CHAPTER 1 INTRODUCTION Following Schumpeter‟S (1939

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SEMICON® Southeast Asia 2017 25–27 April, 2017 Spice Arena, Penang, Malaysia

POST SHOW REPORT 25–27 APRIL, 2017 SPICE ARENA, PENANG, MALAYSIA SEMICON® Southeast Asia 2017 25–27 April, 2017 Spice Arena, Penang, Malaysia Highlights: • NEW: Futura-X@World-of-IoT • NEW: Technology Start-up Showcase • NEW: Vietnam Investment Seminar • Inauguration of the Semiconductor Fabrication Association Malaysia • International Sourcing Program (Hosted by MATRADE) Key Visiting Companies • More than 60 hours of specialized technical and business programs • Networking Night at Fort Cornwallis (Hosted by Invest-in-Penang) • Amkor • SEMICON SEA University Program • ASE • B. Braun Medical • Broadcom Registration • CARSEM • Continental Automotive Total Attendance 6,762 • Fuji Electric • GLOBALFOUNDRIES Total Verifi ed Visitors 4,917 • Globetronics Total Exhibitors 1,845 • Hana Microelectronics • ICDREC • Inari Technology Visitors by Region • Infi neon • Intel Corporation Malaysia 79% • Jabil Circuit International 21% • Keysight Technologies • Lam Research • NXP Expanded Electronics Supply Chain Presence • ON Semiconductor • Osram Opto Semiconductors Addressing the need for collaboration across the electronics • Renesas manufacturing supply chain, SEMICON Southeast Asia increasingly • SanDisk attracts audiences from multiple industry segments, including: • Siemens • Silterra Malaysia • Design and Electronics Design Automation • STMicroelectronics • Electronics Manufacturing Services • UNISEM • Flexible Electronics • VITROX • Western Digital • System Integrators • X-fab • Automotive www.semiconsea.org POST SHOW REPORT 25–27 APRIL, 2017 -

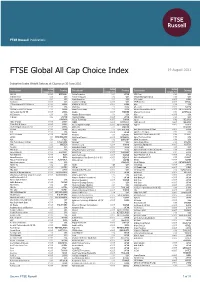

FTSE Global All Cap Choice Index

2 FTSE Russell Publications 19 August 2021 FTSE Global All Cap Choice Index Indicative Index Weight Data as at Closing on 30 June 2021 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 1&1 AG <0.005 GERMANY Activia Properties 0.01 JAPAN AES Corp. 0.03 USA 10X Genomics 0.03 USA Activision Blizzard 0.12 USA Affiliated Managers Group 0.01 USA 1Life Healthcare 0.01 USA Acuity Brands Inc 0.01 USA Affle (India) <0.005 INDIA 1st Source <0.005 USA Acushnet Holdings <0.005 USA AFI Properties <0.005 ISRAEL 21Vianet Group ADS (N Shares) <0.005 CHINA ADAMA (A) (SC SZ) <0.005 CHINA Aflac 0.06 USA 2U <0.005 USA Adani Gas 0.01 INDIA AfreecaTV <0.005 KOREA 360 DigiTech ADS (N Shares) 0.01 CHINA Adani Green Energy 0.01 INDIA African Rainbow Minerals Ltd <0.005 SOUTH AFRICA 360 Security (A) (SC SH) <0.005 CHINA Adapteo <0.005 SWEDEN Afterpay Touch Group 0.03 AUSTRALIA 3-D Systems 0.01 USA Adaptive Biotechnologies 0.01 USA Afya <0.005 USA 3i Group 0.02 UNITED Adastria Holdings <0.005 JAPAN AGCO Corp 0.01 USA KINGDOM A-Data Technology <0.005 TAIWAN Ageas 0.02 BELGIUM 3SBio (P Chip) <0.005 CHINA ADBRI <0.005 AUSTRALIA AGFA-Gevaert <0.005 BELGIUM 51job ADS (N Shares) <0.005 CHINA Adcock Ingram Holdings <0.005 SOUTH AFRICA Aggreko <0.005 UNITED 5I5j Holding Group (A) (SC SZ) <0.005 CHINA Addtech B 0.01 SWEDEN KINGDOM 77 Bank <0.005 JAPAN Adecco Group AG 0.02 SWITZERLAND Agile Group Holdings (P Chip) <0.005 CHINA 8x8 <0.005 USA Adeka <0.005 JAPAN Agilent Technologies 0.07 USA A.G.V. -

Retirement Strategy Fund 2055 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2055 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0584% 0.0584% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0328% 0.0328% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0395% 0.0395% AMERICOLD REALTY TRUST REIT USD.01 0.0426% 0.0426% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0247% 0.0247% ASSURA PLC REIT GBP.1 0.0318% 0.0318% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0101% 0.0101% BOSTON PROPERTIES INC REIT USD.01 0.0579% 0.0579% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0417% 0.0417% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0393% 0.0393% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0227% 0.0227% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0104% 0.0104% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0377% 0.0377% COMFORIA RESIDENTIAL REIT IN REIT 0.0327% 0.0327% COUSINS PROPERTIES INC REIT USD1.0 0.0402% 0.0402% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Malaysia`S E&E Industry

Malaysia`s E&E Industry • Malaysia: A Global Electrical and Electronic (E&E) - Developments impacting global industry Page 5 Products Powerhouse . Sustainable E&E talent pool - Records of a well-rooted industry . Embracing the Fourth Industrial Revolution (Industry 4.0) . Vibrant local ecosystem and supply chain - Five decades and beyond - Factsheet: The E&E industry today - Opportunities in E&E subsectors: Semiconductors; LED; solar . E&E at a glance . Semiconductors . Electronic Manufacturing Services (EMS) . LED . E&E-related Associations and Chambers . Solar 01 of Commerce Content • Decide Today: Invest in Malaysia - Strategically located with well-developed infrastructure 02 - Providing access to global markets - Fostering liberalised equity ownership - Facilitating employment of expatriates - Prioritising business-friendly policies - Fostering research facilities/incubators and standards bodies Page 22 - Malaysia allows for maximum repatriation of income - Malaysia guarantees intellectual property protection • How MIDA Helps Smooth out Your Investment Journey in Malaysia - Obtaining applicable financial/monetary/tax incentives Page 24 - Expediting approvals of applications and permits - Facilitation of various processes - Success stories 03 • Next Steps for Your Investment 02 - Learn more about Malaysia’s E&E industry players 04 - Check out how to get started in Malaysia - Connect with MIDA Page 27 E&E is a key driver of Malaysia’s industrial development, contributing significantly to GDP “ growth, export earnings, investment, and employment, thus stimulating the growth of new economic clusters, particularly in relation to manufacturing-related services such as testing and engineering, as well as trade services-related global hub activities 4 Malaysia: A Global Electrical and Electronic Products Powerhouse Records of a well-rooted industry Malaysia’s diverse electrical and electronic products (E&E) industry is in its fifth decade of operations, having started with just eight component production companies in the 1970s (also known as the “8 Samurais”). -

BACHELOR of APPLIED SCIENCE for a Sustainable Tomorrow for Transforming Higher Education Transforming

BACHELOR OF APPLIED SCIENCE BACHELOR BACHELOR OF APPLIED SCIENCE Transforming Higher Education for a Sustainable Tomorrow Bachelor of Applied Science Academic Session 2019/2020 USM Vision Transforming Higher Education for a Sustainable Tomorrow USM Mission USM is a pioneering, transdisciplinary research intensive university that empowers future talents and enables the bottom billions to transform their socio-economic well-being i CONTENTS SECTION A ACADEMIC INFORMATION VISION AND MISSION i CONTENTS ii ACADEMIC CALENDAR iii 1.0 BACHELOR OF APPLIED SCIENCE 1.1 General Information 1 1.2 Areas of Specialization 1 1.3 Programme Structure 2 1.4 Courses Offering 2 * Core Courses 2 * Minor Courses 2 * Elective Courses 2 * Optional Courses 3 * Audit Courses 3 1.5 Course Codes 4 1.6 Classification of year equivalent 4 1.7 Graduation Requirements 4 2.0 ACADEMIC SYSTEM AND GENERAL INFORMATION 2.1 Course Registration 5-11 2.2 Interpretation of Unit/Credit/Course 11 2.3 Examination System 12-16 2.4 Unit Exemption 16-18 2.5 Credit Transfer 18-20 2.6 Academic Integrity 20-24 2.7 USM Mentor Programme 24 2.8 Student Exchange Programme 25-26 2.9 Ownership of Students’ Dissertation/Research Project/ 26 Theses and University’s Intellectual Property 3.0 UNIVERSITY COURSE REQUIREMENTS 3.1 Summary of University Course Requirements 27 3.2 General Studies Components (MPU) 28-33 3.3 Language Skills 34-36 3.4 Options (1-8 Credits) 36-38 SECTION B DEGREE PROGRAMME INFORMATION * School of Physics 40 * School of Mathematical Sciences 101 * School of Biological Sciences -

Camscanner 10-04-2020 17.18.33

CORPORATE ll·CElxiEMALAHlAOCTOBER 5, 2020 S1 COVER STORY normal as the has changed cnstlcaly. Meanwhle, the htensltled US-chinatrade war and the great demupllngbetween the two superpowershave madethe business environmenteven more complex.It Is llke sallng In rough seas on a stormy night. Last month, The Edge took a b1p up north In search of bright spots In the current trying Umes. We met with the captains of the electrlcal and electronics(E&E) and the medical devices Industries. The picture they presented Is not all that gloomy. The Movement Control Order, It seems. Is just a hiccup. In fact. these companies (0 are benefitingfrom trade diversion � and are hiring Instead of firing, and .J,.... (0 expanding, not downsizing, llke s: many others have been forced to do. BY LIEW IIA TENG 2019 demand by end-use & The mature ecosystem that has "'CT been developed since the 1970s has s its name implies, a semicon (0 attractedan Increasing number of ductor chip is made of a mate O> CT multlnaUonal corporaUons to set up rial that conducts current, but g_ their regional producUon bases In not completely.The conductivity "' Communication Computer Consumer AutomotiveB Industrial Government� Penang. of a semiconductor lies some □ ----- ----- --- ---- ----- - We travelled to Bayan Lepas where between that of an insu - - - -- - ::\' -10.5 -18.7 -5.2 -6.9 -13.0 13.0 " and the Batu Kawan Industrial Park, lator, which has almost no con 0"' ductivity,and conductor,which has almost ----- --------- ----------- "' where most of these companies are a - - -

Malaysia—Attracting Superstar Firms in the Electrical and Electronics Industry Through Investment Promotion

Chapter 8 Malaysia—Attracting superstar firms in the electrical and electronics industry through investment promotion MAXIMILIAN PHILIP ELTGEN, YAN LIU, AND YEW KEAT CHONG Summary This case study shows how attracting foreign direct investment (FDI) through active investment promotion jump-started the development of Malaysia’s electrical and electronics (E&E) indus- try, which, facilitated by workforce development and linking programs, significantly upgraded over time. In the early 1970s, proactive investment promotion with high-level political sup- port, along with a competitive investment climate, led a few of the industry’s “superstar” firms to locate in Malaysia. This move launched an incipient industry focused on labor-intensive, low-skilled production and assembly. Over the years, the multinational corporations (MNCs) operating in Malaysia gradually shifted into higher-value-added activities and developed local suppliers, and domestic companies emerged onto the scene. This process was supported by a number of government programs, including the provision of incentives, supplier development efforts, and workforce development initiatives. The creation of the Penang Skills Development Centre in 1989 stands out as an internationally recognized example of a tripartite, industry-led workforce development initiative involving the private sector, government, and academia. By looking at a 50-year process, this case study also provides insights into the effectiveness of dis- tinct strategic approaches and policy tools for leveraging FDI at different phases of a country’s development. Malaysia’s role in the electrical and electronics global value chain The electrical and electronics global value chain The E&E global value chain (GVC) comprises a number of electrical and electronic compo- nents, assembly processes, and distribution channels that serve a variety of end markets (see figure 8.1).1,2 Broadly speaking, the GVC can be divided into five separate production stages: 1. -

STATE STREET INSTITUTIONAL INVESTMENT TRUST Form

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-05-28 | Period of Report: 2021-03-31 SEC Accession No. 0001752724-21-118945 (HTML Version on secdatabase.com) FILER STATE STREET INSTITUTIONAL INVESTMENT TRUST Mailing Address Business Address ONE LINCOLN STREET STATE STREET FINANCIAL CIK:1107414| IRS No.: 046910804 | State of Incorp.:MA | Fiscal Year End: 1231 BOSTON MA 02111 CENTER Type: NPORT-P | Act: 40 | File No.: 811-09819 | Film No.: 21979468 ONE LINCOLN STREET BOSTON MA 02111 6176623239 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Quarterly Report March 31, 2021 State Street Institutional Investment Trust State Street Equity 500 Index Fund State Street Equity 500 Index II Portfolio State Street Aggregate Bond Index Fund State Street Aggregate Bond Index Portfolio State Street Global All Cap Equity ex- U.S. Index Fund State Street Global All Cap Equity ex- U.S. Index Portfolio State Street Small/Mid Cap Equity Index Fund State Street Small/Mid Cap Equity Index Portfolio State Street Defensive Global Equity Fund State Street Emerging Markets Equity Index Fund State Street Hedged International Developed Equity Index Fund State Street Target Retirement Fund State Street Target Retirement 2020 Fund State Street Target Retirement 2025 Fund State Street Target Retirement 2030 Fund State Street Target Retirement 2035 Fund State Street Target Retirement 2040 Fund State Street Target Retirement 2045 Fund State Street Target Retirement 2050 Fund State Street Target Retirement 2055 Fund State Street Target Retirement 2060 Fund State Street Target Retirement 2065 Fund State Street International Value Spotlight Fund State Street China Equity Select Fund The information contained in this report is intended for the general information of shareholders of the Trust. -

List of Semiconductor Fabrication Plants

List of semiconductor fabrication plants This is a list of semiconductor fabrication plants: A semiconductor fabrication plant is where integrated circuits (ICs), also known as microchips, are made. They are either operated by Integrated Device Manufacturers (IDMs) who design and manufacture ICs in-house and may also manufacture designs from design only firms(fabless companies), or by Pure Play foundries, who only manufacture designs from fabless companies but do not design their own ICs. Notes: Plant location is where the plant is located, Started production is when the plant officially started volume(or mass) production, Wafer size is the largest wafer size that the facility is capable of processing, Process Technology Node is the size of the smallest features that the facility is capable of etching onto the wafers, Wafer capacity per month is the plant's Nameplate capacity. It does not mean that the facility is working at that capacity. The number of wafers that a plant actually processes in relation to its nameplate capacity is referred to as the plant's utilization. Technology/Products are the products that the facility is capable of producing, as not all plants can produce all products on the market. Open plants are listed below; plants that are closed are below this first table. Contents Open Closed See also References External links Open Process Wafer Started Wafer size technology Company Plant name Plant location Plant cost (in US$ billions) production Technology/products production (in mm) node (in capacity/month nm) ISRO SCL -

ISO/IEC JTC1/SC17 STANDING DOCUMENT 5 (Updated March 2018) Register of IC Manufacturers

ISO/IEC JTC1/SC17 STANDING DOCUMENT 5 (Updated March 2018) Register of IC manufacturers Identifier Company Country '01' Motorola UK '02' STMicroelectronics SA France '03' Hitachi, Ltd Japan '04' NXP Semiconductors Germany '05' Infineon Technologies AG Germany '06' Cylink USA '07' Texas Instrument France '08' Fujitsu Limited Japan '09' Matsushita Electronics Corporation, Semiconductor Company Japan '0A' NEC Japan '0B' Oki Electric Industry Co. Ltd Japan '0C' Toshiba Corp. Japan '0D' Mitsubishi Electric Corp. Japan '0E' Samsung Electronics Co. Ltd Korea '0F' Hynix Korea '10' LG-Semiconductors Co. Ltd Korea '11' Emosyn-EM Microelectronics USA '12' INSIDE Technology France '13' ORGA Kartensysteme GmbH Germany '14' SHARP Corporation Japan '15' ATMEL France '16' EM Microelectronic-Marin SA Switzerland '17' SMARTRAC TECHNOLOGY GmbH Germany '18' ZMD AG Germany '19' XICOR, Inc. USA '1A' Sony Corporation Japan Identifier Company Country '1B' Malaysia Microelectronic Solutions Sdn. Bhd Malaysia '1C' Emosyn USA '1D' Shanghai Fudan Microelectronics Co. Ltd. P.R. China '1E' Magellan Technology Pty Limited Australia '1F' Melexis NV BO Switzerland '20' Renesas Technology Corp. Japan '21' TAGSYS France '22' Transcore USA '23' Shanghai belling corp., ltd. China '24' Masktech Germany Gmbh Germany '25' Innovision Research and Technology Plc UK '26' Hitachi ULSI Systems Co., Ltd. Japan '27' Yubico AB Sweden '28' Ricoh Japan '29' ASK France '2A' Unicore Microsystems, LLC Russian Federation '2B' Dallas Semiconductor/Maxim USA '2C' Impinj, Inc. USA '2D' RightPlug Alliance USA '2E' Broadcom Corporation USA '2F' MStar Semiconductor, Inc Taiwan, ROC '30' BeeDar Technology Inc. USA ‘31’ RFIDsec Denmark ‘32’ Schweizer Electronic AG Germany ‘33’ AMIC Technology Corp Taiwan ‘34’ Mikron JSC Russia ‘35’ Fraunhofer Institute for Photonic Microsystems Germany ‘36’ IDS Microchip AG Switzerland ‘37’ Kovio USA ‘38’ HMT Microelectronic Ltd Switzerland '39' Silicon Craft Technology Thailand Identifier Company Country ‘3A’ Advanced Film Device Inc. -

Retirement Strategy Fund 2025 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2025 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0233% 0.0233% AEON REIT INVESTMENT CORP REIT 0.0331% 0.0331% ALEXANDER + BALDWIN INC REIT 0.0200% 0.0200% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0991% 0.0991% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0557% 0.0557% ALLIED PROPERTIES REAL ESTAT REIT 0.0372% 0.0372% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0470% 0.0470% AMERICAN HOMES 4 RENT A REIT USD.01 0.0671% 0.0671% AMERICOLD REALTY TRUST REIT USD.01 0.0724% 0.0724% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0210% 0.0210% AROUNDTOWN SA COMMON STOCK EUR.01 0.0420% 0.0420% ASSURA PLC REIT GBP.1 0.0540% 0.0540% AUSTRALIAN DOLLAR 0.0104% 0.0104% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0172% 0.0172% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0172% 0.0172% BOSTON PROPERTIES INC REIT USD.01 0.0983% 0.0983% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0709% 0.0709% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0324% 0.0324% CAMDEN PROPERTY TRUST REIT USD.01 0.0668% 0.0668% CANADIAN DOLLAR 0.0009% 0.0009% CAPITALAND COMMERCIAL TRUST REIT 0.0386% 0.0386% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0177% 0.0177% CITY DEVELOPMENTS LTD COMMON STOCK 0.0219% 0.0219% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0640% 0.0640% COMFORIA RESIDENTIAL REIT IN REIT 0.0555% 0.0555% COUSINS PROPERTIES INC REIT USD1.0 0.0683% 0.0683% CUBESMART REIT USD.01 0.0609% 0.0609% DAIWA OFFICE INVESTMENT -

Industries Machinery & Equipment Engineering Supporting

Malaysia’s Machinery & Equipment and Engineering Supporting Industries THE MACHINERY AND EQUIPMENT (M&E) INDUSTRY Malaysia hosts world renowned advanced and sophisticated M&E manufacturers such as AIDA, SKF, • Malaysia as the Regional Cohu, VAT, Oerlikon Balzers, Favelle Favco, Bromma, Production Hub for M&E Vitrox, Besi, Mühlbauer, SRM ,FMC that leverages on • To Promote High Technology & the nation’s conducive business eco-system. High Value Added M&E • Centre for Training, Malaysia - Your Location for M&E Investments Reconditioning & Upgrading of M&E, Sales and Distribution • Highly skilled manpower for research and Center development and engineering design activities. • A mature engineering supporting industry for the outsourcing of modules, parts & components and engineering services. • Attractive incentives for the manufacture and assembly of high technology and specialised M&E. • A strategic gateway to the ASEAN market population of 634 million people in 2017 and total GDP of US$6.7 trillion by 2030. • Well-developed infrastructures including excellent land, sea and air connectivity, and integrated telecommunication systems. Promoting M&E Growth Machinery and Equipment (M&E) industry is one of the catalytic subsector identified under the 11th Malaysia Plan to spur the country’s economic transformation to greater prosperity, due to its cross cutting linkages with all economic segments such as the primary, manufacturing and services sectors. The adoption of technological advancement would steer the country’s progression to become a high income nation by 2020. To enhance the growth and encourage investments in the M&E sector, the Government offers the following:- Opportunities • Normal tax incentives : The M&E industry is highly competitive and consistently striving to innovate new production (a) Pioneer Status with tax exemption of systems and provide integrated solutions 70% of statutory income for a period of with the most advanced technologies and 5 years, or automation.