The Outlook for Office & Institutional Employment to 2041

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tall Buildings: up up and Away?

expect the best Tall Buildings: Up Up and Away? by Marc Kemerer Originally published in Blaneys on Building (April 2011) There has been much debate about tall buildings (buildings over 12 storeys in height) in Toronto in the past number of years particularly due to the decreasing availability of development land, and the province and municipal forces on intensification – but how tall is too tall and where should tall buildings be permitted? Marc Kemerer is a municipal As we have reported previously, the City of Toronto continues to review proposals for tall towers partner at Blaney McMurtry , against its Tall Buildings Guidelines which set out standards for podiums, setbacks between sister with significant experience in towers and the like. Some of those Guidelines were incorporated into the City’s new comprehensive all aspects of municipal planning and development. zoning by-law (under appeal and subject to possible repeal by City Council - see the Planning Updates section of this issue) while the Guidelines themselves were renewed last year by City Marc may be reached directly Council for continued use in design review. at 416.593.2975 or [email protected]. Over the last couple of years the City has embarked on the “second phase” of its tall buildings review through the “Tall Buildings Downtown Project”. In connection with this phase, the City has recently released the study commissioned by the City on this topic entitled: “Tall Buildings: Inviting Change in Downtown Toronto” (the “Study”). The Study focused on three issues: where should tall buildings be located; how high should tall buildings be; and how should tall buildings behave in their context. -

Entuitive Credentials

CREDENTIALS SIMPLIFYING THE COMPLEX Entuitive | Credentials FIRM PROFILE TABLE OF CONTENTS Firm Profile i) The Practice 1 ii) Approach 3 iii) Better Design Through Technology 6 Services i) Structural Engineering 8 ii) Building Envelope 10 iii) Building Restoration 12 iv) Special Projects and Renovations 14 Sectors 16 i) Leadership Team 18 ii) Commercial 19 iii) Cultural 26 iv) Institutional 33 SERVICES v) Healthcare 40 vi) Residential 46 vii) Sports and Recreation 53 viii) Retail 59 ix) Hospitality 65 x) Mission Critical Facilities/Data Centres 70 xi) Transportation 76 SECTORS Image: The Bow*, Calgary, Canada FIRM PROFILE: THE PRACTICE ENTUITIVE IS A CONSULTING ENGINEERING PRACTICE WITH A VISION OF BRINGING TOGETHER ENGINEERING AND INTUITION TO ENHANCE BUILDING PERFORMANCE. We created Entuitive with an entrepreneurial spirit, a blank canvas and a new approach. Our mission was to build a consulting engineering firm that revolves around our clients’ needs. What do our clients need most? Innovative ideas. So we created a practice environment with a single overriding goal – realizing your vision through innovative performance solutions. 1 Firm Profile | Entuitive Image: Ripley’s Aquarium of Canada, Toronto, Canada BACKED BY DECADES OF EXPERIENCE AS CONSULTING ENGINEERS, WE’VE ACCOMPLISHED A GREAT DEAL TAKING DESIGN PERFORMANCE TO NEW HEIGHTS. FIRM PROFILE COMPANY FACTS The practice encompasses structural, building envelope, restoration, and special projects and renovations consulting, serving clients NUMBER OF YEARS IN BUSINESS throughout North America and internationally. 4 years. Backed by decades of experience as Consulting Engineers. We’re pushing the envelope on behalf of – and in collaboration with OFFICE LOCATIONS – our clients. They are architects, developers, building owners and CALGARY managers, and construction professionals. -

Schedule 4 Description of Views

SCHEDULE 4 DESCRIPTION OF VIEWS This schedule describes the views identified on maps 7a and 7b of the Official Plan. Views described are subject to the policies set out in section 3.1.1. Described views marked with [H] are views of heritage properties and are specifically subject to the view protection policies of section 3.1.5 of the Official Plan. A. PROMINENT AND HERITAGE BUILDINGS, STRUCTURES & LANDSCAPES A1. Queens Park Legislature [H] This view has been described in a comprehensive study and is the subject of a site and area specific policy of the Official Plan. It is not described in this schedule. A2. Old City Hall [H] The view of Old City hall includes the main entrance, tower and cenotaph as viewed from the southwest and southeast corners at Temperance Street and includes the silhouette of the roofline and clock tower. This view will also be the subject of a comprehensive study. A3. Toronto City Hall [H] The view of City Hall includes the east and west towers, the council chamber and podium of City Hall and the silhouette of those features as viewed from the north side of Queen Street West along the edge of the eastern half of Nathan Phillips Square. This view will be the subject of a comprehensive study. A4. Knox College Spire [H] The view of the Knox College Spire, as it extends above the roofline of the third floor, can be viewed from the north along Spadina Avenue at the southeast corner of Bloor Street West and at Sussex Avenue. A5. -

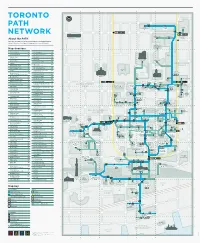

PATH Network

A B C D E F G Ryerson TORONTO University 1 1 PATH Toronto Atrium 10 Dundas Coach Terminal on Bay East DUNDAS ST W St Patrick DUNDAS ST W NETWORK Dundas Ted Rogers School One Dundas Art Gallery of Ontario of Management West Yonge-Dundas About the PATH Square 2 2 Welcome to the PATH — Toronto’s Downtown Underground Pedestrian Walkway UNIVERSITY AVE linking 30 kilometres of underground shopping, services and entertainment ST PATRICK ST BEVERLEY ST BEVERLEY ST M M c c CAUL ST CAUL ST Toronto Marriott Downtown Eaton VICTORIA ST Centre YONGE ST BAY ST Map directory BAY ST A 11 Adelaide West F6 One King West G7 130 Adelaide West D5 One Queen Street East G4 Eaton Tower Adelaide Place C5 One York D11 150 York St P PwC Tower D10 3 Toronto 3 Atrium on Bay F1 City Hall 483 Bay Street Q 2 Queen Street East G4 B 222 Bay E7 R RBC Centre B8 DOWNTOWN Bay Adelaide Centre F5 155 Wellington St W YONGE Bay Wellington Tower F8 RBC WaterPark Place E11 Osgoode UNIVERSITY AVE 483 Bay Richmond-Adelaide Centre D5 UNIVERSITY AVE Hall F3 BAY ST 120 Adelaide St W BAY ST CF Toronto Bremner Tower / C10 Nathan Eaton Centre Southcore Financial Centre (SFC) 85 Richmond West E5 Phillips Canada Life Square Brookfield Place F8 111 Richmond West D5 Building 4 Old City Hall 4 2 Queen Street East C Cadillac Fairview Tower F4 Roy Thomson Hall B7 Cadillac Fairview Royal Bank Building F6 Tower CBC Broadcast Centre A8 QUEEN ST W Osgoode QUEEN ST W Thomson Queen Building Simpson Tower CF Toronto Eaton Centre F4 Royal Bank Plaza North Tower E8 QUEEN STREET One Queen 200 Bay St Four -

Area 83 Eastern Ontario International Area Committee Minutes June 2

ALCOHOLICS ANONYMOUS AREA 83 EASTERN ONTARIO INTERNATIONAL Area 83 Eastern Ontario International Area Committee Minutes June 2, 2018 ACM – June 2, 2018 1 ALCOHOLICS ANONYMOUS AREA 83 EASTERN ONTARIO INTERNATIONAL 1. OPENING…………………………………………………………………………….…………….…4 2. REVIEW AND ACCEPTANCE OF AGENDA………………………………….…………….…...7 3. ROLL CALL………………………………………………………………………….……………….7 4. REVIEW AND ACCEPTANCE OF MINUTES OF September 9, 2017 ACM…………………7 5. DISTRICT COMMITTEE MEMBERS’ REPORTS ……………………………………………....8 District 02 Malton……………………………………………………………………………….…….. 8 District 06 Mississauga……………………………………………………………………….…….. 8 District 10 Toronto South Central…………………………………………………………….….…. 8 District 12 Toronto South West………………………………………………………………….…. 9 District 14 Toronto North Central………………………………………………………………..….. 9 District 16 Distrito Hispano de Toronto…………………………………………………….………..9 District 18 Toronto City East……………………………………………………………………........9 District 22 Scarborough……………………………………………………………………………… 9 District 26 Lakeshore West………………………………………………………………….……….10 District 28 Lakeshore East……………………………………………………………………………11 District 30 Quinte West…………………………………………………………………………….. 11 District 34 Quinte East……………………………………………………………………………… 12 District 36 Kingston & the Islands……………………………………………………………….… 12 District 42 St. Lawrence International………………………………………………………………. 12 District 48 Seaway Valley North……………………………………………………………….……. 13 District 50 Cornwall…………………………………………………………………………………… 13 District 54 Ottawa Rideau……………………………………………………………………………. 13 District 58 Ottawa Bytown…………………………………………………………………………… -

Integrating Transportation and Land Use Planning at the Metropolitan Level in North America 185

Integrating transportation and land use planning at the metropolitan level in North America: multilevel governance in Toronto and Chicago Integrando o planejamento de transporte e de uso do solo em escala metropolitana na América do Norte: governança multinível em Toronto e Chicago Fanny R. Tremblay-Racicot[a], Jean Mercier[b] Licenciado sob uma Licença Creative Commons DOI: 10.7213/urbe.06.002.SE04 ISSN 2175-3369 [a] Ph.D candidate in Urban Studies at Department of Geography and Urban Studies, Temple University, Philadelphia, PA - United States, e-mail: [email protected] [b] Ph.D in public administration (SU), professor at Université Laval, Québec, QC - Canada, e-mail: [email protected] Abstract This article compares the policies and processes by which transportation and land use planning are integra- ted in metropolitan Toronto, Canada, and Chicago, in the United States. Using twenty-four semi-structured interviews with key informants, it describes the array of interventions undertaken by governmental and non-governmental actors in their respective domains to shed light on how the challenge of integrating trans- portation and land use planning is addressed on both sides of the border. Evidence concerning the political dynamics in Toronto and Chicago demonstrates that the capacity of metropolitan institutions to adopt and implement plans that integrate transportation with land use fundamentally depends on the leadership of the province or the state government. Although the federal government of each nation can bypass the sub-national level and intervene in local affairs by funding transportation projects that include land use components, its capacity to promote a coherent metropolitan vision is inherently limited. -

Toronto Police Service Community Consultation and Volunteer Manual

1 November 2019 2 Volunteers and Community Policing The Toronto Police Service (Service) recognizes that volunteers are an integral and vital component of community policing. Service volunteers are welcomed and valued in every community, and their service to the organization is invaluable. Our volunteers serve as the first point of contact between the community and the Service. They make an impact and strengthen ties in our communities, they serve to enhance the delivery of police services, and assist in numerous community engagement initiatives and programs. The Mission Statement of the Toronto Police Service Volunteer Program is; “To create meaningful partnerships through trust, understanding, shared knowledge, effective community engagement and to maintain safety and security in our communities.” Connected by Commitment Revised November 2020 2 3 MESSAGE FROM THE TORONTO POLICE SERVICES BOARD On behalf of the Toronto Police Services Board, I would like to extend our deep and sincere appreciation to all of our volunteers for giving your time, energy, and dedication to the Toronto Police Service and to all of the communities that make up the City of Toronto. The Toronto Police Service is recognized as outstanding model in the policing community in the way in which it consults with its communities. The Board is extremely proud of this achievement and is committed to continuously working to ensure that we remain a progressive leader in this vital area. Strong and meaningful partnership with the community is an essential component of the Board’s emphasis on community policing. Indeed, The Way Forward, the Transformational Task Force’s action plan report, charts an approach to policing that is founded on embracing partnerships to create safe communities. -

MINISTRY of CORRECTIONS Facilities AREA 83

MINISTRY OF CORRECTIONS Facilities AREA 83 Name of Facility Address Contact Numbers Area / District Brockville Jail 613-341-2870 10 Wall St. Fax: 613-342-0962 Area 83 Brockville, ON K6V 4R9 District 66 Golden Triangle Ontario 905-457-7050 109 McLaughlin Rd. S. Correctional Institute Fax: 905-452-8606 Area 83 Brampton, ON L6Y 2C8 District 02 Malton St. Lawrence Valley 613-341-2870 Area 83 PO Box 8000 1804 Hwy 2 Correctional & Fax: 613-345-3844 E. Treatment Centre District 66 Golden Triangle Brockville, ON K6V 7N2 Central East 705-328-6000 Area 83 Correctional Centre 541 Hwy 36 Fax: 705-328-6001 Lindsay, ON K9V 6H2 District 86 Kawartha Quinte 613-354-9701 89 Richmond Blvd. Area 83 Detention Centre Fax: 613-354-1209 Napanee, ON K7R 3S1 District 34 Quinte East Ottawa-Carleton Detention 613-824-6080 Area 83 Centre 2244 Innes Road Fax: 613-824-0732 Ottawa, ON K1B 4C4 District 54 Ottawa Rideau Toronto South Detention Center 160 Horner Ave. Area 83 Etobicoke, Ont District 6/18 Toronto Intermittent Centre 160 Horner Ave. (TIC) Etobicoke, Ont Toronto East 416-750-3513 Area 83 55 Civic Rd. Detention Centre Fax: 416-750-3345 Toronto (Scarborough), District 22 Scarborough ON M1L 2K9 1 of 1 FEDERAL CORRECTIONAL FACILITIES AREA 83 ONTARIO REGION Institutions Regional Treatment Centre (Max) Millhaven Institution (Max) 560 King Street West Highway 33 PO Box 22 PO Box 280 Kingston, Ontario K7L 4V7 Bath, Ontario K0H 1G0 (613) 536-6901 (613) 351-8000 Fax: (613) 536-4115 Fax: (613) 351-8136 A/Executive Director: Kathy Hinch Warden: Curtis Jackson District -

Rapid Transit in Toronto Levyrapidtransit.Ca TABLE of CONTENTS

The Neptis Foundation has collaborated with Edward J. Levy to publish this history of rapid transit proposals for the City of Toronto. Given Neptis’s focus on regional issues, we have supported Levy’s work because it demon- strates clearly that regional rapid transit cannot function eff ectively without a well-designed network at the core of the region. Toronto does not yet have such a network, as you will discover through the maps and historical photographs in this interactive web-book. We hope the material will contribute to ongoing debates on the need to create such a network. This web-book would not been produced without the vital eff orts of Philippa Campsie and Brent Gilliard, who have worked with Mr. Levy over two years to organize, edit, and present the volumes of text and illustrations. 1 Rapid Transit in Toronto levyrapidtransit.ca TABLE OF CONTENTS 6 INTRODUCTION 7 About this Book 9 Edward J. Levy 11 A Note from the Neptis Foundation 13 Author’s Note 16 Author’s Guiding Principle: The Need for a Network 18 Executive Summary 24 PART ONE: EARLY PLANNING FOR RAPID TRANSIT 1909 – 1945 CHAPTER 1: THE BEGINNING OF RAPID TRANSIT PLANNING IN TORONTO 25 1.0 Summary 26 1.1 The Story Begins 29 1.2 The First Subway Proposal 32 1.3 The Jacobs & Davies Report: Prescient but Premature 34 1.4 Putting the Proposal in Context CHAPTER 2: “The Rapid Transit System of the Future” and a Look Ahead, 1911 – 1913 36 2.0 Summary 37 2.1 The Evolving Vision, 1911 40 2.2 The Arnold Report: The Subway Alternative, 1912 44 2.3 Crossing the Valley CHAPTER 3: R.C. -

2 Way All Day GO Train Survey 2018

2 Way All Day GO Train Survey 2018 Winter 2018-2019 KEY When explained the concept of a two-way, all day GO Train was explained, TAKEAWAYS an overwhelming majority of Ontarians (80%) support this initiative. Those who support the idea cite And, when presented with a list of reasons for the new service, reduced traffic and traffic congestion reducing traffic congestion and GHGs by taking cars off the highways as the main reason for their support, were slightly more compelling reasons than those tied to while those who oppose the idea say infrastructure, strengthening the technology corridor or attracting they would not be affected by the train talent (although these are also seen to be good reasons). or worry about the cost to taxpayers. Half (51%) say they will use the two-way all day GO train; 13% would use it at least once a week. This number is the same for those live along the corridor but rises to 20% for commuters. The percentage who would “definitely” Moreover, of those who For this reason, it is not surprising or “probably” use the train for work or would use the service most that four in five (81%) believe it is school jumps to 52% among frequently (i.e. once a week important to have a connection to commuters but only stands at 37% for or more) the principal uses Toronto Pearson. residents who live along the line. are for work or school or to go to Toronto Pearson. KEY The People support 2WADGO TAKEAWAYS While support is highest among Torontonians, those who live along the line and commuters, voters in South/West Ontario (77%) and even North/East Ontario (70%) overwhelmingly support 2WADGO. -

Redeveloping the Distillery District, Toronto

Place Differentiation: Redeveloping the Distillery District, Toronto by Vanessa Kirsty Mathews A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Department of Geography University of Toronto © Copyright by Vanessa Kirsty Mathews 2010 Place Differentiation: Redeveloping the Distillery District, Toronto Doctor of Philosophy Vanessa Kirsty Mathews, 2010 Department of Geography University of Toronto Abstract What role does place differentiation play in contemporary urban redevelopment processes, and how is it constructed, practiced, and governed? Under heightened forms of interurban competition fueled by processes of globalization, there is a desire by place- makers to construct and market a unique sense of place. While there is consensus that place promotion plays a role in reconstructing landscapes, how place differentiation operates – and can be operationalized – in processes of urban redevelopment is under- theorized in the literature. In this thesis, I produce a typology of four strategies of differentiation – negation, coherence, residue, multiplicity – which reside within capital transformations and which require activation by a set of social actors. I situate these ideas via an examination of the redevelopment of the Gooderham and Worts distillery, renamed the Distillery District, which opened to the public in 2003. Under the direction of the private sector, the site was transformed from a space of alcohol production to a space of cultural consumption. The developers used a two pronged approach for the site‟s redevelopment: historic preservation and arts-led regeneration. Using a mixed method approach including textual analysis, in-depth interviews, visual analysis, and site observation, I examine the strategies used to market the Distillery as a distinct place, and the effects of this marketing strategy on the valuation of art, history, and space. -

Section Ii Geographical List / Liste Géographique 1

SECTION II GEOGRAPHICAL LIST / LISTE GÉOGRAPHIQUE 1 Routing Numbers / Numéros d'acheminement Electronic Paper(MICR) Électronique Papier(MICR) Postal Address - Addresse postale 100 MILE HOUSE, BC 000108270 08270-001 BANK OF MONTREAL Cariboo Mall, P.O. Box 10, 100 Mile House, BC V0K 2E0 001000550 00550-010 CANADIAN IMPERIAL BANK OF COMMERCE 100 Mile House Banking Centre, 1-325 Birch Ave, Box 98, 100 Mile House, BC V0K 2E0 000304120 04120-003 ROYAL BANK OF CANADA 100 Mile House Branch, 200 Birch Ave-PO Box 700, 200 Birch Ave, 100 Mile House, BC V0K 2E0 ABBEY, SK 000300118 00778-003 ROYAL BANK OF CANADA Abbey Branch, Wayne & Cathedral, c/o 120 Centre St, Abbey, SK S0N 0A0 (Sub to 00778) ABBOTSFORD, BC 000107090 07090-001 BANK OF MONTREAL Abbotsford Main, 101-32988 South Fraser Way, Abbotsford, BC V2S 2A8 000107490 07490-001 Highstreet Branch, 3122 Mt.Leham Rd, Abbotsford, BC V2T 0C5 000120660 20660-001 Lower Sumas Mountain, 1920 North Parallell Road, Abbotsford, BC V3G 2C6 000200240 00240-002 THE BANK OF NOVA SCOTIA Abbotsford, #100-2777 Gladwin Road, Abbotsford, BC V2T 4V1 (Sub to 11460) 000211460 11460-002 Clearbrook, PO Box 2151, Clearbrook Station, Abbotsford, BC V2T 3X8 000280960 80960-002 Ellwood Centre, #1-31205 Maclure Road, Abbotsford, BC V2T 5E5 (Sub to 11460) 000251680 51680-002 Glenn Mountain Village, Unit 106 2618 McMillan Road, Abbotsford, BC V3G 1C4 001000420 00420-010 CANADIAN IMPERIAL BANK OF COMMERCE Abbotsford, 2420 McCallum Rd, Abbotsford, BC V2S 6R9 (Sub to 08820) 001001720 01720-010 McCallum Centre, Box 188, Abbotsford,