45 50 Residential Retail Office 62 NOI Analysis 55

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Canton of Basel-Stadt

Canton of Basel-Stadt Welcome. VARIED CITY OF THE ARTS Basel’s innumerable historical buildings form a picturesque setting for its vibrant cultural scene, which is surprisingly rich for THRIVING BUSINESS LOCATION CENTRE OF EUROPE, TRINATIONAL such a small canton: around 40 museums, AND COSMOPOLITAN some of them world-renowned, such as the Basel is Switzerland’s most dynamic busi- Fondation Beyeler and the Kunstmuseum ness centre. The city built its success on There is a point in Basel, in the Swiss Rhine Basel, the Theater Basel, where opera, the global achievements of its pharmaceut- Ports, where the borders of Switzerland, drama and ballet are performed, as well as ical and chemical companies. Roche, No- France and Germany meet. Basel works 25 smaller theatres, a musical stage, and vartis, Syngenta, Lonza Group, Clariant and closely together with its neighbours Ger- countless galleries and cinemas. The city others have raised Basel’s profile around many and France in the fields of educa- ranks with the European elite in the field of the world. Thanks to the extensive logis- tion, culture, transport and the environment. fine arts, and hosts the world’s leading con- tics know-how that has been established Residents of Basel enjoy the superb recre- temporary art fair, Art Basel. In addition to over the centuries, a number of leading in- ational opportunities in French Alsace as its prominent classical orchestras and over ternational logistics service providers are well as in Germany’s Black Forest. And the 1000 concerts per year, numerous high- also based here. Basel is a successful ex- trinational EuroAirport Basel-Mulhouse- profile events make Basel a veritable city hibition and congress city, profiting from an Freiburg is a key transport hub, linking the of the arts. -

ZHAW SML Fact Sheet 2021-2022.Pdf

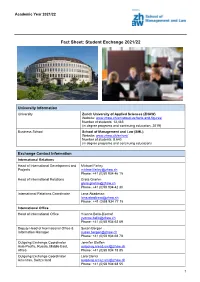

Academic Year 2021/22 Fact Sheet: Student Exchange 2021/22 University Information University Zurich University of Applied Sciences (ZHAW) Website: www.zhaw.ch/en/about-us/facts-and-figures/ Number of students: 13,485 (in degree programs and continuing education, 2019) Business School School of Management and Law (SML) Website: www.zhaw.ch/en/sml/ Number of students: 8,640 (in degree programs and continuing education) Exchange Contact Information International Relations Head of International Development and Michael Farley Projects [email protected] Phone: +41 (0)58 934 46 15 Head of International Relations Greta Gnehm [email protected] Phone: +41 (0)58 934 42 30 International Relations Coordinator Lena Abadesso [email protected] Phone: +41 (0)58 934 77 15 International Office Head of International Office Yvonne Bello-Bischof [email protected] Phone: +41 (0)58 934 62 69 Deputy Head of International Office & Susan Bergen Information Manager [email protected] Phone: +41 (0)58 934 68 78 Outgoing Exchange Coordinator Jennifer Steffen Asia-Pacific, Russia, Middle East, [email protected] Africa Phone: +41 (0)58 934 78 85 Outgoing Exchange Coordinator Lara Clerici Americas, Switzerland [email protected] Phone: +41 (0)58 934 68 55 1 Academic Year 2021/22 Outgoing Exchange Coordinator Miguel Corredera Europe [email protected] Phone: +41 (0)58 934 41 02 Incoming Exchange Coordinator Alice Ragueneau Overseas [email protected] Phone: +41 (0)58 934 62 51 Incoming Exchange Coordinator Sandra Aerne Europe -

Vineyards and Wines

Welcome to the Canton of Vaud! Dear media representatives, The Canton of Vaud uses the Lake Geneva Region brand to promote tourism in this area. Our organisation has a presence in over twenty markets on four continents and its chief mission is to promote destinations in our region − both in Switzerland and abroad. From our base in Lausanne, we work with our colleagues at Switzerland Tourism on the tourism market and with local tourist boards. This Press Release is intended to introduce you to the key themes that define the Canton of Vaud. It showcases the region's wide variety of scenery, activities and events. It includes general information along with anecdotes, descriptions, key statistics and plenty of links that will enable you to explore subjects in greater depth. The Press Department of the Lake Geneva Region Tourist Office will be delighted to help you with basic advice or detailed plans, welcoming you in person or making all the arrangements for a press trip. The "Media" section, on our website, www.lake‐geneva‐region.ch, also offers extensive information including the latest press releases, news from the region and access to a multimedia database where over 2,000 high‐ definition photos and videos can be downloaded. To access the area, just click on the link below and complete the online form. Whatever you’re looking for, just get in touch and we’ll be delighted to help you. Media information: www.lake‐geneva‐region.ch/media Media library: www.lake‐geneva‐region.ch/photos Mobile app: appmobile.lake‐geneva‐region.ch Share your experiences at #MyVaud and follow us on: VAUD – Lake Geneva Region MyVaud We’re here to help Lake Geneva Region Tourist Office Media Relations Department Mrs. -

Quick Guide to the Eurovision Song Contest 2018

The 100% Unofficial Quick Guide to the Eurovision Song Contest 2018 O Guia Rápido 100% Não-Oficial do Eurovision Song Contest 2018 for Commentators Broadcasters Media & Fans Compiled by Lisa-Jayne Lewis & Samantha Ross Compilado por Lisa-Jayne Lewis e Samantha Ross with Eleanor Chalkley & Rachel Humphrey 2018 Host City: Lisbon Since the Neolithic period, people have been making their homes where the Tagus meets the Atlantic. The sheltered harbour conditions have made Lisbon a major port for two millennia, and as a result of the maritime exploits of the Age of Discoveries Lisbon became the centre of an imperial Portugal. Modern Lisbon is a diverse, exciting, creative city where the ancient and modern mix, and adventure hides around every corner. 2018 Venue: The Altice Arena Sitting like a beautiful UFO on the banks of the River Tagus, the Altice Arena has hosted events as diverse as technology forum Web Summit, the 2002 World Fencing Championships and Kylie Minogue’s Portuguese debut concert. With a maximum capacity of 20000 people and an innovative wooden internal structure intended to invoke the form of Portuguese carrack, the arena was constructed specially for Expo ‘98 and very well served by the Lisbon public transport system. 2018 Hosts: Sílvia Alberto, Filomena Cautela, Catarina Furtado, Daniela Ruah Sílvia Alberto is a graduate of both Lisbon Film and Theatre School and RTP’s Clube Disney. She has hosted Portugal’s edition of Dancing With The Stars and since 2008 has been the face of Festival da Cançao. Filomena Cautela is the funniest person on Portuguese TV. -

Zug (8Th) and Basel (10Th) Rank Far Ahead of Lausanne (36Th), Bern (38Th), Zurich (41St), Lugano (53Rd), and Geneva (69Th) in the Expat City Ranking 2019

• Zug (8th) and Basel (10th) rank far ahead of Lausanne (36th), Bern (38th), Zurich (41st), Lugano (53rd), and Geneva (69th) in the Expat City Ranking 2019. • Based on the ranking, Taipei, Kuala Lumpur, Ho Chi Minh City, Singapore, Montréal, Lisbon, Barcelona, Zug, The Hague, and Basel are the best cities to move to in 2020. • Kuwait City (82nd), Rome, Milan, Lagos (Nigeria), Paris, San Francisco, Los Angeles, Lima, New York City, and Yangon (73rd) are the world’s worst cities. Munich, 3 December 2019 — Seven Swiss cities are featured in the Expat City Ranking 2019 by InterNations, the world’s largest expat community with more than 3.5 million members. They all rank among the top 20 in the world for the quality of life, receiving mostly high marks for safety, local transportation, and the environment. On the other hand, expats struggle to get settled, with Zurich and Bern even ranking among the world’s worst cities in this regard. While the local cost of living is rated negatively across the board, the performance of the Swiss cities varies more in the Finance & Housing and Urban Work Life Indices. The Expat City Ranking is based on the annual Expat Insider survey by InterNations, which is with more than 20,000 respondents in 2019 one of the most extensive surveys about living and working abroad. In 2019, 82 cities around the globe are analyzed in the survey, offering in-depth information about five areas of expat life: Quality of Urban Living, Getting Settled, Urban Work Life, Finance & Housing, and Local Cost of Living. -

Field Report Florence Meeting Bern/Winterthur

Gesundheit Field Report Florence Meeting Bern/Winterthur 18.-22. April 2017 Bern Fachhochschule in collaboration with ZHAW and FH Ostschweiz, Bern and Winterthur, Switzerland Students and Staff, Bachelor Midwifery and Nursing, various study years The conference of the 25th Florence Network Annual Meeting took place from Tuesday 18th April – Saturday 22th April 2017 in Switzerland. We spent four days in Bern at the University of Applied Sciences and one day in Winterthur, in cooperation with the Zurich University of Applied Sciences and the University of Applied Sciences St. Gallen. The conference theme was “Mental Health: Global Challenge – Local Actions”. During the week, the differences between the health care systems of the participating countries and especially those regarding mental health care were discussed. Keynote speakers talked about mental health and various workshops on different aspects of mental health were offered. The WHO defined 2017 Mental Health as “a state of well-being”. But what does that mean? Mental Health in Midwifery Due to the vulnerability of the perinatal period, a lot of women and men suffer from mental illnesses during this stage of life. That is why the midwifery workshops and keynote speeches of the FNAM were mainly about the topic of perinatal and above all postnatal depression and its treatment. According to Anke Berger’s presentation, 18% of Swiss pregnant women and 19% of new mothers suffer from a mental disorder. Although this is a high percentage, only 50% of these women are detected and can be treated. The treatment itself is a big challenge as psychopharmacological drugs may influence the foetus as well as the composition of breast milk. -

Brand Guidelines Version 5-2017/2018

BRAND GUIDELINES VERSION 5-2017/2018 OPERATED BY EBU THE EUROVISION SONG CONTEST - “ A SIMPLE IDEA THAT HAS SUCCEEDED. “MARCEL BEZENÇON DIRECTOR OF THE EBU (1950-1970) AND INITIATOR OF THE EUROVISION SONG CONTEST — 2 THE NAME The name of the event in public communication is always Eurovision Song Contest. For headlines and on social media, but only when practical limitations such as character limits apply, the event can be referred to as Eurovision. The abbreviation ESC may only be used for internal communications, as it is largely unknown to the public. In some countries, the Eurovision Song Contest has a translated name, such as Eurovisie Songfestival (Dutch) or Grand Prix Eurovision de la Chanson (French). These names may be used, but only in national communication. EUROVISION SONG CONTEST BRAND GUIDELINES — 3 THE LOGO Until the 2003 Eurovision Song Contest, each Host Broadcaster designed its own logo for the contest. In 2004, the EBU introduced a generic logo, to be accompanied by a theme and supporting artwork on a year-by-year basis. The logo was designed by London-based agency JM Enternational. In 2014, the EBU introduced a revamp, the current version of the logo. It was revamped by Storytegic and implemented in collaboration with Scrn. Eurovision is set in custom typograpy Song Contest is set in Gotham Bold with +25% letter spacing and +25% word spacing EUROVISION SONG CONTEST BRAND GUIDELINES — 4 THE ECO-SYSTEM The Eurovision Song Contest generic identity consists of an eco-system with four different applications, shown below. Some basic guidelines: Ÿ The generic logo can only be used by EBU and its partners; Ÿ The event logo can only be used for a particular event by the EBU, Host Broadcaster, Participating Broadcasters and Event Partners (sponsors); Ÿ A national logo can only be used by the EBU, its partners and each respective Participating Broadcaster; Ÿ The flag heart can only be used for illustrative purposes (e.g. -

18 Lake Geneva Region – Lausanne

18 lake geneva region – lausanne practical information How to get there: Lausanne has good con- nections to all major cities in Switzerland and almost hourly direct trains to France (Paris, 3h 50min.), Italy (Milan, 3h 50min.) and Germany (approx. 5 hours). 1 At the train station you’ll find the i tourist office (021 613 73 73); lockers, bicycle rental, currency exchange, rest rooms, fast food, small shops and a post of- fice. Lausanne is beautiful but very hilly, so be prepared for some steep walks when dis- covering Lausanne on foot! The center is a few steps up from the main station at place St. François. 2 Ouchy, the port of Laus- View of the city of Lausanne anne, is a beautiful place. There is another i tourist office at Avenue de Rhodanie 2. @ Internet at Quanta virtual fun space, ausanne resides on the hillside between Lake Geneva below and the woods above, 8 Fondation de l’Hermitage at Route du pl. de la Gare 4; Fleur de Pains, Avenue surrounded by meadowland and vineyards, facing the Alps. Lausanne was officially Signal 2 is housed in a beautiful 19th- d’Ouchy 73. Wireless Internet access is Lnamed the Olympic Capital in June 1994, a unique and prestigious title awarded by century residence and is devoted to hold- available at Flon, Palud, Riponne, St-Fran- the International Olympic Committee, headquartered in Lausanne since 1915. Popular ing temporary exhibitions on the fine arts. çois, Montbenon, Navigation, Port. with students, Lausanne features numerous private schools and one of the country’s It’s surrounded by a magnificent park! largest university campuses, comprising the Federal Institute of Technology (EPFL) and Tue – Sun 10 am – 6 pm, Thu until 9 pm, www.lausanne-tourisme.ch the University of Lausanne. -

Regions and Cities at a Glance 2018 – SWITZERLAND Economic Trends

q http://www.oecd.org/regional Regions and Cities at a Glance 2018 – SWITZERLAND Economic trends in regions Regional gap in GDP per capita, 2000-15 Index of regional disparity in GDP per capita, 2016 Top 20 % richest over bottom 20% poorest regions GDP per capita in USD PPP 2016 2000 Ratio 4 80 000 Small regions Large regions Highest region (TL3) (TL2) 70 000 Zurich 66 646 USD 3 60 000 Switzerland 52 323 USD 50 000 Lowest region 2 Eastern Switzerland 40 000 47 868 USD 1 30 000 2008 2011 2015 Country (number of regions considered) Regional disparities in terms of GDP per capita have slightly decreased in Switzerland over the last sixteen years, with Eastern Switzerland having a GDP per capita equivalent to 72% of Zurich’s GDP per capita in 2015. Regional economic disparities in Switzerland are among the lowest among OECD countries. With a productivity growth of 1.7% per year over the period 2008-14, Ticino not only had the highest level of productivity in 2014 but also recorded the largest growth among Swiss regions. Following a significantly lower productivity growth (0.1% per year), Zurich was replaced by Ticino as the frontier region in terms of productivity in Switzerland in 2010. With a youth unemployment of 15.6% in 2017 that was similar to the OECD average, Lake Geneva had the highest youth unemployment in the country. Youth unemployment in Central Switzerland only amounted to 4.1%, 11.5 percentage points below the youth unemployment rate in Lake Geneva. Productivity trends, most and least dynamic regions, 2008-14 Youth unemployment rate, 15-24 years old, 2007-17 GDP per worker in USD PPP rate (%) 130 000 Ticino: highest 25 125 000 productivity in 2016 and Highest rate highest productivity 20 Lake Geneva Region 120 000 growth (+1.7% average OECD Ticino: highest 15 15.6% 115 000 annual growth over productivity growth 2008-14) Switzerland 110 000 (+1.7% annually) 10 Zurich: lowest 8.1% 105 000 productivity growth 5 Lowest rate (+0.1% annually) 100 000 0 Central Switzerland 2008 2009 2010 2011 2012 2013 2014 2007 2012 2017 4.1% Source: OECD Regional Database. -

Maps Heerbrugg En.Qxp:4507 Leica Map.Qxp

Leica Geosystems Heerbrugg Switzerland From Zürich Airport to Heerbrugg: Austria …by car Au From the airport in Zürich, follow the green & white Border/ highway signs to the A1 highway towards Zurich - Gallen/Zürich St. Customs Winterthur – St. Gallen. Exit Remain on the A1 highway in St. Gallen and follwing to Au the signs to the A13, towards St. Margrethen – Chur. After approximately 110 km (1h15 min drive) from the airport, leave the highway at exit Au, Lustenau. Heerbrugg To At the end of the exit, turn to the right towards Au / Berneck. Take the third exit at the roundabout towards Heerbrugg. (Austria) Lustenau Krönele, Hotel 10 There are 5 traffic lights between there and the Post DC Widnau Heinrich-Wild-Strasse Berneck To office headoffices of Leica Geosystems, still approximately 3,5 km away. At the fourth traffic light, you will have reached the Heerbrugg Bus station other end of Heerbrugg and the premises of Leica To Altstätten Geosystems will be on your left. Railway station A13 Motorway Drive on and 300 m after the sign designating the 2 8 Rhine 7 1 village of Balgach, turn left into the Heinrich-Wild- Leica To Heerbrugg 4 6 Strasse on the far end of the Leica Geosystem 3 9 5 premises. Widnau The parking lot for visitors is locatecd directly in front Car Hotel Forum Wash Hotel Löwen of the reception building of Leica Geosystems Hotel Metropol (first building on the left) (Please remember that there is an annual permit to be paid for using the highways in Switzerland. Hotel Hotel Coop Hotel To WidnauFreihof All cars using the highways must have the paid Bad Balgach Supermarket Heerbrugghof permit or “vignette” glued on their windshields) Roundabout Traffic light Canal …by train Exit to To Allow at least 30 minutes between arrival of the Bus stop Widnau/ Diepoldsau Diepoldsau plane and the departure of the train. -

09:30 Joint SSP-EFP Session COVID-19 08:30

Scientific Programme Thursday, 17 June 2021 Joint Sessions, Virtual Room 1 08:30 - 09:30 Joint SSP-EFP Session COVID-19 Chair: Michael Tamm (Basel, Switzerland) Chair: Zouhair Souissi (Tunis, Tunisia) 08:30 - 08:40 Short 2021 update on treatment options in COVID19 Alexandra Calmy (Geneva, Switzerland) 08:40 - 08:50 COVID in children: (including multisystem inflammatory syndrome) Arnaud L’Huillier (Geneva, Switzerland) 08:50 - 09:00 Acute respiratory failure in COVID patients outside the ICU Dan Adler (Geneva, Switzerland) 09:00 - 09:10 COVID and vascular disease (vasculitis, thromboembolic disorders..) Marc Righini (Geneva, Switzerland) 09:10 - 09:20 Swiss COVID lung study Manuela Funke-Chambour (Bern, Switzerland) 09:20 - 09:30 Q & A Joint Sessions, Virtual Room 2 08:30 - 09:30 Joint SSP-EFP Session Sleep disordered breathing 1 Chair: Robert Thurnheer (Münsterlingen, Switzerland) Chair: Quy Ngo Chau (Hanoi, Viet Nam) 08:30 - 08:50 New Swiss recommendations 2020 for the diagnosis and treatment of sleep apnoea Raphaël Heinzer (Lausanne, Switzerland) 08:50 - 09:05 Residual sleepiness in patients treated for sleep apnoea Jean-Louis Pepin (Grenoble, France) 09:05 - 09:20 New treatments for OSA Malcolm Kohler (Zürich, Switzerland) 09:20 - 09:30 Q & A Joint Sessions, Virtual Room 3 08:30 - 09:30 Joint SSP-EFP Session E-cigarettes Chair: Macé Schuurmans (Winterthur, Switzerland) Chair: Florin Mihaltan (Bucharest, Romania) Page 1 / 18 Scientific Programme 08:30 - 08:45 Toxicity of E-Cigarettes Philippe Camus (Dijon, France) 08:45 - 09:00 E-cigarettes and „Heat not burn devices“: an individual opportunity, but risks for society Jacques Cornuz (Lausanne, Switzerland) 09:00 - 09:15 Impact of e-cigarettes on smoking in adolescents Jürg Barben (St. -

Zurich University of Applied Sciences School of Management and Law Winterthur

Zurich University of Applied Sciences School of Management and Law Winterthur Bachelor’s Thesis Introduction of Capacity Mechanisms in European Energy Markets: Implications for Swiss Market Participants Supervisor Johanna Cludius Author Casper Erik Wilbers Einfangstrasse 19 8406 Winterthur [email protected] S12467338 Winterthur, 22. Mai 2015 Casper Erik Wilbers Declaration of authorship I hereby declare that this thesis is my own work, that it has been generated by me without the help of others and that all sources are clearly referenced. I further declare that I will not supply any copies of this thesis to any third parties without written permission by the director of this degree program. I understand that the Zurich University of Applied Sciences (ZHAW) reserves the right to use plagiarism detection software to make sure that the content of this thesis is completely original. I hereby agree for this thesis, naming me as its author, to be sent abroad for this purpose, where it will be kept in a database to which this university has sole access. I also understand that I will be entitled at any time to ask for my name and any other personal data to be deleted. Furthermore, I understand that pursuant to § 16 (1) in connection with § 22 (2) of the federal law on universities of applied sciences (FaHG) all rights to this thesis are assigned to the ZHAW, except for the right to be identified as its author. Student’s name (in block letters) Casper Erik Wilbers Student’s signature ………………………………………….. Bachelor’s Thesis - Introduction of Capacity Mechanisms in European Energy Markets i Casper Erik Wilbers Lecturer’s statement concerning publication This statement concerns the publication1) of the bachelor thesis “Introduction of Capacity Mechanisms in European Energy Markets: Implications for Swiss Market Participants”.