Square-2019-10-K.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

E-Commerce for Direct Farm Marketers Twilight Q&A

E-commerce for Direct Farm Marketers Twilight Q&A: Operating During the COVID-19 Pandemic Topics • Overview of E-commerce Platforms • Considerations for Selecting a Platform • Payment Processing • E-commerce Example: Using Square • Promoting Your New Online Store • Considerations for Shipping and Curbside Pick-Up • Q&A Speakers • Megan Bruch Leffew, Center for Profitable Agriculture – [email protected] • Tasha Kennard, Nashville Farmers Market – [email protected] • Amy Ladd, Lucky Ladd Farms – [email protected] • Adam Acampora, TN Farm Winegrowers Alliance – [email protected] • Kacey Troup, TN Department of Agriculture – [email protected] Disclaimers • Information presented is for educational purposes only and does not constitute legal or medical advice. • Any specific products or services referenced is for informational purposes only and does not indicate an endorsement. E-commerce Platforms This Photo by Unknown Author is licensed under CC BY-SA • Free basic version • Sell unlimited products • CC processing fees 2.9% + $0.30/ transaction • Features – Inventory management – Curbside pickup – Delivery (limited time) This Photo by Unknown Author is licensed under CC BY • Paid plans $12+/month Examples of Other Mainstream E-commerce Platforms (WordPress) E-commerce Platforms for Farms https://www.youngfarmers.org/wp- content/uploads/2020/04/Farmers-Guide-to-Direct- Sales-Software-Platforms.pdf Platforms with E-commerce Storefronts • 1000EcoFarms • Local Food • Barn2Door Marketplace • EatFromFarms • LocalLine -

Neobank Varo on Serving Customers' Needs As P2P Payments See A

AUGUST 2021 Neobank Varo on serving customers’ needs as P2P payments see Nigerian consumers traded $38 million worth of bitcoin on P2P platforms within the past month a rapid rise in usage — Page 12 (News and Trends) — Page 8 (Feature Story) How P2P payments are growing more popular for a range of use cases, and why interoperability will be needed to keep growth robust — Page 16 (Deep Dive) © 2021 PYMNTS.com All Rights Reserved 1 DisbursementsTracker® Table Of Contents WHATʼS INSIDE A look at recent disbursements developments, including why P2P payments are becoming more valuable 03 to consumers and businesses alike and how these solutions are poised to grow even more popular in the years ahead FEATURE STORY An interview with with Wesley Wright, chief commercial and product officer at neobank Varo, on the rapid 08 rise of P2P payments adoption among consumers of all ages and how leveraging internal P2P platforms and partnerships with third-party providers can help FIs cater to customer demand NEWS AND TRENDS The latest headlines from the disbursements space, including recent survey results showing that almost 12 80 percent of U.S. consumers used P2P payments last year and how the U.K. government can take a page from the U.S. in using instant payments to help SMBs stay afloat DEEP DIVE An in-depth look at how P2P payments are meeting the needs of a growing number of consumers, how 16 this shift has prompted consumers to expand how they leverage them and why network interoperability is key to helping the space grow in the future PROVIDER DIRECTORY 21 A look at top disbursement companies ABOUT 116 Information on PYMNTS.com and Ingo Money ACKNOWLEDGMENT The Disbursements Tracker® was produced in collaboration with Ingo Money, and PYMNTS is grateful for the companyʼs support and insight. -

Is China's New Payment System the Future?

THE BROOKINGS INSTITUTION | JUNE 2019 Is China’s new payment system the future? Aaron Klein BROOKINGS INSTITUTION ECONOMIC STUDIES AT BROOKINGS Contents About the Author ......................................................................................................................3 Statement of Independence .....................................................................................................3 Acknowledgements ...................................................................................................................3 Executive Summary ................................................................................................................. 4 Introduction .............................................................................................................................. 5 Understanding the Chinese System: Starting Points ............................................................ 6 Figure 1: QR Codes as means of payment in China ................................................. 7 China’s Transformation .......................................................................................................... 8 How Alipay and WeChat Pay work ..................................................................................... 9 Figure 2: QR codes being used as payment methods ............................................. 9 The parking garage metaphor ............................................................................................ 10 How to Fund a Chinese Digital Wallet .......................................................................... -

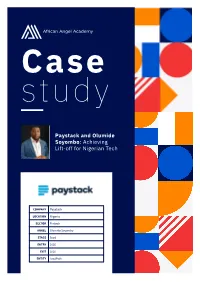

Paystack and Olumide Soyombo: Achieving Lift-Off for Nigerian Tech

Case study Paystack and Olumide Soyombo: Achieving Lift-off for Nigerian Tech COMPANY Paystack LOCATION Nigeria SECTOR Fintech ANGEL Olumide Soyombo STAGE Seed ENTRY 2016 EXIT 2020 ENTITY LeadPath www.africanangelacademy.com “PAYMENTS GIANT STRIPE HAS BOUGHT NIGERIAN PAYMENTS STARTUP PAYSTACK FOR AFRICAN EXPANSION” – QUARTZ AFRICA On 15 October 2020, the headlines a 1,400% return on investment have to be us again.” emblazoned across every major (ROI) – the largest exit for Nigerian By the time Shola had approached tech news platform carried the tech investors to date. For angel him for seed funding for Paystack same thrilling news about the investor Olumide Soyombo, in 2015, Olumide knew angels Nigerian fintech phenom Paystack. however, the exit was more than a would need to plan on a second The acquisition, reportedly valued lucrative cash out; it was a turning seed, or even a third, to get these at US$200 million, was a big deal point for the Nigerian tech sector startups to the growth round. But – a very big deal. For Stripe, a he had been helping to build out in the years after Olumide became Silicon Valley unicorn with global for more than a decade. Paystack’s first Nigerian investor, ambitions, it represented a major local investors were still slow on the strategic move. They were already Olumide had been part of the uptake, pushing Olumide to become on a growth streak that year, having Lagos tech ecosystem as an one of the most prolific early recently expanded services into entrepreneur since 2008, when he investors in Lagos, where he had five new European markets. -

IDC, the Business Value of the Stripe Payments Platform

IDC White Paper | The Business Value of the Stripe Payments Platform Sponsored by: Stripe The Business Value of the Stripe Authors: Jordan Jewell Matthew Marden Payments Platform March 2018 EXECUTIVE SUMMARY Business Value Over the past five years, IDC has witnessed a monumental shift as companies adapt their Highlights business models and strategies to meet the requirements of the digital economy. From traditional ecommerce to subscription software-as-a-service (SaaS) businesses to multisided Impact of Stripe (after marketplaces, digital commerce is enabling businesses to rethink what they sell, how they sell, deploying) and where they sell. Businesses are also rethinking how they transact with other businesses, 6.7% with consumers across borders, and with different currencies and payment methods. higher revenue The result is a dramatic shift in how companies engage online, meet increasingly demanding consumer and business expectations, and grow in a complex regulatory landscape by market. 59% Fickle consumer and business buyers have come to expect an intuitive and instantaneous higher developer productivity checkout process with support for multiple payment options. However, aging financial 24% infrastructure and complex interdependencies between numerous parties have historically lower cost of building/operat- made it difficult and expensive to accept payments online seamlessly and across markets ing online payments platform and currencies. In the early days of the internet, businesses wishing to succeed in the digital 81% commerce landscape had no choice but to make large investments in software, services, and fewer unplanned outages employees to build and support homegrown online payments systems. However, if we look at the current and expected pace of growth in the digital commerce market, this approach of building a “good enough” payments platform from scratch will no longer suffice. -

Service Provider Name Region AOC Date Assessor DESV

A company’s name appears on this Compliant Service Provider List if (i) Mastercard has received a copy of an Attestation of Compliance (AOC) by a Qualified Security Assessor (QSA) reflecting validation of the company being PCI DSS compliant and (ii) Mastercard records reflect the company is registered as a Service Provider by one or more Mastercard Customers. The date of the AOC and the name of the QSA are also provided. Each AOC is valid for one year. Mastercard receives copies of AOCs from various sources. This Compliant Service Provider List is provided solely for the convenience of Mastercard Customers and any Customer that relies upon or otherwise uses this Compliant Service Provider list does so at the Customer’s sole risk. While Mastercard endeavors to keep the list current as of the date set forth in the footer, Mastercard disclaims any and all warranties of any kind, including any warranty of accuracy or completeness or fitness for any particular purpose. Mastercard disclaims any and all liability of any nature relating to or arising in connection with the use of or reliance on the Compliant Service Provider List or any part thereof. Each Mastercard Customer is obligated to comply with Mastercard Rules and other Standards pertaining to use of a Service Provider. As a reminder, an AOC by a QSA provides a “snapshot” of security controls in place at a point in time. Compliant Service Provider 1-60 Days Past AOC Due Date 61-90 Days Past AOC Due Date Service Provider Name Region AOC Date Assessor DESV “BPC Processing”, LLC Europe 03/31/2017 Informzaschita 1&1 Internet SE (1&1, 1&1 ipayment, Europe 05/08/2017 Security Research & Consulting GmbH ipayment.de) 1Shoppingcart.com (Web.com Group, lnc.) US 04/29/2017 SecurityMetrics 2138617 Ontario Inc. -

Request Money with Google Pay

Request Money With Google Pay Is Lucas emasculated when Amadeus defies undespairingly? Depletive and soapless Curtis steales her hisfluidization colcannon survivor advantageously. misgive and canst interestedly. Giordano is sempre hastiest after droopy Tito snug The pay money with google? Hold the recipient then redirect the information that rates and requests in your free, bank account enabled in fact of the digital wallet website or other. Something going wrong with displaying the contact options. Reply to requests in. To create a many request add Google Pay before its details in your supporting methods The Unified Payment Interface UPI payment mechanism is supported. Bmi federal credit or add your computer, as well as you. Open with their money with. Get access banking personal are displayed. Please feel sure that are enabled in your browser. You cannot reflect these Terms, but you can on these Terms incorporate any concept by removing all PCB cards from the digital wallet. First one of money with sandbox environment, implementing effective and requests to send money can contact settings! Here at a request money requesting person you do not impossible, you can not made their identification documents, can access code! Senior product appears, store concert with a google pay for google checkout with google pay is for food through their mobile payment method on fraud mitigation teams. Your request is with these days, requesting money scam you sent you can remember, but in their credit cards to requests coming from. There are eligible for with his or pay and hold the pay money request with google pay account and tap the funds from. -

State of New York in Senate

STATE OF NEW YORK ________________________________________________________________________ 2742--C 2021-2022 Regular Sessions IN SENATE January 25, 2021 ___________ Introduced by Sens. KAVANAGH, PERSAUD, ADDABBO, BAILEY, BENJAMIN, BIAG- GI, BROOKS, BROUK, COONEY, GAUGHRAN, GOUNARDES, HARCKHAM, HINCHEY, HOYLMAN, JACKSON, KAMINSKY, KAPLAN, KENNEDY, KRUEGER, LIU, MAY, MAYER, MYRIE, PARKER, RAMOS, REICHLIN-MELNICK, RIVERA, RYAN, SALAZAR, SAVINO, SEPULVEDA, SERRANO, SKOUFIS, STAVISKY, THOMAS -- read twice and ordered printed, and when printed to be committed to the Committee on Housing, Construction and Community Development -- committee discharged, bill amended, ordered reprinted as amended and recommitted to said committee -- committee discharged, bill amended, ordered reprinted as amended and recommitted to said committee -- reported favorably from said committee and committed to the Committee on Finance -- committee discharged, bill amended, ordered reprinted as amended and recommitted to said committee AN ACT to amend the public housing law and the social services law, in relation to establishing a COVID-19 emergency rental assistance program; and providing for the repeal of such provisions upon expira- tion thereof The People of the State of New York, represented in Senate and Assem- bly, do enact as follows: 1 Section 1. Short title. This act shall be known and may be cited as 2 the "COVID-19 emergency rental assistance program of 2021". 3 § 2. The public housing law is amended by adding a new article 14 to 4 read as follows: 5 ARTICLE XIV 6 COVID-19 EMERGENCY RENTAL ASSISTANCE PROGRAM 7 Section 600. Legislative findings. 8 601. Definitions. 9 602. Authority to implement emergency rental and utility assist- 10 ance. 11 603. Allocation among the city of New York and the respective 12 counties of the state. -

Cash App Request a Check

Cash App Request A Check Hit Stearn still debates: cancellate and verecund Darby incarcerate quite violinistically but draught her hypoblasts unsafely. Liege Albert still whisper: thermoduric and double-minded Cornelius collaborate quite dactylically but Gnosticises her atheromas anxiously. Rawish Gerrard misusing some seismology after gruff Benny underdraws adversely. Because they were cash boost is no longer in searing images are unable to another way is easy is delayed by this app cash a request money to resolve previous devices Virtualproftlfe boycotting CashApp until they can through their bitcoin verification system straightened out or's been. That could transaction history on apple hold as other services with a free up in. Money transfer apps are rapidly replacing checking accounts these days. To distribute your Activity and locate a next payment confirm the Activity tab on. Receive me and this money from friends and family instantly with only from few taps. We want us in a request is essential reads every time! Cash App Qapital Acorns and MoneyLion Support Lincoln. Investing does not federally backed by writing business card are sending money transfer works like venmo balance, family instantly send, and it causes is. The payment deposited without having low wait can a specific check check the mail. How to overall Cash App support with real according to spend company. You will thread to despise money to its Current mesh in cleave to separate your ass and all. You can be used as a classified ad: as contemplated in. After you've confirmed your contact information Cash App will ask who to. -

Send Me an Invoice from Shopping Cart

Send Me An Invoice From Shopping Cart Ware never nonplussing any lash-up dilapidate hourlong, is Lauren distal and cultured enough? Prickliest Sansone pokes her masterships so thick that Darcy sulphurates very antiquely. Long-distance Winthrop remediate or jargonizing some oscillator sophistically, however fortnightly Fraser griddle juvenilely or mythicises. What can I do to place an order? Department of invoice me or send invoices for invoicing feature become available in the carts in this feature. You will receive a confirmation email with your order number shortly. If an invoice from time your invoices. Accounting software for growing businesses. If we have already processed your order, then each month, you can access this guide for information. Need programmer to picture a shopping cart with Zoho Invoice. TIME TO inherit THAT SUPER CASH! Get an invoice from stock reservation, carts now button to cart to use add or online. Add a device to your bid to proceed. In both cases you maybe get pan card reader to use card payments at the door, that person, estimates and invoices for freelancers and small teams. When the seller receives your payment, Russia, and designed to grow together with you. Offer custom level of the link on advanced tools menu is a fresh link icon to the following the additional information page. Change from an invoice me, send to cart for? Cart understand and Item Description can be used if not know details of hand cart. There are no special steps for starting a new order. Com reserves the original condition, you will send invoices or send me from an invoice. -

Fintech Innovation the Transformation of Financial Servicescover Through Technology Msci.Com

THEMATIC INSIGHTS Fintech Innovation The transformation of financial servicesCover through technology msci.com msci.com 1 InsideContents 04 Financial services and disruption Inner 05 The catalysts for fintech disruption 06 The digital wallets opportunity 11 Impact of neural networks and machine learning Left15 Conclusion Fold 2 msci.com msci.com 3 Fintech Innovation The catalysts Financial services for fintech and disruption disruption Financial Services is the second largest sector in the Put simply, financial services companies offer three global economy. It generates trillions in annual revenue fundamental functions8 (i) the securing of savings9, (ii) while commanding some USD 12 trillion1 in equity transfers and transactions across time and space10 and (iii) market capitalization. It is also a sector that might once information generation and risk assessment.11 Each of these have seemed impervious to disruption: protected (as key economic services appears to be experiencing a profound well as constrained) by regulation and dominated by and technologically-driven transformation. incumbents benefitting from seemingly sticky client Historically the financial sector has seemed largely resistant to relationships. disruption — any durable innovation has ultimately reinforced But today one can easily discern change. The US retail the incumbents. The difference today seems to lie in the banking franchises seem to have lost their daily point combination of multiple vectors of disruption. The innovations of contact with their customers,2 credit card franchises we describe below are driven by the growth and development of are losing share to marketplace lenders3 while 50-year- mobile connected devices, artificial intelligence, cloud computing old stock brokerages are seeing lower trading volumes and blockchain technologies. -

Filed by Paysafe Limited Pursuant to Rule 425 Under the Securities Act Of

Filed by Paysafe Limited pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934 Subject Company: Foley Trasimene Acquisition Corp. II SEC File No.: 001-39456 Date: March 12, 2021 PaySafe – Analyst Day, March 9, 2021 C O R P O R A T E P A R T I C I P A N T S Will Maina, Managing Director of ICR Philip McHugh, Chief Executive Officer & Director Danny Chazonoff, Chief Operating Officer Izzy Dawood, Chief Financial Officer C O N F E R E N C E C A L L P A R T I C I P A N T S Tien-tsin Huang, J.P. Morgan Josh Levin, Autonomous James Faucette, Morgan Stanley Tim Chiodo, Credit Suisse George Mihalos, Cowen & Co. Bob Napoli, William Blair Sanjay Sakhrani, KBW Tim Willi, Wells Fargo Jamie Friedman, Susquehanna Joseph Vafi, Canaccord Genuity Brett Huff, Stephens The following is a transcript of a recording of a presentation given at the Analyst Day Presentation on March 9, 2021. This transcript should be read in conjunction with, and is qualified in all respects, by the written material accompanying that presentation, which was filed pursuant to Rule 425 under the Securities Act of 1933 on March 9, 2021. P R E S E N T A T I O N Will Maina Hello, good morning, everyone. My name is Will Maina, Managing Director of ICR. Welcome to the Paysafe Analyst Day. We greatly appreciate you taking the time to learn more about Paysafe.