Change and Opportunity Retail Foods China

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Is a High Refund Strategy Always Effective?

Is a High Refund Strategy Always Effective? Shueh-Chin Ting, Professor, Department of Education, National University of Tainan, Taiwan ABSTRACT Retailers often use a refund strategy to guarantee that their products are the lowest price. However, does a high refund strategy announced by retailers definitively help consumers to believe that their products have the lowest price? Hierarchical moderator regression analysis was used to examine the moderating effect of a retailer’s reputation on the relationship between refund size and the believability of the lowest price. The results indicate that refund size has no direct effect on the believability of the lowest price and the effect is moderated by a retailer’s reputation. For reputable retailers, refund size has a positive influence on the believability of the lowest price. For less reputable retailers, refund size has a negative influence on the believability of the lowest price. Prior studies neglected the importance of a retailer’s reputation in implementing refund strategies. This study has resolved this research gap. Keywords: believability of the lowest price, guarantee strategy, refund size, retailer’s reputation. INTRODUCTION Retailers often use low-price guarantees (LPGs) as a signal to attract consumers and increase sales. Consumers interpret LPGs as signals that a particular retailer is committed to low prices (Borges, and Babin, 2012). Price-matching guarantees (PMGs) are commonly used by retailers as promises to match the lowest price for an item that a customer can find elsewhere (Yuan and Krishna, 2011). Signaling theory has been used to understand the overall effect of a PMG on consumer perceptions (Borges, 2009). -

151016 CB China Power of Retailing 2015 CN.Docx

China Power of Retailing 2015 China Power of Retailing 2015 1 Foreword 2015 has witnessed the recovery of a global economy and the gradual stabilization of a real economy in China. While the Eurozone economy continues to improve, the differentiation among its economies remains noticeable. “Abeconomics” throws Japan into deep recession. The United States of America, as the only exception, enters the trajectory of a strong recovery and the US dollar has appreciated sharply against other major world currencies. Its well-anticipated rise in interest rate in the fourth quarter forebodes an accelerated devaluation of currencies in most emerging economies. As a result, the pressure on devaluating RMB is mounting. With a slowed growth rate, the Chinese economy has arrived at the stage of new normal. The YoY growth for the first half of the year lingers around 7%, hindered by the deceleration of the three engines that used to propel GDP growth – a sluggish export, a slow growth in investment and a domestic consumption that continues to fall behind expectation. Although the growth rate of the total retail of consumer goods has dropped, it has far outpaced the domestic industrial growth. With the consumer confidence seeing constant improvement that will further free up consumption potential, consumption is expected to continue pulling the economy in the future. A continued fall in oil prices has offset the inflationary pressure, curbing the inflation at a lower level to make room for executing a lax monetary policy. To further boost investment and consumption, and reduce enterprise financing costs, the government has gradually redirected its macro economy from “stabilize growth and adjust structure” to “ensure growth,” making the lowering of interest rate and reserve ratio possible in the second half of the year. -

Merger Control 2018 Seventh Edition

Merger Control 2018 Seventh Edition Contributing Editors: Nigel Parr & Ross Mackenzie GLOBAL LEGAL INSIGHTS – MERGER CONTROL 2018, SEVENTH EDITION Editors Nigel Parr & Ross Mackenzie, Ashurst LLP Production Editor Andrew Schofi eld Senior Editors Suzie Levy Caroline Collingwood Group Consulting Editor Alan Falach Publisher Rory Smith We are extremely grateful for all contributions to this edition. Special thanks are reserved for Nigel Parr & Ross Mackenzie for all their assistance. Published by Global Legal Group Ltd. 59 Tanner Street, London SE1 3PL, United Kingdom Tel: +44 207 367 0720 / URL: www.glgroup.co.uk Copyright © 2018 Global Legal Group Ltd. All rights reserved No photocopying ISBN 978-1-912509-17-1 ISSN 2048-1292 This publication is for general information purposes only. It does not purport to provide comprehensive full legal or other advice. Global Legal Group Ltd. and the contributors accept no responsibility for losses that may arise from reliance upon information contained in this publication. This publication is intended to give an indication of legal issues upon which you may need advice. Full legal advice should be taken from a qualifi ed professional when dealing with specifi c situations. The information contained herein is accurate as of the date of publication. Printed and bound by CPI Group (UK) Ltd, Croydon, CR0 4YY June 2018 CONTENTS Preface Nigel Parr & Ross Mackenzie, Ashurst LLP General chapter Anti-competitive buyer power under UK and EC merger control – too much of a good thing? Burak Darbaz, Ben Forbes & Mat Hughes, AlixPartners UK LLP 1 Country chapters Albania Anisa Rrumbullaku, CR PARTNERS 19 Australia Sharon Henrick & Wayne Leach, King & Wood Mallesons 24 Austria Astrid Ablasser-Neuhuber & Gerhard Fussenegger, bpv Hügel Rechtsanwälte GmbH 39 Canada Micah Wood & Kevin H. -

Global Powers of Retailing 2019 Contents

Global Powers of Retailing 2019 Contents Top 250 quick statistics 4 Global economic outlook 5 Top 10 highlights 8 Global Powers of Retailing Top 250 11 Geographic analysis 19 Product sector analysis 23 New entrants 27 Fastest 50 30 Study methodology and data sources 35 Endnotes 39 Contacts 41 Welcome to the 22nd edition of Global Powers of Retailing. The report identifies the 250 largest retailers around the world based on publicly available data for FY2017 (fiscal years ended through June 2018), and analyzes their performance across geographies and product sectors. It also provides a global economic outlook, looks at the 50 fastest-growing retailers, and highlights new entrants to the Top 250. Top 250 quick statistics, FY2017 Minimum retail US$4.53 US$18.1 revenue required to be trillion billion among Top 250 Aggregate Average size US$3.7 retail revenue of Top 250 of Top 250 (retail revenue) billion 5-year retail Composite 5.7% revenue growth net profit margin 5.0% Composite (CAGR from Composite year-over-year retail FY2012-201 2.3% return on assets revenue growth 3.3% Top 250 retailers with foreign 23.6% 10 operations Share of Top 250 Average number aggregate retail revenue of countries where 65.6% from foreign companies have operations retail operations Source: Deloitte Touche Tohmatsu Limited. Global Powers of Retailing 2019. Analysis of financial performance and operations for fiscal years ended through June 2018 using company annual reports, Supermarket News, Forbes America’s largest private companies and other sources. 4 Global economic outlook 5 Global Powers of Retailing 2019 | Global economic outlook The global economy is currently at a turning point. -

1 Abundant Glory Limited British Virgin Islands Executive

Appendix B Present Directorships of Edith SHIH as at effective date of appointment Role Name of Company Place of Incorporation (Executive / Non-Executive) 1 Abundant Glory Limited British Virgin Islands Executive 2 Actionfirm Limited British Virgin Islands Executive 3 AICT Advisory Limited British Virgin Islands Executive Alexandria International Container Terminals 4 Egypt Executive Company S.A.E. 5 Alpha Metrics Limited British Virgin Islands Executive 6 Americas Intermodal Services SA/NV Belgium Executive 7 Americas Shipyard SA/NV Belgium Executive 8 Amsterdam Container Terminals B.V. Netherlands Executive 9 Amsterdam Marine Terminals B.V. Netherlands Executive 10 Amsterdam Port Holdings B.V. Netherlands Executive 11 Anovio Holdings Limited Cyprus Executive 12 APM Terminals Dachan Company Limited Hong Kong Executive 13 Aqaba Terminal Services Limited British Virgin Islands Executive 14 Asia Pacific Honour Holdings Limited British Virgin Islands Executive 15 Bajacorp, S.A. de C.V. Mexico Executive 16 Barcelona Europe South Terminal, S.A. Spain Executive 17 Best Fortune S.a r.l. Luxembourg Executive 18 Best Month Profits Limited British Virgin Islands Executive 19 Best Oasis Holdings Limited British Virgin Islands Executive 20 Best People Resources Limited British Virgin Islands Executive 21 Beyond Excel Investments Limited British Virgin Islands Executive 22 Brightease Profits Limited British Virgin Islands Executive 23 Brisbane Container Terminals Pty Limited Australia Executive Appendix B 24 Buenos Aires Container Terminal Services S.A. Argentina Alternate Director 25 Cape Fortune B.V. Netherlands Executive 26 Central America Shipyard SA/NV Belgium Executive 27 China Terminal Services Holding Company Limited Bermuda Executive 28 Clivedon Limited British Virgin Islands Executive 29 CLK Limited British Virgin Islands Executive 30 Coastal Work Logistics Limited British Virgin Islands Executive 31 Container Security Inc. -

GFSI : Overview and GFSI : Overview and Comparaison of Comparaison Of

GFSI : Overview and comparaison of schemes CMC May 5, 2011 GFSI Background In 2000….. ¾ FdFood saftfetycrises ¾ Profileration of individual retailer schemes ¾ Burden to suppliers and producers due to frequent audits ¾ Lack of efficiency and high costs in the food supply chain Global Food Safety Initiative ¾ GFSI lhdlaunched at the CIES AlAnnual Congress in 2000, following a directive from the food business CEOs. ¾ Food Safety was then, and is still, top of mind with consumers. Consumer trust needs to be strengthened and maintained, while making the suppl y chain safer. ¾ Managed by The Consumer Goods Forum GFSI managed by The Consumer Goods Forum ¾ An independent global parity‐based Consumer Goods network ¾ Over 650 Members ¾ Representing 70 countries ¾ Over 3 continents Paris, HQ Washington D.C. Tokyo €2.1 trillion THE CONSUMER GOODS FORUM BOARD OF DIRECTORS MANUFACTURER RETAILER COLLEGE COLLEGE 25 25 CEOsCOs CEOsCOs Retailer College Manufacturer College « Safe Food for Consumers Everywhere » GFSI Mission Driving continuous improvement in food safety to strengthen consumer confidence worldwide GFSI Objectives Reduce food safety risks Manage cost GFSI Develop competencies Knowledge exchange and capacity building and networking How does GFSI work? ¾ Benchmarks existing food safety schemes, including pre‐farm gate schemes against the GFSI Guidance Document. ¾ Determines whether a scheme is equivalent to the Guidance Document requirements. ¾ Helps and encourages food safety stakeholders to share knowledge and strategy for food safety and to develop best food safety practice in a common global framework. What GFSI Does NOT Do ¾ Make policy for retailers or manufacturers ¾ Make policy for standard owners ¾ Undertake any accreditation or certification activities ¾ Have involvement with an area outside the scope of food safety i.e. -

Global Powers of Retailing Top 250, FY2015

Global Powers of Retailing 2017 | Top 250 Global Powers of Retailing Top 250, FY2015 FY2015 FY2015 Parent Parent FY2010- FY2015 FY2015 company/ company/ # 2015 Retail Retail group group Countries Retail revenue Country revenue revenue¹ net income¹ of revenue rank Company of origin (US$M) (US$M) (US$M) Dominant operational format operation CAGR² 1 Wal-Mart Stores, Inc. US 482,130 482,130 15,080 Hypermarket/Supercenter/Superstore 30 2.7% 2 Costco Wholesale Corporation US 116,199 116,199 2,409 Cash & Carry/Warehouse Club 10 8.3% 3 The Kroger Co. US 109,830 109,830 2,049 Supermarket 1 6.0% 4 Schwarz Unternehmenstreuhand KG Germany 94,448 94,448 n/a Discount Store 26 7.4% 5 Walgreens Boots Alliance, Inc. US 89,631 103,444** 4,279 Drug Store/Pharmacy 10 5.9% (formerly Walgreen Co.) 6 The Home Depot, Inc. US 88,519 88,519 7,009 Home Improvement 4 5.4% 7 Carrefour S.A. France 84,856 87,593 1,247 Hypermarket/Supercenter/Superstore 35 -3.1% 8 Aldi Einkauf GmbH & Co. oHG Germany 82,164e 82,164e n/a Discount Store 17 8.0% 9 Tesco PLC UK 81,019 82,466 535 Hypermarket/Supercenter/Superstore 10 -2.3% 10 Amazon.com, Inc. US 79,268 107,006 596 Non-Store 14 20.8% 11 Target Corporation US 73,785 73,785 3,363 Discount Department Store 1 2.3% 12 CVS Health Corporation US 72,007 153,290 5,239 Drug Store/Pharmacy 3 4.7% 13 Metro Ag Germany 68,066** 68,066** 821 Cash & Carry/Warehouse Club 31 -2.5% 14 Aeon Co., Ltd. -

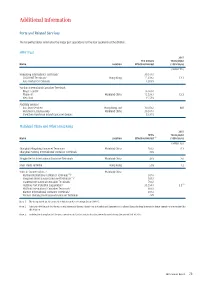

Additional Information

additional Information ports and related services The following tables summarise the major port operations for the four segments of the division. HpH trust 2015 The Group’s Throughput Name Location Effective Interest (100% basis) (million TEU) Hongkong International Terminals/ 30.07% / COSCO-HIT Terminals/ Hong Kong 15.03% / 12.1 Asia Container Terminals 12.03% Yantian International Container Terminals - Phase I and II/ 16.96% / Phase III/ Mainland China 15.53% / 12.2 West Port 15.53% Ancillary Services - Asia Port Services/ Hong Kong and 30.07% / N/A Hutchison Logistics (HK)/ Mainland China 30.07% / Shenzhen Hutchison Inland Container Depots 23.35% Mainland China and other Hong Kong 2015 HPH’s Throughput Name Location Effective Interest (1) (100% basis) (million TEU) Shanghai Mingdong Container Terminals/ Mainland China 50% / 8.3 Shanghai Pudong International Container Terminals 30% Ningbo Beilun International Container Terminals Mainland China 49% 2.0 River Trade Terminal Hong Kong 50% 1.2 Ports in Southern China - Mainland China (2) Nanhai International Container Terminals / 50% / (2) Jiangmen International Container Terminals / 50% / Shantou International Container Terminals/ 70% / (3) Huizhou Port Industrial Corporation/ 33.59% / 2.5 Huizhou International Container Terminals/ 80% / Xiamen International Container Terminals/ 49% / Xiamen Haicang International Container Terminals 49% Note 1: The Group holds an 80% interest in Hutchison Ports Holdings Group (“HPH”). Note 2: Although HPH Trust holds the economic interest in the two River Ports in Nanhai and Jiangmen in Southern China, the legal interests in these operations are retained by this division. Note 3: Includes the throughput of the port operations in Gaolan and Jiuzhou that were disposed during the second half of 2015. -

China - Peoples Republic Of

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 1/26/2011 GAIN Report Number: CH0816 China - Peoples Republic of Post: Shanghai ATO China Retail Annual Report Report Categories: Retail Food Sector Approved By: Keith Schneller Prepared By: Leanne Wang, May Liu, Tong Wang and ATO-Chengdu Report Highlights: With increased disposal income, urbanization and food safety concerns, Chinese are consuming more U.S. food products; this is partly due to the excellent quality and safety reputation of American food products. While the Chinese economy has slowed this past year, it is still growing faster than any other major economy. This fact and Chinese customers‟ growing taste for imported products, makes the Chinese market very attractive to many U.S. food producers. Executive Summary In response to rising inflation and food safety concerns, more Chinese people are cutting back on eating out and are now cooking more and more at home. Consumers of imported food are generally expatriates and high and upper –middle income locals. They are least affected by inflation and pay great attention to food safety. Consumption of western style products continues to grow as they generally are regarded as good quality, nutritious and safe. Some products, such as fresh fruit, frozen vegetables and nuts, have much deeper penetration, and some supermarkets and convenience stores are becoming more interested in imported products. Rapid economic growth has caused the total U.S. dollar sales value of food and beverages to rise by 26.2% to USD132 billion in 2008. -

SUSTAINABILITY, SOCIAL MEDIA… and the FUTURE of RETAIL

THE COCA-COLA RETAILING RESEARCH Councils SUSTAINABILITY, SOCIAL MEDIA… AND THE FUTURE OF RETAIL Global Retail Summit London, August 2012 The first Coca-Cola Retailing Research Council was formed in 1978 in North America to help retail customers address industry issues through organized discussion and commissioned research. Today, the Company sponsors six Councils throughout the world: North America, NACS North America, Europe, Asia, Latin America, and Eurasia & Africa. Each Council is comprised of up to 20 retail leaders and non-voting Coca-Cola system executives. Widely considered to be among the industry’s most prestigious retail think tanks, the Coca-Cola Retailing Research Councils have published more than 50 proprietary studies on issues ranging from shopper insights and new market dynamics to technology, innovation and social media. THIS PUBLIcatION IS A COLLECTION OF PAPers PRODUCED FROM PresentatIONS at GLOBAL RetaIL SUMMIT. Panel DIscUSSIONS DURIng THE SUMMIT WERE NOT RECORDED. © 2012 THE COCA-COla EXPOrt CORPOratION, UNDER THE AUSPIces OF THE COCA-COla RetaILIng ResearcH COUncIls CONTENTS FOREWORD FACING UP TO NEW REALITIES Muhtar Kent PAGE 2 SUSTAINABILITY THE CHALLENGE FOR RETAILERS HRH Prince Charles PAGE 4 WELCOME TO THE NEW NORMAL Lord Deben PAGE 8 THE QUEST FOR CHANGE Carter Roberts PAGE 12 WHY LESS HAS TO MEAN MORE Dr Jason Clay PAGE 16 SOCIAL MEDIA BACK TO THE FUTURE? James Quarles PAGE 22 BE YOURSELF… SIMPLY FLAWSOME Wendy Clark PAGE 28 IT PAYS TO TALK. BUT KEEP IT RELEVANT… AND HONEST Richard Reed PAGE 30 THE FUTURE OF RETAILING HOW TO PREPARE FOR THE ‘PERFECT STORM’ Mark Price PAGE 34 SUMMARY THE PROMISE OF SUSTAINABLE GROWTH PAGE 38 LIST OF MEMBERS PAGE 40 CCRRC Global Retail Summit RepoRt FOREWORD FACING UP TO NEW REALITIES Muhtar Kent Chairman and Chief Executive Officer The Coca-Cola Company ince 1978, the Coca-Cola Retailing This is why I am convinced that sustaina- Research Council has generated over bility and social media will forever be con- 40 extensive, proprietary studies on nected at the hip. -

Chartered Secretaries American Express Credit Cards

Chartered Secretaries American Express Credit Cards Chartered Secretaries American Express® Platinum Credit Card and Chartered Secretaries American Express®Gold Credit Card are two co-branded cards that have been created in collaboration with The Hong Kong Institute of Chartered Secretaries (HKICS) and have been specifically designed to recognise and benefit our members. As a Member/Graduate/Student of HKICS, you are cordially invited to become a Chartered Secretaries American Express Platinum or Gold Card Cardmember. This card provides a highly convenient way to pay for HKICS membership fees, CPD events and seminars, examination fees and other fees. Application forms Exclusive privileges Merchants List Application forms Chartered Secretaries American Express Platinum Credit Card application form Chartered Secretaries American Express Gold Credit Card application form Application with required documents should be sent to: American Express International Inc Attn: New Accounts GPO Box 11250 Hong Kong Note: 1. Terms and conditions apply to the above offers and privileges. Please visit www.americanexpress.com.hk to learn more. 2. The Chartered Secretaries American Express co-branded Card is a privilege from HKICS. All Credit Card applicationapprovals will be at the sole discretion of American Express International Inc 3. For any enquiries, please call 2277 1370 Back to top Exclusive privileges: Chartered Secretaries American Express® Platinum Credit Card Half annualfee waiver saving you HK$800 a year Generous welcome offers including HK$500 Lane Crawford or Esso Synergy Fuel Cash Voucher, plus 10X Membership Rewards points in the first 3 months, up to 300,000 points Up to HK$500 travel package discount coupon when you purchasing travel packages from Farrington American Express Travel Services Ltd. -

Hong Kong Health and Beauty Retail Stores

Hong Kong Health and Beauty Retail Guide December 2014 Introduction With a wealthy population of 7 million and GDP of US$235 billion, Hong Kong is a large, high-value and expanding market for Australian consumer products, including beauty and health products. In 2013, A$132 million of Australian cosmetics and skin care were exported to Hong Kong. Australian cosmetic and skin care products have an international reputation as safe, environmentally friendly and consistently high quality. Australia is also recognised as a reliable source of quality cosmetics, skin care and health products, particularly in the natural and organic skincare categories. Hong Kong’s total sales in beauty and personal care products remained strong in 2013, reaching over HK$14.5 billion (over A$2 billion). Last year more than 50 million visitors, including some 40 million mainland Chinese, came to shop in Hong Kong, with cosmetics and skin care items a key focus. Hong Kong is a significant market in its own right and an excellent testing ground for international products entering the region. Austrade has launched a special video insights series to provide Australian beauty companies with first-hand perspectives from experts in the market. These videos provide advice on the latest market trends and tactics to be used in Hong Kong and China. Check it out from Austrade website. Table of Contents Page Number Overview of Hong Kong Distribution Channels - Beauty and Health Products 3 Hong Kong Health and Beauty Retail Stores Specialty Stores 4 Department Stores 5 Beauty Counters at Department Stores 6 Pharmacy Chains 8 Multi-brand Shops 8 Australian Concept Stores 9 Supermarkets 10 Austrade Contacts 12 November 2014 Austrade Health and Beauty Products Retail Stores in Hong Kong> 2 Overview of Hong Kong Distribution Channels - Beauty and Health Products Hong Kong has a sophisticated retail sector for the sale and distribution of health and beauty products.