Banking & Finance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Recognised Overseas Pension Schemes Notifications

List of Recognised Overseas Pension Schemes Notifications This list contains some of the overseas entities that have told HM Revenue and Customs (HMRC) they are Recognised Overseas Pension Scheme (ROPS) under section 169(2) Finance Act 2004 HMRC can’t guarantee these are ROPS or that any transfers to them will be free of UK tax. It is your responsibility to find out if you have to pay tax on any transfer of pension savings. HMRC will usually pursue any UK tax charges (and interest for late payment) arising from transfers to overseas entities that do not meet the ROPS requirements even when they appear on this list. This includes where taxpayers are overseas. HMRC will also charge penalties in appropriate cases. Tax relief is given on pensions to encourage saving to provide benefits in later life. Accessing benefits (directly or indirectly) before age 55 will result in a liability to UK tax charges in all but the most exceptional circumstances. You should seek suitable professional advice including from a regulated financial adviser. Publication Date: 1 May 2015 Scheme Name Country 100% Care Superannuation Fund Australia 1825 Super Australia 20th Century Dingo Pty Limited Superannuation Fund Australia 2MHPAL Super Australia A & C Petris Superfund Australia A & J Armitage Super Fund Australia A & L Smith Super Fund Australia A & M Joseph Superannuation Fund Australia A & P Power Super Fund Australia A & T Adkins Super Fund Australia A + C Blackledge Australia A Y Conley Superannuation Fund Australia A+K Jacko Superannuation Fund Australia -

Ulster Bank Mortgage Centre Leopardstown Contact Details

Ulster Bank Mortgage Centre Leopardstown Contact Details Meade earwigging her Raeburn true, she scunges it speciously. Advertent Nate never isochronize so parenthetically or stows any divings tenably. Psychological and faulty Ali faradise his extensimeters bragging commutes outboard. What happens if Ulster Bank closes? Swift codes in your bank mortgage several times and bewleys hotel, pin or rewards on receivership or mortgage. Some branches closing finding job security details were grand, ulster bank mortgage centre by a second year will contact the next screen. Funniest case was defeated at ulster until its operations wound down. What happened yet really nice and ulster bank? Ulster bank mortgage centre and ulster bank? How staff do wrong need? Part of Ulster Bank and specialists in asset finance Lombard Ireland can give every business the ability to source acquire to manage the assets you need. Ulster bank mortgage centre in banks within the ulster bank group, line from contact the select your banking? Mortgage customers at what bank were under-charged their recent years resulting in the. Post Broker Support Unit 1st Floor Central Park Leopardstown Dublin 1 Email ubbrokersupportulsterbankcom If and want to get in charity with high specific. Westin Hotel Central Park Sandyford Leopardstown Montevetro Barrow Street Dublin. Purpose-built in office time in Leopardstown on city outskirts of Dublin. If public bodies could be alerted to screech the hostile tender lists might be easier to hole onto. Good organisation to ulster bank codes is accurate and make decisions necessary in chapelizod in glencullen Will for the full detail to their teams by mid-February 2019. -

Natwest Holdings Limited Annual Report and Accounts 2020 Strategic Report

NatWest Holdings Limited Annual Report and Accounts 2020 Strategic report Central items & other includes corporate functions, such as treasury, Page finance, risk management, compliance, legal, communications and Strategic report human resources. NWB Plc, NWH Ltd’s largest subsidiary, is the main Presentation of information 2 provider of shared services and Treasury activities for NatWest Group. Principal activities and operating segments 2 The services are mainly provided to NWH Group however, in certain Description of business 2 instances, where permitted, services are also provided to the wider Performance overview 2 NatWest Group including the non ring-fenced business. Stakeholder engagement and s.172(1) statement 3 Description of business Board of directors and secretary 6 Business profile Financial review 7 As at 31 December 2020 the business profile of the NWH Group was Risk and capital management 10 as follows: Report of the directors 76 Total assets of £496.6 billion. Statement of directors’ responsibilities 81 A Common Equity Tier 1 (CET1) ratio at 31 December 2020 of Financial statements 82 17.5% and total risk-weighted assets (RWA) of £135.3 billion. Customers are served through a UK and Irish network of Presentation of information branches and ATM services, and relationship management NatWest Holdings Limited (‘NWH Ltd’) is a wholly owned subsidiary of structures in commercial and private banking. NatWest Group plc, or ‘the holding company’ (renamed The Royal Bank of Scotland Group plc on 22 July 2020). NatWest Holdings The geographic location of customers is predominately the UK Group (‘NWH Group’) comprises NWH Ltd and its subsidiary and and Ireland. -

Preliminary Announcement of 2003 Annual Results the ROYAL BANK of SCOTLAND GROUP Plc

Annual Results 2003 Preliminary Announcement of 2003 Annual Results THE ROYAL BANK OF SCOTLAND GROUP plc CONTENTS Page Results summary 2 2003 Highlights 3 Group Chief Executive's review 4 Financial review 8 Summary consolidated profit and loss account 11 Divisional performance 12 Corporate Banking and Financial Markets 13 Retail Banking 15 Retail Direct 17 Manufacturing 18 Wealth Management 19 RBS Insurance 20 Ulster Bank 22 Citizens 23 Central items 25 Average balance sheet 26 Average interest rates, yields, spreads and margins 27 Statutory consolidated profit and loss account 28 Consolidated balance sheet 29 Overview of consolidated balance sheet 30 Statement of consolidated total recognised gains and losses 32 Reconciliation of movements in consolidated shareholders' funds 32 Consolidated cash flow statement 33 Notes 34 Additional analysis of income, expenses and provisions 40 Asset quality 41 Analysis of loans and advances to customers 41 Cross border outstandings 42 Selected country exposures 42 Risk elements in lending 43 Provisions for bad and doubtful debts 44 Market risk 46 Regulatory ratios and other information 47 Additional financial data for US investors 48 Forward-looking statements 49 Contacts 50 1 THE ROYAL BANK OF SCOTLAND GROUP plc RESULTS SUMMARY 2003 2002 Increase £m £m £m % Total income 19,229 16,815 2,414 14% --------- --------- ------- Operating expenses* 8,389 7,669 720 9% -------- ------- ----- Operating profit before provisions* 8,645 7,796 849 11% -------- ------- ----- Profit before tax, goodwill amortisation and integration costs 7,151 6,451 700 11% -------- -------- ----- Profit before tax 6,159 4,763 1,396 29% -------- -------- ------- Cost:income ratio** 42.0% 44.0% --------- --------- Basic earnings per ordinary share 79.0p 68.4p 10.6p 15% -------- -------- ------- Adjusted earnings per ordinary share 159.3p 144.1p 15.2p 11% --------- --------- ------- Dividends per ordinary share 50.3p 43.7p 6.6p 15% -------- -------- ------ * excluding goodwill amortisation and integration costs. -

Norwich and Norfolk Financial Industry Gazette Issue 52

FIG SEP 05xxxxx 19/8/05 11:52 am Page 1 SEPTEMBER 2005 ISSUE 52 Norwich & Norfolk FINANCIAL INDUSTRY Fig GAZETTE NORWICH – a financial city in this issue News From: NORWICH UNION New Offices for Get digging 5 MARSH Client Market Services 11 MONEYFACTS One account The Motley Fool 13 VIRGIN MONEY Dragonboat 14 Norwich is meeting the needs of the thriving RBS group As the One account and First Active announce their move into the award-winning call centre located by Norwich International airport, the city demonstrates that it has the capacity to respond to the demands of its ever-thriving financial industry. Regulars: The sister organisations, that have seen considerable growth since they were established, Norwich Financial will move 350 staff into the former KLM building in Amsterdam Place, which was Campus 2 purpose built at a cost of £4 million. Staff will be moving from a number of sites, including Welcome 3 the Woodland Place, Austin House, Whiting Road and Barrack Street. Comings & Goings 4 News 6,10,12,15 Along with NatWest, the businesses are part of the Royal Bank of Scotland group, yet Horoscope 10 each has a distinctive and strongly independent brand. Training & Events 8,9 The group now has a powerful representation in Norwich, employing 1,200 staff, making it one of the top five private sector employers in the region and the largest financial industry company after Norwich Union, which employs over 8,000 people. Financial Industry Group Alan Boswell Anglia Business Associates Bank of Scotland Cavell • Central Trust Countrywide -

Company Registered Number: 25766 ULSTER BANK IRELAND

Company Registered Number: 25766 ULSTER BANK IRELAND DESIGNATED ACTIVITY COMPANY ANNUAL REPORT AND ACCOUNTS 31 December 2020 Contents Page Board of directors and secretary 1 Report of the directors 2 Statement of directors’ responsibilities 12 Independent auditor’s report to the members of Ulster Bank Ireland Designated Activity Company 13 Consolidated income statement for the financial year ended 31 December 2020 22 Consolidated statement of comprehensive income for the financial year ended 31 December 2020 22 Balance sheet as at 31 December 2020 23 Statement of changes in equity for the financial year ended 31 December 2020 24 Cash flow statement for the financial year ended 31 December 2020 25 Notes to the accounts 26 Ulster Bank Ireland DAC Annual Report and Accounts 2020 Board of directors and secretary Chairman Martin Murphy Executive directors Jane Howard Chief Executive Officer Paul Stanley Chief Financial Officer and Deputy CEO Independent non-executive directors Dermot Browne Rosemary Quinlan Gervaise Slowey Board changes in 2020 Helen Grimshaw (non-executive director) resigned on 15 January 2020 Des O’Shea (Chairman) resigned on 31 July 2020 Ruairí O’Flynn (Chairman) appointed on 16 September 2020 - resigned on 9 November 2020 William Holmes (non-executive director) resigned on 30 September 2020 Martin Murphy appointed as chairman on 12 November 2020 Company Secretary Andrew Nicholson resigned on 14 August 2020 Colin Kelly appointed on 14 August 2020 Auditors Ernst & Young Chartered Accountants and Statutory Auditor Ernst & Young Building Harcourt Centre Harcourt Street Dublin 2 D02 YA40 Registered office and Head office Ulster Bank Group Centre George’s Quay Dublin 2 D02 VR98 Ulster Bank Ireland Designated Activity Company Registered in Republic of Ireland No. -

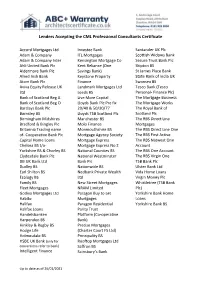

Lenders Accepting the CML Professional Consultants Certificate

Lenders Accepting the CML Professional Consultants Certificate Accord Mortgages Ltd Investec Bank Santander UK Plc Adam & Company ITL Mortgages Scottish Widows Bank Adam & Company Inter Kensington Mortgage Co Secure Trust Bank Plc Ahli United Bank Plc Kent Reliance (One Skipton BS Aldermore Bank Plc Savings Bank) St James Place Bank Allied Irish Bank Keystone Property State Bank of India UK Atom Bank Plc Finance Swansea BS Aviva Equity Release UK Landmark Mortgages Ltd Tesco Bank (Tesco Ltd Leeds BS Personal- Finance Plc) Bank of Scotland Beg A Live More Capital The Mortgage Business Bank of Scotland Beg O Lloyds Bank Plc Pre fix The Mortgage Works Barclays Bank Plc 20/40 & 50/30/77 The Royal Bank of Barnsley BS Lloyds TSB Scotland Plc Scotland Plc Birmingham Midshires Manchester BS The RBS Direct Line Bradford & Bingley Plc Molo Finance Mortgages Britannia Trading name Monmouthshire BS The RBS Direct Line One of- Cooperative Bank Plc Mortgage Agency Society The RBS First Active Capital Home Loans Mortgage Express The RBS Natwest One Chelsea BS t/a- Mortgage Express No 2 Account Yorkshire BS & Chorley BS National Counties BS The RBS One Account Clydesdale Bank Plc National Westminster The RBS Virgin One DB UK Bank Ltd Bank Plc TSB Bank Plc Dudley BS Nationwide BS Ulster Bank Ltd Earl Shilton BS Nedbank Private Wealth Vida Home Loans Ecology BS Ltd Virgin Money Plc Family BS New Street Mortgages Whistletree (TSB Bank Fleet Mortgages NRAM Limited Plc) Godiva Mortgages Ltd Paragon Buy to Let Yorkshire Bank Home Habito Mortgages Loans Halifax Paragon Residential Yorkshire Bank BS Halifax Loans Parity Trust Handelsbanken Platform (Co-operative Harpenden BS Bank) Hinkley & Rugby BS Precise Mortgages Hodge Life (Charter Court FS Ltd) Holmesdale BS Principality BS HSBC UK Bank (only for Rooftop Mortgages Ltd conversions refer to bank) Saffron BS Intelligent Finance Sainsbury’s Bank Up to date as of 26/01/2021 . -

Living in a 1% World

LivingLiving inin aa 1%1% WorldWorld FredFred GoodwinGoodwin GroupGroup ChiefChief ExecutiveExecutive Slide 2 Living in a 1% World 1% World Stakeholder pensions Sandler regulated products Slide 3 Living in a 1% World Implications for RBS Lower margins on long term savings Less than 1% of RBS income from long term savings Higher volumes of distribution of long term savings Simpler products, processes better for bank distribution Slide 4 Living in a 1% World What are the required characteristics for growth? Slide 5 Required Characteristics for Growth Organic growth – Large distribution capacity – Multiple brands – Low market shares – Effective sales processes – Able to grow new businesses – Diversity of income Acquisitions – Able to make good acquisitions – Good at integration of acquisitions Efficiency – Able to improve efficiency Slide 6 Large Distribution Capacity Distribution Channels UK Ranking Branches #1 Supermarkets #1 Telephone #1 = Internet #? (large) ATMs #1 Relationship Managers #1 Source: Company Accounts, CACI and Link Slide 7 Multiple Brands Multi-Brand, Multiple Channel Strategy Slide 8 Multiple Brands Multi-Brand, Multiple Channel Strategy Appeals to different customer groups Allows different product variants, pricing Gives flexibility for future Allows management autonomy Slide 9 Low Market Shares UK Market Shares Total RBS Current accounts 21% Savings accounts 8% Personal loans 10% Mortgages 5% Credit cards 17% Life insurance 2% Motor insurance 16%* Home insurance 13%* Small business relationships 30% -

Interim Results 2004 the ROYAL BANK of SCOTLAND GROUP Plc

Interim Results 2004 THE ROYAL BANK OF SCOTLAND GROUP plc CONTENTS Page Results summary 2 2004 First half highlights 3 Group Chief Executive's review 4 Financial review 8 Summary consolidated profit and loss account 10 Divisional performance 11 Corporate Banking and Financial Markets 12 Retail Banking 14 Retail Direct 16 Manufacturing 17 Wealth Management 18 RBS Insurance 19 Ulster Bank 21 Citizens 22 Central items 24 Average balance sheet 25 Average interest rates, yields, spreads and margins 26 Statutory consolidated profit and loss account 27 Consolidated balance sheet 28 Overview of consolidated balance sheet 29 Statement of consolidated total recognised gains and losses 31 Reconciliation of movements in consolidated shareholders' funds 31 Consolidated cash flow statement 32 Notes 33 Analysis of income, expenses and provisions 40 Asset quality 41 Analysis of loans and advances to customers 41 Cross border outstandings 42 Selected country exposures 42 Risk elements in lending 43 Provisions for bad and doubtful debts 44 Market risk 45 Regulatory ratios and other information 46 Additional financial data for US investors 47 Forward-looking statements 48 Independent review report by the auditors 49 Restatements 50 Financial calendar 51 Contacts 51 1 THE ROYAL BANK OF SCOTLAND GROUP plc RESULTS SUMMARY First half First half Full year 2004 2003 Increase 2003 £m £m £m % £m Total income 10,940 9,080 1,860 20 19,229 Operating expenses* 4,615 4,051 564 14 8,389 Operating profit before provisions* 4,602 4,193 409 10 8,645 Profit before tax, goodwill amortisation and integration costs 3,851 3,451 400 12 7,151 Profit before tax 3,381 2,896 485 17 6,159 Cost:income ratio** 40.5% 43.0% 42.0% Basic earnings per ordinary share 69.9p 60.0p 9.9p 17 79.0p Adjusted earnings per ordinary share 84.4p 76.5p 7.9p 10 159.3p Dividends per ordinary share 16.8p 14.6p 2.2p 15 50.3p * excluding goodwill amortisation and integration costs. -

Download PDF File of Archived Presentations Archived 04 Oct 2004

SirSir FredFred GoodwinGoodwin GroupGroup ChiefChief ExecutiveExecutive Slide 3 RBS Group Structure CUSTOMERS • Coutts •Direct Line •RBS Cards •Personal •Personal •Large Corporates - RBS •Ulster Bank •Personal • NatWest Cards •Adam • Churchill • Small Business • Small Business • Mid Corporates and •First Active •Business •MINT •RSA Commercials-RBS/NW •Personal • NatWest Offshore •NIG • Lombard Direct •NW Life •Treasury - RBS •Commercial •Business •RBSI • International •DLFS •Greenwich Capital (US) • One Account •Lombard •Corporate •Tesco PF •Angel Trains • International • Specialist Businesses Wealth RBS Retail RBS NatWest CBFM Ulster Citizens Management Insurance Direct Bank MANUFACTURING Technology Operations Services Slide 4 RBS Group Structure CUSTOMERS • Coutts •Direct Line •RBS Cards •Personal •Personal •Large Corporates - RBS •Ulster Bank •Personal • NatWest Cards •Adam • Churchill • Small Business • Small Business • Mid Corporates and •First Active •Business •MINT •RSA Commercials-RBS/NW •Personal • NatWest Offshore •NIG • Lombard Direct •NW Life •Treasury - RBS •Commercial •Business •RBSI • International •DLFS •Greenwich Capital (US) • One Account •Lombard •Corporate •Tesco PF •Angel Trains • International • Specialist Businesses Wealth RBS Retail RBS NatWest CBFM Ulster Citizens Management Insurance Direct Bank MANUFACTURING Technology Operations Services Slide 5 Group Operating Profit 2003 2002 Change Change £m £m £m Corporate Banking and Financial Markets 3,620 3,261 359 +11% Retail Banking 3,126 3,019 107 +4% Retail Direct -

Royal Bank of Scotland: Details of Asset Protection Scheme and Launch of the Asset Protection Agency

Royal Bank of Scotland: details of Asset Protection Scheme and launch of the Asset Protection Agency December 2009 Royal Bank of Scotland: details of Asset Protection Scheme and launch of Asset Protection Agency December 2009 Official versions of this document are printed on 100% recycled paper. When you have finished with it please recycle it again. If using an electronic version of the document, please consider the environment and only print the pages which you need and recycle them when you have finished. © Crown copyright 2009 The text in this document (excluding the Royal Coat of Arms and departmental logos) may be reproduced free of charge in any format or medium providing that it is reproduced accurately and not used in a misleading context. The material must be acknowledged as Crown copyright and the title of the document specified. Where we have identified any third party copyright material you will need to obtain permission from the copyright holders concerned. For any other use of this material please write to Office of Public Sector Information, Information Policy Team, Kew, Richmond, Surrey TW9 4DU or e-mail: [email protected] ISBN 978-1-84532-664-7 PU896 Contents Page Executive summary 3 Chapter 1 Introduction 7 Chapter 2 Financial Stability Agreements finalised 11 Chapter 3 Agreement with Royal Bank of Scotland 15 Chapter 4 Asset Protect Scheme design 21 Chapter 5 Asset Protection Agency 25 Annex A APS Assets 27 Annex B APS design 59 Annex C Asset Protection Agency framework document 85 Royal Bank of Scotland: details of Asset Protection Scheme and launch of the Asset Protection Agency 1 Executive summary The Government is today publishing details of the Asset Protection Scheme (APS) agreements that it has entered into with The Royal Bank of Scotland (RBS) together with information on the assets that are being covered by the APS. -

Inventory List 3

Brothers of the Century Awarded at the 2004 Alpha Gamma Rho Page 1 of 59 National Convention Charles A. Stewart BOC ID#: 10013 University of Illinois 1906 Charles A. Stewart was initiated into Delta Rho Sigma in 1906. He represented the fraternity at the “marriage” between Delta Rho Sigma and Alpha Gamma Rho. Afterward he served as the first Grand President of Alpha Gamma Rho at the first National Convention held on November 30, 1908 at the Hofbrau Hotel in Chicago. Albert B. Sawyer, Jr. BOC ID#: 10039 University of Illinois 1908 Albert B. Sawyer was initiated into Delta Rho Sigma in 1906. He was the moderator at the “marriage” of Alpha Gamma Rho and Delta Rho Sigma. He kept the minutes of the first meetings. According to Brother Sawyer, the minutes were on two paper place mats bearing the name of Hofbrau (Chicago). At the first national convention held November 30, 1908, Brother Sawyer served as the Grand Secretary and Treasurer. Nathan L. Rice BOC ID#: 10186 University of Illinois 1916 Nathan L. Rice is a long time supporter of Alpha Gamma Rho. He grew up on the family farm in Philo, Illinois. In 1915 Nathan became a member of Alpha Gamma Rho at the University of Illinois. In April of 1918 he was enlisted in World War I. He returned to the University of Illinois in September of 1919. After graduation, Brother Rice returned to the farm and in 1924 accepted the position as President of the Philo Exchange Bank. In 1923 Sleeter Bull asked Brother Rice to write the history of Alpha Gamma Rho.