Grocery Outlet Bargain Market II

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

United Natural Foods (UNFI)

United Natural Foods Annual Report 2019 Form 10-K (NYSE:UNFI) Published: October 1st, 2019 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended August 3, 2019 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______ to _______ Commission File Number: 001-15723 UNITED NATURAL FOODS, INC. (Exact name of registrant as specified in its charter) Delaware 05-0376157 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 313 Iron Horse Way, Providence, RI 02908 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (401) 528-8634 Securities registered pursuant to Section 12(b) of the Act: Name of each exchange on which Title of each class Trading Symbol registered Common Stock, par value $0.01 per share UNFI New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Market Analysis for Grocery Retail Space in Forest Grove, Oregon

MARKET ANALYSIS FOR GROCERY RETAIL SPACE IN FOREST GROVE, OREGON PREPARED FOR THE CITY OF FOREST GROVE, FEBRUARY 2018 TABLE OF CONTENTS I. INTRODUCTION ............................................................................................................................................. 2 II. EXECUTIVE SUMMARY .................................................................................................................................. 2 III. TRADE AREA DEFINITION .............................................................................................................................. 4 IV. GROCERY MARKET OVERVIEW ...................................................................................................................... 5 THE PORTLAND METRO MARKET .............................................................................................................................. 5 METRO LOCATION PATTERNS ................................................................................................................................... 8 FOREST GROVE-CORNELIUS ................................................................................................................................... 15 V. SOCIO-ECONOMIC CONDITIONS .................................................................................................................. 19 POPULATION & HOUSEHOLDS ................................................................................................................................ 19 EMPLOYMENT & COMMUTING .............................................................................................................................. -

Buy BJ's Wholesale Club

23 July 2018 Retailing / Department Stores & Broadlines BJ's Wholesale Club Deutsche Bank Research Rating Company Date Buy BJ's Wholesale Club 23 July 2018 Initiation of Coverage North America United States Reuters Bloomberg Exchange Ticker Price at 19 Jul 2018 (USD) 25.70 Consumer BJ.N BJ US NYS BJ Price target 30.00 Retailing / Department Stores & Broadlines 52-week range 27.05 - 22.00 BJ’s is Back and Better than Ever Valuation & Risks Mike Baker, CFA Initiating coverage with a Buy rating and $30 price target We are initiating coverage with a Buy rating and $30 target. Positive investment Research Analyst themes include: (1) unique positioning in a favorable industry supports improving +1-617-217-6253 top line; (2) improved processes and platform to drive sales and margin opportunities; (3) growing membership fee income the backbone to future profit Stock & option liquidity data Market Cap (USDm) 3,593.5 gains; and (4) a new club opportunity is also additive to sales. Each of these Shares outstanding (m) 139.8 themes contribute to a compelling long-term financial model, including solid sales Free float (%) 100 from comps, store growth and membership, mid-single-digit profitability gains Volume (19 Jul 2018) 96,880 and mid-double-digit EPS growth. Our price target is based on a target multiple Option volume (und. shrs., 1M avg.) 79,277 that is at a slight premium to peers, with scenario analysis pointing to 2x upside Source: Deutsche Bank versus downside. We see four positive investment themes 1. Unique positioning in a favorable industry supports improving top line: We believe the club industry has among the best fundamentals in retailing and BJ’s is well positioned within the club channel to drive top- line growth. -

Alabama Vendor List.Xlsx

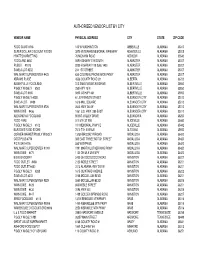

AUTHORIZED VENDOR LIST BY CITY VENDOR NAME PHYSICAL ADDRESS CITY STATE ZIP CODE FOOD GIANT #716 100 W WASHINGTON ABBEVILLE ALABAMA 36310 SUPER DOLLAR DISCOUNT FOODS 3970 VETERANS MEMORIAL PARKWAY ADAMSVILLE ALABAMA 35005 HYATT'S MARKET INC 70 MCHANN ROAD ADDISON ALABAMA 35540 FOODLAND #450 509 HIGHWAY 119 SOUTH ALABASTER ALABAMA 35007 PUBLIX #1073 9200 HIGHWAY 119 Suite 1400 ALABASTER ALABAMA 35007 SAVE-A-LOT #202 244 1ST STREET ALABASTER ALABAMA 35007 WAL MART SUPERCENTER #423 630 COLONIAL PROMENADE PKWY ALABASTER ALABAMA 35007 ABRAMS PLACE 4556 COUNTY ROAD 29 ALBERTA ALABAMA 36720 ALBERTVILLE FOODLAND 313 SAND MOUNTAIN DRIVE ALBERTVILLE ALABAMA 35950 PIGGLY WIGGLY #500 250 HWY 75 N ALBERTVILLE ALABAMA 35950 SAVE-A-LOT #165 5850 US HWY 431 ALBERTVILLE ALABAMA 35950 PIGGLY WIGGLY #238 61 JEFFERSON STREET ALEXANDER CITY ALABAMA 35010 SAVE-A-LOT #489 1616 MILL SQUARE ALEXANDER CITY ALABAMA 35010 WAL MART SUPERCENTER #726 2643 HWY 280 W ALEXANDER CITY ALABAMA 35010 WINN DIXIE #456 1061 U.S. HWY. 280 EAST ALEXANDER CITY ALABAMA 35010 ALEXANDRIA FOODLAND 85 BIG VALLEY DRIVE ALEXANDRIA ALABAMA 36250 FOOD FARE 517 5TH ST NW ALICEVILLE ALABAMA 35442 PIGGLY WIGGLY #102 101 MEMORIAL PKWY E ALICEVILLE ALABAMA 35442 BURTON'S FOOD STORE 7010 7TH AVENUE ALTOONA ALABAMA 35952 CORNER MARKET/PIGGLY WIGGLY 13759 BROOKLYN ROAD ANDALUSIA ALABAMA 36420 COST PLUS #774 305 EAST THREE NOTCH STREET ANDALUSIA ALABAMA 36420 PIC N SAV #776 550 W BYPASS ANDALUSIA ALABAMA 36420 WAL MART SUPERCENTER #1091 1991 MARTIN LUTHER KING PKWY ANDALUSIA ALABAMA 36420 WINN DIXIE -

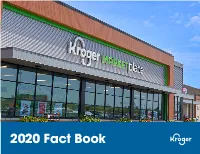

2020 Fact Book Kroger at a Glance KROGER FACT BOOK 2020 2 Pick up and Delivery Available to 97% of Custom- Ers

2020 Fact Book Kroger At A Glance KROGER FACT BOOK 2020 2 Pick up and Delivery available to 97% of Custom- ers PICK UP AND DELIVERY 2,255 AVAILABLE TO PHARMACIES $132.5B AND ALMOST TOTAL 2020 SALES 271 MILLION 98% PRESCRIPTIONS FILLED HOUSEHOLDS 31 OF NEARLY WE COVER 45 500,000 640 ASSOCIATES MILLION DISTRIBUTION COMPANY-WIDE CENTERS MEALS 34 DONATED THROUGH 100 FEEDING AMERICA FOOD FOOD BANK PARTNERS PRODUCTION PLANTS ARE 35 STATES ACHIEVED 2,223 ZERO WASTE & THE DISTRICT PICK UP 81% 1,596 LOCATIONS WASTE OF COLUMBIA SUPERMARKET DIVERSION FUEL CENTERS FROM LANDFILLS COMPANY WIDE 90 MILLION POUNDS OF FOOD 2,742 RESCUED SUPERMARKETS & 2.3 MULTI-DEPARTMENT STORES BILLION kWh ONE OF AMERICA’S 9MCUSTOMERS $213M AVOIDED SINCE MOST RESPONSIBLE TO END HUNGER 2000 DAILY IN OUR COMMUNITIES COMPANIES OF 2021 AS RECOGNIZED BY NEWSWEEK KROGER FACT BOOK 2020 Table of Contents About 1 Overview 2 Letter to Shareholders 4 Restock Kroger and Our Priorities 10 Redefine Customer Expereince 11 Partner for Customer Value 26 Develop Talent 34 Live Our Purpose 39 Create Shareholder Value 42 Appendix 51 KROGER FACT BOOK 2020 ABOUT THE KROGER FACT BOOK This Fact Book provides certain financial and adjusted free cash flow goals may be affected changes in inflation or deflation in product and operating information about The Kroger Co. by: COVID-19 pandemic related factors, risks operating costs; stock repurchases; Kroger’s (Kroger®) and its consolidated subsidiaries. It is and challenges, including among others, the ability to retain pharmacy sales from third party intended to provide general information about length of time that the pandemic continues, payors; consolidation in the healthcare industry, Kroger and therefore does not include the new variants of the virus, the effect of the including pharmacy benefit managers; Kroger’s Company’s consolidated financial statements easing of restrictions, lack of access to vaccines ability to negotiate modifications to multi- and notes. -

Retail Scene Report

GFSI CONFERENCE 2020 – DISCOVERY TOURS 25th February | Seattle, USA Retail Scene Report Seattle, Washington State & America’s Pacific Northwest 19 The Consumer Goods Forum GFSI CONFERENCE 2020 – DISCOVERY TOURS 25th February | Seattle, USA Retail Scene Report Seattle, Washington State & America’s Pacific Northwest FEBRUARY 2020 Kantar Consulting for The Consumer Goods Forum’s GFSI Conference 2020 20 The Consumer Goods Forum GFSI CONFERENCE 2020 – DISCOVERY TOURS 25th February | Seattle, USA Contents Seattle, Washington State & America’s Pacific Northwest .............. 22 Food Retail in the Pacific Northwest ........................................................ 24 Supercenters & Warehouse Clubs ........................................................ 27 Supermarkets & Convenience Stores .................................................. 29 Full-Service Supermarkets .................................................................. 29 Value/Private-Label Supermarkets ................................................ 32 Convenience Stores ................................................................................ 34 Food Safety in America & Washington State ......................................... 35 The US Federal Government & Agencies ........................................... 35 Washington State Food Safety ................................................................ 36 City, Town, & Local Food Safety ............................................................ 37 Conclusions ........................................................................................................ -

Oregon Redemption Centers Albany Beaverton

Oregon Redemption Centers and Associated Retailers (5,000 or more sq ft in size) ZONE 1 ZONE 2 EXEMPT** DEALER REDEMPTION CENTERS*** FULL SERVICE PARTICIPATING RETAILERS PARTICIPATING RETAILERS (accept 144 containers) (accept 24 containers) REDEMPTION CENTERS (accept 0 containers) (accept 24 containers) 0 - 2.0 miles radius Albany from redemption center No Zone 2 Zone 1 No Zone 2141 Santiam Hwy SE Albany Grocery Outlet Albany East Liquor Store 1103 ALOHA 1950 14th Ave SE 2530 Pacific Blvd SE Albertsons #3557 approved 6/18/2015 Big Lots #4660 Dollar Tree #1508 6055 SW 185th 2000 14th Ave SE, Ste 102 1307 Waverly Dr SE Bi-Mart #606 Lowe's #3057 BEAVERTON 2272 Santiam Hwy 1300 9th Ave SE Fred Meyer #482 Costco #0682 15995 SW Walker Rd 3130 Killdeer Ave SE Fred Meyer #005 CANBY 2500 Santiam Blvd Fred Meyer #651 North Albany Market 1401 SE 1st Ave 621 NE Hickory Rite Aid #5365 Safeway #2604 1235 Waverly Dr SE 1051 SW 1st Ave Safeway #1659 1990 14th Ave SE CLACKAMAS Target #T609 Fred Meyer #063 2255 14th Ave SE 16301 SE 82nd Dr Walgreens #6530 1700 Pacific Blvd SE DALLAS Walmart #5396 Safeway #4404 1330 Goldfish Farm SE 138 W Ellendale Ave Wheeler Dealer 1740 SE Geary St EUGENE Winco Foods Fred Meyer #325 (Santa Clara) 3100 Pacific Blvd SE 60 Division St 0 - 2.0 miles radius 2.01 - 2.8 miles radius Beaverton from redemption center from redemption center Either Zone FLORENCE 9307 SW Beaverton-Hillsdale Hwy Albertsons #505 99 Ranch Cost Plus World Market #6060 Fred Meyer #464 5415 SW Beaverton Hillsdale Hwy 8155 SW Hall Blvd 10108 SW Washington -

TENANT CREDIT RATINGS - 1St Quarter 2017

TENANT CREDIT RATINGS - 1st Quarter 2017 - PROVIDED TO YOU BY: TENANT CREDIT RATINGS MOODY’S AND STANDARD & POOR’S Hanley Investment Group is a boutique real estate brokerage and advisory services company that specializes in the sale of commercial retail properties nationwide. Our expertise, proven track record and unwavering dedication to put client needs first continues to set us apart in the industry. Hanley Investment Group creates value by delivering exceptional results through the use of property-specific marketing strategies, cutting-edge technology and local market knowledge. Our nationwide relationships with investors, developers, institutions, franchisees, brokers and 1031 exchange buyers are unparalleled in the industry, translating into maximum exposure and pricing for each property marketed and sold. With unmatched service, Hanley Investment Group has redefined the experience of selling retail investment properties. RETAIL TENANT LIST WITH TICKER SYMBOLS & CREDIT RATINGS - 1st Quarter 2017 - CREDIT TENANCY MOODY’S STANDARD & POOR’S Highest Quality Aaa AAA High Quality Aa AA Upper Medium Grade A A Medium Grade Baa BBB Lower Medium Grade * Ba BB Lower Grade * B B Poor Quality * Caa CCC Speculative * Ca CC No Interest Being Paid or BK Petition Filed * C C Note: The ratings from Aa to Ca by Moody’s may be modified by the addition of a 1, 2 or 3 to show the relative standing within the category. 1=High 3=Low * Below Investment Grade • Hanley Investment Group • 3500 East Coast Highway, Suite 100, Corona del Mar, CA 92625 • P: 949.585.7610 • www.HanleyInvestment.com • TENANT CREDIT RATINGS MOODY’S AND STANDARD & POOR’S TENANT TICKER MOODY'S S&P SUBSIDIARIES, AFFILIATES, AND BRAND NAMES AUTOMOTIVE Advance Auto Parts, Western Auto Supply, Discount Auto Parts, Advance Auto Parts, Inc. -

Covid19 Apr09 Info from Ala G

Company Work Phone Mailing Address City ST Zip County Curbside Home Delivery Third Party Service Food Giant #716 334-585-2789 100 W. Washington Street Abbeville AL 36310 Henry Publix Super Markets #1073 205-663-3443 9200 Hwy. 119, Ste. 1400 Alabaster AL 35007-5327 Shelby No Yes Instacart, Shipt Target 250 S Colonial Drive Alabaster AL Shelby Yes Yes Shipt 35007 Walmart Neighborhood Market 4756 9085 Highway 119 Alabaster AL 35007 Shelby Yes No Walmart Supercenter 0423 205-620-0360 630 Colonial Promenade Pkwy Alabaster AL 35007 Shelby Yes Yes DoorDash, PointPickup, Postmates, Roadie and Spark Albertville Foodland 256-891-0390 313 Sand Mountain Drive Albertville AL 35950 Marshall No No JMBL, Inc. 256-891-5410 P.O. Drawer 370 Albertville AL 35950-0006 Marshall No No Piggly Wiggly #500 256-878-2075 250 AL HWY 75 N Albertville AL 35951 Marshall Save-A-Lot #23562 256-891-1339 5850 US HWY 431 Albertville AL 35950-2049 Marshall Piggly Wiggly #238 256-234-3454 61 Jefferson Street Alexander City AL 35010 Tallapoosa Save-A-Lot #489 56) 215-4197 1612 Mill Square Street Alexander City AL 35010 Tallapoosa Walmart Supercenter 0726 205-324-0316 2643 Hwy 280 West Alexander City AL 35010-3675 Tallapoosa Yes No Winn-Dixie #456 256-234-5141 1061 US HWY 280 E Alexander City AL 35010-4622 Tallapoosa Alexandria Foodland 256-847-8466 P.O. Box 548 Alexandria AL 36250 Calhoun No No Food Outlet Jr. #465 334-820-4218 6346 Highway 431 Alexandria AL 36250-5005 Calhoun No No Food Fare 205-373-8734 517 5th St. -

Alturas Planning Commission Regular Meeting City Hall Council Chambers March 14, 2018 5:30 P.M

Alturas Planning Commission Regular Meeting City Hall Council Chambers March 14, 2018 5:30 p.m. The meeting was called to order by Chairman Bill Hall at 5:30 p.m. Commissioners present: Tom Romero, Marlene Hamilton, Chris Lauppe. Commissioners absent: Robert Dolan. Staff present: Planner Jennifer Andersen Planning Director Joe Picotte, City Council Planning Dept. Liaison Mark Steffek, Secretary Bobbi Jean Melbourn, City Treasurer Sara Peet, Administrative Asst. Macey Binning. Public attending: 32 No one is present under the public forum. MOTION by Commissioner Romero, SECONDED by Commissioner Hamilton to approve the minutes of the December 13, 2017 meeting. ALL AYES. Commissioner Hall reviewed the guidelines of a Public Hearing and introduces Planner Jennifer Andersen to the public. PUBLIC HEARING ITEM A: Opened at 5:43 p.m. Clement Balser of Blackpoint Group, Inc. is requesting a Use Permit (UP2018-01) to develop a portion of vacant APN 001-090-014 into a retail shopping center anchored by a Grocery Outlet store. Planner Jennifer Andersen explains the location of the proposed project is north of the Department of Motor Vehicles with direct access from Highway 299 (W. 12th Street) and secondary access off of N. West 'C' Street. The Center is proposed as a phased development with Phase 1 to include a 16,000 SF Grocery Outlet and all the improvements illustrated in the Site Plan except the paving and landscaping surrounding the drive- through restaurant area and the curb and sidewalk improvements immediately surrounding the second retail pad. The proposed Use Permit is currently conditioned for any tenant. -

How Wages and Working Conditions for California's

HOW WAGES AND WORKING CONDITIONS FOR CALIFORNIA’S FOOD RETAIL WORKERS HAVE DECLINED AS THE INDUSTRY HAS THRIVED By Saru Jayaraman and the Food Labor Research Center, University of California, Berkeley Primary Research Support Provided by the Food Chain Workers Alliance and Professor Chris Benner, University of California, Davis June 2014 Commissioned by United Food and Commercial Workers, Western States Council EXECUTIVE SUMMARY – Shelved: How Wages and Working Conditions for California’s Food Retail Workers Have Declined as the Industry has Thrived Shelved: How Wages and Working Conditions for California’s Food Retail Workers Have Declined as the Industry has Thrived is based on worker surveys, in-depth interviews with workers and employers, analysis of industry and government data, and reviews of existing aca- demic literature. It represents the most comprehensive analysis ever conducted of California’s food retail industry. The report shows that while California’s food retail industry has enjoyed consistent growth over the past two decades, the expansion of a low-price, low-cost business model – and the choices that traditional, unionized grocers have made in the face of it – have produced a dramatic wage decline, with high rates of poverty and hunger among workers in a sector that once enjoyed relatively high wages and unionization rates. The report calls for a two- pronged strategy to arrest and reverse these trends: support for unionization, and public policies that support livable wages and benefits. This strategy would promote the creation of good jobs in the food retail sector and help build long-term prosperity for California’s families and communities. -

Private Label: Brand Positioning in the New World Order

Private Label: Brand Positioning in the New World Order SEPTEMBER 2011 03 Executive Summary 05 Introduction 06 Private Label Share Trends 11 Price Discount by Department 12 Category Level Concentration 13 Private Label Purchase Segments 14 Category Opportunity 19 Conclusions 21 Success Story: Attribute Drivers™ 22 Resources 1 Private Label: Brand Positioning in the New World Order A New Look at Private Label Shhhh! Grab the box with the funny logo and put it at the bottom of the basket so no one will know we’re buying a private label cereal. Our friends will think one of us lost our jobs. It wasn’t long ago that many shoppers felt this way about private label. Today, private label is in just about every U.S. household. For a while, many manufacturers and retailers viewed private label as a juggernaut that couldn’t be stopped, but the truth is much more subtle. In recent months and years, many retailers have innovated very successfully to create private label offerings with different pricing strategies to attract shoppers of varying income levels, invested in developing products for categories heretofore dominated by national brands, and introduced private label products for hundreds of staple products to ensure a private label offering for many basic needs. Yet, savvy manufacturers haven’t sat on their hands. They have developed new products with added ingredients and/or features to create new levels of differentiation, become more aggressive with pricing, and generated new merchandising and promotion strategies. Both manufacturers and retailers know private label products are not a panacea, but they have been delivering solid quality at substantial savings—important always, but particularly critical for many consumers in a down economy.