The Monetary Systems of the Han and Roman Empires

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

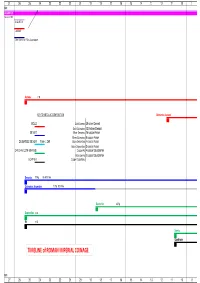

TIMELINE of ROMAN IMPERIAL COINAGE

27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 B.C. AUGUSTUS 16 Jan 27 BC AUGUSTUS CAESAR Other title: e.g. Filius Augustorum Aureus 7.8g KEY TO METALLIC COMPOSITION Quinarius Aureus GOLD Gold Aureus 25 silver Denarii Gold Quinarius 12.5 silver Denarii SILVER Silver Denarius 16 copper Asses Silver Quinarius 8 copper Asses DE-BASED SILVER from c. 260 Brass Sestertius 4 copper Asses Brass Dupondius 2 copper Asses ORICHALCUM (BRASS) Copper As 4 copper Quadrantes Brass Semis 2 copper Quadrantes COPPER Copper Quadrans Denarius 3.79g 96-98% fine Quinarius Argenteus 1.73g 92% fine Sestertius 25.5g Dupondius 12.5g As 10.5g Semis Quadrans TIMELINE of ROMAN IMPERIAL COINAGE B.C. 27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 9 10 11 A.D.A.D. denominational relationships relationships based on Aureus Aureus 7.8g 1 Quinarius Aureus 3.89g 2 Denarius 3.79g 25 50 Sestertius 25.4g 100 Dupondius 12.4g 200 As 10.5g 400 Semis 4.59g 800 Quadrans 3.61g 1600 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 91011 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 19 Aug TIBERIUS TIBERIUS Aureus 7.75g Aureus Quinarius Aureus 3.87g Quinarius Aureus Denarius 3.76g 96-98% fine Denarius Sestertius 27g Sestertius Dupondius 14.5g Dupondius As 10.9g As Semis Quadrans 3.61g Quadrans 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 TIBERIUS CALIGULA CLAUDIUS Aureus 7.75g 7.63g Quinarius Aureus 3.87g 3.85g Denarius 3.76g 96-98% fine 3.75g 98% fine Sestertius 27g 28.7g -

Hwang, Yin (2014) Victory Pictures in a Time of Defeat: Depicting War in the Print and Visual Culture of Late Qing China 1884 ‐ 1901

Hwang, Yin (2014) Victory pictures in a time of defeat: depicting war in the print and visual culture of late Qing China 1884 ‐ 1901. PhD Thesis. SOAS, University of London http://eprints.soas.ac.uk/18449 Copyright © and Moral Rights for this thesis are retained by the author and/or other copyright owners. A copy can be downloaded for personal non‐commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder/s. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. When referring to this thesis, full bibliographic details including the author, title, awarding institution and date of the thesis must be given e.g. AUTHOR (year of submission) "Full thesis title", name of the School or Department, PhD Thesis, pagination. VICTORY PICTURES IN A TIME OF DEFEAT Depicting War in the Print and Visual Culture of Late Qing China 1884-1901 Yin Hwang Thesis submitted for the degree of Doctor of Philosophy in the History of Art 2014 Department of the History of Art and Archaeology School of Oriental and African Studies, University of London 2 Declaration for PhD thesis I have read and understood regulation 17.9 of the Regulations for students of the School of Oriental and African Studies concerning plagiarism. I undertake that all the material presented for examination is my own work and has not been written for me, in whole or in part, by any other person. -

Hadrian and the Greek East

HADRIAN AND THE GREEK EAST: IMPERIAL POLICY AND COMMUNICATION DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of the Ohio State University By Demetrios Kritsotakis, B.A, M.A. * * * * * The Ohio State University 2008 Dissertation Committee: Approved by Professor Fritz Graf, Adviser Professor Tom Hawkins ____________________________ Professor Anthony Kaldellis Adviser Greek and Latin Graduate Program Copyright by Demetrios Kritsotakis 2008 ABSTRACT The Roman Emperor Hadrian pursued a policy of unification of the vast Empire. After his accession, he abandoned the expansionist policy of his predecessor Trajan and focused on securing the frontiers of the empire and on maintaining its stability. Of the utmost importance was the further integration and participation in his program of the peoples of the Greek East, especially of the Greek mainland and Asia Minor. Hadrian now invited them to become active members of the empire. By his lengthy travels and benefactions to the people of the region and by the creation of the Panhellenion, Hadrian attempted to create a second center of the Empire. Rome, in the West, was the first center; now a second one, in the East, would draw together the Greek people on both sides of the Aegean Sea. Thus he could accelerate the unification of the empire by focusing on its two most important elements, Romans and Greeks. Hadrian channeled his intentions in a number of ways, including the use of specific iconographical types on the coinage of his reign and religious language and themes in his interactions with the Greeks. In both cases it becomes evident that the Greeks not only understood his messages, but they also reacted in a positive way. -

Edc 370S – Fall 2019

ADVANCED METHODS ENGLISH/ LANGUAGE ARTS/ READING EDC 370S, FALL 2019 SZB 334 TUESDAYS 1-4 Instructor: Allison Skerrett Email: [email protected] Phone: (512).232.4883 Office Location and Hours: SZB 334A, by appointment Teaching Assistant: Randi Beth Brady Teaching Assistant/Field Supervisor: Lori Van Dike Email: [email protected] Office Hours: SZB 334D, by appointment Office Hours: SZB 334H, by appointment Email: [email protected] Phone: (478).250.5660 Phone: (281).705.3721 Course Overview & Objectives Welcome to your advanced methods course! This past summer you had your first opportunity to work with students while beginning to think about what it means to teach literacy in an “urban” classroom. This course will be a space for us to continue that work examining, reflecting on, and defining our teaching practice. This course was designed for you, members of the undergraduate University of Texas Urban Teachers secondary English certification program. It was built using several underlying principles: that teaching and learning have sociopolitical dimensions; that our work as educators is informed by theory, empirical research, and knowledge of our own practice; and that learning is social and recursive. Throughout the semester you will explore the theoretical background and practical applications of different approaches to teaching English Language Arts in a secondary context, including teaching reading. You will learn about, develop, implement, analyze, and revise curriculum and instruction that are informed by research, theory, and best practices for teaching language arts. Each week in class and in your field placement you will be asked to be an involved participant in your own learning: engaging in class discussions, pursuing your own inquiries about teaching, and reflecting on your experiences. -

The Roman Empire – Roman Coins Lesson 1

Year 4: The Roman Empire – Roman Coins Lesson 1 Duration 2 hours. Date: Planned by Katrina Gray for Two Temple Place, 2014 Main teaching Activities - Differentiation Plenary LO: To investigate who the Romans were and why they came Activities: Mixed Ability Groups. AFL: Who were the Romans? to Britain Cross curricular links: Geography, Numeracy, History Activity 1: AFL: Why did the Romans want to come to Britain? CT to introduce the topic of the Romans and elicit children’s prior Sort timeline flashcards into chronological order CT to refer back to the idea that one of the main reasons for knowledge: invasion was connected to wealth and money. Explain that Q Who were the Romans? After completion, discuss the events as a whole class to ensure over the next few lessons we shall be focusing on Roman Q What do you know about them already? that the children understand the vocabulary and events described money / coins. Q Where do they originate from? * Option to use CT to show children a map, children to locate Rome and Britain. http://www.schoolsliaison.org.uk/kids/preload.htm or RESOURCES Explain that the Romans invaded Britain. http://resources.woodlands-junior.kent.sch.uk/homework/romans.html Q What does the word ‘invade’ mean? for further information about the key dates and events involved in Websites: the Roman invasion. http://www.schoolsliaison.org.uk/kids/preload.htm To understand why they invaded Britain we must examine what http://www.sparklebox.co.uk/topic/past/roman-empire.html was happening in Britain before the invasion. -

Chinese Underground Banking and 'Daigou'

Chinese Underground Banking and ‘Daigou’ October 2019 NAC/NECC v1.0 Purpose This document has been compiled by the National Crime Agency’s National Assessment Centre from the latest information available to the NCA regarding the abuse of Chinese Underground Banking and ‘Daigou’ for money laundering purposes. It has been produced to provide supporting information for the application by financial investigators from any force or agency for Account Freezing Orders and other orders and warrants under the Proceeds of Crime Act 2002. It can also be used for any other related purpose. This document is not protectively marked. Executive Summary • The transfer of funds for personal purposes out of China by Chinese citizens is tightly regulated by the Chinese government, and in all but exceptional circumstances is limited to the equivalent of USD 50,000 per year. All such transactions, without exception, are required to be carried out through a foreign exchange account opened with a Chinese bank for the purpose. The regulations nevertheless provide an accessible, legitimate and auditable mechanism for Chinese citizens to transfer funds overseas. • Chinese citizens who, for their own reasons, choose not to use the legitimate route stipulated by the Chinese government for such transactions, frequently use a form of Informal Value Transfer System (IVTS) known as ‘Underground Banking’ to carry them out instead. Evidence suggests that this practice is widespread amongst the Chinese diaspora in the UK. • Evidence from successful money laundering prosecutions in the UK has shown that Chinese Underground Banking is abused for the purposes of laundering money derived from criminal offences, by utilising cash generated from crime in the UK to settle separate and unconnected inward Underground Banking remittances to Chinese citizens in the UK. -

Princeton/Stanford Working Papers in Classics

Princeton/Stanford Working Papers in Classics Coin quality, coin quantity, and coin value in early China and the Roman world Version 2.0 September 2010 Walter Scheidel Stanford University Abstract: In ancient China, early bronze ‘tool money’ came to be replaced by round bronze coins that were supplemented by uncoined gold and silver bullion, whereas in the Greco-Roman world, precious-metal coins dominated from the beginnings of coinage. Chinese currency is often interpreted in ‘nominalist’ terms, and although a ‘metallist’ perspective used be common among students of Greco-Roman coinage, putatively fiduciary elements of the Roman currency system are now receiving growing attention. I argue that both the intrinsic properties of coins and the volume of the money supply were the principal determinants of coin value and that fiduciary aspects must not be overrated. These principles apply regardless of whether precious-metal or base-metal currencies were dominant. © Walter Scheidel. [email protected] How was the valuation of ancient coins related to their quality and quantity? How did ancient economies respond to coin debasement and to sharp increases in the money supply relative to the number of goods and transactions? I argue that the same answer – that the result was a devaluation of the coinage in real terms, most commonly leading to price increases – applies to two ostensibly quite different monetary systems, those of early China and the Roman Empire. Coinage in Western and Eastern Eurasia In which ways did these systems differ? 1 In Western Eurasia coinage arose in the form of oblong and later round coins in the Greco-Lydian Aegean, made of electron and then mostly silver, perhaps as early as the late seventh century BCE. -

Lu Zhiqiang China Oceanwide

08 Investment.FIN.qxp_Layout 1 14/9/16 12:21 pm Page 81 Week in China China’s Tycoons Investment Lu Zhiqiang China Oceanwide Oceanwide Holdings, its Shenzhen-listed property unit, had a total asset value of Rmb118 billion in 2015. Hurun’s China Rich List He is the key ranked Lu as China’s 8th richest man in 2015 investor behind with a net worth of Rmb83 billlion. Minsheng Bank and Legend Guanxi Holdings A long-term ally of Liu Chuanzhi, who is known as the ‘godfather of Chinese entrepreneurs’, Oceanwide acquired a 29% stake in Legend Holdings (the parent firm of Lenovo) in 2009 from the Chinese Academy of Social Sciences for Rmb2.7 billion. The transaction was symbolic as it marked the dismantling of Legend’s SOE status. Lu and Liu also collaborated to establish the exclusive Taishan Club in 1993, an unofficial association of entrepreneurs named after the most famous mountain in Shandong. Born in Shandong province in 1951, Lu In fact, according to NetEase Finance, it was graduated from the elite Shanghai university during the Taishan Club’s inaugural meeting – Fudan. His first job was as a technician with hosted by Lu in Shandong – that the idea of the Shandong Weifang Diesel Engine Factory. setting up a non-SOE bank was hatched and the proposal was thereafter sent to Zhu Getting started Rongji. The result was the establishment of Lu left the state sector to become an China Minsheng Bank in 1996. entrepreneur and set up China Oceanwide. Initially it focused on education and training, Minsheng takeover? but when the government initiated housing Oceanwide was one of the 59 private sector reform in 1988, Lu moved into real estate. -

The Gallic Empire (260-274): Rome Breaks Apart

The Gallic Empire (260-274): Rome Breaks Apart Six Silver Coins Collection An empire fractures Roman chariots All coins in each set are protected in an archival capsule and beautifully displayed in a mahogany-like box. The box set is accompanied with a story card, certificate of authenticity, and a black gift box. By the middle of the third century, the Roman Empire began to show signs of collapse. A parade of emperors took the throne, mostly from the ranks of the military. Years of civil war and open revolt led to an erosion of territory. In the year 260, in a battle on the Eastern front, the emperor Valerian was taken prisoner by the hated Persians. He died in captivity, and his corpse was stuffed and hung on the wall of the palace of the Persian king. Valerian’s capture threw the already-fractured empire into complete disarray. His son and co-emperor, Gallienus, was unable to quell the unrest. Charismatic generals sought to consolidate their own power, but none was as powerful, or as ambitious, as Postumus. Born in an outpost of the Empire, of common stock, Postumus rose swiftly through the ranks, eventually commanding Roman forces “among the Celts”—a territory that included modern-day France, Belgium, Holland, and England. In the aftermath of Valerian’s abduction in 260, his soldiers proclaimed Postumus emperor. Thus was born the so-called Gallic Empire. After nine years of relative peace and prosperity, Postumus was murdered by his own troops, and the Gallic Empire, which had depended on the force of his personality, began to crumble. -

Tenarishydril Premium Connections Catalogue En 6 MB

Premium Connections Catalogue Table of contents 4 20 INTRODUCTION CONNECTIONS BY TECHNOLOGY TenarisHydril Wedge Series Integrated Tubular Solutions Wedge 563® Unparalleled Product Technology Wedge XP™ 2.0 Steel Grades Wedge 625® Dopeless® Technology Wedge 623® Reliable Manufacturing Quality Wedge 523® Wedge 521® Wedge 513® 13 Wedge 511® Application Guide Wedge 533® Connections Nomenclature Dimensional Range Blue® Series Blue® Blue® Max Blue® Heavy Wall Blue® Riser Large OD BlueDock® Connector Blue® Quick Seal ER™ TenarisXP® Series TXP® Buttress Legacy Series Legacy connections INTRODUCTION For information on other connections, visit www.tenaris.com PREMIUM CONNECTIONS CATALOGUE TenarisHydril 3 TenarisHydril TenarisHydril offers outstanding premium TenarisHydril premium connections are supplied connection design and technology worldwide. and supported by Tenaris, the leading manufac- With a comprehensive range of high performance turer and supplier of steel tubes and integrated products backed by an extensive global field tubular services to the world's energy industry. service network and licensed threading shops, we For further information please visit our website at develop solutions to meet the needs of ever more www.tenaris.com. demanding E&P environments. 4 Integrated Tubular Solutions Tenaris meets the evolving needs of the oil and gas industry with a commitment to unparalleled service, quality and innovative technology. Over the years, the oil and gas industry has moved Our TenarisHydril Blue® Series of connections from its onshore roots to more complex shallow are renowned for their outstanding performance water and deepwater operations, and on to uncon- in critical offshore and high pressure applications, ventional reserves. Operators seek not just reliable where fully tested gas-tight seals are required. -

Münzen Aus Dem Reich Der Mitte – Von Der Kaurischnecke Zum Käsch

Münzen aus dem Reich der Mitte – von der Kaurischnecke zum Käsch Um 1500 v. Chr. benutzte man in China Schneckengehäuse als Münzen; später wurden die Schnecken aus Knochen oder Kupfer nachgeahmt. Daneben zirkulierte Gerätegeld, zum Beispiel in Form von Messer- oder Spatenmünzen, aber auch runde Münzen waren in Gebrauch. 211 v. Chr. begann der erste chinesische Kaiser mit der Ausgabe von einheitlichen Reichsmünzen, aus denen sich schliesslich die Käschmünze entwickelte: eine runde Kupfermünze mit viereckigem Loch, die bis zum Ende der chinesischen Kaiserzeit im Jahr 1911 ausgegeben wurde. 1 von 21 www.sunflower.ch China, Shang-Dynastie, durchbohrte Cypraea moneta (Kauri) Denomination: Cypraea Moneta (Kauri) Prägeautorität: Prägeort: Prägejahr: -1500 Gewicht in Gramm: 0.9 Durchmesser in mm: 21.0 Material: Andere Eigentümer: Sunflower Foundation Kaurischnecken waren die langlebigste Währung aller Zeiten. In China wurden sie schon vor über 3000 Jahren als Geld benutzt und liefen, zusammen mit anderen Zahlungsmitteln, bis 1578 um. Die chinesische Schrift, die im 2. Jahrtausend v. Chr. entwickelt wurde, verwendet das Zeichen für Kauri noch heute in Wörtern wie Münze, Geld, Kaufen, Wert und ähnlichen. Das Zeichen ist auch Bestandteil der Inschrift auf vielen chinesischen Käschmünzen. Der venezianische Händler Marco Polo, der im späten 13. Jahrhundert während mehrerer Jahre in China lebte, überlieferte in seinen Reisebeschreibungen (Il Milione) einige Preise. Demnach bezahlte man damals in China für ein Huhn 5 Kauri, für vier Kilogramm Getreide 8 Kauri und für eine Kuh 320 Kauri. 2 von 21 www.sunflower.ch China, Zhou-Dynastie, Kauriimitation aus Knochen, ca. 700 v. Chr. Denomination: Kauriimitation Prägeautorität: Zhou-Dynastie Prägeort: Unbestimmt Prägejahr: -700 Gewicht in Gramm: 2.84 Durchmesser in mm: 28.0 Material: Andere Eigentümer: Sunflower Foundation Um dem Handel und dem täglichen Gebrauch zu genügen, brauchte man eine grosse Menge Kauris. -

Augustine on Manichaeism and Charisma

Religions 2012, 3, 808–816; doi:10.3390/rel3030808 OPEN ACCESS religions ISSN 2077-1444 www.mdpi.com/journal/religions Article Augustine on Manichaeism and Charisma Peter Iver Kaufman Jepson School, University of Richmond, Room 245, Jepson Hall, 28 Westhampton Way, Richmond, VA 23173, USA; E-Mail: [email protected] Received: 5 June 2012; in revised form: 28 July 2012 / Accepted: 1 August 2012 / Published: 3 September 2012 Abstract: Augustine was suspicious of charismatics‘ claims to superior righteousness, which supposedly authorized them to relay truths about creation and redemption. What follows finds the origins of that suspicion in his disenchantment with celebrities on whom Manichees relied, specialists whose impeccable behavior and intellectual virtuosity were taken as signs that they possessed insight into the meaning of Christianity‘s sacred texts. Augustine‘s struggles for self-identity and with his faith‘s intelligibility during the late 370s, 380s, and early 390s led him to prefer that his intermediaries between God and humanity be dead (martyred), rather than alive and charismatic. Keywords: arrogance; Augustine; charisma; esotericism; Faustus; Mani; Manichaeism; truth The Manichaean elite or elect adored publicity. Augustine wrote the first of his caustic treatises against them in 387, soon after he had been baptized in Milan and as he was planning passage back to Africa, where he was born, raised, and educated. Baptism marked his devotion to the emerging mainstream Christian orthodoxy and his disenchantment with the Manichees‘ increasingly marginalized Christian sect, in which, for nine or ten years, in North Africa and Italy, he listened to specialists—charismatic leaders and teachers.