Testimony of John Denniston Partner Kleiner Perkins Caufield & Byers Before the Senate Energy & Natural Resources Commit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post-Pandemic Reflections: Future Mobility COVID-19’S Potential Impact on the New Mobility Ecosystem

THEMATIC INSIGHTS Post-Pandemic Reflections: Future Mobility COVID-19’s potential impact on the new mobility ecosystem msci.com msci.com 1 Contents 04 Mobility-as-a-Service and the COVID-19 shock 06 Growing Pains in the Future Mobility Market 16 Mobility Services: Expansion and Acceleration 18 COVID-19: A Catalyst for Autonomous Delivery? 2 msci.com msci.com 3 Future Mobility A growing database collated by Neckermann Strategic Advisors has over Mobility-as- 700 public and private companies involved with different elements of the autonomous Mobility-as-a-Service (MaaS) value chain. a-Service A list that doesn’t yet include all the producers of electric, two-wheeled and public transport that contribute to the full and the mobility ecosystem. In the 1910s, the automotive industry was COVID-19 shock vast, and the rising tide was lifting every boat, albeit not profitably. However, by the time the Roaring Twenties came to an end in Even prior to the COVID-19 crisis, we discussed in our first Thematic 1929, the number of US auto manufacturers Insight1 how the world might be in the midst of the largest transformation had already fallen to 44, only to consolidate in mobility since the advent of the automobile some 120 years ago. Will much further after the Great Depression. the current pandemic prove to be a system shock that accelerates the It is, of course, tempting to see a parallel demise of inflexible and unprofitable business models and acts as a to the last five years in mobility. Just prior catalyst for the growth of more digital and service-oriented businesses in to the COVID-19 crisis, there were initial the mobility space? How might industry-wide headwinds affect the new signs of stress in this tapestry of privately- business models and technologies at least in the short-term? funded companies in the Future Mobility New industries naturally go through a series of iterations before becoming ecosystem. -

How Uber Won the Rideshare Wars and What Comes Next

2/18/2020 How Uber Won The Rideshare Wars and What Comes Next CUSTOMER EXPERIENCE | HOW UBER WON THE RIDESHARE WARS AND WHAT COMES NEXT How Uber Won The Rideshare Wars and What Comes Next How Uber won the first phase of the rideshare war and how cabs, competitors, and car companies are battling back. BY ELYSE DUPRE — AUGUST 29, 2016 VIEW GALLERY https://www.dmnews.com/customer-experience/article/13035536/how-uber-won-the-rideshare-wars-and-what-comes-next 1/18 2/18/2020 How Uber Won The Rideshare Wars and What Comes Next View Gallery In 2011, two University of Michigan alums Adrian Fortino and Jahan Khanna partnered with venture capitalist Sunil Paul to revolutionize how people got from point A to point B quickly without having to do much. The company was Sidecar, and the idea was simple: “We're going to replace your car with your iPhone,” Fortino explains. Sidecar did not lack competition. Around this time, the taxi industry was experimenting with new ways to make it easier for individuals to summon cars. And entrepreneurs, frustrated with wait times, imagined new ways to hire someone to drive them around. Multiple companies formed to solve this need, including one that is now considered a global powerhouse: Uber. By the time Sidecar went into beta testing in February 2012, Uber, or UberCab as it was originally known when it was founded in 2009, had raised at least $37.5 million at a $330 million post-money valuation, according to VentureBeat. Lyft followed shortly after when it went into beta in mid 2012, boasting more than $7 million in funding, according to TechCrunch's figures. -

Enterprise Tech 30—The 2021 List

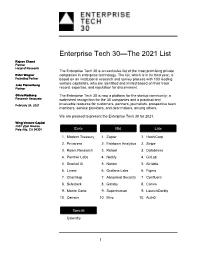

Enterprise Tech 30—The 2021 List Rajeev Chand Partner Head of Research The Enterprise Tech 30 is an exclusive list of the most promising private Peter Wagner companies in enterprise technology. The list, which is in its third year, is Founding Partner based on an institutional research and survey process with 103 leading venture capitalists, who are identified and invited based on their track Jake Flomenberg Partner record, expertise, and reputation for discernment. Olivia Rodberg The Enterprise Tech 30 is now a platform for the startup community: a Research Associate watershed recognition for the 30 companies and a practical and February 24, 2021 invaluable resource for customers, partners, journalists, prospective team members, service providers, and deal makers, among others. We are pleased to present the Enterprise Tech 30 for 2021. Wing Venture Capital 480 Lytton Avenue Palo Alto, CA 94301 Early Mid Late 1. Modern Treasury 1. Zapier 1. HashiCorp 2. Privacera 2. Fishtown Analytics 2. Stripe 3. Roam Research 3. Retool 3. Databricks 4. Panther Labs 4. Netlify 4. GitLab 5. Snorkel AI 5. Notion 5. Airtable 6. Linear 6. Grafana Labs 6. Figma 7. ChartHop 7. Abnormal Security 7. Confluent 8. Substack 8. Gatsby 8. Canva 9. Monte Carlo 9. Superhuman 9. LaunchDarkly 10. Census 10. Miro 10. Auth0 Special Calendly 1 2021 The Curious Case of Calendly This year’s Enterprise Tech 30 has 31 companies rather than 30 due to the “curious case” of Calendly. Calendly, a meeting scheduling company, was categorized as Early-Stage when the ET30 voting process started on January 11 as the company had raised $550,000. -

Perspectives on the Ridesourcing Revolution: Surveying Individual Attitudes Toward Uber and Lyft to Inform Urban Transportation Policymaking

Perspectives on the Ridesourcing Revolution: Surveying individual attitudes toward Uber and Lyft to inform urban transportation policymaking By Margo Dawes Bachelor of Science in Civil Engineering and Planning Massachusetts Institute of Technology Cambridge, MA (2015) Submitted to the Department of Urban Studies and Planning in partial fulfillment of the requirements for the degree of Master in City Planning at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2016 © 2016 Margo Dawes. All Rights Reserved The author hereby grants to MIT the permission to reproduce and to distribute publicly paper and electronic copies of the thesis document in whole or in part in any medium now known or hereafter created. Author________________________________________________________________________ Department of Urban Studies and Planning Certified by____________________________________________________________________ Assistant Professor Jinhua Zhao, Ph.D. Department of Urban Studies and Planning Thesis Supervisor Accepted by___________________________________________________________________ Associate Professor P. Christopher Zegras Chair, MCP Committee Department of Urban Studies and Planning 2 Perspectives on the Ridesourcing Revolution: Surveying individual attitudes toward Uber and Lyft to inform urban transportation policymaking By Margo Dawes Submitted to the Department of Urban Studies and Planning on May 19, 2016, in partial fulfillment of the requirements for the degree of Master in City Planning Abstract Media coverage of ridesourcing services such as Uber and Lyft has described a rivalry between new technology and the established taxi industry. Individual users and non-users of ridesourcing, however, may have more nuanced perspectives, but policymakers have little guidance on how to best represent these interests. This thesis uses a standardized questionnaire distributed across the United States by an online survey company to understand individual attitudes toward Uber, Lyft, and ridesourcing technology as a whole. -

Advanced Transportation Market Update

Advanced Transportation Market Update September 2019 Electric Mobility-as- Autonomous Data & Trucking & Vehicles a-Service Infrastructure Analytics Logistics About Greentech Capital Advisors Our mission is to empower companies and investors who are creating a more efficient and sustainable global infrastructure. We are purpose-built to ensure that our clients achieve success. We have deeply experienced bankers who are sector experts and understand our clients' industries and needs. We reach a vast global network of buyers, growth companies, asset owners and investors, and thereby provide clients with more ways to succeed through a deeper relationship network. We have directly relevant transaction experience which enables us to find creative structures and solutions to close transactions. We are an expert team of 75 professionals working seamlessly on our clients' behalf in New York, Zurich and San Francisco and through a strategic partnership in Japan. Our team of experienced bankers provides conflict-free advice and thoughtful, innovative solutions. Greentech Capital Advisors / 1 Advanced Transportation Market Update September 2019 News Selected Business > Amazon announced plans to order 100,000 electric delivery trucks from Rivian, a Developments developer of electric SUVs and pickup trucks, and deploy them by 2024 (Verge) > Canoo, a developer of EVs, unveiled its first electric vehicle with Level 2 AV technology; it will only be offered under a monthly subscription (Electrek) > ChargePoint, a developer of EV charging solutions, released -

Advanced Transportation Market Update

Advanced Transportation Market Update February 2020 Electric Mobility-as- Autonomous Data & Trucking & Vehicles a-Service Infrastructure Analytics Logistics About Greentech Capital Advisors Our mission is to empower companies and investors who are creating a more efficient and sustainable global infrastructure. We are purpose-built to ensure that our clients achieve success. We have deeply experienced bankers who are sector experts and understand our clients' industries and needs. We reach a vast global network of buyers, growth companies, asset owners and investors, and thereby provide clients with more ways to succeed through a deeper relationship network. We have directly relevant transaction experience which enables us to find creative structures and solutions to close transactions. We are an expert team of 75 professionals working seamlessly on our clients' behalf in New York, Zurich and San Francisco. Greentech Capital Advisors / 1 Advanced Transportation Market Update February 2020 News Selected Business > Apple announced a new feature enabling iPhones to serve as car keys (9to5Mac) Developments > Bird announced the launch of Bird Pay, a QR-based payment system that facilitates the purchase of items from participating local businesses (TechCrunch) > Cartken, an autonomous delivery startup still in stealth mode, was recently launched by a team spun out from Google’s failed Bookbot project (TechCrunch) > Cruise received permission from the California Public Utilities Commission to start Greentech’s Take: driving passengers in its autonomous Chevrolet Bolt (VentureBeat) > Legacy OEMs are now > Daimler announced plans to develop chargers for its all-electric trucks (Press Release) racing to bring EVs to market as consumer > Ford announced plans to bring eight EV models to market in 2020 (TechCrunch) and government > Jaguar Land Rover introduced an electric urban vehicle concept resembling a shuttle demand shifts towards car, with plans for a mobility service pilot in Coventry, U.K. -

No Slide Title

Technology, Telecom & Digital Media Industry Update January 2012 Member FINRA/SIPC www.harriswilliams.com Table of Contents Technology, Telecom & Digital Media What We've Been Reading…………………………………………………………………………………………1 Recent HW&Co. TTDM Article……………………………………………………………………………………………2 Bellwethers……………………………………………………………………………………………3 TTDM Public Market Trading Statistics………………………………………………………………………..…………………..4 Recent TTDM M&A Activity…………………………………………………………………………………………….5 Recent U.S. TTDM Initial Public Offerings………………………………………………………………………….………………...………..6 Public and M&A Market Overview by Sector Data and Information Services………………………………………………………………..…………..7 Financial Technology…………………………………………………………………………9 Internet & Digital Media……………………………………………………..…………………..11 IT and Tech-Enabled Services………………………………………………………………..14 Software – Application…………………………………………………….…………………..16 Software – Infrastructure……………………………………………………..…………………..19 Software – SaaS……………………………………………………………………………………………………..21 Tech Hardware……………………………………………………………………..…………………..23 Telecom………………………………………………………………………………………………..26 Selected HW&Co. TTDM Transactions…………………………………………………………………………………………..29 TTDM Group Overview and Disclosures…………………………………………………………………………………………..30 What We’ve Been Reading Tech M&A Spending Increases 17% in 2011 as Number of Transactions Hits a Five-Year High MarketWatch 1/05/2012 Technology acquirers increased M&A spending for the second year in a row in 2011, driving the total number of technology deals to its highest level since 2006. Acquirers spent $219 billion -

Data for the People

DATA FOR THE PEOPLE 9780465044696-text.indd 1 11/18/16 1:21 PM ALSO BY ANDREAS WEIGEND Time Series Prediction Computational Finance Decision Technologies for Financial Engineering Neural Networks in Financial Engineering 9780465044696-text.indd 2 11/18/16 1:21 PM DATA FOR THE PEOPLE How to Make Our Post-Privacy Economy Work for You ANDREAS WEIGEND New York 9780465044696-text.indd 3 11/18/16 1:21 PM Copyright © 2017 by Andreas Weigend Published in the United States by Basic Books, an imprint of Perseus Books, LLC, a subsidiary of Hachette Book Group, Inc. All rights reserved. Printed in the United States of America. No part of this book may be repro- duced in any manner whatsoever without written permission except in the case of brief quota- tions embodied in critical articles and reviews. For information, contact Basic Books, 250 West 57th Street, New York, NY 10107. Books published by Basic Books are available at special discounts for bulk purchases in the United States by corporations, institutions, and other organizations. For more information, please contact the Special Markets Department at Perseus Books, 2300 Chestnut Street, Suite 200, Philadelphia, PA 19103, or call (800) 810-4145, ext. 5000, or email special.markets@ perseusbooks.com. A CIP catalog record for this book is available from the Library of Congress. ISBN: 978-0-465-04469-6 (hardcover) ISBN: 978-0-465-09653-4 (e-book) 10 9 8 7 6 5 4 3 2 1 9780465044696-text.indd 4 11/18/16 1:21 PM To p., f., and s. -

October 2019 Advanced Transportation Monthly Update

Advanced Transportation Market Update October 2019 Electric Mobility-as- Autonomous Data & Trucking & Vehicles a-Service Infrastructure Analytics Logistics About Greentech Capital Advisors Our mission is to empower companies and investors who are creating a more efficient and sustainable global infrastructure. We are purpose-built to ensure that our clients achieve success. We have deeply experienced bankers who are sector experts and understand our clients' industries and needs. We reach a vast global network of buyers, growth companies, asset owners and investors, and thereby provide clients with more ways to succeed through a deeper relationship network. We have directly relevant transaction experience which enables us to find creative structures and solutions to close transactions. We are an expert team of 75 professionals working seamlessly on our clients' behalf in New York, Zurich and San Francisco and through a strategic partnership in Japan. Our team of experienced bankers provides conflict-free advice and thoughtful, innovative solutions. Greentech Capital Advisors / 1 Advanced Transportation Market Update October 2019 News Selected Business > Bosch announced a new silicone carbide semiconductor to be used in EV powertrains Developments with increased efficiency that will help boost a car’s driving range by 6% (CNET) > DiDi Mobility Japan, a JV between Didi Chuxing and Softbank, announced plans to accelerate its expansion to 20 cities in Japan by the end of 2019 (New Mobility) > Dyson announced plans to abandon its EV development project, which employed 600 people and was funded by the company with $2.7bn (Electrek) > General Motors downgraded 2019 earnings by ~$3bn due to the impact of the 40- day strike at its U.S. -

Ihuman Neural Interfaces Report

iHuman Blurring lines between mind and machine PERSPECTIVE Emerging technologies As science expands our understanding of the world it can lead to the emergence of new technologies. These can bring huge benefits, but also challenges, as they change society’s relationship with the world. Scientists, developers and wider society must ensure that we maximise the benefits from new technologies while minimising these challenges. The Royal Society has established an Emerging Technologies Working Party to examine such developments and create perspectives. Neural interfaces Neural interfaces, broadly defined, are devices that interact with the nervous system of an individual. More specifically, the term is frequently used to describe electronic devices that are placed on the outside or inside of the brain or other components of the central and peripheral nervous system, such as nerves and links between nerves and muscles, to record or stimulate activity – or both. Interfaces placed inside the brain or body are known as internal, invasive or implanted technologies, as opposed to external, non- invasive or wearable devices. The Royal Society expects that neural interface technologies will continue to raise profound ethical, political, social and commercial questions that should be addressed as soon as possible to create mechanisms to approve, regulate or control the technologies as they develop, as well as managing the impact they may have on society. Supplement materials and references are available online at royalsociety.org/ihuman-perspective PERSPECTIVE – iHuman 3 iHuman: blurring lines between mind and machine Issued: September 2019 DES6094 ISBN: 978-1-78252-420-5 © The Royal Society The text of this work is licensed under the terms of the Creative Commons Attribution License which permits unrestricted use, provided the original author and source are credited. -

2021 Success Stories | Rice Business Plan Competition 101 Edu AC

2021 Success Stories | Rice Business Plan Competition 101 Edu Carnegie Mellon University | 2017 | www.101edu.co 101 is a venture-backed startup that is transforming the college STEM education with a next- generation active learning platform that promotes student engagement and improves student outcomes. Their first product for chemistry, Chem101, has quickly grown from 8 to over 200 higher ed institutions in the span of the past two years. Their unique approach focuses on elegant, discipline-specific assessment tools, such as molecular structure drawing, that triumph over generic multiple-choice tools and outdated online homework. The company was the winner of Inc. magazine's 2017 Coolest College Startup and the Student Startup Madness 2017 @ SXSW Interactive competitions. They won third place at the McGinnis Venture Competition 2017 @ Carnegie Mellon University. 101 was featured by CNBC, Inc., Cheddar, Royal Society of Chemistry, and Edtech Digest. They are based in New York City. AC Biode The University of Cambridge | 2019 | www.acbiode.com AC Biode is developing the world's first-ever AC (Alternating Current) battery by "Biode", which has both the characteristics of Anode and Cathode. With offices in Tokyo, Japan and Cambridge, England, the company has won a number of competitions in the past 12 months, including the Monozukuri Hardware Cup 2020, Tech Briefs' Create the Future, and the Mitaka Business Plan Competition. AcceleDent Formerly OrthoAccel Technologies | University of Illinois at Chicago | 2006 | www.acceledent.com Based in Houston, AcceleDent is a privately owned medical device company developing, manufacturing and marketing products to enhance dental care and orthodontic treatment. AcceleDent is the first FDA-cleared clinical approach to safely accelerate orthodontic tooth movement by applying gentle micropulses (SoftPulse Technology) as a complement to existing orthodontic treatment. -

Advanced Transportation Market Update

Advanced Transportation Market Update January 2020 Electric Mobility-as- Autonomous Data & Trucking & Vehicles a-Service Infrastructure Analytics Logistics About Greentech Capital Advisors Our mission is to empower companies and investors who are creating a more efficient and sustainable global infrastructure. We are purpose-built to ensure that our clients achieve success. We have deeply experienced bankers who are sector experts and understand our clients' industries and needs. We reach a vast global network of buyers, growth companies, asset owners and investors, and thereby provide clients with more ways to succeed through a deeper relationship network. We have directly relevant transaction experience which enables us to find creative structures and solutions to close transactions. We are an expert team of 75 professionals working seamlessly on our clients' behalf in New York, Zurich and San Francisco. Greentech Capital Advisors / 1 Advanced Transportation Market Update January 2020 News Selected Business > Ehang, a manufacturer of autonomous aerial vehicles, received FAA approval to fly in Developments the U.S. and delivered 40 aircrafts to paying customers (TechCrunch) > Ford approved using hydrotreated vegetable oil as fuel for its vans (Press Release) Greentech’s Take: > GM announced a $2.2bn plan to retrofit its Detroit-Hamtramck plant for the mass U.S. OEMs, historically production of autonomous and electric vehicles (The Verge) reluctant to embrace EVs, > GM announced plans to debut an all-electric Hummer branded vehicle (NPR)