US Options Margin

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Here We Go Again

2015, 2016 MDDC News Organization of the Year! Celebrating 161 years of service! Vol. 163, No. 3 • 50¢ SINCE 1855 July 13 - July 19, 2017 TODAY’S GAS Here we go again . PRICE Rockville political differences rise to the surface in routine commission appointment $2.28 per gallon Last Week pointee to the City’s Historic District the three members of “Team him from serving on the HDC. $2.26 per gallon By Neal Earley @neal_earley Commission turned into a heated de- Rockville,” a Rockville political- The HDC is responsible for re- bate highlighting the City’s main po- block made up of Council members viewing applications for modification A month ago ROCKVILLE – In most jurisdic- litical division. Julie Palakovich Carr, Mark Pierzcha- to the exteriors of historic buildings, $2.36 per gallon tions, board and commission appoint- Mayor Bridget Donnell Newton la and Virginia Onley who ran on the as well as recommending boundaries A year ago ments are usually toward the bottom called the City Council’s rejection of same platform with mayoral candi- for the City’s historic districts. If ap- $2.28 per gallon of the list in terms of public interest her pick for Historic District Commis- date Sima Osdoby and city council proved Giammo, would have re- and controversy -- but not in sion – former three-term Rockville candidate Clark Reed. placed Matthew Goguen, whose term AVERAGE PRICE PER GALLON OF Rockville. UNLEADED REGULAR GAS IN Mayor Larry Giammo – political. While Onley and Palakovich expired in May. MARYLAND/D.C. METRO AREA For many municipalities, may- “I find it absolutely disappoint- Carr said they opposed Giammo’s ap- Giammo previously endorsed ACCORDING TO AAA oral appointments are a formality of- ing that politics has entered into the pointment based on his lack of qualifi- Newton in her campaign against ten given rubberstamped approval by boards and commission nomination cations, Giammo said it was his polit- INSIDE the city council, but in Rockville what process once again,” Newton said. -

How Options Implied Probabilities Are Calculated

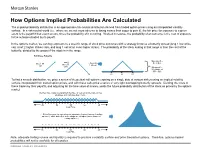

No content left No content right of this line of this line How Options Implied Probabilities Are Calculated The implied probability distribution is an approximate risk-neutral distribution derived from traded option prices using an interpolated volatility surface. In a risk-neutral world (i.e., where we are not more adverse to losing money than eager to gain it), the fair price for exposure to a given event is the payoff if that event occurs, times the probability of it occurring. Worked in reverse, the probability of an outcome is the cost of exposure Place content to the outcome divided by its payoff. Place content below this line below this line In the options market, we can buy exposure to a specific range of stock price outcomes with a strategy know as a butterfly spread (long 1 low strike call, short 2 higher strikes calls, and long 1 call at an even higher strike). The probability of the stock ending in that range is then the cost of the butterfly, divided by the payout if the stock is in the range. Building a Butterfly: Max payoff = …add 2 …then Buy $5 at $55 Buy 1 50 short 55 call 1 60 call calls Min payoff = $0 outside of $50 - $60 50 55 60 To find a smooth distribution, we price a series of theoretical call options expiring on a single date at various strikes using an implied volatility surface interpolated from traded option prices, and with these calls price a series of very tight overlapping butterfly spreads. Dividing the costs of these trades by their payoffs, and adjusting for the time value of money, yields the future probability distribution of the stock as priced by the options market. -

Tax Treatment of Derivatives

United States Viva Hammer* Tax Treatment of Derivatives 1. Introduction instruments, as well as principles of general applicability. Often, the nature of the derivative instrument will dictate The US federal income taxation of derivative instruments whether it is taxed as a capital asset or an ordinary asset is determined under numerous tax rules set forth in the US (see discussion of section 1256 contracts, below). In other tax code, the regulations thereunder (and supplemented instances, the nature of the taxpayer will dictate whether it by various forms of published and unpublished guidance is taxed as a capital asset or an ordinary asset (see discus- from the US tax authorities and by the case law).1 These tax sion of dealers versus traders, below). rules dictate the US federal income taxation of derivative instruments without regard to applicable accounting rules. Generally, the starting point will be to determine whether the instrument is a “capital asset” or an “ordinary asset” The tax rules applicable to derivative instruments have in the hands of the taxpayer. Section 1221 defines “capital developed over time in piecemeal fashion. There are no assets” by exclusion – unless an asset falls within one of general principles governing the taxation of derivatives eight enumerated exceptions, it is viewed as a capital asset. in the United States. Every transaction must be examined Exceptions to capital asset treatment relevant to taxpayers in light of these piecemeal rules. Key considerations for transacting in derivative instruments include the excep- issuers and holders of derivative instruments under US tions for (1) hedging transactions3 and (2) “commodities tax principles will include the character of income, gain, derivative financial instruments” held by a “commodities loss and deduction related to the instrument (ordinary derivatives dealer”.4 vs. -

Bond Futures Calendar Spread Trading

Black Algo Technologies Bond Futures Calendar Spread Trading Part 2 – Understanding the Fundamentals Strategy Overview Asset to be traded: Three-month Canadian Bankers' Acceptance Futures (BAX) Price chart of BAXH20 Strategy idea: Create a duration neutral (i.e. market neutral) synthetic asset and trade the mean reversion The general idea is straightforward to most professional futures traders. This is not some market secret. The success of this strategy lies in the execution. Understanding Our Asset and Synthetic Asset These are the prices and volume data of BAX as seen in the Interactive Brokers platform. blackalgotechnologies.com Black Algo Technologies Notice that the volume decreases as we move to the far month contracts What is BAX BAX is a future whose underlying asset is a group of short-term (30, 60, 90 days, 6 months or 1 year) loans that major Canadian banks make to each other. BAX futures reflect the Canadian Dollar Offered Rate (CDOR) (the overnight interest rate that Canadian banks charge each other) for a three-month loan period. Settlement: It is cash-settled. This means that no physical products are transferred at the futures’ expiry. Minimum price fluctuation: 0.005, which equates to C$12.50 per contract. This means that for every 0.005 move in price, you make or lose $12.50 Canadian dollar. Link to full specification details: • https://m-x.ca/produits_taux_int_bax_en.php (Note that the minimum price fluctuation is 0.01 for contracts further out from the first 10 expiries. Not too important as we won’t trade contracts that are that far out.) • https://www.m-x.ca/f_publications_en/bax_en.pdf Other STIR Futures BAX are just one type of short-term interest rate (STIR) future. -

Options Slide Deck Updated Version

www.levelupbootcamps.com 4/4/21 Derivatives Option Strategies 4/4/21 LevelUp, LLC©2021 All rights reserved 1 1 Derivatives & Currency Management Option Strategies 4/4/21 LevelUp, LLC©2021 All rights reserved 2 2 Level Up, LLC©2021 All rights reserved 1 www.levelupbootcamps.com 4/4/21 Risk Management with Options Synthetic Positions • Synthetic Long & Short Forward Option Strategies • Synthetic Puts & Calls Multiple Option Strategies Single Option + Underlying Single Option Directionless Volatility Long U/L Risk Reduction Writing Puts • Long Straddle = LC + LP Covered Call = U/L + SC • Lower purchase cost • Short Straddle = SC + SP • Income enhancement • Fiduciary put = SP + Money Spreads • Reduce at favorable price cash to cover (ftn 13) “Small Moves Up or Down” • Target price realization The Greeks • Bull & Bear Call Spreads • Manza Case 1. Delta + & - • Bear & Bull Put Spreads Protective Put = U/L + LP 2. Gamma + • Insurance Calendar Spreads 3. Theta (time) - Collar = U/L + LP + SC Short “Its all about Theta” 4. Vega (Implied Vol) + • Risk Reversal • Long Calendar Spread Portfolio Mgt • Short Calendar Spread Short U/L Risk Reduction 1. Strategies using • Short U/L + Long Call volatility & market view • Short U/L + Short Put 2. Adjusting risk exposure 4/4/21 LevelUp, LLC©2021 All rights reserved 3 3 Single Option Strategies Refresher . just in case + + X S Long Call – LC S Short Call – SC - - X “writing” Want U/L up – bullish Want U/L down – bearish Right to buy at strike price X Obligated to sell at strike price X Max gain = ∞ when S -

11 Option Payoffs and Option Strategies

11 Option Payoffs and Option Strategies Answers to Questions and Problems 1. Consider a call option with an exercise price of $80 and a cost of $5. Graph the profits and losses at expira- tion for various stock prices. 73 74 CHAPTER 11 OPTION PAYOFFS AND OPTION STRATEGIES 2. Consider a put option with an exercise price of $80 and a cost of $4. Graph the profits and losses at expiration for various stock prices. ANSWERS TO QUESTIONS AND PROBLEMS 75 3. For the call and put in questions 1 and 2, graph the profits and losses at expiration for a straddle comprising these two options. If the stock price is $80 at expiration, what will be the profit or loss? At what stock price (or prices) will the straddle have a zero profit? With a stock price at $80 at expiration, neither the call nor the put can be exercised. Both expire worthless, giving a total loss of $9. The straddle breaks even (has a zero profit) if the stock price is either $71 or $89. 4. A call option has an exercise price of $70 and is at expiration. The option costs $4, and the underlying stock trades for $75. Assuming a perfect market, how would you respond if the call is an American option? State exactly how you might transact. How does your answer differ if the option is European? With these prices, an arbitrage opportunity exists because the call price does not equal the maximum of zero or the stock price minus the exercise price. To exploit this mispricing, a trader should buy the call and exercise it for a total out-of-pocket cost of $74. -

OPTION-BASED EQUITY STRATEGIES Roberto Obregon

MEKETA INVESTMENT GROUP BOSTON MA CHICAGO IL MIAMI FL PORTLAND OR SAN DIEGO CA LONDON UK OPTION-BASED EQUITY STRATEGIES Roberto Obregon MEKETA INVESTMENT GROUP 100 Lowder Brook Drive, Suite 1100 Westwood, MA 02090 meketagroup.com February 2018 MEKETA INVESTMENT GROUP 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA 02090 781 471 3500 fax 781 471 3411 www.meketagroup.com MEKETA INVESTMENT GROUP OPTION-BASED EQUITY STRATEGIES ABSTRACT Options are derivatives contracts that provide investors the flexibility of constructing expected payoffs for their investment strategies. Option-based equity strategies incorporate the use of options with long positions in equities to achieve objectives such as drawdown protection and higher income. While the range of strategies available is wide, most strategies can be classified as insurance buying (net long options/volatility) or insurance selling (net short options/volatility). The existence of the Volatility Risk Premium, a market anomaly that causes put options to be overpriced relative to what an efficient pricing model expects, has led to an empirical outperformance of insurance selling strategies relative to insurance buying strategies. This paper explores whether, and to what extent, option-based equity strategies should be considered within the long-only equity investing toolkit, given that equity risk is still the main driver of returns for most of these strategies. It is important to note that while option-based strategies seek to design favorable payoffs, all such strategies involve trade-offs between expected payoffs and cost. BACKGROUND Options are derivatives1 contracts that give the holder the right, but not the obligation, to buy or sell an asset at a given point in time and at a pre-determined price. -

Oil and Gas Futures and Options Market UDC: 550.8:552.1 DOI: 10.17794/Rgn.2017.4.5

45 The Mining-Geology-Petroleum Engineering Bulletin Oil and Gas Futures and Options Market UDC: 550.8:552.1 DOI: 10.17794/rgn.2017.4.5 Review scientiƤ c paper Ante Nosi©1; Daria Karasalihovi© Sedlar2; Lucija Juki©3 1 INA Industrija nafte d.d., V.Holjevca 10, 10 000 Zagreb, Master of Pet. Eng. 2 University of Zagreb, Faculty of Mining, Geology and Petroleum Engineering, Pierottijeva 6, 10 000 Zagreb, DSc, Associate Professor 3 University of Zagreb, Faculty of Mining, Geology and Petroleum Engineering, Pierottijeva 6, 10 000 Zagreb, Master of Pet. Eng, Assistant Abstract Energy mineral resource markets are represented by complex supply and demand ratios which are depending on diơ er- ent factors such as technical (transport) and geopolitical. The main characteristicof energy markets is represented by an uneven geographic distribution of hydrocarbon reserves and production on one hand, and energy consumption on the other. World oil markets, although geographically localized, because of speciƤ c market trade, represent a unique global market with a decreasing price diơ erence. Price diơ erences are the result of the development of transport possibilities of oil supply. The development of transport routes of natural gas and an increasing number of liqueƤ ed natural gas termi- nals in the world give pressure to the natural gas market and its integration into the global gas market. The integration of regional gas markets into a common European gas market is the main energy policy of EU concerning natural gas. On the other hand, there are still signiƤ cant price diơ erences on some markets (e.g. -

“Hedging with a Stock Option”

IOSR Journal of Business and Management (IOSR-JBM) e-ISSN: 2278-487X, p-ISSN: 2319-7668. Volume 17, Issue 9.Ver. I (Sep. 2015), PP 06-11 www.iosrjournals.org “Hedging With a Stock Option” Afzal Ahmad Assistant Professor of Accounting International Islamic University Chittagong Chittagong Abstract: The aim of this paper is to provide a discussion of the use of stock options in risk management and how they can be used for hedging purposes. This aim is achieved by reviewing the literature and analysing practical hedging examples in the context of an investment company. The results of the discussion show that stock options can be employed by companies as a protection against the downside risk when volatility in the market is high. They can also be used during the periods of low volatility to achieve a specific expected payoff within a band of stock prices. The case study reviewed the strategies that involved naked put and calls as well as more complex hedging procedures, namely the butterfly strategy and the bear spread strategy. By purchasing a put option or selling a call option, the company anticipates a decrease in stock prices as in this case there would be a positive payoff. However, when higher prices are anticipated, the company is interested in purchasing a call option or selling a put option. The butterfly strategy allows the firm to cut potential losses and profits to a specific range whereas the bear spread protects against an increase in volatility. The latter strategy implies entering positions in options with different strike prices. -

Put Selling Strategy Rules

Put selling strategy rules Theme This strategy is not my own original strategy. Over time I have seen a few traders teaching this strategy. I practiced this strategy a few years ago and turned my initial $2,000 account into $21,000 in about a year and a half. It is a very profitable strategy if done well and correctly. If wrong, you can ruin your own account. Later, when I considered myself a king of the world, I switched into trading SPX spreads in hoping to make even more money. I lost them all. The strategy is as follows: 1) Sell puts against a dividend stock as long as you get assigned and buy the stock 2) Buy the stock, keep it, collect dividends 3) Sell covered calls against the stock as long as you get assigned and sell the stock 4) Sell the stock 5) Rinse and repeat This strategy offers a lot of variations and with a great dose of imagination you will be able to use it even beyond these simple steps. Over time you will see, that this strategy can help you make money even when you end up in a disastrous, loosing trade. Creating a stock list Create a list of at least 30 stocks to choose from. I select dividend stocks because if I get assigned I am OK to buy the stock. The worst thing you want to do ever is trying to defend your ITM position because you do not want the stock. Although, primarily I choose dividend stocks, it is OK to have a few good quality non-dividend stocks, so don’t limit yourself. -

Spread Scanner Guide Spread Scanner Guide

Spread Scanner Guide Spread Scanner Guide ..................................................................................................................1 Introduction ...................................................................................................................................2 Structure of this document ...........................................................................................................2 The strategies coverage .................................................................................................................2 Spread Scanner interface..............................................................................................................3 Using the Spread Scanner............................................................................................................3 Profile pane..................................................................................................................................3 Position Selection pane................................................................................................................5 Stock Selection pane....................................................................................................................5 Position Criteria pane ..................................................................................................................7 Additional Parameters pane.........................................................................................................7 Results section .............................................................................................................................8 -

Basic Financial Derivatives

An Introduction to Lecture 3 Mathematical Finance UiO-STK-MAT3700 Autumn 2018 Professor: S. Ortiz-Latorre Basic Financial Derivatives The valuation of financial derivatives will be based on the principle of no arbitrage. Definition 1. Arbitrage means making of a guaranteed risk free profit with a trade or a series of trades in the market. Definition 2. An arbitrage free market is a market which has no opportunities for risk free profit. Definition 3. An arbitrage free price for a security is a price that ensure that no arbitrage opportunity can be designed with that security. The principle of no arbitrage states that the markets must be arbitrage free. Some financial jargon will be used in what follows. One says that has/takes a long position on an asset if one owns/is going to own a positive amount of that asset. One says that has/takes a short position on an asset if one has/is going to have a negative amount of that asset. Being short on money means borrowing. You can take a short position on many financial assets by short selling. Example 4 (Short selling). To implement some trading strategy you need to sell some amount of shares (to get money and invest in other assets). The problem is that you do not have any shares right now. Then, you can borrow the shares from another investor for a time period (paying interest) and sell the borrowed shares in the market to get the money you need for your strategy. To close this position, at the end of the borrowing period you must buy again the shares in the market and give them back to the lender.