Lille City Story

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

From Lille-Flandres to Lille-Europe —The Evolution of a Railway Station Corinne Tiry

Feature From Lille-Flandres to Lille-Europe From Lille-Flandres to Lille-Europe —The Evolution of a Railway Station Corinne Tiry Since the mid-19th century, European Council, the Northern Railway Company economic arguments finally prevailed and cities evolved around the railway station established in 1845 by the Rothschild a good compromise was adopted—two as a central pivot where goods and people family, the French government and some stations would be built, a terminal inside converge. This is still true today when of Lille's most prominent citizens. These the city walls for passengers traffic, and a railway stations take on a new role as controversies also stimulated nearby urban through terminal outside for goods traffic. urban hubs in the European high-speed projects. Construction of the passenger terminal train network. Lille in northern France, started in 1845, and lasted 3 years. which has two stations from different The Railway Station Enters However, the builders underestimated the railway periods—Lille-Flandres and Lille- the City scale of both passenger and freight traffic Europe, is a good example illustrating this and the capacity was soon saturated. To quasi-continuous past and present urban In the 19th century, the railway station solve this new problem, an Imperial ambitions. became a new gateway to the city, Decree in 1861 allowed the Northern Lille is a city of 170,000 adjacent to the disrupting both the city walls' protective Railway Company to start construction of French-Belgian border. It is at the economic function, as well as the urban layout. The a marshalling yard—called Saint-Sauveur heart of the Lille-Roubaix-Tourcoing- original controversy in Lille emerged from station—south of the main passenger Villeneuve d'Ascq conurbation of 1.2 this duality and a station inside the city station, at the junction of the old city and million people, ranking (excepting Paris) was strongly opposed by the military. -

Why Paris Region Is the #1 Destination on the Planet: with 50 Million Visitors Each Year, the Area Is Synonymous with “Art De Vivre”, Culture, Gastronomy and History

Saint-Denis Basilicum and Maison de la Légion d’Honneur © Plaine Commune, Direction du Développement Economique, SEPE, Som VOSAVANH-DEPLAGNE - Plain of Montesson © CSAGBS-EDesaux - La Défense Business district © 11h45 for Defacto - Campus © Ecole Polytechnique Paris/Saclay. J. Barande - © Ville d’Enghien-les-Bains - INSEAD Fontainebleau © Yann Piriou - Charenton-le-Pont – Ivry-sur-Seine © ParisEstMarne&Bois - Bassin de La Villette, Paris Plages © CRT Ile-de-France - Tripelon-Jarry Welcome to Paris Region Paris Region Facts and Figures 2020 lays out a panorama of the region’s economic dynamism and social life, Europe’s business positioning it among the leading regions in Europe and worldwide. & innovation With its fundamental key indicators, the brochure “Paris Region Facts and powerhouse Figures 2020” is a tool for decision and action for companies and economic stakeholders. It is useful to economic and political leaders of the region and to all those who want to have a global vision of this dynamic regional economy. Paris Region Facts and Figures 2020 is a collaborative publication produced by Choose Paris Region, L’Institut Paris Region and the Paris Île-de-France Regional Chamber of Commerce and Industry. Jardin_des_tuileries_Tour_Eiffel_01_tvb CRT IDF-Van Biesen Table of contents 5 Welcome to Paris Region 27 Digital Infrastructure 6 Overview 28 Real Estate 10 Population 30 Transport and Mobility 12 Economy and Business 32 Logistics 18 Employment 34 Meetings and Exhibitions 20 Education 36 Tourism and Quality of life 24 R&D and Innovation Paris Region Facts & Figures 2020 Welcome to Paris Region 5 A dynamic and A business fast-growing region and innovation powerhouse Paris Region, The Paris Region is a truly global region which accounts for 23.3% The highest GDP in the European of France’s workforce, 31% of Union (EU28) in billions of euros. -

Séance Du Conseil Des Communes De Neuville-En-Ferrain, Tourcoing

Séance du Conseil des communes de Neuville-en-Ferrain, Tourcoing, Roubaix, Hem, Leers, Lys-lez-Lannoy 29 avril 2019 Le 29 avril 2019, à 18h15, le Conseil des Communes, Composé des élus des communes de Neuville-en-Ferrain, Tourcoing, Roubaix, Hem, Leers et Lys-lez- Lannoy, Et en présence de représentants des communes de Wattrelos, Wasquehal, Forest-sur-Marque, Mouvaux, Roncq et Villeneuve d’Ascq, S’est réuni à l’Hôtel de Ville de Roubaix, pour convenir d’une contribution commune en faveur du développement des infrastructures de transports collectifs structurants sur le versant Nord-est du territoire Métropolitain, à horizon 2035. Le vœu a été adopté à la majorité. Détail des votes : 201 votes en faveur du vœu, 5 abstentions. 0 contre. Vœu en faveur d’une contribution des communes de Neuville-en-Ferrain, Tourcoing, Roubaix, Hem, Leers, Lys-lez-Lannoy dans le cadre de l’élaboration du Schéma Directeur des Infrastructures de Transports Vu la délibération n°18 C 0983 prise par la Métropole européenne du Lille du 14 décembre 2018, lançant la concertation du SDIT ; Considérant l’invitation de la MEL à échanger sur l’avenir des infrastructures de transports collectifs structurants sur le territoire métropolitain, et en particulier sur son versant Nord- Est, à échéance 2035 ; Considérant l’urgence climatique et la volonté de nos communes de répondre à la demande de nos populations réclamant, à juste titre, des efforts sans précédent pour contribuer à la transition écologique et à nos changements de comportements en termes de déplacements ; Considérant -

Paris Region Facts & Figures 2021

Paris Region Facts & Figures 2021 Welcome to Paris Region Europe’s Leading Business and Innovation Powerhouse Paris Region Facts and Figures 2021 lays out a panorama of the Region’s economic dynamism and social life, positioning it among the leading regions in Europe and worldwide. Despite the global pandemic, the figures presented in this publication do not yet measure the impact of the health crisis, as the data reflects the reality of the previous months or year.* With its fundamental key indicators, the brochure, “Paris Region Facts and Figures 2021,” is a tool for decision and action for companies and economic stakeholders. It is useful to economic and political leaders of the Region and to all who wish to have a global vision of this dynamic regional economy. Paris Region Facts and Figures 2021 is a collaborative publication produced by Choose Paris Region, L’Institut Paris Region, and the Paris Île-de-France Regional Chamber of Commerce and Industry. *L’Institut Paris Region has produced a specific note on the effects of the pandemic on the Paris Region economy: How Covid-19 is forcing us to transform the economic model for The Paris Region, February 2021 Cover: © Yann Rabanier / Choose Paris Region 2nd cover: © Pierre-Yves Brunaud / L’Institut Paris Region © Yann Rabanier / Choose Paris Region Table of contents Welcome to Paris Region 5 Overview 6 Population 10 Economy and Business 12 Employment 18 Education 20 R&D and Innovation 24 Digital Infrastructure 27 Real Estate 28 Transport and Mobility 30 Logistics 32 Meetings and Exhibitions 34 Tourism and Quality of life 36 Welcome to Paris Region A Dynamic and A Thriving Business Paris Region, Fast-growing Region and Research Community A cultural and intellectual The highest GDP in the EU28 in A Vibrant, Innovative metropolis, a scientific and billions of euros. -

Hem Croix Roubaix Wattrelos Leers Toufflers Lys-Lez

r. Le Duc vers Tourcoing rue L4 vers Halluin L8 Patriotes Parc Jules CH Dron Gounod vers Tourcoing r. G. Philippot du Lion 2 Fauré 35 Risquons Tout rue Roubaix r. de Union L8 de St Liévin Mercure Le Hutin Wattrelos Centre bd de Metz CIT5 r. de Tourcoing CIT5 17 30 Guinguette Rollin Canal L4 r. Briffaut De Gaulle Foch Bd de r. d’Oran Vallon Metz 10 R. de Herriot CIT5 La Roselière rue du Blanc Seau Tourcoing La Vigne r. de la Baillerie Alsace Fosse aux Z6 Wattrelos Place Wattrelos Chênes Quartier Beaulieu Centre Commercial MWR La Paix L3 35 E. Moreau Pellart République Carnot Collège St Rémi ROUBAIX Carnot Z6 TER L3 WATTRELOS Gare Jean Place Avelghem Hommelet rue Lebas Roubaix 33 Chaptal Nations Galon Roubaix d'Eau Mouvaux Unies r. de Grand Place L8 Liane L4 Condition 35 Publique Un nouvel itinéraire de Leers Centre Eurotéléport Commercial35 à Roubaix Fosse aux Chênes, 2 R P. de Carnot Tourcoing et Halluin Roubaix 10 L3 L4 L8 C12 Roubaix rue Roubaix Charles 33 34 35 36 L4 34 Dunant de Gaulle 226 MWR 33 av. de rue de l’Épeule Ste Élisabeth de Epeule A.Mongy Verdun Leers LEERS Montesquieu St Jean Guesde Roubaix r. Kléber Trois C. Commercial rue du Mal. Leclerc Manufacture Vélodrome Wattrelos vers Lomme r. DammartinR. de Montgolfier Ponts L4 66 St Philibert Denain Coq Français Fraternité Van Der r. de Lannoy Verdun Meersch 2 J. Moulin Danièle Bd. de CIT5 Mulhouse Beaumont Lesaffre Coubertin Manufacture Mairie L8 Dupuy Fraternité Avenue des Sports Lys Liane 33 Hôpital de Lôme Pont Rouge 66 de Croix av. -

European Conference of Ministers Responsible for Regional Planning I Nt Er Go Ve R M E N Tal Commissions for Co-Operation in Frontier Regions

EUROPEAN CONFERENCE OF MINISTERS RESPONSIBLE FOR REGIONAL PLANNING I NT ER GO VE R M E N TAL COMMISSIONS FOR CO-OPERATION IN FRONTIER REGIONS A SURVEY Council of Europe Strasbourg 1973 This document is published as a background paper on Theme No. IV FRONTIER REGIONS of the Second European Conference of Ministers responsible for Regional Planning. It constitutes an inventory of commissions, both existing or envisaged, for co-operation in frontier regions. The information was supplied by national Delegations to the Committee of Senior Officials preparing the Second Ministerial Conference. The following reports are published in the same series : TRANS-FRONT1ER CO-OPERATION IN EUROPE - CONFERENCE REPORT PRESENTED BY THE BELGIAN DELEGATION / “CEMAT (73) 4_7 EUROPEAN CO-OPERATION IN FRONTIER REGIONS - STUDY BY JEAN-MARIE QUINTIN / “CEMAT (73) BP 9J FRONTIER REGIONS IN EUROPE - AN ANALYTICAL STUDY BY R. STRASSOLDO / “CEMAT (73) BP 10_7 THE CO-OPERATION OF EUROPEAN FRONTIER REGIONS - A STUDY OF THE EUROPEAN SYMPOSIUM ON FRONTIER REGIONS BY V. von MALCHUS /ÄS/Coll/Front. (72) CONSULTATIVE ASSEMBLY REPORT ON THE EUROPEAN SYMPOSIUM ON FRONTIER REGIONS. RAPPORTEUR KARL AHRENS / “Doc 3228J. 30.942 CEMAT (73) BP 11 09.4 Table of contents Page INTRODUCTION 3 BILA.TERAL COMMISSIONS AND AGREEMENTS AT INTERGOVERNMENTAL LEVEL 7 2.1 AUSTRIA - ITALY 7 2.1.1 The "Accordino" 7 2.1.2 Italo-Austrian Sub-Commissions on regional problems and the Port of Trieste .7 2.2 AUSTRIA - SWITZERLAND 7 2.3 BELGIUM - FRANCE 8 2.3.1 Franco-Belgian Plenary Commission for Regional Planning in Frontier Regions 8 2.4 BELGIUM - FEDERAL'REPUBLIC OF GERMANY • ■ ; . -

De Lille À Tournai – 28,3 Km

De Lille à Tournai – 28,3 km Cet itinéraire peut être suivi aussi bien par les marcheurs que les cyclistes. Dénivelé positif cumulé : 60m Dénivelé négatif cumulé : 48m Altitude maxi : 77m Départ de la Grand-Place de Lille. Face à la l'immeuble de la Voix du Nord, prendre à gauche la rue des Manneliers. Tourner à droite et prendre la rue Faidherbe jusqu'à la gare de Lille Flandres Prendre à gauche, passer devant le centre commercial « Euralille » et continuer par l'avenue Le Corbusier Au bout du pont, passer au dessus du périphérique et continuer en face la rue du faubourg de Roubaix. Passer devant l'église St Maurice des champs et continuer tout droit. Passer au dessus de la voie rapide allant de Roubaix à Lille. Au rond-point, prendre la fourche vers la droite (Avenue des Acacias – Mons en Baroeul). Continuer tout droit. La rue devient l'Avenue Robert Schuman. Passer devant les tours de l'Europe (à droite) et la mairie de Mons en Baroeul (à gauche). 04/2016 De Lille à Tournai 1 / 7 Tourner à droite Avenue René Coty. A l'extrémité, prendre à gauche la rue Jules Guesde. Vous êtes désormais à Villeneuve d'Ascq, quartier de Flers-bourg. Longer le supermarché Cora, traverser le boulevard de l'Ouest et poursuivre en face la rue Jules Guesde. Environ 250 mètres plus loin, prendre à droite la rue du général Leclerc sur environ 200 mères. Tourner à gauche, place de la Liberté. Puis contourner l'église St Pierre à droite par la rue Jeanne d'Arc. -

Portrait De Territoire Nord Franche

Nord Franche-Comté - Canton du Jura Un territoire contrasté entre une partie française urbaine à forte densité et un côté suisse moins peuplé vec 330 000 habitants, le territoire « Nord Franche-Comté - Canton du Jura » est le plus peuplé des quatre territoires de coopération. Il comprend les agglomérations françaises de Belfort et de Montbéliard. En Suisse, deux pôles d’emploi importants, ceux de Delémont et de Porrentruy, attirent des actifs résidant dans les petites communes françaises situées le long de la frontière. L’industrie est bien implantée dans ce territoire, structurée autour de grands établissements relevant en grande partie de la fabrication de matériel de transport côté Afrançais, davantage diversifiée côté suisse. Démographie : une évolution contrastée Ce territoire se caractérise par de part et d’autre de la frontière des collaborations régulières et multiscalaires qui associent principalement le Canton du Jura, Le territoire « Nord Franche-Comté - Canton (14 100) et une vingtaine de communes de le Département du Territoire de Belfort, du Jura » est un territoire de 330 000 habitants plus de 2000 habitants. la Communauté de l’Agglomération situé dans la partie la moins montagneuse de Le contraste est fort avec la partie suisse, si- Belfortaine (CAB) et la Préfecture du l’Arc jurassien. De fait, il est densément peu- tuée dans le canton du Jura, qui compte 105 Territoire de Belfort. plé, avec 226 habitants au km² alors que la habitants au km² et comprend moins d’une di- De nombreuses réalisations sont à relever, moyenne de l’Arc jurassien se situe à 133 ha- zaine de communes dépassant les 2000 habi- notamment dans le domaine culturel bitants au km². -

Independence and Trade: the Speci C E Ects of French Colonialism

Independence and trade: the specic eects of French colonialism Emmanuelle Lavallée¤ Julie Lochardy June 2012z Very preliminary. Please do note cite. Abstract Empirical evidence suggests that colonial rule and subsequent indepen- dence inuence past and current trade of former colonies. Independence ef- fects could dier substantially across former empires if they are related to the end of dierent preferential trade arrangements. Thanks to an original dataset including new data on pre-independence bilateral trade, this paper explores the impact of independence on former colonies' trade (imports and exports) for dierent empires on the period 1948-2007. We show that independence reduces trade (imports and exports) with the former metropole and that this eect is mainly driven by former French colonies. We also nd that, after independence, trade of all former colonies increase with third countries. A close inspection of the eects over time highlights that independence eects are gradual but tend to be more rapid and more intense in the case of exports. These results oer indirect evidence for the long-lasting inuence of colonial trade policies. Author Keywords: Trade; Decolonization; French Empire. JEL classication codes: F10; F54. ¤Université Paris-Dauphine, LEDa, UMR DIAL. Email: [email protected]. yErudite, University of Paris-Est Créteil. Email: [email protected]. zWe would like to thank participants at the IRD-DIAL Seminar and participants at the Con- ference on International Economics (CIE) 2012 for useful comments and suggestions. 1 1 Introduction Several studies highlight the consequences of colonial rule on bilateral trade. Mitchener and Wei- denmier (2008) assess the contemporaneous eects of empire on trade over the period 1870-1913. -

Press Kit Lille 2016

www.lilletourism.com PRESS KIT LILLE 2016 ALL YOU NEED IS LILLE Press Release Just 80 minutes away from London, 1 hour from Paris and 35 minutes from Brussels, Lille could quite easily have melted into the shadows of its illustrious neighbours, but instead it is more than happy to cultivate and show off all that makes it stand out from the crowd! Flemish, Burgundian and then Spanish before it became French, Lille boasts a spectacular heritage. A trading town since the Middle Ages, a stronghold under Louis XIV, a hive of industry in the 19th century and an ambitious hub in the 20th century, Lille is now imbued with the memories of the past, interweaved with its visions for the future. While the Euralille area is a focal point of bold architecture by Rem Koolhaas, Jean Nouvel or Christian de Portzamparc, the Lille-Sud area is becoming a Mecca for fashionistas. Since 2007, some young fashion designers (sponsored by Agnès b.) have set up workshops and boutiques in this new “fashion district” in the making. With lille3000, it’s the whole city that has started to look towards the future, enjoying a dramatic makeover for this new recurrent event, geared towards contemporary art and innovation. The European Capital of Culture in 2004, Lille is now a leading light in this field, with the arts ma- king themselves quite at home here. From great museums to new alternative art centres, from the Opera to the theatres through the National Or- chestra, culture is a living and breathing part of everyday life here. -

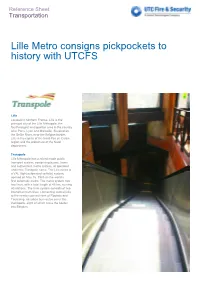

Lille Metro Reference-Sheet.Pdf

Reference Sheet Transportation Lille Metro consigns pickpockets to history with UTCFS Lille Located in northern France, Lille is the principal city of the Lille Métropole, the fourth-largest metropolitan area in the country after Paris, Lyon and Marseille. Situated on the Deûle River, near the Belgian border, Lille is the capital of the Nord-Pas de Calais region and the préfecture of the Nord department. Transpole Lille Métropole has a mixed mode public transport system, comprising buses, trams and a driverless metro system, all operated under the Transpole name. The Lille metro is a VAL (light automated vehicle) system, opened on May 16, 1983 as the world’s first automatic metro. The metro system has two lines, with a total length of 45 km, serving 60 stations. The tram system consists of two interurban tram lines, connecting central Lille to the nearby communities of Roubaix and Tourcoing. 68 urban bus routes cover the metropolis, eight of which cross the border into Belgium. Pre-existing situation & UTCFS's role UTCFS's solution Across the entire Lille metro network there are UTCFS offered Transpole a complete video over 1,200 security cameras installed. surveillance solution. Data from the existing Transpole sought to modernise its 1,200 cameras that monitor stations and lines surveillance system to increase passenger is directly transmitted through 80 VisioWave security. It decided to upgrade the system to Evolution encoder/decoder devices. Analogue enable a complete digital grid overview of all data from cameras is converted into digital 60 stations. All camera data would need to be streams, enabling efficient transmission over storable and available for possible an IP network. -

Eléments Clés Pdu Adopté En Avril 2011 Au Sommaire

Eléments clés pdu adopté en avril 2011 au sommaire Vers une nouvelle mobilité 04 2000 > 2010 > 2020 : évolution et adaptation 06 Le Plan de déplacements urbains 2010 > 2020 09 L’état des lieux 09 L’évaluation environnementale et l’annexe accessibilité 12 Les objectifs et les actions 13 Edition : Service communication Lille Métropole Conception graphique : Resonance.coop - Roubaix Rédaction : Service communication Lille Métropole - Bernard Fautrez, Resonance.coop Photos : Direction de la communication LMCU Impression : Imprimerie la Centrale Lens Réalisé sur un papier PEFC par un imprimeur labélisé imprim’vert Mai 2011 PEFC/10-31-1495 Certifi é PEFC - Provient de forêts gérées durablement. www.pefc-france.org Inventer une 2 édito Martine AUBRY, Présidente Lille Métropole Adopté en avril 2011 par le Conseil de Communauté, le Plan de déplacements urbains concré- tise notre engagement en faveur d’une métropole durable et solidaire où les villes, villages et quartiers combinent de façon harmonieuse habitat, développement économique et transports. Nous devons répondre aux aspirations de chacun, celles de se déplacer facilement et confor- tablement dans un espace public de qualité ; nous devons aussi favoriser le développement et le rayonnement de notre territoire et prendre toute notre part dans la lutte contre le réchauf- fement climatique. Préparé sous la responsabilité d’Eric Quiquet, 1er vice-président chargé des transports et de Daniel Janssens, vice-président chargé du dossier, le Plan de déplacements urbains de Lille Métropole répond à ces objectifs et entend ainsi inventer une mobilité durable pour demain. Nous l’avons construit dans une large concertation avec les territoires, les institutions et les habitants.