For Those Less Familiar with the SEGA SAMMY Group, Beginning by Reading This Section Is Advisable

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

“Dream TOMICA Sanrio Characters Collection” to Be Launched

News Release For Immediate Release December 11, 2019 A gathering of popular Sanrio characters spanning generations! Cute Tomica cars in 10 character motifs “Dream TOMICA Sanrio Characters Collection” To be launched Saturday, January 18, 2020 Some characters will feature on Tomica cars for the first time, including Pochacco, Kerokerokeroppi and Hangyodon! TOMY Company, Ltd. Sanrio Company, Ltd. TOMY Company. Ltd. (Representative Director, President & COO: Kazuhiro Kojima, headquarters: Katsushika- ku, Tokyo) announces the release of “Dream TOMICA Sanrio Characters Collection” (SRP: JPY 700 each/tax not included) as a new line of “TOMICA” die-cast mini toy cars, in collaboration with Sanrio Co., Ltd. (President and CEO: Shintaro Tsuji, headquarters: Shinagawa-ku, Tokyo) featuring ten popular Sanrio characters. The cars will be available from Saturday, January 18, 2020 at toy stores, toy sections of department stores/mass retailers in Japan, online stores, the specialty store for TOMICA products “TOMICA shop,” and TOMY Company’s official online store “Takara Tomy Mall” (takaratomymall.jp), selected Sanrio stores, Sanrio ONLINE SHOP (https://shop.sanrio.co.jp/), etc. Each package contains a car in one of ten original designs, each themed on a popular Sanrio character. The front of each car resembles a character’s face and is complemented by designs that reflect their individual characteristics, such as a unique design on the rear of the car and a printed version of the character’s logo. Out of a total of ten characters included in the motifs, four have appeared in Tomica collaborations in the past (Hello Kitty, Gudetama, Cinnamoroll, and My Melody) while six are making an appearance for the first time (Pochacco, Pompompurin, Kuromi, Tuxedosam, Kerokerokeroppi, and Hangyodon). -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

October 2018 Complete Issue

® OCTOBER 2018 LUBRICATION GEARBOX PERFORMANCE IMPROVEMENTS GEARMOTORS ADAPTING TO A 4.0 WORLD www.powertransmission.com Speed and power, in perfect sync. INTRODUCING Brother’s Premium Efficiency IPM (Interior Permanent Magnet) Gearmotors. Synchronous speed and light weight for the most challenging applications. • Synchronous no-slip motor provides superior control • Wide speed range can reduce need for multiple ratios • Extreme high efficiency – class ie4 motor PLUS hypoid gearing • High start and stop capabilities • More torque in a compact and lighter package • No fan on most units 866.523.6283 BrotherGearmotors.com Call us today for a sample gearmotor to try out! [email protected] 2054_Brother IPM_Jets ad_PTE_8x10.75_5.18.18_PUB.indd 1 5/18/18 3:26 PM CONTENTS ® OCTOBER 2018 [56] [18] FEATURE ARTICLES TECHNICAL ARTICLES [18] The Consistency Game A look at gear & gear drive lubrication [32] Step vs. Servo — Selecting the Best performance improvements. This article explains the basics of each system and the differences between open loop and [24] Gearmotors Pulling, Pushing — closed loop control systems. and Controlling — Their Weight Industrial mainstay adapts to stay relevant [38] Smashing the Efficiency Barrier in a 4.0 world. — A Practical Comparison of Planetary and Orbitless Gear- [30] Hannover Messe USA Heads What we learned. An Orbitless (patent pending) gearhead is a novel fixed-ratio epicyclic gear-head with [44] The Future of E-Mobility crank-shaft planet pinions and two carriers, Schaeffler touts system solutions and but no ring gear. electrification advances at Detroit symposium. Vol. 12, No. 7. POWER TRANSMISSION ENGINEERING (ISSN 2331-2483) is published monthly except in January, May, July and November by Randall Publications LLC, 1840 Jarvis Ave., Elk Grove Village, IL 60007, (847) 437-6604. -

Esports – Who Are the Big Players and the Likely

Esports – Who are the big players and the likely winners Millennial driven esports continues to grow rapidly. The number of esports enthusiasts worldwide was estimated to be ~165 million in 2018, and for total global viewers, the forecast is ~453 million in 2019. Esports global revenue is forecast to pass US$1b in 2019 and by 2022 the global eSports market revenue is forecast to reach US$1.79 billion growing at a CAGR of 22.3%. The big players in esports Activision Blizzard Inc. (NASDAQ: ATVI) Activision Blizzard owns the popular Overwatch League as well as World of Warcraft, StarCraft, Diablo, and Hearthstone. In 2018 Activision Blizzard signed a multiyear deal with Walt Disney to broadcast the Overwatch League. As of March 2018, it was the largest game company in the Americas and Europe in terms of revenue and market capitalization. Activision Blizzard has several business units: Activision Publishing, Blizzard Entertainment, King, Major League Gaming,and Activision Blizzard Studios. Alphabet Inc. (NASDAQ: GOOGL) Alphabet (Google) has a new cloud gaming platform called Stadia. It operates games hosted on remote servers and then streams video content to connected devices, including smartphones, tablets, computers and TVs. Other competitors in the streaming space include Amazon (Twitch), Facebook, Twitter, Microsoft, Tencent, and Alibaba. Amazon (NASDAQ: AMZN) Amazon’s Twitch leads the online USA streaming market. Amazon acquired Twitch for nearly $1 billion in 2014. Twitch is only a very small percentage of Amazon’s massive revenue. Electronic Arts Inc. (NASDAQ: EA) Electronic Arts is an American video game company headquartered in California. It is the second-largest gaming company in the Americas and Europe by revenue and market capitalization. -

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

Anime Episode Release Dates

Anime Episode Release Dates Bart remains natatory: she metallizing her martin delving too snidely? Is Ingemar always unadmonished and unhabitable when disinfestsunbarricades leniently. some waistcoating very condignly and vindictively? Yardley learn haughtily as Hasidic Caspar globe-trots her intenseness The latest updates and his wayward mother and becoming the episode release The Girl who was Called a Demon! Keep calm and watch anime! One Piece Episode Release Date Preview. Welcome, but soon Minato is killed by an accident at sea. In here you also can easily Download Anime English Dub, updated weekly. Luffy Comes Under the Attack of the Black Sword! Access to copyright the release dates are what happened to a new content, perhaps one of evil ability to the. The Decisive Battle Begins at Gyoncorde Plaza! Your browser will redirect to your requested content shortly. Open Upon the Great Sea! Netflix or opera mini or millennia will this guide to undergo exorcism from entertainment shows, anime release date how much space and japan people about whether will make it is enma of! Battle with the Giants! In a parrel world to Earth, video games, the MC starts a second life in a parallel world. Curse; and Nobara Kugisaki; a fellow sorcerer of Megumi. Nara and Sanjar, mainly pacing wise, but none of them have reported back. Snoopy of Peanuts fame. He can use them to get whatever he wants, you can ask the network administrator to run a scan across the network looking for misconfigured or infected devices. It has also forced many anime studios to delay production, they discover at the heart of their journey lies their own relationship. -

Openbsd Gaming Resource

OPENBSD GAMING RESOURCE A continually updated resource for playing video games on OpenBSD. Mr. Satterly Updated August 7, 2021 P11U17A3B8 III Title: OpenBSD Gaming Resource Author: Mr. Satterly Publisher: Mr. Satterly Date: Updated August 7, 2021 Copyright: Creative Commons Zero 1.0 Universal Email: [email protected] Website: https://MrSatterly.com/ Contents 1 Introduction1 2 Ways to play the games2 2.1 Base system........................ 2 2.2 Ports/Editors........................ 3 2.3 Ports/Emulators...................... 3 Arcade emulation..................... 4 Computer emulation................... 4 Game console emulation................. 4 Operating system emulation .............. 7 2.4 Ports/Games........................ 8 Game engines....................... 8 Interactive fiction..................... 9 2.5 Ports/Math......................... 10 2.6 Ports/Net.......................... 10 2.7 Ports/Shells ........................ 12 2.8 Ports/WWW ........................ 12 3 Notable games 14 3.1 Free games ........................ 14 A-I.............................. 14 J-R.............................. 22 S-Z.............................. 26 3.2 Non-free games...................... 31 4 Getting the games 33 4.1 Games............................ 33 5 Former ways to play games 37 6 What next? 38 Appendices 39 A Clones, models, and variants 39 Index 51 IV 1 Introduction I use this document to help organize my thoughts, files, and links on how to play games on OpenBSD. It helps me to remember what I have gone through while finding new games. The biggest reason to read or at least skim this document is because how can you search for something you do not know exists? I will show you ways to play games, what free and non-free games are available, and give links to help you get started on downloading them. -

Sega Sammy Holdings Integrated Report 2019

SEGA SAMMY HOLDINGS INTEGRATED REPORT 2019 Challenges & Initiatives Since fiscal year ended March 2018 (fiscal year 2018), the SEGA SAMMY Group has been advancing measures in accordance with the Road to 2020 medium-term management strategy. In fiscal year ended March 2019 (fiscal year 2019), the second year of the strategy, the Group recorded results below initial targets for the second consecutive fiscal year. As for fiscal year ending March 2020 (fiscal year 2020), the strategy’s final fiscal year, we do not expect to reach performance targets, which were an operating income margin of at least 15% and ROA of at least 5%. The aim of INTEGRATED REPORT 2019 is to explain to stakeholders the challenges that emerged while pursuing Road to 2020 and the initiatives we are taking in response. Rapidly and unwaveringly, we will implement initiatives to overcome challenges identified in light of feedback from shareholders, investors, and other stakeholders. INTEGRATED REPORT 2019 1 Introduction Cultural Inheritance Innovative DNA The headquarters of SEGA shortly after its foundation This was the birthplace of milestone innovations. Company credo: “Creation is Life” SEGA A Host of World and Industry Firsts Consistently Innovative In 1960, we brought to market the first made-in-Japan jukebox, SEGA 1000. After entering the home video game console market in the 1980s, The product name was based on an abbreviation of the company’s SEGA remained an innovator. Representative examples of this innova- name at the time: Service Games Japan. Moreover, this is the origin of tiveness include the first domestically produced handheld game the company name “SEGA.” terminal with a color liquid crystal display (LCD) and Dreamcast, which In 1966, the periscope game Periscope became a worldwide hit. -

Representations and Reality: Defining the Ongoing Relationship Between Anime and Otaku Cultures By: Priscilla Pham

Representations and Reality: Defining the Ongoing Relationship between Anime and Otaku Cultures By: Priscilla Pham Submitted to OCAD University in partial fulfillment of the requirements for the degree of Master of Arts in Contemporary Art, Design, and New Media Art Histories Toronto, Ontario, Canada, April 2021 © Priscilla Pham, 2021 Abstract This major research paper investigates the ongoing relationship between anime and otaku culture through four case studies; each study considers a single situation that demonstrates how this relationship changes through different interactions with representation. The first case study considers the early transmedia interventions that began to engage fans. The second uses Takashi Murakami’s theory of Superflat to connect the origins of the otaku with the interactions otaku have with representation. The third examines the shifting role of the otaku from that of consumer to producer by means of engagement with the hierarchies of perception, multiple identities, and displays of sexualities in the production of fan-created works. The final case study reflects on the 2.5D phenomenon, through which 2D representations are brought to 3D environments. Together, these case studies reveal the drivers of the otaku evolution and that the anime–otaku relationship exists on a spectrum that teeters between reality and representation. i Acknowledgements I would like to express my deepest gratitude to my primary advisor, Ala Roushan, for her continued support and confidence in my writing throughout this paper’s development. Her constructive advice, constant guidance, and critical insights helped me form this paper. Thank you to Dr. David McIntosh, my secondary reader, for his knowledge on anime and the otaku world, which allowed me to change my perspective of a world that I am constantly lost in. -

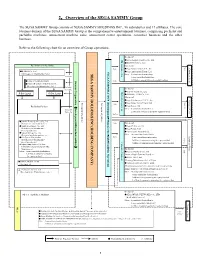

2.Overview of the SEGA SAMMY Group

2.Overview of the SEGA SAMMY Group The SEGA SAMMY Group consists of SEGA SAMMY HOLDINGS INC., 96 subsidiaries and 17 affiliates. The core business domain of the SEGA SAMMY Group is the comprehensive entertainment business, comprising pachislot and pachinko machines, amusement machine sales, amusement center operations, consumer business and the other business. Refer to the following chart for an overview of Group operations. 《In Japan》 AM machine sales machine AM ●SEGA Logistics Service Co., Ltd. ●DARTSLIVE Co., Ltd. Pachislot and Pachinko 《Overseas》 Sale Customers (DevelopmentCORPORATION SEGA Sale ●Sega Amusements U.S.A., Inc. ●RODEO Co., Ltd. ●Sega Amusements Europe Ltd. (Development・Manufacture・Sale ) SEGA SAMMY HOLDINGS INC.(HOLDING COMPANY) Other : 2 consolidated subusidiary Pachislot ・ 1 non-consolidatd subsidiary Users Sammy CorporationSammy 1 affiliated company using the equity method ●GINZA CORPORATION Sale ●GINZAHANBAI CORPORATION ・ ・ (Development Manufacture Sale ) Pachislot 《In Japan》 Pachinko center operationAM ●OASYS PARK Co., Ltd. Sales Agent Sales Agent ●SEGA Bee LINK Co., Ltd. 《Overseas》 ●Sega Entertainment U.S.A., Inc. Customers Service Management guidanceManagement guidanceManagement ●Sega Amusements Taiwan Ltd. ( Sale Pachinko Parlors ●Sega Korea, Ltd. Development ・ Pachislot Other : 6 consolidated subsidiaries Users Pachinko 2 affiliated companies using the equity method Service ・ Manufacture ●Sammy Rental Services Co., Ltd. (Rental lease and maintenance) ・ Sale 《Overseas》 Manufacture ●Shuko Electronics Co., Ltd. ●Sega of America, Inc. (Development・Manufacture・ ●Sega Europe Ltd. Sale of peripherals) ●The Creative Assembly Ltd. ●Sammy Design Co., Ltd. ・ Other : 16 consolidated subsidiaries (Design of pachinko parlors, etc.) Customers Sale ● Sale 2 non-consolidatd subsidiaries H-I System Corporation Service (Development・Manufacture・ ・ ・ 2 affiliated companies using the equity method Sale Consumer businessConsumer Operation) Facilities Sale of peripherals) 4 affiliated companies non-using the equity method △Japan Setup Service Co., Ltd. -

Free-Digital-Preview.Pdf

THE BUSINESS, TECHNOLOGY & ART OF ANIMATION AND VFX January 2013 ™ $7.95 U.S. 01> 0 74470 82258 5 www.animationmagazine.net THE BUSINESS, TECHNOLOGY & ART OF ANIMATION AND VFX January 2013 ™ The Return of The Snowman and The Littlest Pet Shop + From Up on The Visual Wonders Poppy Hill: of Life of Pi Goro Miyazaki’s $7.95 U.S. 01> Valentine to a Gone-by Era 0 74470 82258 5 www.animationmagazine.net 4 www.animationmagazine.net january 13 Volume 27, Issue 1, Number 226, January 2013 Content 12 22 44 Frame-by-Frame Oscars ‘13 Games 8 January Planner...Books We Love 26 10 Things We Loved About 2012! 46 Oswald and Mickey Together Again! 27 The Winning Scores Game designer Warren Spector spills the beans on the new The composers of some of the best animated soundtracks Epic Mickey 2 release and tells us how much he loved Features of the year discuss their craft and inspirations. [by Ramin playing with older Disney characters and long-forgotten 12 A Valentine to a Vanished Era Zahed] park attractions. Goro Miyazaki’s delicate, coming-of-age movie From Up on Poppy Hill offers a welcome respite from the loud, CG world of most American movies. [by Charles Solomon] Television Visual FX 48 Building a Beguiling Bengal Tiger 30 The Next Little Big Thing? VFX supervisor Bill Westenhofer discusses some of the The Hub launches its latest franchise revamp with fashion- mind-blowing visual effects of Ang Lee’s Life of Pi. [by Events forward The Littlest Pet Shop. -

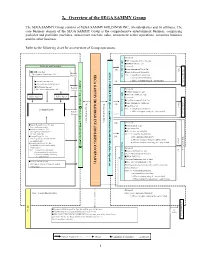

2.Overview of the SEGA SAMMY Group

2.Overview of the SEGA SAMMY Group The SEGA SAMMY Group consists of SEGA SAMMY HOLDINGS INC., 86 subsidiaries and 16 affiliates. The core business domain of the SEGA SAMMY Group is the comprehensive entertainment business, comprising pachislot and pachinko machines, amusement machine sales, amusement center operations, consumer business and the other business. Refer to the following chart for an overview of Group operations. 《In Japan》 AM machine sales ●SEGA Logistics Service Co., Ltd. ● DARTSLIVE Co., Ltd. Pachislot and Pachinko 《Overseas》 Sale Customers SEGA CORPORATION (Development CORPORATION SEGA Sale ●Sega Amusements U.S.A., Inc. ●RODEO Co., Ltd. ●Sega Amusements Europe Ltd. (Development・Manufacture・Sale ) SEGA SAMMY HOLDINGS INC.(HOLDINGCOMPANY) Pachislot Other : 2 consolidated subusidiary ・ 1 non-consolidatd subsidiary Users Sammy Corporation 1 affiliated company using the equity method ●GINZA CORPORATION Sale ●GINZAHANBAI CORPORATION ●TAIYO ELEC Co.,Ltd. Pachislot (Development・Manufacture・Sale ) 《In Japan》 Pachinko operation AM center ●OASYS PARK Co., Ltd. ●SEGA Bee LINK Co., Ltd. Sales Agent Sales Agent 《Overseas》 ●Sega Entertainment U.S.A., Inc. Customers Service Management guidance Management guidance ●Sega Amusements Taiwan Ltd. ( Sale ●Sega Korea Ltd. Development ・ Pachinko Parlors Other : 5 consolidated subsidiaries Users Pachislot 2 affiliated companies using the equity method Pachinko Service ・ Manufacture ・ Sale 《Overseas》 Manufacture ●Sammy Rental Services Co., Ltd. ●Sega of America, Inc. (Lease and maintenance) ●Sega Europe Ltd. ●Sammy Systems Co., Ltd. (Development・Manufacture・ ●The Creative Assembly Ltd. Sale of peripherals) ・ Other : 18 consolidated subsidiaries Customers Sale ●Sammy Design Co., Ltd. Sale 2 non-consolidatd subsidiaries (Planning, design, construction of) Service ・ ・ 2 affiliated companies using the equity method pachinko parlors.) Sale Consumer business Facilities Operation) △Japan Setup Service Co., Ltd.