China Transportation Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Air China Limited

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular, you should consult a stockbroker or other registered dealer in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares of Air China Limited, you should at once hand this circular to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale was effected for transmission to the purchaser or the transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. AIR CHINA LIMITED (a joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 753) CONNECTED TRANSACTION: PURCHASE OF EQUITY INTEREST IN AIR CHINA CARGO FROM CAPITAL AIRPORTS HOLDING COMPANY Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders A letter from the Board is set out on pages 4 to 8 of this circular and a letter from the Independent Board Committee is set out on pages 9 to 10 of this circular. A letter of advice from Kingsway Capital Limited, the Independent Financial Adviser, containing its advice to the Independent Board Committee and the independent Shareholders of the Company is set out on pages 11 to 17 of this circular. -

Beijing Capital International Airport Co., Ltd. 02 01 2016 Corporate Social Responsibility Report Beijing Capital International Airport Co., Ltd

1 Beijing Capital International Airport Co., Ltd. 02 01 2016 Corporate Social Responsibility Report Beijing Capital International Airport Co., Ltd. About the Report Dear readers, this report reflects BCIA's practice and performance in fulfilling its social responsibility in 2016. We hope to present, via this report, BCIA's ideas and practices in terms of corporate social responsibility, and in the meanwhile, communicate with stakeholders in an honest and transparent way to promote sustainable development of BCIA. Reporting Period Scope of Report Reporting Release Cycle Data Sources The reporting period spans the calendar year from January 1, 2016 The main body of the report is Beijing Capital International Airport This is an annual report, and is the 6th consecutive CSR report Financial data of this report come from the audited BCIA Annual to December 31, 2016, and also includes contents and data that pre- Co., Ltd., including administration supporting departments in charge published by BCIA. Report. Other data come from formal internal documents and dates the stated reporting period. of the company. statistics of BCIA. Report Compilation Principles Reference Access to this Report Environmental, Social and Governance Reporting Guidance (HK-ESG) issued by Hong Kong Stock Exchange For the convenience of indication and reading, the "Beijing Capital http://www.bcia.com.cn/investor/csr.shtml Global Reporting Initiative's (GRI) International Airport Co., Ltd." in this report is also referred to as You can download the electronic version of the report from our GB/T 36001 Guidance on Social Responsibility Reporting "We", "the Company" or "the Capital Airport". "Capital Airport website: http://www.bcia.com.cn/investor/csr.shtml ISO26000: Guidance on Social Responsibility issued by International Organization for Standardization Group" in the report refers to Capital Airport Holding Company and If you need the paper version or have any suggestions, please contact us. -

2019 Corporate Social Responsibility Report

2019 企业社会责任报告 CORPORATE SOCIAL RESPONSIBILITY REPORT 北京首都国际机场股份有限公司 About the Report This report reflects the practice and performance of Beijing Capital International Airport Co., Ltd. in fulfilling its social responsibility in 2019. We hope to present, via this report, our CSR ide- as and practices and communicate with stakeholders in an honest and transparent way, so as to promote our sustainable development. Reference For better readability, the “Beijing Capital International Airport Co., Ltd.” in this report is also referred to as “BCIA” “the Company” or “we”. “CAH” in the report refers to Capital Airports Holding Company and all its wholly-owned or holding subsidiaries. Reporting Period The reporting period spans the calendar year from January 1, 2019 to December 31, 2019, and also includes some contents and data that predates the stated reporting period. Reporting Cycle This annual report is the 9th CSR report published by BCIA consecutively. Reporting Scope The main reporter is Beijing Capital International Airport Co., Ltd., including all the management and supporting departments of the Company. Compilation Principles This report is prepared in accordance with the GRI Sustainability Reporting Standards (GRI Standards) issued by the Global Sustainability Standards Board (GSSB). It also refers to the re- quirements of the UN Sustainable Development Goals (SDGs), ISO 26000: Guidance on Social Responsibility issued by International Organization for Standardization and Environmental, Social and Governance Reporting Guide (HK-ESG) issued by the Stock Exchange of Hong Kong Ltd. Data Sources The financial data of this report is extracted from the audited BCIA Annual Report. Other data comes from formal internal documents and statistics of BCIA. -

UNITED STATES BANKRUPTCY COURT Southern District of New York *SUBJECT to GENERAL and SPECIFIC NOTES to THESE SCHEDULES* SUMMARY

UNITED STATES BANKRUPTCY COURT Southern District of New York Refco Capital Markets, LTD Case Number: 05-60018 *SUBJECT TO GENERAL AND SPECIFIC NOTES TO THESE SCHEDULES* SUMMARY OF AMENDED SCHEDULES An asterisk (*) found in schedules herein indicates a change from the Debtor's original Schedules of Assets and Liabilities filed December 30, 2005. Any such change will also be indicated in the "Amended" column of the summary schedules with an "X". Indicate as to each schedule whether that schedule is attached and state the number of pages in each. Report the totals from Schedules A, B, C, D, E, F, I, and J in the boxes provided. Add the amounts from Schedules A and B to determine the total amount of the debtor's assets. Add the amounts from Schedules D, E, and F to determine the total amount of the debtor's liabilities. AMOUNTS SCHEDULED NAME OF SCHEDULE ATTACHED NO. OF SHEETS ASSETS LIABILITIES OTHER YES / NO A - REAL PROPERTY NO 0 $0 B - PERSONAL PROPERTY YES 30 $6,002,376,477 C - PROPERTY CLAIMED AS EXEMPT NO 0 D - CREDITORS HOLDING SECURED CLAIMS YES 2 $79,537,542 E - CREDITORS HOLDING UNSECURED YES 2 $0 PRIORITY CLAIMS F - CREDITORS HOLDING UNSECURED NON- YES 356 $5,366,962,476 PRIORITY CLAIMS G - EXECUTORY CONTRACTS AND UNEXPIRED YES 2 LEASES H - CODEBTORS YES 1 I - CURRENT INCOME OF INDIVIDUAL NO 0 N/A DEBTOR(S) J - CURRENT EXPENDITURES OF INDIVIDUAL NO 0 N/A DEBTOR(S) Total number of sheets of all Schedules 393 Total Assets > $6,002,376,477 $5,446,500,018 Total Liabilities > UNITED STATES BANKRUPTCY COURT Southern District of New York Refco Capital Markets, LTD Case Number: 05-60018 GENERAL NOTES PERTAINING TO SCHEDULES AND STATEMENTS FOR ALL DEBTORS On October 17, 2005 (the “Petition Date”), Refco Inc. -

Rural Migrants in Shanghai

The Making of the Chinese Working Class: Rural Migrants in Shanghai by Li Ma This thesis/dissertation document has been electronically approved by the following individuals: Nee,Victor (Chairperson) Swedberg,Richard (Minor Member) Strang,David (Minor Member) THE MAKING OF THE CHINESE WORKING CLASS: RURAL MIGRANTS IN SHANGHAI A Dissertation Presented to the Faculty of the Graduate School of Cornell University In Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy by Li Ma August 2010 © 2010 Li Ma THE MAKING OF THE CHINESE WORKING CLASS: RURAL MIGRANTS IN SHANGHAI Li Ma, Ph. D. Cornell University 2010 My dissertation analyzes the institutional mechanisms that cause the persistence of class and status inequalities between rural migrants and urban residents in post- socialist Shanghai. I examine how remnants of China’s socialist institutions , after the gradualist market reform, continue to stratify rural migrants and their second generation through sociopolitical processes. Making two thirds of the labor force nowadays in China, rural migrants experience social forces in China’s emerging market capitalism as well as repercussions from the socialist legacy. Drawing from historical archives and a 12-month ethnographic fieldwork in Shanghai, I demonstrate how rules, norms, organizations and beliefs in contemporary Chinese society make rural or urban residence identities the most salient sites of social distinction. I examine the blending and segregating processes of rural migrants’ life in the city. I also analyze how rural migrants respond to social exclusion with a variety of strategies. I argue that since rural migrants and urban residents have been classified into two different forms of citizenship that were deeply rooted in the ideological and organizational structures of Chinese socialism. -

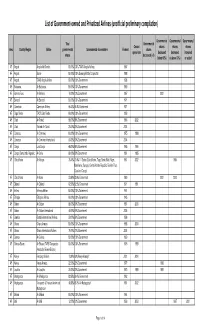

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

Corporate Social Responsibility Report 2017

CORPORATE SOCIAL RESPONSIBILITY REPORT 2017 Beijing Capital International Airport Co., Ltd. CONTECONTENTSNTS About the Report 02 Message from the Chairman 04 Figures in 2017 06 Prosperity in a New Era 08 The guideline of the 19th CPC National Con- gress leads national gateway’s development 10 towards a new stage 01 Building an International Hub Connecting 12 the World 02 Gathering Strength to Build a Safe Airport 20 03 Building a Green Airport with Perseverance 30 04 Building a Smart Airport through Innovation 40 05 Providing Sincere Service to Build a Hu- 48 man-oriented Airport About Us Company Profile 60 Corporate Governance 61 Responsibility Management 63 Honors 65 Outlook 66 Key Performance Indicators 68 HK-ESG Index 69 Reader Feedback 72 Corporate Social Responsibility Report 2017 CORPORATE SOCIAL 02 Beijing Capital International Airport Co., Ltd. 2017 RESPONSIBILITY REPORT 03 About the Report This report reflects Beijing Capital International Airport Co., Ltd. (BCIA)'s practice and performance in fulfill- ing its social responsibility in 2017. We hope to present, via this report, BCIA's ideas and practices in terms of corporate social responsibility, and in the meanwhile, communicate with stakeholders in an honest and trans- Data Sources Reference parent way to promote sustainable development of BCIA. The financial data of this report was extracted from For the convenience of indication and reading, the the audited BCIA Annual Report. Other data comes “Beijing Capital International Airport Co., Ltd.” in from formal internal documents and statistics of this report is also referred to as “We”, “the Com- BCIA. pany” or “the Capital Airport”. -

Download Article

Advances in Economics, Business and Management Research, volume 21 3rd Annual International Conference on Management, Economics and Social Development (ICMESD 2017) Study on the Development Planning of Ji'nan Airport Logistics Park 1,a 2,b 1,c* Shan-Shan WANG , Kai DING , Xiao-Xue REN 1Shandong Jiaotong University, Ji'nan 250357, China 2Dalian Maritime University, Dalian 116026, China [email protected], [email protected], [email protected] *Xiao-Xue REN Keywords: Airport logistics park, Facilities planning, Operation. Abstract. With the rapid development of civil aviation and airport infrastructure, the airport logistics industry of China is in the initial stage of the strategy, its role in social and economic life is more and more important, and its development is a measure of the openness of China's market, the degree of economic development and make an important standard for the convenience of the material. The airport logistics park is an important part of modern logistics, and is the product of the effective combination of modern logistics and traditional air freight. Firstly, conception of development plan of Ji'nan Airport Logistics Park; secondly, in order to make the logistics park intensive function more powerful, more comprehensive, more to improve its service function and facilities planning; finally, This paper puts forward the design scheme of the development mode of Ji'nan airport logistics park, and puts forward the development mode of the airport logistics park. Introduction After decades of construction and development, China's civil aviation airport system has begun to take shape, and it formed in Beijing, Shanghai, Guangzhou and other hub airports as the center, taken Ji'nan, Chengdu, Kunming, Chongqing, Xi'an, Urumqi, Wuhan, Shenzhen, Shenyang, Hangzhou and other provincial capitals or key cities for the backbone of the backbone and the rest of the city. -

Strategy Report Hong Kong Equity Research

Thursday, 3 December, 2020 China Merchants Securities (HK) Co., Ltd. Strategy Report Hong Kong Equity Research 2021 Outlook: Road towards restoration Jessie Guo, PhD +852 3189 6121 [email protected] “Lives of great men all remind us, we can make our lives sublime. Let Edith Qian, CFA +852 3189 6752 us, then, be up and doing. With a heart for any fate, still achieving, still [email protected] pursuing; learn to labour and to wait”. Harrington Zhang, PhD - Henry Wadsworth Longfellow, A Psalm of Life +852 3189 6751 [email protected] Tommy Wong View on economic recovery +852 3189 6634 [email protected] The outbreak of COVID-19 sent global economic growth deep into negative Johnny Wong territory in 2020. Synchronised large-scale fiscal and monetary policies +852 3189 6357 prevented major economies from sliding into perennial recession. [email protected] According to the IMF, global GDP will contract by 4.4% in 2020 and rebound Yonghuo Liang +86 755 8290 4571 by 5.2% in 2021, but the pace of recovery will be uneven across countries. [email protected] We expect the US economy to have a relatively muted start next year, and Kevin Chen then followed by a brighter second half, while the Fed’s monetary policy will +852 3189 6125 remain abundantly accommodative throughout the entire 2021. [email protected] Felix Luo, PhD +852 3189 6288 We stay positive on China’s economic outlook, mainly driven by domestic [email protected] consumption and manufacturing investment. We expect a rather neutral Yiding Jiao, CFA fiscal and monetary policy stance. -

283936 (H Share Eng).Indb

Bank of Communications Co., Ltd. 2011 Annual Report Stock Code: 03328 No. 188, Yin Cheng Zhong Lu, Shanghai P.R. China Cheng Zhong Lu, Shanghai P.R. Yin No. 188, www.bankcomm.com Bank of Communications Co., Ltd. Company Profi le Founded in 1908, Bank of Communications Co., Ltd. is one of the oldest banks in China as well as one of the note-issuing banks in modern China. The Bank was listed on the Hong Kong Stock Exchange in June 2005 and on the Shanghai Stock Exchange in May 2007. The Bank currently has 155 domestic branches, comprising 30 provincial branches, 7 branches directly managed by the Head Offi ce and 118 managed by provinces. It has also established 2,637 operating locations in 173 cities and 112 counties nationwide. In addition, the Bank has set up 12 overseas institutions, comprising branches in Hong Kong, New York, Tokyo, Singapore, Seoul, Frankfurt, Macau, Ho Chi Minh City, Sydney and San Francisco, representative offi ce in Taipei and Bank of Communications (UK) Co., Ltd. According to the “Top 1000 World Banks 2011” published by the British magazine “The Banker”, the Bank was ranked number 35 based on its Tier 1 Capital. For the fi rst time, the Bank was also ranked among the top 25 banks worldwide in terms of profi t before tax with a ranking of number 24. The Bank is one of the major fi nancial services providers in China. The Bank’s business scope includes commercial banking, securities services, trust services, fi nancial leasing, fund management, insurance and offshore fi nancial services. -

Volume 7 , Issue 3 March 2005 CCAR

CHINA CIVIL AVIATION REPORT www.ChinaCivilAviation.com Volume 7, Issue 3 民 航 报 导 March 2005 Business Aviation China’s Premier Jet Charter Operator Speaks About the Market GA in China Takes a Forward Step New Baiyun Airport’s Parallel Runways Air China and Airbus’ Big Deal And More.... 民航报导是经由民航总局、国家新闻署核准,以《中国民用航空》英文版方式向全世界民航机构、企业,个人介绍中国 民航改革开放成果和现况的刊物,印刷和电子版本同步发行。免费订阅电子版本,请浏览www.ChinaCivilAviation.com 发行人:赵嘉国 联络地址:美国世兴公司 Uniworld LLC, 690 Garcia Ave., Suite A/B, Pittsburg, CA 94565, USA Tel: 925-439-3799 Fax: 925-439-3268 E-mail: [email protected] Anytime, Anywhere Contents 金鹿航空 Volume 7, issue 3 March 2005 Pg 2 News Briefs The Spark to Ignite the GA Fire a Reality Executive Flight Charter Service Civil Aviation Flight University of China Steps up Training Equipment Private Ownership of Aviation Transport Firms Now Possible Your World According to Your Schedule Capital Airport Holding Company’s New Goals Complete Cargo Station Opened at Chongqing Airport China Civil Aviation Report Low Rate of Delays Lufthansa Plane Wanders Off the Beaten Path, Literally Raytheon Enters Business Jet Arena Pg 5 Aircraft Update Air China and Airbus Sign Agreement for 20 A330-200s th The 6 ERJ145 Off the Assembly Line Chinese Firms to be Involved in A380 Production Air China Obtains 5 Bombardier Regional Jets Pg 6 Commercial Aviation Corner British Airways Increase Operation Capacity in China Shanghai Pudong Airport’s Second Runway Cleared for Operation Guangzhou New Baiyun Airport Reveals Parallel Landing Plans Cathay Pacifi c Looking to Cement -

TIANANMEN: CHINA's STRUGGLE for DEMOCRACY ITS PRELUDE, DEVELOPMENT, AFTERMATH, and Impacf

OccAsioNAl PApERS/ REpRiNTS SERiES iN CoNTEMpoRARY AsiAN STudiEs NUMBER 2 - 1990 (97) TIANANMEN: CHINA'S STRUGGLE FOR , DEMOCRACY , •• ITS PRELUDE, DEVELOPMENT, AFTERMATH, AND IMPACT Edited by Winston L. Y. Yang and Marsha L. Wagner Scltool of LAw UNivERsiTy of 0 MARylANd. c ' 0 Occasional Papers/Reprint Series in Contemporary Asian Studies General Editor: Hungdah Chiu Executive Editor: Chih-Yu Wu Managing Editor: Chih-Yu Wu Editorial Advisory Board Professor Robert A. Scalapino, University of California at Berkeley Professor Gaston J. Sigur, George Washington University Professor Shao-chuan Leng, University of Virginia Professor James Hsiung, New York University Dr. Lih-wu Han, Political Science Association of the Republic of China Professor J. S. Prybyla, The Pennsylvania State University Professor Toshio Sawada, Sophia University, Japan Professor Gottfried-Karl Kindermann, Center for International Politics, University of Munich, Federal Republic of Germany Professor Choon-ho Park, International Legal Studies, Korea University, Republic of Korea All contributions (in English only) and communications should be sent to Professor Hungdah Chiu, University of Maryland School of Law, 500 West Baltimore Street, Baltimore, Maryland 21201 USA. All publications in this series reflect only the views of the authors. While the editor accepts responsibility for the selection of materials to be published, the individual author is responsible for statements of facts and expressions of opinion con tained therein. Subscription is US $18.00 for 6 issues (regardless of the price of individual issues) in the United States and $24.00 for Canada or overseas. Check should be addressed to OPRSCAS. Price for single copy of this issue: US $8.00.