No Slide Title

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Testimony of John Denniston Partner Kleiner Perkins Caufield & Byers Before the Senate Energy & Natural Resources Commit

TESTIMONY OF JOHN DENNISTON PARTNER KLEINER PERKINS CAUFIELD & BYERS BEFORE THE SENATE ENERGY & NATURAL RESOURCES COMMITTEE MARCH 7, 2007 Introduction Good morning, Chairman Bingaman, Ranking Member Domenici and Members of the Committee. My name is John Denniston and I am a Partner at the venture capital firm Kleiner Perkins Caufield & Byers. It’s my privilege to be here today and to have the opportunity to share my views on moving advanced energy technologies to the marketplace. Ensuring a sound energy future is one of the most urgent policy challenges facing our nation and indeed the global community, and I sincerely appreciate this Committee’s leadership in this arena. Along with the rest of America, venture capital and technology industry professionals – Republicans and Democrats alike -- are deeply concerned about the risks to our nation’s welfare posed by our energy dilemma. Specifically, this includes the looming climate crisis, our oil addiction, and the very real danger of losing our global competitive edge. Yet our industry is also in a unique position to recognize that each challenge presents dramatic new opportunities to build our economy, creating jobs and prosperity. Kleiner Perkins is a member of the National Venture Capital Association and a founding member of TechNet, a network of 200 CEOs of the nation’s leading technology companies. I serve on TechNet’s Green Technologies Task Force, which next week will release a detailed set of policy recommendations to drive the development and adoption of technologies we believe can help solve some of the world’s most pressing energy and environmental problems. -

Post-Pandemic Reflections: Future Mobility COVID-19’S Potential Impact on the New Mobility Ecosystem

THEMATIC INSIGHTS Post-Pandemic Reflections: Future Mobility COVID-19’s potential impact on the new mobility ecosystem msci.com msci.com 1 Contents 04 Mobility-as-a-Service and the COVID-19 shock 06 Growing Pains in the Future Mobility Market 16 Mobility Services: Expansion and Acceleration 18 COVID-19: A Catalyst for Autonomous Delivery? 2 msci.com msci.com 3 Future Mobility A growing database collated by Neckermann Strategic Advisors has over Mobility-as- 700 public and private companies involved with different elements of the autonomous Mobility-as-a-Service (MaaS) value chain. a-Service A list that doesn’t yet include all the producers of electric, two-wheeled and public transport that contribute to the full and the mobility ecosystem. In the 1910s, the automotive industry was COVID-19 shock vast, and the rising tide was lifting every boat, albeit not profitably. However, by the time the Roaring Twenties came to an end in Even prior to the COVID-19 crisis, we discussed in our first Thematic 1929, the number of US auto manufacturers Insight1 how the world might be in the midst of the largest transformation had already fallen to 44, only to consolidate in mobility since the advent of the automobile some 120 years ago. Will much further after the Great Depression. the current pandemic prove to be a system shock that accelerates the It is, of course, tempting to see a parallel demise of inflexible and unprofitable business models and acts as a to the last five years in mobility. Just prior catalyst for the growth of more digital and service-oriented businesses in to the COVID-19 crisis, there were initial the mobility space? How might industry-wide headwinds affect the new signs of stress in this tapestry of privately- business models and technologies at least in the short-term? funded companies in the Future Mobility New industries naturally go through a series of iterations before becoming ecosystem. -

Operaing the EPON Protocol Over Coaxial Distribuion Networks Call for Interest

Operang the EPON protocol over Coaxial Distribu&on Networks Call for Interest 08 November 2011 IEEE 802.3 Ethernet Working Group Atlanta, GA 1 Supporters Bill Powell Alcatel-Lucent Steve Carlson High Speed Design David Eckard Alcatel-Lucent Hesham ElBakoury Huawei Alan Brown Aurora Networks Liming Fang Huawei Dave Baran Aurora Networks David Piehler Neophotonics Edwin MalleIe Bright House Networks Amir Sheffer PMC-Sierra John Dickinson Bright House Networks Greg Bathrick PMC-Sierra Ed Boyd Broadcom ValenWn Ossman PMC-Sierra Howard Frazier Broadcom Alex Liu Qualcomm Lowell Lamb Broadcom Dylan Ko Qualcomm Mark Laubach Broadcom Steve Shellhammer Qualcomm Will Bliss Broadcom Mike Peters Sumitomo Electric Industries Robin Lavoie Cogeco Cable Inc. Yao Yong Technical Working CommiIee of China Radio & Ma SchmiI CableLabs TV Associaon Doug Jones Comcast Cable Bob Harris Time Warner Cable Jeff Finkelstein Cox Networks Kevin A. Noll Time Warner Cable John D’Ambrosia Dell Hu Baomin Wuhan Yangtze OpWcal Technologies Co.,Ltd. Zhou Zhen Fiberhome Telecommunicaon Ye Yonggang Wuhan Yangtze OpWcal Technologies Co.,Ltd. Technologies Zheng Zhi Wuhan Yangtze OpWcal Technologies Co.,Ltd. Boris Brun Harmonic Inc. Marek Hajduczenia ZTE Lior Assouline Harmonic Inc. Meiyan Zang ZTE David Warren HewleI-Packard Nevin R Jones ZTE 2 Objec&ves for This Mee&ng • To measure the interest in starWng a study group to develop a standards project proposal (a PAR and 5 Criteria) for: Operang the EPON protocol over Coaxial DistribuWon Networks • This meeWng does not: – Fully explore the problem – Debate strengths and weaknesses of soluWons – Choose any one soluWon – Create PAR or five criteria – Create a standard or specificaon 3 Agenda • IntroducWon • Market PotenWal • High Level Concept • Why Now? • Q&A • Straw Polls 4 The Brief History of EPON 2000 EPON Today.. -

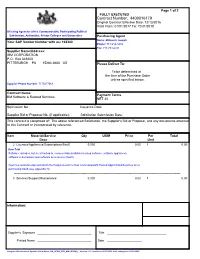

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

How Uber Won the Rideshare Wars and What Comes Next

2/18/2020 How Uber Won The Rideshare Wars and What Comes Next CUSTOMER EXPERIENCE | HOW UBER WON THE RIDESHARE WARS AND WHAT COMES NEXT How Uber Won The Rideshare Wars and What Comes Next How Uber won the first phase of the rideshare war and how cabs, competitors, and car companies are battling back. BY ELYSE DUPRE — AUGUST 29, 2016 VIEW GALLERY https://www.dmnews.com/customer-experience/article/13035536/how-uber-won-the-rideshare-wars-and-what-comes-next 1/18 2/18/2020 How Uber Won The Rideshare Wars and What Comes Next View Gallery In 2011, two University of Michigan alums Adrian Fortino and Jahan Khanna partnered with venture capitalist Sunil Paul to revolutionize how people got from point A to point B quickly without having to do much. The company was Sidecar, and the idea was simple: “We're going to replace your car with your iPhone,” Fortino explains. Sidecar did not lack competition. Around this time, the taxi industry was experimenting with new ways to make it easier for individuals to summon cars. And entrepreneurs, frustrated with wait times, imagined new ways to hire someone to drive them around. Multiple companies formed to solve this need, including one that is now considered a global powerhouse: Uber. By the time Sidecar went into beta testing in February 2012, Uber, or UberCab as it was originally known when it was founded in 2009, had raised at least $37.5 million at a $330 million post-money valuation, according to VentureBeat. Lyft followed shortly after when it went into beta in mid 2012, boasting more than $7 million in funding, according to TechCrunch's figures. -

Enterprise CRM Suites

Oracle Corporation et al v. SAP AG et al Doc. 844 Att. 14 EXHIBIT N Dockets.Justia.com August 29, 2008 | Updated: September 2, 2008 The Forrester Wave™: Enterprise CRM Suites, Q3 2008 by William Band for Business Process & Applications Professionals Making Leaders Successful Every Day ORCLX-PIN-000006_001 For Business Process & Applications Professionals Includes a Forrester Wave™ August 29, 2008 | Updated: September 2, 2008 The Forrester Wave™: Enterprise CRM Suites, Q3 2008 Buyers Face Difficult Choices In A Crowded Market by William Band with Sharyn C. Leaver, Pete Marston, Natalie L. Petouhoff, Ph.D., Elisse Gaynor, and Andrew Magarie EXECUTIVE SUMMARY Forrester evaluated leading enterprise CRM suite solutions against 516 criteria and found that with the latest releases of their solutions, Oracle’s Siebel and SAP maintain their status as Leaders with comprehensive functionality and much improved usability. Microsoft, salesforce.com, RightNow, and Oracle CRM On Demand have improved their credibility as enterprise-class solutions and have graduated into the Leaders group. The latter vendors all get high marks for ease-of-use and quick time-to-value. The Leaders are challenged by Strong Performers offering a diverse range of benefits. Oracle’s E-Business Suite CRM and PeopleSoft CRM are good options for their respective ERP customers looking for end-to-end integration. Chordiant, ciboodle, and Pegasystems offer business process management (BPM) strengths to help enterprises orchestrate complex customer-facing processes. Infor CRM Epiphany and Onyx CRM are working to regain market momentum through investments in product enhancements being made by their respective new corporate parents, Infor and Consona. -

Emerging Technologies for Academic Libraries in the Digital Age CHANDOS INFORMATION PROFESSIONAL SERIES

Emerging Technologies for Academic Libraries in the Digital Age CHANDOS INFORMATION PROFESSIONAL SERIES Series Editor: Ruth Rikowski (email: [email protected]) Chandos’ new series of books are aimed at the busy information professional. They have been specially commissioned to provide the reader with an authoritative view of current thinking. They are designed to provide easy-to-read and (most importantly) practical coverage of topics that are of interest to librarians and other information professionals. If you would like a full listing of current and forthcoming titles, please visit our web site www.chandospublishing.com or contact Hannah Grace-Williams on email [email protected] or telephone number +44 (0) 1993 848726. New authors: we are always pleased to receive ideas for new titles; if you would like to write a book for Chandos, please contact Dr Glyn Jones on email [email protected] or telephone number +44 (0) 1993 848726. Bulk orders: some organisations buy a number of copies of our books. If you are interested in doing this, we would be pleased to discuss a discount. Please contact Hannah Grace-Williams on email [email protected] or telephone number +44 (0) 1993 848726. Emerging Technologies for Academic Libraries in the Digital Age LILI LI Chandos Publishing Oxford · England Chandos Publishing (Oxford) Limited TBAC Business Centre Avenue 4 Station Lane Witney Oxford OX28 4BN UK Tel: +44 (0) 1993 848726 Fax: +44 (0) 1865 884448 E-mail: [email protected] www.chandospublishing.com First published in Great Britain in 2009 ISBN: 978 1 84334 320 2 (paperback) 978 1 84334 323 3 (hardback) 1 84334 320 7 (paperback) 1 84334 323 1 (hardback) © LiLi Li, 2009 British Library Cataloguing-in-Publication Data. -

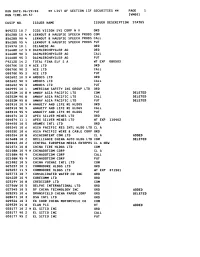

LIST of SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 Ivmool

RUN DATE:06/29/00 ** LIST OF SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 IVMOOl CUSIP NO. ISSUER NAME ISSUER DESCRIPTION STATUS B49233 10 7 ICOS VISION SYS CORP N V ORD B5628B 10 4 * LERNOUT & HAUSPIE SPEECH PRODS COM B5628B 90 4 LERNOUT & HAUSPIE SPEECH PRODS CALL B5628B 95 4 LERNOUT 8 HAUSPIE SPEECH PRODS PUT D1497A 10 1 CELANESE AG ORD D1668R 12 3 * DAIMLERCHRYSLER AG ORD D1668R 90 3 DAIMLERCHRYSLER AG CALL D1668R 95 3 DAIMLERCHRYSLER AG PUT F9212D 14 2 TOTAL FINA ELF S A WT EXP 080503 G0070K 10 3 * ACE LTD ORD G0070K 90 3 ACE LTD CALL G0070K 95 3 ACE LTD PUT GO2602 10 3 * AMDOCS LTD ORD GO2602 90 3 AMDOCS LTD CALL GO2602 95 3 AMDOCS LTD PUT GO2995 10 1 AMERICAN SAFETY INS GROUP LTD ORD G0352M 10 8 * AMWAY ASIA PACIFIC LTD COM DELETED G0352M 90 8 AMWAY ASIA PACIFIC LTD CALL DELETED G0352M 95 8 AMWAY ASIA PACIFIC LTD PUT DELETED GO3910 10 9 * ANNUITY AND LIFE RE HLDGS ORD GO3910 90 9 ANNUITY AND LIFE RE HLDGS CALL GO3910 95 9 ANNUITY AND LIFE RE HLDGS PUT GO4074 10 3 APEX SILVER MINES LTD ORD GO4074 11 1 APEX SILVER MINES LTD WT EXP 110402 GO4450 10 5 ARAMEX INTL LTD ORD GO5345 10 6 ASIA PACIFIC RES INTL HLDG LTD CL A G0535E 10 6 ASIA PACIFIC WIRE & CABLE CORP ORD GO5354 10 8 ASIACONTENT COM LTD CL A ADDED G1368B 10 2 BRILLIANCE CHINA AUTO HLDG LTD COM DELETED 620045 20 2 CENTRAL EUROPEAN MEDIA ENTRPRS CL A NEW G2107X 10 8 CHINA TIRE HLDGS LTD COM G2108N 10 9 * CHINADOTCOM CORP CL A G2108N 90 9 CHINADOTCOM CORP CALL G2lO8N 95 9 CHINADOTCOM CORP PUT 621082 10 5 CHINA YUCHAI INTL LTD COM 623257 10 1 COMMODORE HLDGS LTD ORD 623257 11 -

ZILLOW GROUP, INC. (Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A (Rule 14a-101) INFORMATION REQUIRED IN PROXY STATEMENT SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material under § 240.14a-12 ZILLOW GROUP, INC. (Name of Registrant as Specified in its Charter) N/A (Name of Person(s) Filing Proxy Statement, if Other Than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. -

PDF: 300 Pages, 5.2 MB

The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: Global Reach Emerging Ties Between the San Francisco Bay Area and India A Bay Area Council Economic Institute Report by R. Sean Randolph President & CEO Bay Area Council Economic Institute and Niels Erich Global Business/Transportation Consulting November 2009 Bay Area Council Economic Institute 201 California Street, Suite 1450 San Francisco, CA 94111 (415) 981-7117 (415) 981-6408 Fax [email protected] www.bayareaeconomy.org Rangoli Designs Note The geometric drawings used in the pages of this report, as decorations at the beginnings of paragraphs and repeated in side panels, are grayscale examples of rangoli, an Indian folk art. Traditional rangoli designs are often created on the ground in front of the entrances to homes, using finely ground powders in vivid colors. This ancient art form is believed to have originated from the Indian state of Maharashtra, and it is known by different names, such as kolam or aripana, in other states. Rangoli de- signs are considered to be symbols of good luck and welcome, and are created, usually by women, for special occasions such as festivals (espe- cially Diwali), marriages, and birth ceremonies. Cover Note The cover photo collage depicts the view through a “doorway” defined by the section of a carved doorframe from a Hindu temple that appears on the left. -

1 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: September 30, 2000 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries Institutional Investment Manager Filing this Report: Name: AMERICAN INTERNATIONAL GROUP, INC. Address: 70 Pine Street New York, New York 10270 Form 13F File Number: 28-219 The Institutional Investment Manager filing this report and the person by whom it is signed represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Edward E. Matthews Title: Vice Chairman -- Investments and Financial Services Phone: (212) 770-7000 Signature, Place, and Date of Signing: /s/ Edward E. Matthews New York, New York November 14, 2000 - ------------------------------- ------------------------ ----------------- (Signature) (City, State) (Date) Report Type (Check only one.): [X] 13F HOLDINGS REPORT. (Check if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check if no holdings reported are in this report, and all holdings are reported in this report and a portion are reported by other reporting manager(s).) [ ] 13F COMBINATION REPORT. (Check