Policy Note on Co-Operation Department

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Unclaimed Dividend As on March 31, 2014 For

LIST OF UNCLAIMED DIVIDEND AS ON MARCH 31, 2014 FOR FINANCIAL YEAR 2006-07 DPID CO_FOLIO NAME LOCATION PIN BANK_ACC BANK_NM BEN_POS AMOUNT DIV_CAT MICR WARNO 35 KRISHNA SAHAI 600 450.00 3 42 17023 42 VINOD MALHOTRA 200 150.00 3 44 17024 81 NARENDRA GUPTA 208002 1000 750.00 3 62 17026 IN300239 11928248 RAYAMARAKKAR VEETTIL MOHAMMED ABDUL KADER 081010100345101 UTI BANK LTD 500 375.00 5 65 6337 IN303028 52416976 LAKSHMI SUNDAR CANADA M2H2K4 0 602601251547 I C I C I BANK 500 375.00 5 66 16691 IN303028 53312700 RAJIV KUMAR WADHWA 0 032601075085 I C I C I BANK 160 120.00 5 67 16773 IN303028 53152064 IPTHIKAR AHAMED KSA 11461 000401800418 I C I C I BANK 100 75.00 5 69 16765 IN302679 33533755 DIWAKAR KESHAV KAMATH CANADA-L5B4P5 111111 NRO020901075271 ICICI BANK LTD 104 78.00 5 73 15273 IN302902 41446558 KAMATH JAHANARA DIWAKAR CANADA-L5B4P5 111111 NRO020901075645 ICICI BANK LTD 104 78.00 5 74 15818 IN303028 50981646 STANLY JOHN 111111 004601076690 I C I C I BANK 1000 750.00 5 76 16549 IN300484 12487732 VASANT CHHEDA 111111 064010100122504 AXIS BANK LTD 10000 7500.00 5 78 8114 IN302902 41368936 MATSYA RAJ SINGH KUWAIT-913119 111111 628101076232 I C I C I BANK 100 75.00 5 79 15806 IN301549 16866066 SATISH GANGWANI 400832 0011060006675 HDFC BANK LTD TULSIANI 1300 975.00 5 80 12307 IN300888 14561256 SURBHI AGRAWAL MALAYSIA 504700 4034317 SYNDICATE BANK 2600 1950.00 5 81 9833 IN301549 18385836 PADMAJA UPPALAPATI SOUTH AFRICA 999999 0041060014403 HDFC BANK LTD ITC CENTRE 200 150.00 5 82 12420 IN303028 51253550 ISMAIL MOHAMED GHOUSE 999999 000401473103 -

Current Affairs

CURRENT AFFAIRS Chapter 1 International and National Affairs 1 2 Financial Affairs 46 3 Political Affairs 58 4 Legal and Other Affairs 75 Lesson 1 INTERNATIONAL AND NATIONAL AFFAIRS 1 2 Current Affairs INTERNATIONAL MONETARY FUND The International Monetary Fund (IMF) is an organization of 189 countries, working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty around the world. Created in 1945, the IMF is governed by and accountable to the 189 countries that make up its near-global membership. The IMF's primary purpose is to ensure the stability of the international monetary system—the system of exchange rates and international payments that enables countries (and their citizens) to transact with each other. The Fund's mandate was updated in 2012 to include all macroeconomic and financial sector issues that bear on global stability. Fast Facts • Membership : 189 countries • Headquarters : Washington, D.C. • Executive Board : 24 Directors each representing a single country or groups of countries • The largest borrowers : Argentina, Ukraine, Greece, Egypt • The largest precautionary loans : Mexico, Colombia, Morocco Primary aims of IMF to: • Promote international monetary cooperation; • Facilitate the expansion and balanced growth of international trade; • Promote exchange stability; • Assist in the establishment of a multilateral system of payments; and • Make resources available (with adequate safeguards) to members experiencing balance-of- payments difficulties. Current Affairs 3 IMF in News Economic recovery for India in 2020-21: IMF The International Monetary Fund, which sharply cut India's growth rate, has projected a recovery in 2020-21, as per the statement of IMF’s Chief Economist Gita Gopinath during the news conference in Davos for the release of the World Economic Outlook (WEO) update on January 20, 2020. -

Government of India Ministry of Commerce & Industry Department

Government of India Ministry of Commerce & Industry Department of Commerce Directorate General of Foreign Trade Udyog Bhawan, New Delhi Dated 09. 07. 2015 Trade Notice No. 07/2015 To 1. All IEC Holders 2. All EPCs / All Chambers of Trade and Industries 3. FIEO/ASSOCHAM/CII 4. All RA’s of DGFT Subject: Operationalisation of online payments through debit / credit cards. In keeping with the Digital India vision of Hon'ble Prime Minister, and taking yet another crucial step towards paperless, online functioning in 24x7 environment, Directorate General of Foreign Trade has launched the facility of online payment of application fees through Credit/Debit cards and electronic fund transfer from 53 Banks (List annexed). 2. As a measure of Trade Facilitation and Ease of Doing Business, DGFT has already operationalised the facility of Online filing of various applications by the exporters/importers under the Foreign Trade Policy (2015-20). Early this year, DGFT also operationalised the facility of online submission of applications for issue of online Importer Exporter Code in digital format or e-IEC for exporters/importers. Now with the online payment facility being available from 53 banks, as well as through Credit and Debit cards, it would be possible to not only apply online for e-IEC and benefits under various schemes under Foreign Trade Policy but also make online payment of required application fee. 3. The charges applicable for using internet banking, debit/credit cards will be as follows: Transaction Visa / Master Card Credit card transaction: Processing 1.45% of payment amount per transaction. Charges Visa / Master Card/Rupay Debit Card transactions: For transactions upto Rs.2000/- : 0.75% of payment amount per transaction. -

Lending Policies of Dindigul District Central Co-Operative Bank Limited in Tamilnadu, India - a View N

International Journal of Research in Management, Economics & Commerce (Impact Factor: 4.604, ISSN 2250-057X, Volume 5 Issue 3, March 2015) Website: www.indusedu.org LENDING POLICIES OF DINDIGUL DISTRICT CENTRAL CO-OPERATIVE BANK LIMITED IN TAMILNADU, INDIA - A VIEW N. Selvaraj Assistant Professor of Commerce, Saraswathi Narayanan College, Madurai, Tamilnadu, India ABSTRACT Agriculture occupies a dominant position in the Indian economy. The well being of the people of India largely depends on the progress of agriculture. The co-operative credit has been recognised as the hope of the farmers to provide the basis of prosperity and the opportunity to meet the demand for funds. In the absence of adequate financial help, the farmers and agricultural labours are the ready victims of money lenders and indigenous bankers who charge exorbitant rates of interest. The Co-operative Banks are institutions established with the objectives to facilitate rural credit and to promote thrift and self help among the economically weaker sections of the society. So it is suggested to utilize the resources in more effective manner and also have a continuous profit planning to increase its profitability. To reduce overdues a large number of field staff is to be engaged for collection of dues. Keyword: co-operative credit, overdue, Co-efficient of variation, Co-operative Banks and lending. E-mail id:- [email protected] Page 1 International Journal of Research in Management, Economics & Commerce (Impact Factor: 4.604, ISSN 2250-057X, Volume 5 Issue 3, March 2015) Website: www.indusedu.org INTRODUCTION “Co-operative movement is one of the most fruitful ways of enlisting public co-operation on a mass scale in our planning and reconstruction activity” V.V. -

Cmdrfdonation.Pdf

Reminiscences on implementation from the war-room – The donation platform for Chief Minister’s Distress Relief Fund i FOREWORD The Chief Ministers Distress Relief Fund (CMDRF) is a unique e-governance application developed by Centre for Development of Imaging Technology (C-DIT) as a part of the Chief Ministers Office (CMO) Suite. This is eventually envisaged as an integrated monitoring and decision support tool for innovative policy interventions. The donation portal was developed a sequel to the CMO suite in the context of the August’18 natural calamity and has contributed substantively to the efforts towards rebuilding Kerala. The effort was unique in that it could bring together several partner banks, partner technology companies, start-ups, and individuals many of whom worked pro-bono. The solution had withstood tough weather and has shown its metal. I am happy that the endeavour has been systematically documented so that the product could be evaluated and further improved. M Sivasankar IAS Director, C-DIT Centre for Development and Imaging Technology (C-DIT) V 7.0 Reminiscences on implementation from the war-room – The donation platform for Chief Minister’s Distress Relief Fund ii Centre for Development and Imaging Technology (C-DIT) V 7.0 Reminiscences on implementation from the war-room – The donation platform for Chief Minister’s Distress Relief Fund iii ACKNOWLEDGEMENT The Finance Department Government of Kerala had entrusted the responsibility of developing a donation portal for the Chief Minister’s Distress Relief Fund on 11 August 2018. The donation portal is the outcome of a systematic effort by C-DIT during the last two months. -

Essel Propac Limited List of Unpaid Dividend 2018-19

ESSEL PROPAC LIMITED LIST OF UNPAID DIVIDEND 2018-19 Details of shareholders whose unclaimed dividend declared on 26 June 2019 is transferred to Unpaid Dividend Account of the Company Yes Bank Limited - Unpaid Dividend Account No. 000166400001496 SR # FOLIO_DPID_CLID No. BENEF_DESCRIPTION INSTRUMENT_ INST_NMBR INST_DATE INSTRUCTION_RE ADD1 ADD2 ADD3 ADD4 PIN AMNT FERENCE_NO 1 IN30048420060241 A RAMAR-914010030475349-AXIS BANK LTD 5.00 854753 7/8/2019 N33922 3198, CHIPPIPARAI, SATTUR TK VIRUDHUNAGAR DT, VIRUDHUNAGAR TAMIL NADU 626001 2 1201060000806633 A ANIL KUMAR-000201627386-ICICI BANK LTD 25.00 847391 7/3/2019 004303 NO 11/13 2nd FLOOR 4th CROSS VENKATESHWAR LAYOUT S.G.PALYA BANGALOR SOUTH DHRAMARAM COIIE BANGALORE 560029 2 A004253 A I SURAIYA 2.50 851452 7/3/2019 003368 403, SARJAN APT., 7,RAIYANIGRAM, SHIMPOLI ROAD, BORIVALI (W), MUMBAI 400092 3 A004373 A JYOTHIRMAYEE 2.50 847195 7/3/2019 004063 H NO 2-2-647/A/77 SRI SAIBABA NAGAR COLONY BAGH AMBERPET HYDERABAD 500013 3 A004254 A K SHRINIVASAN 2.50 847518 7/3/2019 004467 16 ANANDA PURAM MYLAPORE MADRAS 600004 4 IN30051312564400 A KISHORE BABU-145742-UCO BANK 7.50 847552 7/3/2019 004501 FLAT NO G/2 SANTHOSH VENKATESAPURAM VADAPALANI CHENNAI TAMIL NADU 600026 4 1203600000779481 A KUMARASWAMY-609801126259-ICICI BANK LTD 31.25 846971 7/3/2019 004586 2/70 4E ANBU NAGAR KEEZHATHATHIYARKULAM THEREKALPUDUR THRUPATHISARAM KANNIYAKUMARI 629901 5 A00015 A MOHAN KUMAR-33065-THANE JANATA SAHAKARI BANK LTD.(TJS 1,500.00 850784 7/3/2019 005682 FLAT NO 706 7TH FLOOR SKY PILLAR C H S LTD NR NEW SHAKTI MILLS DR AMBEDKAR ROAD THANE (W) 400601 5 A04239 A RAMAKRISHNA 1,000.00 846886 7/3/2019 004114 15-451-B-2 KAMALA NAGAR ANANTAPUR A P 515001 6 1204470001115722 A RAMAPRASAD L-008010101134863-AXIS BANK LTD 125.00 847311 7/3/2019 004219 4-45-1 ASHOK HOUSE PEDAWALTAIR VISAKHAPATNAM 530017 6 A004376 A S RAO 2.50 847325 7/3/2019 004233 47-1-14, 2F/8, USHODAYA APTS., DANAVAIPET, RAJAHMUNDRY 533103 7 A00024 A V A MARUTI RAM-1832-A P STATE CO - OP BANK LTD 2,000.00 850836 7/3/2019 005743 C/O. -

Sl.No. Salutation Name Designation Organisation / Department I CHAIRMAN Executive Director with Addl

STATE LEVEL BANKERS' COMMITTEE, TAMIL NADU CONVENOR : INDIAN OVERSEAS BANK 148 th STATE LEVEL BANKERS' COMMITTEE HELD ON 16.12.2016 LIST OF PARTICIPANTS Sl.No. Salutation Name Designation Organisation / Department I CHAIRMAN Executive Director with Addl. charge of 1 Mr. R.Subramaniakumar MD & CEO Indian Overseas Bank II GOVERNMENT OF INDIA 2 Mr. A.K.Dogra Deputy Secretary Dept. of Financial Services II GOVERNMENT OF TAMILNADU AND RELATED DEPARTMENTS / AGENCIES 3 Mr. K.Shanmugam, IAS Additional Chief Secretary (Finance) Govt. of Tamil Nadu 4 Mr. Kumar Jayant,IAS Managing Director TAHDCO 5 Ms. Rita Harish Thakkar, IAS Addl.Commissioner Industries & Commerce 6 Ms. Lalitha R, IAS Dy.Secretary Food & Coop Dept 7 Mr. K.S.Santhalingam A.D (FI) MSME Dt 8 Mr. R.Ekambaram Addl Director Industries & Commerce Dept 9 Mr. S.Annamalai JD TNCDW 10 Mr. M.Subburaj Jt. Director of Fisheries Fisheries Dept 11 Ms. G.Jayalakshmi Jt.Director Directorate of Social Welfare 12 Mr. G.Srinivasa Rao Jt.Director (Credit) TNCDW 13 Mr. S.Nagaraj Jt.Director, OSD Handloom & Textiles 14 Mr. M.Narayanasamy DD Agriculture Dept. Directorate of Agriculture 15 Mr. S.Arun kumar Asst Director (Funds) Directorate of Ex.Service Men's welfare 16 Mr. C.Baskar Asst Director KVIC 17 Mr. N.Nagaraj Asst Director 18 Dr. S.Muzamil Rafeek MVSC Asst Director AH Dept 19 Mr. M.Chinna Thambi Asst Director KVIC, Chennai 20 Mr. A.Nagarajan Asst Director of Sericulture Govt. Anna Silk Exchange , Kancheepuram 21 Ms. C.Poongothai ED, TNSFAC Dept of Agri Marketing 22 Mr. B.Lindsy Jesudial Financial Controller Adi Dravida & Tribal Dept 23 Mr. -

AGENDA: 1 118Th SLBC

AGENDA: 1 127th SLBC CONFIRMATION OF THE MINUTES OF THE EARLIER MEETING The minutes of the 126th State Level Bankers‟ Committee Meeting convened on 29.06.2011 (already circulated vide SLBC letter dated 26.07.2011) may be confirmed. AGENDA No: 2 Follow-up action on the decision of the earlier meetings: Notification of Centres for Deposit Of Title Deeds for Creation of Equitable Mortgage Transaction (EMT) SLBC Convenor requested the Principal Secretary, Finance, Government of Tamil Nadu vide SLBC letter dated 11.01.2011, with a copy of the above GO of Government of Kerala, to arrange for notification of all centres in Tamil Nadu where Bank Branches are located on the lines done in Kerala. State Government is again requested to notify all the centres where bank branches are located as notified centres. AGENDA No: 3 127th SLBC New Issues 1. Providing Banking services in every village having population of over 2000 The details of revised list of villages (4385) having population over 2000 identified and allotted to various Banks by DCCs for extension of banking services were placed in the SLRM 2010. As per the plan submitted by member banks, 2188 villages have to be covered in 2010-11 and 2197 villages in 2011-12. As per the Quarterly progress report submitted by Banks as per Annexure B, 2505 villages have been covered as on 30.06.2011. The details are furnished in the annexure. Member Banks are requested to ensure extension of banking services to villages as per plan submitted by them and ensure 100% achievement by December 2011 as decided earlier. -

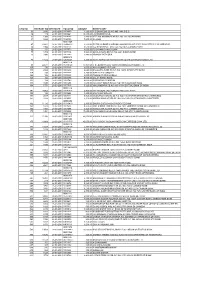

Chq No Warrant No Wrntdate Folio No Amount Beneficiary

CHQ NO WARRANT NO WRNTDATE FOLIO NO AMOUNT BENEFICIARY 31 2036 28-09-2011 0008330 4,160.00 K S BHANGOO SB A/C NO 1891 O B C 34 119 28-09-2011 0000441 10,880.00 LAV KUMAR KAUL 35 1993 28-09-2011 0008203 2,880.00 NEELAM SAWHNAY SB A/C NO 137 INDIAN BANK 37 5222 28-09-2011 0020399 7,680.00 S L RAO IN301549 47 20922 28-09-2011 16486920 3,200.00 SATISH KUMAR KHURANA 00441050006337 HDFC BANK LTD DLF CHAKRAPUR 56 1966 28-09-2011 0008128 3,520.00 GULSHAN KHULLAR C A/C NO 7426 CANARA BANK 62 154 28-09-2011 0000572 8,000.00 PUSHYAMI CHANGULANI 75 1729 28-09-2011 0007384 5,920.00 SUNIL K SONI SB A/C NO 6663 INDIAN BANK 76 7996 28-09-2011 0067909 2,880.00 PRANAY KATHURIA IN300214 78 11632 28-09-2011 12083346 3,200.00 NEHA NATANI 01750110001879 KOTAK MAHINDRA BANK LTD IN301774 98 22471 28-09-2011 15830120 17,953.60 C S LEASEFIN LTD 126010200006644 AXIS BANK LTD 105 170 28-09-2011 0000623 8,000.00 AJAY KUMAR KRIPLANI 115 2022 28-09-2011 0008286 4,640.00 BALGOPAL NAIR SB A/C NO 12838 SYNDICATE BANK 124 193 28-09-2011 0000696 3,200.00 WANTI DEVI GROVER 128 102 28-09-2011 0000393 8,000.00 PARAMJIT SINGH KOHLI 129 104 28-09-2011 0000395 8,000.00 BALJIT SINGH KOHLI 132 199 28-09-2011 0000740 4,000.00 DARSHAN LAL MADAN 133 1680 28-09-2011 0007206 4,640.00 KULDEEP SINGH SB A/C NO 14435 BANK OF INDIA 134 1774 28-09-2011 0007513 5,920.00 VIMLA MEHRA SB A/C NO 4113 CENTRAL BANK OF INDIA IN300724 147 16063 28-09-2011 10045956 6,400.00 BEENA SURI 5465 PUNJAB AND SIND BANK 155 180 28-09-2011 0000654 3,200.00 ANUPAMA MIGLANI 156 2037 28-09-2011 0008331 5,920.00 MEENAKSHI -

A Handbook on E-Payment

User Manual, e-Payment Town and Country Planning Department, Haryana A Handbook on e-Payment TOWN AND COUNTRY PLANNING DEPARTMENT, GOVERNMENT OF HARYANA Revision History Version Date 1.0 02/08/2016 1.1 10/01/2017 1.2 10/02/2017 1.3 15/09/2017 1.4 24/08/2018 IT CELL Page 1 User Manual, e-Payment Town and Country Planning Department, Haryana Table of Contents 1.0 Introduction ....................................................................................................................... 3 1.1 The Salient features of e-Payment ........................................................................... 3 1.2 Minimum Hardware & Software Requirement ........................................................ 3 1.3 Support ........................................................................................................................... 3 2.0 Getting Started .................................................................................................................. 4 2.1 Registration ................................................................................................................... 4 2.2 Login ............................................................................................................................... 5 2.3 Forgot password ........................................................................................................... 5 3. Dashboard ........................................................................................................................... 6 4.0 Making Payment ............................................................................................................... -

Bill Payment Options

Bill Payment Options Payment of electricity charges shall be made in the following modes other than the TANGEDCO’s Collection Centers: Services Through Banking Account S.No Mode of Payment Charges Head Axis bank Bank of Baroda Bank of India Canara Bank Catholic Syrian Bank Central Bank of India City Union bank Federal Bank HDFC bank Current ICICI Bank consumption IDBI bank Charges, Internet – Payment Net Indian Bank 1 NIL Advance Banking Indian Overseas Bank payments, Karur Vysya Bank Arrear Lakshmi Vilas bank Payments Punjab National Bank State Bank of India TNSC bank TamilNadu Mercantile Bank Union Bank of India Current consumption Internet – Payment Charges, Axis bank As applicable 2 Gateway (Any Master / Advance HDFC bank VISA card) payments, Arrear Payments Current consumption Canara Bank Charges, Internet – Payment 3 Indian Bank Rs.5 to 10 Advance Debit Card Indian Overseas Bank payments, Arrear Payments Current Payment through Mobile consumption (Wireless Application City Union Bank 4 NIL Charges, Protocol) Karur Vysya Bank Arrear Payments Current Payment through Mobile consumption 5 (Short Message Service) Indian Bank NIL Charges, Arrear Payments Upto Rs Current Rs 1000 5 consumption Charges, Rs.1001 to 10 Arrear Rs.2500 Payments Selected India Post 6 India POST Counters counters Rs.2501 (2522 Post offices) 15 to Rs.5000 Above 20 Rs.5000 City Union Bank Current Indian Overseas Bank consumption 7 Bank Counters Lakshmi Vilas bank Rs.5 to 10 Charges, TamilNadu Mercantile Arrear Bank Payments Current consumption TamilNadu Mercantile 8 Bank ATM NIL Charges, Bank, Federal Bank Arrear Payments Current consumption Urban Common Service 9 As applicable Charges, centers Arrear Payments e-seva centers Current consumption TamilNadu Arasu Cable 10 9120 Nos. -

Authorised Payment Channels of CESC Limited • Axis Bank Gateway

Authorised Payment Channels of CESC Limited Axis Bank Gateway PayTM Gateway Bill Desk Gateway Kotak Bank Andhra Bank Allahabad Bank Airtel Money Airtel Payment Bank Axis Bank Corporate Bank of Baroda Corporate Bank of Bahrain and Kuwait Bank of Baroda Retail Bandhan Bank BNP Paribas Bank Of India Bank of Maharashtra Central Bank of India Canara BankCOB Corporate Punjab National Bank Corporation BankCSB City Union Bank Deutsche Bank DIGI Bank DCB Corporate Netbanking Development Credit Bank Dena Bank Netbanking Dhanlaxmi Bank Corporate Dhanlaxmi Federal Bank Scan&Pay Federal Bank HDFC UPI HDFC Bank Limited Unified Payment Interface System ICICI Bank IDBI Bank IDBI Corporate IDFC Bank Netbanking IndusInd Bank Indian Bank Indian Overseas Bank Jammu and Kashmir Bank Limited Janata Sahakari BankKBL Kalyan Janata Sahakari Bank Karur Vysya Bank Limited Lakshmi Vilas Bank Corporate Lakshmi Vilas Bank Retail Mobikwik Mehsana Urban Co. Op. Bank NKGSB Bank ORIENTAL BANK OF COMMERCE Punjab & Maharashtra Co Punjab National Bank Punjab & Sind Bank RBL Bank Reliance Jio Ratnakar Corporate Banking State Bank of Hyderabad State Bank of India State Bank of Bikaner and Jaipur State Bank of MysoreSBP State Bank of TravancoreSCB South Indian Bank Ltd Shamrao Vithal Co Saraswat Bank Syndicate Bank TJSBTMB TNSC Bank Union Bank of India UCO Bank United Bank of India Axis Bank Bharat QR Code Vijaya Bank Vodafone mPesa YES Bank Bhartiya Mahila Bank Cosmos Bank Catholic Syrian Bank Karnataka