2019 Private Label Industry Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WIC Authorized Vendors

WIC Authorized Vendors Vendor Street Address City Zip Code Phone Location 1 CVS #0085 972 SILVER LN EAST HARTFORD 06108 8605690888 CVS #0942 542 PROVIDENCE BROOKLYN 06234 8607790523 542 PROVIDENCE RD RD BROOKLYN 06234 (41.79872, - 71.903428) DEFLORIO'S VARIETY 115 ELY AVE NORWALK 06854 2038662590 115 ELY AVE NORWALK 06854 (41.092537, - 73.42441) BIG Y WORLD CLASS MARKET 65 PALOMBA DR ENFIELD 06082 8607495514 65 PALOMBA DR #48 ENFIELD 06082 (41.990555, - 72.571489) STOP & SHOP #644 44 LAKE AVE EXT DANBURY 06811 2037978901 44 LAKE AVE EXT #46 #46 DANBURY 06811 (41.38654, - 73.487638) CVS #10367 930 WHITE TRUMBULL 06611 2032612542 930 WHITE PLAINS RD PLAINS RD TRUMBULL 06611 (41.245281, - 73.197198) Page 1 of 224 09/30/2021 WIC Authorized Vendors Planning Counties Zip Code 2 Town Index Regions 5 39 37 19 9 1040 155 103 1 1041 108 49 9 1040 60 34 2 1040 76 144 Page 2 of 224 09/30/2021 WIC Authorized Vendors STOP & SHOP #630 44 FENN RD NEWINGTON 06111 8606678380 44 FENN RD NEWINGTON 06111 (41.698061, - 72.756446) CVS #1080 817 BANK ST NEW LONDON 06320 8604435359 817 BANK ST NEW LONDON 06320 (41.348725, - 72.10706) CARIBBEAN AMERICAN VARIETY 407 CENTER ST MERIDEN 06450 2032351502 407 CENTER ST MERIDEN 06450 (41.54501, - 72.793571) LOS CHICOS ALEGRES 317 E MAIN ST WATERBURY 06702 2037570657 317 E MAIN ST WATERBURY 06702 (41.554536, - 73.03533) CVS #0954 311 MAIN ST TERRYVILLE 06786 8603142890 311 MAIN ST TERRYVILLE 06786 (41.67989, - 73.019399) CVS #0388 613 BOSTON MADISON 06443 2032459438 613 BOSTON POST RD POST RD MADISON 06443 Page 3 of 224 -

Whole Foods Market ™ Case Study: Leadership and Employee Retention Kristin L

Johnson & Wales University ScholarsArchive@JWU MBA Student Scholarship Graduate Studies 5-17-2012 Whole Foods Market ™ Case Study: Leadership and Employee Retention Kristin L. Pearson Johnson & Wales University - Providence, [email protected] Follow this and additional works at: https://scholarsarchive.jwu.edu/mba_student Part of the Business Administration, Management, and Operations Commons, Business and Corporate Communications Commons, Business Law, Public Responsibility, and Ethics Commons, Corporate Finance Commons, Human Resources Management Commons, and the Labor Relations Commons Repository Citation Pearson, Kristin L., "Whole Foods Market ™ Case Study: Leadership and Employee Retention" (2012). MBA Student Scholarship. 8. https://scholarsarchive.jwu.edu/mba_student/8 This Research Paper is brought to you for free and open access by the Graduate Studies at ScholarsArchive@JWU. It has been accepted for inclusion in MBA Student Scholarship by an authorized administrator of ScholarsArchive@JWU. For more information, please contact [email protected]. Running Head: WHOLE FOODS MARKET™: LEADERSHIP AND EMPLOYEE RETENTION Johnson & Wales University Providence, Rhode Island Feinstein Graduate School Presented to Professor Martin W. Sivula Ph.D. Whole Foods Market ™ Case Study: Leadership and Employee Retention A Research Project Submitted in Partial Fulfillment of the Requirements for the MBA Degree Course: RSCH5500 Kristin L. Pearson 05/17/2012 WHOLE FOODS MARKET™: LEADERSHIP AND EMPLOYEE RETENTION TABLE OF CONTENTS Page I. ABSTRACT .................................................................................................2 -

Lidl Expanding to New York with Best Market Purchase

INSIDE TAKING THIS ISSUE STOCK by Jeff Metzger At Capital Markets Day, Ahold Delhaize Reveals Post-Merger Growth Platform Krasdale Celebrates “The merger and integration of Ahold and Delhaize Group have created a 110th At NYC’s Museum strong and efficient platform for growth, while maintaining strong business per- Of Natural History formance and building a culture of success. In an industry that’s undergoing 12 rapid change, fueled by shifting customer behavior and preferences, we will focus on growth by investing in our stores, omnichannel offering and techno- logical capabilities which will enrich the customer experience and increase efficiencies. Ultimately, this will drive growth by making everyday shopping easier, fresher and healthier for our customers.” Those were the words of Ahold Delhaize president and CEO Frans Muller to the investment and business community delivered at the company’s “Leading Wawa’s Mike Sherlock WWW.BEST-MET.COM Together” themed Capital Markets Day held at the Citi Executive Conference Among Those Inducted 20 In SJU ‘Hall Of Honor’ Vol. 74 No. 11 BROKERS ISSUE November 2018 See TAKING STOCK on page 6 Discounter To Convert 27 Stores Next Year Lidl Expanding To New York With Best Market Purchase Lidl, which has struggled since anteed employment opportunities high quality and huge savings for it entered the U.S. 17 months ago, with Lidl following the transition. more shoppers.” is expanding its footprint after an- Team members will be welcomed Fieber, a 10-year Lidl veteran, nouncing it has signed an agree- into positions with Lidl that offer became U.S. CEO in May, replac- ment to acquire 27 Best Market wages and benefits that are equal ing Brendan Proctor who led the AHOLD DELHAIZE HELD ITS CAPITAL MARKETS DAY AT THE CITIBANK Con- stores in New York (26 stores – to or better than what they cur- company’s U.S. -

South Shore Park Comprehensive Plan for Strategic Place Activation Report Prepared As a Collaboration Between A.W

South Shore Park Comprehensive Plan For Strategic Place Activation Report prepared as a collaboration between A.W. Perry, Place Strategists and Vanz Consulting. The material produced herein has been compiled at the exclusive request of A.W. Perry as a framework for the activation of their real estate holdings in Hingham & Rockland. Any conclusions presented reflect the research and opinions of A.W. Perry, Place Strategists and Vanz Consulting. These materials do not necessarily reflect the positions of the Towns of Hingham or Rockland. 15 November 2019 SOUTH SHORE PARK | COMPREHENSIVE PLAN FOR STRATEGIC PLACE ACTIVATION 3 COMPREHENSIVE PLAN FOR STRATEGIC PLACE ACTIVATION (CPSPA) FOR THE SOUTH SHORE PARK A Comprehensive Plan for Strategic Place Activation (CPSPA) for the South Shore Park The following report includes Step 1 | Deep Dive + Discovery, Step 2 | The Scientific (SSP), Hingham and Rockland, MA, is developed to meet the market demand and Research Plan, Steps 3 | Programmatic Plan, and Step 4 | Place Activation Guidelines. opportunities, providing the required spatial environments for a more seamless and Steps 1 and 2 focus on analyzing the existing site conditions, and the initial proposed resilient development phasing. conceptual master plan design. These steps aim to provide the analytical framework for Steps 3 and 4 that focus on proposing a programmatic development scheme for A bottom up approach is adopted to ensure the link between a large-scale the overall master plan and two sets of guidelines to be adopted by specialists along comprehensive framework and the human scale. The focus of the CPSPA is to the development process. -

United Natural Foods (UNFI)

United Natural Foods Annual Report 2019 Form 10-K (NYSE:UNFI) Published: October 1st, 2019 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended August 3, 2019 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______ to _______ Commission File Number: 001-15723 UNITED NATURAL FOODS, INC. (Exact name of registrant as specified in its charter) Delaware 05-0376157 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 313 Iron Horse Way, Providence, RI 02908 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (401) 528-8634 Securities registered pursuant to Section 12(b) of the Act: Name of each exchange on which Title of each class Trading Symbol registered Common Stock, par value $0.01 per share UNFI New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

FTC V. Whole Foods Market (D.C. Cir.)

PUBLIC COPY - SEALED MATERIAL DELETED ORAL ARGUMENT NOT YET SCHEDULED No. 07-5276 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT FEDERAL TRADE COMMISSION, Plaintiff-Appellant, v. WHOLE FOODS MARKET, INC., and WILD OATS MARKETS, INC., Defendants-Appellees. Appeal from the United States District Court for the District of Columbia, Civ. No. 07-cv-Ol021-PLF PROOF BRIEF FOR APPELLANT FEDERAL TRADE COMMISSION JEFFREY SCHMIDT WILLIAM BLUMENTHAL Director General Counsel Bureau of Competition JOHN D. GRAUBERT KENNETH L. GLAZER Principal Deputy General Counsel Deputy Director JOHNF.DALY MICHAEL J. BLOOM Deputy General Counsel for Litigation Director of Litigation MARILYN E. KERST THOMAS J. LANG Attorney THOMAS H. BROCK Federal Trade Commission CATHARINE M. MOSCATELLI 600 Pennsylvania Ave., N.W. MICHAEL A. FRANCHAK Washington, D.C. 20580 JOAN L. HElM Ph. (202) 326-2158 Attorneys Fax (202) 326-2477 CERTIFICATE AS TO PARTIES, RULINGS, AND RELATED CASES Pursuant to Circuit Rule 28(1)(1), Appellant Federal Trade Commission certifies as follows: (A) PARTIES FEDERAL TRADE COMMISSION (Plaintiff) WHOLE FOODS MARKET, INC. (Defendant) WILD OATS MARKETS, INC. (Defendant) APOLLO MANAGEMENT HOLDING LP (Intervenor) DELHAIZE AMERICA. INC. (Interested Party) H.E. BUTT GROCERY COMPANY (Intervenor) KROGER CO. (Intervenor) PUBLIX SUPER MARKETS, INC. (Intervenor) SAFEWAY INC. (Intervenor) SUPERVALU INC (Intervenor) TRADER JOE'S COMPANY (Intervenor) TARGET CORPORATION (Movant) WAL-MART STORES, INC. (Intervenor) WINN-DIXIE STORES INC (Intervenor) WEGMANS FOOD MARKETS, INC. (Movant) AMICI CURIAE AMERICAN ANTITRUST INSTITUTE CONSUMER FEDERATION OF AMERICA ORGANIZATION FOR COMPETITIVE MARKETS (B) RULING UNDER REVIEW Federal Trade Commission v. Whole Foods Market, Inc., 502 F. -

Chilled Prepared Foods

Chilled Prepared Foods DESCRIPTION NET WEIGHT CATERING UKROPS BY LION FOOD HARRIS TEETER KROGER LIBBY MARKET PUBLIX WEGMANS FOOD LION FOOD HARRIS TEETER KROGER LIBBY MARKET PUBLIX WEGMANS DESCRIPTION NET WEIGHT UKROP'S MARKET HALL NET WT 6 LB AUTHENTIC ITALIAN LASAGNA (2.72KG) ••• NET WT 62.4 OZ BAKED SPAGHETTI (3.9LB/1.79KG) ••• BEEF TOP ROUND LONDON NET WT 5 LB BROIL IN SAUCE (2.27kg) •• BLACKENED GRILLED CHICKEN NET WT 4.25 LB BREAST (1.93kg) •••• BLACKENED GRILLED CHICKEN NET WT 4.25 LB BREAST (DICED) (1.93kg) •• NET WT 48 OZ CHICKEN COBBLER (3lb/1.36kg) ••• NET WT 53.3 OZ CHICKEN PARMIGIANA (3.33lb/1.51kg) •• NET WT 4.25 LB HOMESTYLE MEATLOAF (1.93kg) ••• NET WT 5 LB MEATBALLS IN MARINARA SAUCE (2.27kg) ••• NET WT 4 LB PARMESAN CHICKEN TENDERS (1.81kg) • PULLED PORK TOMATO NET WT 5 LB BARBEQUE (2.27kg) ••• BULK NET WT 4 LB ROASTED PULLED CHICKEN (1.6kg) •• SALISBURY STEAK NET WT 48 OZ WITH ONION GRAVY (3lb/1.36kg) ••• SEASONED GRILLED NET WT 4.25 LB CHICKEN BREAST (1.93kg) •••• SEASONED GRILLED NET WT 4.25 LB CHICKEN BREAST (DICED) (1.93kg) •• SOUTHERN STYLE PULLED PORK NET WT 5 LB VINEGAR BARBEQUE (2.27kg) •••• NET WT 5 LB BANANA PUDDING (2.27kg) •• NET WT 6 LB BROCCOLI AND RICE CASSEROLE (2.72kg) •••• BRUSSELS SPROUTS NET WT 5 LB WITH PANCETTA (2.27kg) •• NET WT 5 LB BUTTER BEANS AND CORN (2.27kg) ••• NET WT 5 LB COLLARD GREENS (2.27kg) ••• 1 UKROP'S MARKET HALL DESCRIPTION NET WEIGHT LION FOOD HARRIS TEETER KROGER LIBBY MARKET PUBLIX WEGMANS NET WT 5 LB CORN PUDDING (2.27KG) •••• DUCHESS POTATO CASSEROLE NET WT 5 LB (2.27KG) •••• -

Where Can I Get My Flu and Pneumonia Vaccines? Flu Shots Are the Best Protection Against Influenza for You and Your Loved Ones

Where can I get my flu and pneumonia vaccines? Flu shots are the best protection against influenza for you and your loved ones. They are available for free.* Some pharmacies and provider offices may also offer pneumococcal vaccines for free as well. Please check with your local pharmacy for more information. Some national and regional pharmacies are listed below. When you go to get your shot(s), remember to bring your member ID card with you. Pharmacy Website albertsons.com/pharmacy Albertsons Pharmacy (Jewel-Osco) jewelosco.com/pharmacy Costco costco.com/Pharmacy CVS Pharmacies (CVS Pharmacy, Longs Drug) cvs.com/flu Giant Eagle gianteagle.com/pharmacy Hannaford hannaford.com/flu H-E-B heb.com/pharmacy Hy-Vee hy-vee.com/health/pharmacy Kmart Pharmacy pharmacy.kmart.com/ Kroger kroger.com/topic/pharmacy Meijer Pharmacy meijer.com/pharmacy Publix publix.com/pharmacy Rite Aid Pharmacy riteaid.com/flu Safeway Pharmacy (Safeway, Carrs, Pavilions, Randalls, safeway.com/flushots Tom Thumb, Vons) Sam’s Club samsclub.com Stop & Shop stopandshop.com/sns-rx Walgreens Pharmacy (Walgreens, Duane Reade) walgreens.com/flu Walmart Stores Inc. walmart.com/pharmacy Wegmans wegmans.com/pharmacy For more pharmacies offering flu or pneumococcal pneumonia vaccines in your area, call Customer Service at the number on the back of your member ID card. * Even if you don’t have prescription drug coverage with UnitedHealthcare,® you can get your flu vaccine at these participating pharmacies for no additional cost. This information is not a complete description of benefits. Contact the plan for more information. Limitations, copayments, and restrictions may apply. -

Buy BJ's Wholesale Club

23 July 2018 Retailing / Department Stores & Broadlines BJ's Wholesale Club Deutsche Bank Research Rating Company Date Buy BJ's Wholesale Club 23 July 2018 Initiation of Coverage North America United States Reuters Bloomberg Exchange Ticker Price at 19 Jul 2018 (USD) 25.70 Consumer BJ.N BJ US NYS BJ Price target 30.00 Retailing / Department Stores & Broadlines 52-week range 27.05 - 22.00 BJ’s is Back and Better than Ever Valuation & Risks Mike Baker, CFA Initiating coverage with a Buy rating and $30 price target We are initiating coverage with a Buy rating and $30 target. Positive investment Research Analyst themes include: (1) unique positioning in a favorable industry supports improving +1-617-217-6253 top line; (2) improved processes and platform to drive sales and margin opportunities; (3) growing membership fee income the backbone to future profit Stock & option liquidity data Market Cap (USDm) 3,593.5 gains; and (4) a new club opportunity is also additive to sales. Each of these Shares outstanding (m) 139.8 themes contribute to a compelling long-term financial model, including solid sales Free float (%) 100 from comps, store growth and membership, mid-single-digit profitability gains Volume (19 Jul 2018) 96,880 and mid-double-digit EPS growth. Our price target is based on a target multiple Option volume (und. shrs., 1M avg.) 79,277 that is at a slight premium to peers, with scenario analysis pointing to 2x upside Source: Deutsche Bank versus downside. We see four positive investment themes 1. Unique positioning in a favorable industry supports improving top line: We believe the club industry has among the best fundamentals in retailing and BJ’s is well positioned within the club channel to drive top- line growth. -

Happy Holidays!

AFL-CIO, CLC Pathmark Bankruptcy Update Pages 4 & 5 | Local 1500 raises over $125,000 for Charity Page 6 | Labor Day Parade Page 7 | Shop Steward Seminar Pages 8 & 9 FR Happy OM LOCAL Holidays! 1500 2 The Register December 2015 The Register 3 THE PRESIDENT’S PERSPECTIVE JUST FOR THE RECORD By Bruce W. Both By Anthony G. Speelman, Secretary-Treasurer @Aspeel1500 New York’sLocal Grocery Workers’1500 Union STATE OF THE UNION OUR NEW UNION 2015 presented many challenges to us. The relied on its convenience and size for its popu- On-demand shopping habits through the digital As I mentioned in my September column, For the many workers at Pathmark stores heads about, what’s next? They immediately A&P bankruptcy obviously overshadows them all. larity. It’s been the place where you can find 10 age have molded our society’s workforce into on- 2015 year was an enormous test for our entire that were bought by other employers, you contacted our Union’s Organizing Department. The bankruptcy comes at a time where the tradi- different types of pasta or five different brands of demand workers. union. It feels like years ago that we negotiat- know that wasn’t the case for every transition Just as our department was there for the eight tional grocery store’s future is very much in doubt. peanut butter. Two-income families are prevalent across ed eight new excellent contracts in the early agreement. Some new store owners wouldn’t Mrs. Green’s workers when they were fired ille- Companies are now merging in order to com- You’ll find that peanut butter in the aisle, America, therefore there aren’t as many stay at months of 2015. -

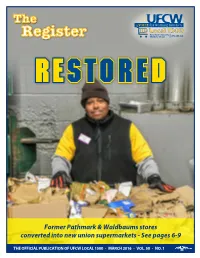

Former Pathmark & Waldbaums Stores Converted Into New Union

AFL-CIO, CLC RESTORED Former Pathmark & Waldbaums stores converted into new union supermarkets - See pages 6-9 THE OFFICIAL PUBLICATION OF UFCW LOCAL 1500 • MARCH 2016 • VOL. 50 • NO. 1 2 The Register March 2016 The Register 3 THE PRESIDENT’S PERSPECTIVE JUST FOR THE RECORD By Bruce W. Both By Anthony G. Speelman, Secretary-Treasurer @Aspeel1500 New York’sLocal Grocery Workers’1500 Union A COURT CASE TO CHANGE THE LABOR MOVEMENT 2016 CHALLENGES Friedrichs v. California Teachers Association aims to rewrite the rules how public unions operate The A&P bankruptcy is over. We saved nearly This is especially important to our union The company also recently announced it would 2,500 jobs and now it’s time to focus on what after the A&P bankruptcy. One year ago, 27% be purchasing the 70,000 square foot former A monumental case, posed to rewrite a 40-year compete is on the forefront of union-members across According to The New York Times, “A ruling in the challenges we face in 2016. of our members worked at Stop & Shop. Today Pathmark in East Meadow. The idea I’m getting precedent guiding public sector labor relations, will America. If unions are defunded, who then, fights for teachers’ favor would affect millions of government In 2014 we negotiated a three-year contract over 40% of our union works under the Stop & at is there’s a growing number of new grocery be ruled on later this summer by the five Republican- working men and women? workers and culminate a political and legal campaign with ShopRite. -

Wegmans-Case-Study-061118.Pdf

Tiffany Smith JUNE 2018 WORK-BASED LEARNING IN ACTION OPPORTUNITY FOR YOUTH MEETS BUSINESS OPPORTUNITY: WEGMANS & HILLSIDE WORK-SCHOLARSHIP CONNECTION Work-Based Learning in Action is a series of case studies highlighting effective models of work-based learning. This case study is part of Walmart’s work with JFF, Making Work-Based Learning Work for Retail, and covers companies that have implemented valuable work-based learning programs that provide lessons for employers creating or redesigning their own retail work-based learning program. Wegmans, a regional supermarket chain, Hillside Family of Agencies, Wegmans is one of the largest private companies has supported the Work-Scholarship in the US, with 47,000 employees. Over a Connection program in its work to quarter of the Wegmans workforce are help young people graduate from high high school- and college-aged students. school and launch their careers. The Wegmans recognizes that the success Hillside Work-Scholarship Connection of these young workers translates into (HW-SC) blends supports for high school company success, and it has translated graduation with work-based learning, this into its training investments. Through in turn creating a talent pipeline for its 30-year engagement as a founding Wegmans. As Meghan Wagner, director leader and now core partner to the of the HW-SC Jobs Institute, describes, 1 the program design builds on the idea PROGRAM ORIGINS that work and career experiences are not always linear, “but there’s a pathway In the mid-1980s, Wegmans, a regional here that we can help young people supermarket chain with over 90 stores understand that every experience ties in the eastern United States, faced a into the next opportunity.” troubling reality: a 100 percent turnover rate among its young part-time workers.