off at a Shooting Alley where they got a chance to practice their Hurling and Football shooting skills. Then it was on to the GAA Museum and Shop where the kids maxed-out on souvenir pens and pencils. The squad arrived home well fed and well informed. Thanks to all the parents who came along and the U9s themselves, who were very well behaved (most of the time anyway). THE DOCUMENT SHOP Inside this issue: ST. PATRICKS SCHOOL • Colour Copy and Printing up to A3 • A3 colour copies €0.70 each - A4 Black €0.10 each • Laminating, Binding, Booklets finished up to 100 pages, Liam McCarthy Cup 2 Castleknock Hurling & Glossy Brochures, Business Cards visits Castleknock Football Club • Mail Merge, MS Access Database Design and Programming Win for Junior B 2 Footballers Would like to congratulate the •Small quantities a speciality • —————–—— Win for U10A Girls 2 teachers and pupils of St. -

Cuntais Leithreasa Iniúchta 2005

Cuntais Leithreasa Iniúchta 2005 Cuntais Leithreasa de na Suimeanna arna ndeonú ag an Oireachtas le haghaidh Seirbhísí Poiblí don bhliain dar chríoch 31 Nollaig 2005 Arna dtíolacadh faoi réir Alt 3(10) den Acht Ard-Reachtaire Cuntas agus Ciste (Leasú), 1993 Baile Átha Cliath Arna fhoilsiú ag Oifig an tSoláthair Le ceannach díreach ón Oifig Dhíolta Foilseachán Rialtais, Teach Sun Alliance, Sráid Theach Laighean, Baile Átha Cliath 2 nó tríd an bpost ó Foilseacháin Rialtais, An Rannóg Post-Tráchta, 51 Faiche Stiabhna, Baile Átha Cliath 2 (Teil: 01-6476000, Fax: 01-4752760) nó trí aon díoltóir leabhar. (Prn. A6/0431) Praghas €13.00 © Rialtas na hÉireann 2006 Clár Ábhair Leathanach Na Cuntais Oiriúnacha – Tabhairt Isteach iii Dualgais an Ard-Reachtaire Cuntas agus Ciste agus na n-Oifigeach Cuntasóireachta i leith na gCuntas Oiriúnaigh. iii Ráiteas Polasaithe agus Prionsabal Cuntasóireachta v Ráiteas ag Oifigigh Cuntasóireachta ar Smacht Airgeadúil Inmheánach ix Achomair de Chuntais Oiriúnacha xi Cuntais Teaghlachas an Uachtaráin 1 Roinn an Taoisigh 6 Oifig an Ard-Aighne 14 An Phríomh-Oifig Staidrimh 21 Oifig an Ard-Reachtaire Cuntas agus Ciste 28 Oifig an Aire Airgeadais 35 Aoisliúntas agus Liúntais Scoir 44 Oifig na gCoimisinéirí Achomhairc 48 Oifig na gCoimisinéirí Ioncaim 52 Oifig na nOibreacha Poiblí 58 An tSaotharlann Stáit 70 Rúnseirbhís 77 Oifig an Phríomh-Aturnae Stáit 80 Oifig an Stiúrthóra Ionchúiseamh Poiblí 87 An Oifig Luachála 92 i An tSeirbhís um Cheapachain Phoiblí 98 Oifig an Choimisiúin um Cheapacháin Serbhíse Poiblí 105 Oifig -

Appropriation Accounts 2008

Comptroller and Auditor General Appropriation Accounts 2008 Accounts for presentation to Dáil Éireann pursuant to Section 3 (11) of the Comptroller and Auditor General (Ammendment) Act, 1993 September 2009 © Government of Ireland 2009 Table of Contents Page Part 1: Introduction The Appropriation Accounts 7 Duties of Accounting Officers in relation to the Appropriation Accounts 8 Duties of the Comptroller and Auditor General in relation to the Appropriation Accounts 9 Part 2: Appropriation Accounts Statement of Accounting Policies and Principles 15 Standard Statement on Internal Financial Control 19 Vote 1 President's Establishment 21 Vote 2 Department of the Taoiseach 27 Vote 3 Office of the Attorney General 35 Vote 4 Central Statistics Office 43 Vote 5 Office of the Comptroller and Auditor General 49 Vote 6 Office of the Minister for Finance 57 Vote 7 Superannuation and Retired Allowances 67 Vote 8 Office of the Appeal Commissioners 73 Vote 9 Office of the Revenue Commissioners 77 Vote 10 Office of Public Works 85 Vote 11 State Laboratory 97 Vote 12 Secret Service 105 Vote 13 Office of the Chief State Solicitor 109 Vote 14 Office of the Director of Public Prosecutions 117 Vote 15 Valuation Office 123 Vote 16 Public Appointments Service 131 Vote 17 Office of the Commission for Public Service Appointments 137 3 Vote 18 Office of the Ombudsman 143 Vote 19 Office of the Minister for Justice, Equality and Law Reform 149 Vote 20 Garda Síochána 163 Vote 21 Prisons 175 Vote 22 The Courts Service 185 Vote 23 Property Registration Authority 193