Invoice Payment Terms on Paypal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Electronic Fund Transfers Your Rights

ELECTRONIC FUND TRANSFERS YOUR RIGHTS AND RESPONSIBILITIES Indicated below are types of Electronic Fund Transfers we are capable of handling, some of which may not apply to your account. Please read this disclosure carefully because it tells you your rights and obligations for the transactions listed. You should keep this notice for future reference. Electronic Fund Transfers Initiated By Third Parties. You may authorize a third party to initiate electronic fund transfers between your account and the third party’s account. These transfers to make or receive payment may be one-time occurrences or may recur as directed by you. These transfers may use the Automated Clearing House (ACH) or other payments network. Your authorization to the third party to make these transfers can occur in a number of ways. For example, your authorization to convert a check to an electronic fund transfer or to electronically pay a returned check charge can occur when a merchant provides you with notice and you go forward with the transaction (typically, at the point of purchase, a merchant will post a sign and print the notice on a receipt). In all cases, these third party transfers will require you to provide the third party with your account number and bank information. This information can be found on your check as well as on a deposit or withdrawal slip. Thus, you should only provide your bank and account information (whether over the phone, the Internet, or via some other method) to trusted third parties whom you have authorized to initiate these electronic fund transfers. -

Form Ssa-714 (07-2005)

YOU CAN MAKE YOUR PAYMENT BY CREDIT CARD As a convenience, we offer you the option to make your payment by credit card. However, regular credit card rules will apply. You may also pay by check or money order. We Honor Most Major Credit Cards Please fill in all the information below and return it with your request. Note: Please read Privacy Act Notice CHECK ONE ---------------------------------------------- > MasterCard Visa Discover American Express Diners Card Credit Card Holder’s Name ---------------------------- > Print First, Middle Initial, Last Name Credit Card Holder’s Address ------------------------- > Number & Street City, State, Zip Code Daytime Telephone Number --------------------------- > - - Area Code Telephone Number Amount Charged $ - - - Credit Card Number Credit Card Expiration Date Month Year Credit Card Holder’s Signature ----------------------- > Authorization DO NOT WRITE IN THIS SPACE OFFICE USE ONLY --------------------------------------- > Name Date PRIVACY ACT STATEMENT The Social Security Administration (SSA) has authority to collect the information requested on this form under § 205 of the Social Security Act. Giving us this information is voluntary. You do not have to do it. We will need this information only if you choose to make payment by credit card. You do not need to fill out this form if you choose another means of payment (for example, by check or money order). If you choose the credit card payment option, we will provide the information you give us to the banks handling your credit card account and SSA’s account. We may also provide this information to another person or government agency to comply with federal laws requiring the release of information from our records. You can find these and other routine uses of information provided to SSA listed in the Federal Register. -

Contactless Operating Mode Requirements Clarification Whitepaper

Contactless Operating Mode Requirements Clarification Whitepaper Version 1.0 Publication Date: February 2020 U.S. Payments Forum ©2020 Page 1 About the U.S. Payments Forum The U.S. Payments Forum, formerly the EMV Migration Forum, is a cross-industry body focused on supporting the introduction and implementation of EMV chip and other new and emerging technologies that protect the security of, and enhance opportunities for payment transactions within the United States. The Forum is the only non-profit organization whose membership includes the entire payments ecosystem, ensuring that all stakeholders have the opportunity to coordinate, cooperate on, and have a voice in the future of the U.S. payments industry. Additional information can be found at http://www.uspaymentsforum.org. EMV ® is a registered trademark in the U.S. and other countries and an unregistered trademark elsewhere. The EMV trademark is owned by EMVCo, LLC. Copyright ©2020 U.S. Payments Forum and Smart Card Alliance. All rights reserved. The U.S. Payments Forum has used best efforts to ensure, but cannot guarantee, that the information described in this document is accurate as of the publication date. The U.S. Payments Forum disclaims all warranties as to the accuracy, completeness or adequacy of information in this document. Comments or recommendations for edits or additions to this document should be submitted to: [email protected]. U.S. Payments Forum ©2020 Page 2 Table of Contents 1. Introduction .......................................................................................................................................... 4 2. Contactless Operating Modes ............................................................................................................... 5 2.1 Impact of Contactless Operating Mode on Debit Routing Options .............................................. 6 3. Contactless Issuance Requirements ..................................................................................................... 7 4. -

Is China's New Payment System the Future?

THE BROOKINGS INSTITUTION | JUNE 2019 Is China’s new payment system the future? Aaron Klein BROOKINGS INSTITUTION ECONOMIC STUDIES AT BROOKINGS Contents About the Author ......................................................................................................................3 Statement of Independence .....................................................................................................3 Acknowledgements ...................................................................................................................3 Executive Summary ................................................................................................................. 4 Introduction .............................................................................................................................. 5 Understanding the Chinese System: Starting Points ............................................................ 6 Figure 1: QR Codes as means of payment in China ................................................. 7 China’s Transformation .......................................................................................................... 8 How Alipay and WeChat Pay work ..................................................................................... 9 Figure 2: QR codes being used as payment methods ............................................. 9 The parking garage metaphor ............................................................................................ 10 How to Fund a Chinese Digital Wallet .......................................................................... -

Key Payment and Service Information What Is Paypal?

Key Payment and Service Information What is PayPal? • PayPal enables individuals and businesses to send electronic money online. It also provides other financial and non-financial services closely related to online payments. These services are collectively referred to hereafter as the “Service”. • PayPal does not provide credit and/or escrow services. • PayPal does not allow you to hold funds in your PayPal account. Who provides the Service? The Service is provided by PayPal (Europe) S.á r.l. & Cie, S.C.A. (also referred to as “PayPal” in this document) to registered users in the European Union (each a “User”). • PayPal (Europe) S.à r.l. & Cie, S.C.A. (R.C.S. Luxembourg B 118 349) is duly licensed as a Luxembourg credit institution in the sense of Article 2 of the law of 5 April 1993 on the financial sector as amended (the “Law”) and is under the prudential supervision of the Luxembourg supervisory authority, the Commission de Surveillance du Secteur Financier Opening a PayPal account • The Service allows individuals and businesses to open an account maintained byPayPal (an “account”). • To be eligible for an account, a User must: o either be an individual (at least 18 years old) or a business that is able to form a legally binding contract; and o have satisfactorily completed our sign-up process • As part of our sign-up process, a User: o must register an email address, which will also act as their ‘User ID’; o may submit details of the source(s) with which they wish to fund their PayPal account (e.g., details of the User’s credit card). -

List of Merchants 4

Merchant Name Date Registered Merchant Name Date Registered Merchant Name Date Registered 9001575*ARUBA SPA 05/02/2018 9013807*HBC SRL 05/02/2018 9017439*FRATELLI CARLI SO 05/02/2018 9001605*AGENZIA LAMPO SRL 05/02/2018 9013943*CASA EDITRICE LIB 05/02/2018 9017440*FRATELLI CARLI SO 05/02/2018 9003338*ARUBA SPA 05/02/2018 9014076*MAILUP SPA 05/02/2018 9017441*FRATELLI CARLI SO 05/02/2018 9003369*ARUBA SPA 05/02/2018 9014276*CCS ITALIA ONLUS 05/02/2018 9017442*FRATELLI CARLI SO 05/02/2018 9003946*GIUNTI EDITORE SP 05/02/2018 9014368*EDITORIALE IL FAT 05/02/2018 9017574*PULCRANET SRL 05/02/2018 9004061*FREDDY SPA 05/02/2018 9014569*SAVE THE CHILDREN 05/02/2018 9017575*PULCRANET SRL 05/02/2018 9004904*ARUBA SPA 05/02/2018 9014616*OXFAM ITALIA 05/02/2018 9017576*PULCRANET SRL 05/02/2018 9004949*ELEMEDIA SPA 05/02/2018 9014762*AMNESTY INTERNATI 05/02/2018 9017577*PULCRANET SRL 05/02/2018 9004972*ARUBA SPA 05/02/2018 9014949*LIS FINANZIARIA S 05/02/2018 9017578*PULCRANET SRL 05/02/2018 9005242*INTERSOS ASSOCIAZ 05/02/2018 9015096*FRATELLI CARLI SO 05/02/2018 9017676*PIERONI ROBERTO 05/02/2018 9005281*MESSAGENET SPA 05/02/2018 9015228*MEDIA SHOPPING SP 05/02/2018 9017907*ESITE SOCIETA A R 05/02/2018 9005607*EASY NOLO SPA 05/02/2018 9015229*SILVIO BARELLO 05/02/2018 9017955*LAV LEGA ANTIVIVI 05/02/2018 9006680*PERIODICI SAN PAO 05/02/2018 9015245*ASSURANT SERVICES 05/02/2018 9018029*MEDIA ON SRL 05/02/2018 9007043*INTERNET BOOKSHOP 05/02/2018 9015286*S.O.F.I.A. -

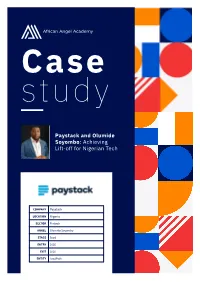

Paystack and Olumide Soyombo: Achieving Lift-Off for Nigerian Tech

Case study Paystack and Olumide Soyombo: Achieving Lift-off for Nigerian Tech COMPANY Paystack LOCATION Nigeria SECTOR Fintech ANGEL Olumide Soyombo STAGE Seed ENTRY 2016 EXIT 2020 ENTITY LeadPath www.africanangelacademy.com “PAYMENTS GIANT STRIPE HAS BOUGHT NIGERIAN PAYMENTS STARTUP PAYSTACK FOR AFRICAN EXPANSION” – QUARTZ AFRICA On 15 October 2020, the headlines a 1,400% return on investment have to be us again.” emblazoned across every major (ROI) – the largest exit for Nigerian By the time Shola had approached tech news platform carried the tech investors to date. For angel him for seed funding for Paystack same thrilling news about the investor Olumide Soyombo, in 2015, Olumide knew angels Nigerian fintech phenom Paystack. however, the exit was more than a would need to plan on a second The acquisition, reportedly valued lucrative cash out; it was a turning seed, or even a third, to get these at US$200 million, was a big deal point for the Nigerian tech sector startups to the growth round. But – a very big deal. For Stripe, a he had been helping to build out in the years after Olumide became Silicon Valley unicorn with global for more than a decade. Paystack’s first Nigerian investor, ambitions, it represented a major local investors were still slow on the strategic move. They were already Olumide had been part of the uptake, pushing Olumide to become on a growth streak that year, having Lagos tech ecosystem as an one of the most prolific early recently expanded services into entrepreneur since 2008, when he investors in Lagos, where he had five new European markets. -

IDC, the Business Value of the Stripe Payments Platform

IDC White Paper | The Business Value of the Stripe Payments Platform Sponsored by: Stripe The Business Value of the Stripe Authors: Jordan Jewell Matthew Marden Payments Platform March 2018 EXECUTIVE SUMMARY Business Value Over the past five years, IDC has witnessed a monumental shift as companies adapt their Highlights business models and strategies to meet the requirements of the digital economy. From traditional ecommerce to subscription software-as-a-service (SaaS) businesses to multisided Impact of Stripe (after marketplaces, digital commerce is enabling businesses to rethink what they sell, how they sell, deploying) and where they sell. Businesses are also rethinking how they transact with other businesses, 6.7% with consumers across borders, and with different currencies and payment methods. higher revenue The result is a dramatic shift in how companies engage online, meet increasingly demanding consumer and business expectations, and grow in a complex regulatory landscape by market. 59% Fickle consumer and business buyers have come to expect an intuitive and instantaneous higher developer productivity checkout process with support for multiple payment options. However, aging financial 24% infrastructure and complex interdependencies between numerous parties have historically lower cost of building/operat- made it difficult and expensive to accept payments online seamlessly and across markets ing online payments platform and currencies. In the early days of the internet, businesses wishing to succeed in the digital 81% commerce landscape had no choice but to make large investments in software, services, and fewer unplanned outages employees to build and support homegrown online payments systems. However, if we look at the current and expected pace of growth in the digital commerce market, this approach of building a “good enough” payments platform from scratch will no longer suffice. -

Mastercard Frequently Asked Questions Platinum Class Credit Cards

Mastercard® Frequently Asked Questions Platinum Class Credit Cards How do I activate my Mastercard credit card? You can activate your card and select your Personal Identification Number (PIN) by calling 1-866-839-3492. For enhanced security, RBFCU credit cards are PIN-preferred and your PIN may be required to complete transactions at select merchants. After you activate your card, you can manage your account through your Online Banking account and/or the RBFCU Mobile app. You can: • View transactions • Enroll in paperless statements • Set up automatic payments • Request Balance Transfers and Cash Advances • Report a lost or stolen card • Dispute transactions Click here to learn more about managing your card online. How do I change my PIN? Over the phone by calling 1-866-297-3413. There may be situations when you are unable to set your PIN through the automated system. In this instance, please visit an RBFCU ATM to manually set your PIN. Can I use my card in my mobile wallet? Yes, our Mastercard credit cards are compatible with PayPal, Apple Pay®, Samsung Pay, FitbitPay™ and Garmin FitPay™. Click here for more information on mobile payments. You can also enroll in Mastercard Click to Pay which offers online, password-free checkout. You can learn more by clicking here. How do I add an authorized user? Please call our Member Service Center at 1-800-580-3300 to provide the necessary information in order to qualify an authorized user. All non-business Mastercard account authorized users must be members of the credit union. Click here to learn more about authorized users. -

A GUIDE to ELECTION YEAR ACTIVITIES of SECTION 501(C)(3) ORGANIZATIONS

A GUIDE TO ELECTION YEAR ACTIVITIES OF SECTION 501(c)(3) ORGANIZATIONS BY STEVEN H. SHOLK, ESQ. STEVEN H. SHOLK, ESQ. GIBBONS P.C. ONE GATEWAY CENTER NEWARK, NEW JERSEY 07102-5310 (973) 596-4639 [email protected] ONE PENNSYLVANIA PLAZA 37th FLOOR NEW YORK, NEW YORK 10119-3701 (212) 613-2000 Copyright Steven H. Sholk 2016 All Rights Reserved 776148.37 999999-00262 TABLE OF CONTENTS Page STATUTORY PROVISIONS ON CONTRIBUTIONS, EXPENDITURES, AND ELECTIONEERING ......................................................................................................... 1 STATUTORY AND REGULATORY PROVISIONS ON CONTRIBUTIONS TO AND FUNDRAISING FOR SECTION 501(c)(3) ORGANIZATIONS ................................ 159 REGULATORY PROVISIONS ON CONTRIBUTIONS, EXPENDITURES, AND ELECTIONEERING ..................................................................................................... 191 VOTER REGISTRATION AND GET-OUT-THE-VOTE DRIVES........................................ 315 VOTER GUIDES....................................................................................................................... 326 CANDIDATE APPEARANCES AND ADVERTISEMENTS ................................................ 339 CANDIDATE DEBATES ......................................................................................................... 352 CANDIDATE USE OF FACILITIES AND OTHER ASSETS ................................................ 355 WEBSITE ACTIVITIES .......................................................................................................... -

Service Provider Name Region AOC Date Assessor DESV

A company’s name appears on this Compliant Service Provider List if (i) Mastercard has received a copy of an Attestation of Compliance (AOC) by a Qualified Security Assessor (QSA) reflecting validation of the company being PCI DSS compliant and (ii) Mastercard records reflect the company is registered as a Service Provider by one or more Mastercard Customers. The date of the AOC and the name of the QSA are also provided. Each AOC is valid for one year. Mastercard receives copies of AOCs from various sources. This Compliant Service Provider List is provided solely for the convenience of Mastercard Customers and any Customer that relies upon or otherwise uses this Compliant Service Provider list does so at the Customer’s sole risk. While Mastercard endeavors to keep the list current as of the date set forth in the footer, Mastercard disclaims any and all warranties of any kind, including any warranty of accuracy or completeness or fitness for any particular purpose. Mastercard disclaims any and all liability of any nature relating to or arising in connection with the use of or reliance on the Compliant Service Provider List or any part thereof. Each Mastercard Customer is obligated to comply with Mastercard Rules and other Standards pertaining to use of a Service Provider. As a reminder, an AOC by a QSA provides a “snapshot” of security controls in place at a point in time. Compliant Service Provider 1-60 Days Past AOC Due Date 61-90 Days Past AOC Due Date Service Provider Name Region AOC Date Assessor DESV “BPC Processing”, LLC Europe 03/31/2017 Informzaschita 1&1 Internet SE (1&1, 1&1 ipayment, Europe 05/08/2017 Security Research & Consulting GmbH ipayment.de) 1Shoppingcart.com (Web.com Group, lnc.) US 04/29/2017 SecurityMetrics 2138617 Ontario Inc. -

Smart Cards Vs Mag Stripe Cards

Benefits of Smart Cards versus Magnetic Stripe Cards for Healthcare Applications Smart cards have significant benefits versus magnetic stripe (“mag stripe”) cards for healthcare applications. First, smart cards are highly secure and are used worldwide in applications where the security and privacy of information are critical requirements. • Smart cards embedded with microprocessors can encrypt and securely store information, protecting the patient’s personal health information. • Smart cards can allow access to stored information only to authorized users. For example, all or portions of the patient’s personal health information can be protected so that only authorized doctors, hospitals and medical staff can access it. The rules for accessing medical information can be enforced by the smart card, even when used offline. • Smart cards support strong authentication for accessing personal health information. Patients and providers can use smart health ID cards as a second factor when logging in to access information. In addition, smart cards support personal identification numbers and biometrics (e.g., a fingerprint) to further protect access. • Smart cards support digital signatures, which can be used to determine that the card was issued by a valid organization and that the data on the card has not been fraudulently altered since issuance. • Smart cards use secure chip technology and are designed and manufactured with features that help to deter counterfeiting and thwart tampering. • Smart cards can help to reduce healthcare fraud by providing strong identity authentication of patients and providers. The use of secure smart chip technology, encryption and other cryptography measures makes it extremely difficult for unauthorized users to access or use information on a smart card or to create duplicate cards.