Bank Audi Sae Annual Report 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

HELWAN SOUTH 3 X 650 Mwe GAS-FIRED STEAM POWER PROJECT

ENGINEERING CONSULTANTS GROUP Arab Republic of Egypt Ministry of Electricity and Energy Egyptian Electricity Holding Company Upper Egypt Electricity Production Company Public Disclosure Authorized HELWAN SOUTH 3 x 650 MWe GAS-FIRED STEAM POWER PROJECT Public Disclosure Authorized Resettlement Policy Framework (RPF) Executive Summary Public Disclosure Authorized March 2013 Project No. 1573 Submitted by: Engineering Consultants Group (ECG) Bldg. 2, Block 10, El-Safarat District Nasr City 11765, Cairo, Egypt. Public Disclosure Authorized P.O. Box: 1167. Cairo 11511, Egypt. _______________________________________________________________________________________________________ ESIA for Helwan South 3x650 MWe Steam Power Plant RPF- Page 2 of 28 March 2013 - Project No. 1573 ENGINEERING CONSULTANTS GROUP TABLE OF CONTENTS LIST OF ACRONYMS AND ABBREVIATION LIST OF FIGURES GLOSSARY 1. THE PROJECT AND THE ROLE OF THE RPF 2. OBJECTIVES OF THE RPF FRAMEWORK 3. LEGISLATIVE FRAMEWORK FOR RESETTLEMENT IN EGYPT 4. WORLD BANK SAFEGUARD POLICIES 5. GAPS AND MEASURES TO BE CONSIDERED REFERENCES _______________________________________________________________________________________________________ ESIA for Helwan South 3x650 MWe Steam Power Plant RPF- Page 3 of 28 March 2013 - Project No. 1573 ENGINEERING CONSULTANTS GROUP LIST OF ACRONYMS AND ABBREVIATION ARP Abbreviated Resettlement Action Plan (RAP) CDA Community Development Association CAPMAS Central Agency for Public Mobilization and Statistics CEPC Cairo Electricity Production Company DAS Drainage -

UNIVERSITY of CALIFORNIA Santa Barbara Egyptian

UNIVERSITY OF CALIFORNIA Santa Barbara Egyptian Urban Exigencies: Space, Governance and Structures of Meaning in a Globalising Cairo A Thesis submitted in partial satisfaction of the requirements for the degree Master of Arts in Global Studies by Roberta Duffield Committee in charge: Professor Paul Amar, Chair Professor Jan Nederveen Pieterse Assistant Professor Javiera Barandiarán Associate Professor Juan Campo June 2019 The thesis of Roberta Duffield is approved. ____________________________________________ Paul Amar, Committee Chair ____________________________________________ Jan Nederveen Pieterse ____________________________________________ Javiera Barandiarán ____________________________________________ Juan Campo June 2014 ACKNOWLEDGEMENTS I would like to thank my thesis committee at the University of California, Santa Barbara whose valuable direction, comments and advice informed this work: Professor Paul Amar, Professor Jan Nederveen Pieterse, Professor Javiera Barandiarán and Professor Juan Campo, alongside the rest of the faculty and staff of UCSB’s Global Studies Department. Without their tireless work to promote the field of Global Studies and committed support for their students I would not have been able to complete this degree. I am also eternally grateful for the intellectual camaraderie and unending solidarity of my UCSB colleagues who helped me navigate Californian graduate school and come out the other side: Brett Aho, Amy Fallas, Tina Guirguis, Taylor Horton, Miguel Fuentes Carreño, Lena Köpell, Ashkon Molaei, Asutay Ozmen, Jonas Richter, Eugene Riordan, Luka Šterić, Heather Snay and Leila Zonouzi. I would especially also like to thank my friends in Cairo whose infinite humour, loyalty and love created the best dysfunctional family away from home I could ever ask for and encouraged me to enroll in graduate studies and complete this thesis: Miriam Afifiy, Eman El-Sherbiny, Felix Fallon, Peter Holslin, Emily Hudson, Raïs Jamodien and Thomas Pinney. -

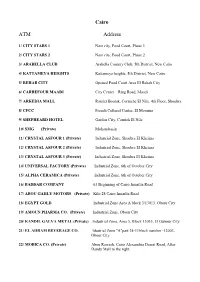

Cairo ATM Address

Cairo ATM Address 1/ CITY STARS 1 Nasr city, Food Court, Phase 1 2/ CITY STARS 2 Nasr city, Food Court, Phase 2 3/ ARABELLA CLUB Arabella Country Club, 5th District, New Cairo 4/ KATTAMEYA HEIGHTS Kattameya heights, 5th District, New Cairo 5/ REHAB CITY Opened Food Court Area El Rehab City 6/ CARREFOUR MAADI City Center – Ring Road, Maadi 7/ ARKEDIA MALL Ramlet Boulak, Corniche El Nile, 4th Floor, Shoubra 8/ CFCC French Cultural Center, El Mounira 9/ SHEPHEARD HOTEL Garden City, Cornish El Nile 10/ SMG (Private) Mohandessin 11/ CRYSTAL ASFOUR 1 (Private) Industrial Zone, Shoubra El Kheima 12/ CRYSTAL ASFOUR 2 (Private) Industrial Zone, Shoubra El Kheima 13/ CRYSTAL ASFOUR 3 (Private) Industrial Zone, Shoubra El Kheima 14/ UNIVERSAL FACTORY (Private) Industrial Zone, 6th of October City 15/ ALPHA CERAMICA (Private) Industrial Zone, 6th of October City 16/ BADDAR COMPANY 63 Beginning of Cairo Ismailia Road 17/ ABOU GAHLY MOTORS (Private) Kilo 28 Cairo Ismailia Road 18/ EGYPT GOLD Industrial Zone Area A block 3/13013, Obour City 19/ AMOUN PHARMA CO. (Private) Industrial Zone, Obour City 20/ KANDIL GALVA METAL (Private) Industrial Zone, Area 5, Block 13035, El Oubour City 21/ EL AHRAM BEVERAGE CO. Idustrial Zone "A"part 24-11block number -12003, Obour City 22/ MOBICA CO. (Private) Abou Rawash, Cairo Alexandria Desert Road, After Dandy Mall to the right. 23/ COCA COLA (Pivate) Abou El Ghyet, Al kanatr Al Khayreya Road, Kaliuob Alexandria ATM Address 1/ PHARCO PHARM 1 Alexandria Cairo Desert Road, Pharco Pharmaceutical Company 2/ CARREFOUR ALEXANDRIA City Center- Alexandria 3/ SAN STEFANO MALL El Amria, Alexandria 4/ ALEXANDRIA PORT Alexandria 5/ DEKHILA PORT El Dekhila, Alexandria 6/ ABOU QUIER FERTLIZER Eltabia, Rasheed Line, Alexandria 7/ PIRELLI CO. -

Trip to Egypt January 25 to February 8, 2020. Day 1

Address : Group72,building11,ap32, El Rehab city. Cairo ,Egypt. tel : 002 02 26929768 cell phone: 002 012 23 16 84 49 012 20 05 34 44 Website : www.mirusvoyages.com EMAIL:[email protected] Trip to Egypt January 25 to February 8, 2020. Day 1 Travel from Chicago to Cairo Day 2 Arrival at Cairo airport, meet & assistance, transfer to the hotel. Overnight at the hotel in Cairo. Day 3 Saqqara, the oldest complete stone building complex known in history, Saqqara features numerous pyramids, including the world-famous Step pyramid of Djoser, Visit the wonderful funerary complex of the King Zoser & Mastaba (Arabic word meaning 'bench') of a Noble. Lunch in a local restaurant. Visit the three Pyramids of Giza, the pyramid of Cheops is the oldest of the Seven Wonders of the Ancient World, and the only one to remain largely intact. ), the Great Pyramid was the tallest man-made structure in the world for more than 3,800 years. The temple of the valley & the Sphinx. Overnight at the hotel in Cairo. Day 4 Visit the Mokattam church, also known by Cave Church & garbage collectors( Zabbaleen) Mokattam, it is the largest church in the Middle East, seating capacity of 20,000. Visit the Coptic Cairo, Visit The Church of St. Sergius (Abu Sarga) is the oldest church in Egypt dating back to the 5th century A.D. The church owes its fame to having been constructed upon the crypt of the Holy Family where they stayed for three months, visit the Hanging Church (The Address : Group72,building11,ap32, El Rehab city. -

A Comparative Class Study in Two Contemporary Cairo Neighborhoods

American University in Cairo AUC Knowledge Fountain Theses and Dissertations 2-1-2018 Marital economies: A comparative class study in two contemporary Cairo neighborhoods Sahar Mohsen Mohammad Follow this and additional works at: https://fount.aucegypt.edu/etds Recommended Citation APA Citation Mohammad, S. (2018).Marital economies: A comparative class study in two contemporary Cairo neighborhoods [Master’s thesis, the American University in Cairo]. AUC Knowledge Fountain. https://fount.aucegypt.edu/etds/694 MLA Citation Mohammad, Sahar Mohsen. Marital economies: A comparative class study in two contemporary Cairo neighborhoods. 2018. American University in Cairo, Master's thesis. AUC Knowledge Fountain. https://fount.aucegypt.edu/etds/694 This Thesis is brought to you for free and open access by AUC Knowledge Fountain. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of AUC Knowledge Fountain. For more information, please contact [email protected]. Marital Economies: A Comparative Class Study in Two Contemporary Cairo Neighborhoods Dedication To the souls of my father and mother who grew up the insisting on success in me. To my beloved family: My husband: Ahmad Sabry My daughters: Noura and Yosra My sons: Sherif and Mahmoud ii Table of Contents Abstract ......................................................................................................................................................... v Neoliberalism, Consumerism and the Production of New Subjectivity ...................................................... -

Egypt State of Environment Report 2008

Egypt State of Environment Report Egypt State of Environment Report 2008 1 Egypt State of Environment Report 2 Egypt State of Environment Report Acknowledgment I would like to extend my thanks and appreciation to all who contributed in producing this report whether from the Ministry,s staff, other ministries, institutions or experts who contributed to the preparation of various parts of this report as well as their distinguished efforts to finalize it. Particular thanks go to Prof. Dr Mustafa Kamal Tolba, president of the International Center for Environment and Development; Whom EEAA Board of Directors is honored with his membership; as well as for his valuable recommendations and supervision in the development of this report . May God be our Guide,,, Minister of State for Environmental Affairs Eng. Maged George Elias 7 Egypt State of Environment Report 8 Egypt State of Environment Report Foreword It gives me great pleasure to foreword State of Environment Report -2008 of the Arab Republic of Egypt, which is issued for the fifth year successively as a significant step of the political environmental commitment of Government of Egypt “GoE”. This comes in the framework of law no.4 /1994 on Environment and its amendment law no.9/2009, which stipulates in its Chapter Two on developing an annual State of Environment Report to be submitted to the president of the Republic and the Cabinet with a copy lodged in the People’s Assembly ; as well as keenness of Egypt’s political leadership to integrate environmental dimension in all fields to achieve sustainable development , which springs from its belief that protecting the environment has become a necessary requirement to protect People’s health and increased production through the optimum utilization of resources . -

Maat for Peace, Development, and Human Rights

Violating Rights of Local Civilian Submitted to: Mechanism of Universal Periodical Review By: Maat for Peace, Development, and Human Rights. August 2009 انعنوان: أول ش انمهك فيصم - برج اﻷطباء – اندور انتاسع – شقه 908 – انجيزة ت / ف : 37759512 /02 35731912 /02 موبايم : 5327633 010 6521170 012 انبريد اﻻنكتروني : [email protected] [email protected] انموقع: www.maatpeace.org www.maat-law.org Report Methodology This report will discuss four components which are drinking water, draining services, environment services, and health services. The report will focus on those four components because there is a connection between them and because they are the more urgent and spread needs watched by Maat Institution. This report depended on three information sources: 1- Results of discussion meetings with citizens: there are 33 discussion meetings were held in some Egyptian governorates, in order to define problems and violations related to public utilities and essential services. 2- Citizens complaints: big number of citizens and their representatives in local public councils delivered written complaints to Maat Institution about specific violations they suffer regarding public utilities and essential services. 3- Journalism subjects published in Egyptian journals regarding violations of economical and social rights and depriving from essential services. First violation regarding the right to have safe drinking water: Egypt witnessed in the last three years increasing public anger because of shortage in drinking water available in many places of the republic. Thus, protest forms rose like demonstrations and stays-in strike to force executive managers to solve this problem. This period also witnessed many cases of water pollutions or mixing drinking water with draining water this is the problem which makes many people infected with hepatitis and renal failure. -

Arab African International Bank (AAIB) Maintained Its Leading Our Ability to Confront Future Challenges and Growth Position As a Leading Financial Institution

“50 GOLDEN YEARS OF VALUE CREATION” VISI N To be the leading financial group in Egypt providing innovative services with a strong regional presence being the gateway for international business into the region. Cover: The Royal Geographical | Society Qasr El Aini Street | Photographer: Barry Iverson This image: The Royal Geographical Society | Qasr El Aini Street | Photographer: Shahir Sirry “ 50 GOLDEN YEARS OF CONFIDENCE” been at the core of AAIB’s values, guiding all its interactions with its clients and a mission to do what is right. TABLE F C NTENT Shareholders 4 Board of Directors 5 Chairman’s Statement 6 Vice Chairman & Managing Director’s Report 8 Financial Statements 13 Balance sheet 14 Income statement 14 Statement of changes in owners’ equity 15 Statement of cash flows 15 Statement of proposed appropriation 16 Notes to the financial statements 16 Auditors’ Report 50 Branches 52 Location description Door of “Inal Al Yusufi” Mosque | Khayameya | Islamic Cairo | Photographer: Karim El Hayawan “ GOLDEN YEARS OF 50 STRENGTH” Only when a solid foundation is built, can an entity really prosper. The trust we have in the Central Bank of Egypt, the Kuwait Investment Authority as shareholders and the stability having a strong dollar based equity gives us the SHARH LDERS PERCENTAGE OF HOLDING Central Bank of Egypt, Egypt 49.37% Kuwait Investment Authority, Kuwait 49.37% Others 1.26% Others 1.26% Kuwait Investment Authority, Central Bank Kuwait of Egypt, 49.37% Egypt 49.37% The Royal Geographical | Society Qasr El Aini Street | Photographer: Barry Iverson “ GOLDEN YEARS OF 50 PASSION ” Our passion is what fuels our growth. -

Governorate Area Type Provider Name Card Specialty Address Telephone 1 Telephone 2

Governorate Area Type Provider Name Card Specialty Address Telephone 1 Telephone 2 Metlife Clinic - Cairo Medical Center 4 Abo Obaida El bakry St., Roxy, Cairo Heliopolis Metlife Clinic 02 24509800 02 22580672 Hospital Heliopolis Emergency- 39 Cleopatra St. Salah El Din Sq., Cairo Heliopolis Hospital Cleopatra Hospital Gold Outpatient- 19668 Heliopolis Inpatient ( Except Emergency- 21 El Andalus St., Behind Cairo Heliopolis Hospital International Eye Hospital Gold 19650 Outpatient-Inpatient Mereland , Roxy, Heliopolis Emergency- Cairo Heliopolis Hospital San Peter Hospital Green 3 A. Rahman El Rafie St., Hegaz St. 02 21804039 02 21804483-84 Outpatient-Inpatient Emergency- 16 El Nasr st., 4th., floor, El Nozha Cairo Heliopolis Hospital Ein El Hayat Hospital Green 02 26214024 02 26214025 Outpatient-Inpatient El Gedida Cairo Medical Center - Cairo Heart Emergency- 4 Abo Obaida El bakry St., Roxy, Cairo Heliopolis Hospital Silver 02 24509800 02 22580672 Center Outpatient-Inpatient Heliopolis Inpatient Only for 15 Khaled Ibn El Walid St. Off 02 22670702 (10 Cairo Heliopolis Hospital American Hospital Silver Gynecology and Abdel Hamid Badawy St., Lines) Obstetrics Sheraton Bldgs., Heliopolis 9 El-Safa St., Behind EL Seddik Emergency - Cairo Heliopolis Hospital Nozha International Hospital Silver Mosque, Behind Sheraton 02 22660555 02 22664248 Inpatient Only Heliopolis, Heliopolis 91 Mohamed Farid St. El Hegaz Cairo Heliopolis Hospital Al Dorrah Heart Care Hospital Orange Outpatient-Inpatient 02 22411110 Sq., Heliopolis 19 Tag El Din El Sobky st., from El 02 2275557-02 Cairo Heliopolis Hospital Egyheart Center Orange Outpatient 01200023220 Nozha st., Ard El Golf, Heliopolis 22738232 2 Samir Mokhtar st., from Nabil El 02 22681360- Cairo Heliopolis Hospital Egyheart Center Orange Outpatient 01200023220 Wakad st., Ard El Golf, Heliopolis 01225320736 Dr. -

Getting by on the Margins: Sudanese and Somali Refugees a Case Report of Refugees in Towns Cairo, Egypt

Getting by on the Margins: Sudanese and Somali Refugees A Case Report of Refugees in Towns Cairo, Egypt Paul Miranda Cairo, Egypt / A Case Report of Refugees in Towns 1 JUNE 2018 Contents About the RIT Project 3 Location 4 Introduction 5 About the Author and How He Wrote the Report 5 Background on Forced Migration to Egypt 6 Legal Framework Governing Refugees in Egypt 8 Background on Forced Migration in Greater Cairo 9 Mapping Cairo’s Refugees 10 Sudanese and Somali Neighborhoods: Hay el Ashr and Araba wa Nus 12 Governance 12 Demographics 13 Spatial Distribution of Populations in Hay el Ashr and Araba wa Nus 13 Refugees’ Experiences 15 Livelihoods 15 Children’s Education 16 Medical services 17 Urban Impact on the Economy and Housing 17 The local economy: Sudanese and Somali businesses 18 Housing 18 Governance 20 African Refugees’ Experiences 21 Racism 21 Social Networks and Political Mobilization 23 Gangs 23 Future Outlooks on Integration 24 Conclusion 25 References 26 Cairo, Egypt / A Case Report of Refugees in Towns 2 About the RIT Project The Refugees in Towns (RIT) project promotes understanding of the migrant/refugee experience in urban settings. Our goal is to understand and promote refugee integration by drawing on the knowledge and perspective of refugees and locals to develop deeper understanding of the towns in which they live. The project was conceived and is led by Karen Jacobsen. It is based at the Feinstein International Center at Tufts University and funded by the Henry J. Leir Foundation. Our goals are twofold Our first long-term goal is to build a theory of integration form the ground up by compiling a global database of case studies and reports to help us analyze and understand the process of immigrant/refugee integration. -

ARKMEN Ltd. Profile Page 2 1

Copyright © 2003-2018 ARKMEN Ltd. All rights reserved. Table of Contents . ARKMEN Ltd. Profile Page 2 1. Our Vision 2. Our Mission 3. Our Strategies . ARKMEN Ltd. Business Lines Page 3 . Introduction Page 4 . Market Penetration Policies Page 4 . IT Solutions Business Line (ProStruct) Page 4 1. The IT Challenge Page 4 2. IT Solutions subdivisions Page 5 - LAN Solutions Page 5 - VPN Solutions Page 5 - VOIP Solutions Page 5 - WAN Solutions Page 5 - CCTV Solutions Page 5 3. The Standard Categorizing of the IT Projects Page 6 - Layer One Tasks Page 6 - Layer Two Tasks Page 6 - Layer Three Tasks Page 6 4. Summary Perspective of IT-Solutions Activities Page 6 . IT Services Business Line (ProSupport) Page 7 1. What is EQSPS Page 7 2. Why EQSPS Page 7 3. How EQSPS has been Created and activated Page 7 - The Initial Field Survey Page 7 - Evaluation and Quotation Page 8 - Offering and Recommendations Page 8 4. EQSPS System Features and Benefits Page 8 . Brands and Partners Page 9 1. On side of ProStruct scope (Active Components) Page 9 2. On side of ProStruct scope (Passive Components) Page 9 3. On side of ProStruct scope (CCTV Solutions) Page 9 4. On side of ProSupport scope Page 9 . ARKMEN Ltd. Partial Reference Projects Page 10 Copyright © 2003-2018 ARKMEN Ltd. All rights reserved. Page 1 of 12 ARKMEN’s Profile: ear valuable customer, We are pleased to introduce ARKMEN as Egypt’s leading premier ICT solutions and with the technology, capability and skills to deliver end-to-end digital solutions for large and medium enterprises in the public and private sectors., destined to render efficient, reliable and dependable support of the computing technology and ICT Solutions & technical services, ARKMEN Ltd. -

ATM Branch Branch Address Area Gameat El Dowal El

ATM Branch Branch address Area Gameat El Dowal Gameat El Dowal 9 Gameat El-Dewal El-Arabia Mohandessein, Giza El Arabeya Thawra El-Thawra 18 El-Thawra St. Heliopolis, Heliopolis, Cairo Cairo 6th of October 6th of October Banks area - industrial zone 4 6th of October City, Giza Zizenia Zizenia 601 El-Horaya St Zizenya , Alexandria Champollion Champollion 5 Champollion St., Down Town, Cairo New Hurghada Sheraton Hurghada Sheraton Road 36 North Mountain Road, Hurghada, Red Sea Hurghada, Red Sea Mahatta Square El - Mahatta Square 1 El-Mahatta Square Sarayat El Maadi, Cairo New Maadi New Maadi 48 Al Nasr Avenu New Maadi, Cairo Shoubra Shoubra 53 Shobra St., Shoubra Shoubra, Cairo Abassia Abassia 111 Abbassia St., Abassia Cairo Manial Manial Palace 78 Manial St., Cairo Egypt Manial , Cairo Hadayek El Kobba Hadayek El Kobba 16 Waly El-Aahd St, Saray El- Hdayek El Kobba, Cairo Hadayek Mall Makram Ebeid Makram Ebeid 86, Makram Ebeid St Nasr City, Cairo Abbass El Akkad Abbass El Akkad 20 Abo El Ataheya str. , Abas Nasr City, Cairo El akad Ext Tayaran Tayaran 32 Tayaran St. Nasr City, Cairo House of Financial Affairs House of Financial Affairs El Masa, Abdel Azziz Shenawy Nasr City, Cairo St., Parade Area Mansoura 2 El Mohafza Square 242 El- Guish St. El Mohafza Square, Mansoura Aghakhan Aghakhan 12th tower nile towers Aghakhan, Cairo Aghakhan Dokki Dokki 64 Mossadak Street, Dokki Dokki, Giza El- Kamel Mohamed El_Kamel Mohamed 2, El-Kamel Mohamed St. Zamalek, Cairo El Haram El Haram 360 Al- Haram St. Haram, Giza NOZHA ( Triumph) Nozha Triumph.102 Osman Ebn Cairo Affan Street, Heliopolis Safir Nozha 60, Abo Bakr El-Seddik St.