NYSE Euronext (Exact Name of Registrant As Specified in Its Charter) Delaware 20-5110848 (State Or Other Jurisdiction of (I.R.S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Membership Application for New York Stock Exchange LLC and NYSE

Membership Application for New York Stock Exchange LLC1 and NYSE American LLC 1 NYSE membership permits the Applicant Firm, upon approval of membership, to participate in the NYSE Bonds platform. TABLE OF CONTENTS Page Application Process and Fees 2-3 Information and Resources 3 Explanation of Terms 4-5 Section 1 – Organizational Profile 6 Section 2 – Applicant Firm Acknowledgement 7 Section 3 – Application Questions 8-9 Section 4 – Floor Based Business 10 Section 5 – Key Personnel 11 Section 6 – Additional Required Documentation and Information 12-14 Section 7 – Designation of Accountant 15 Section 8 – Required Organizational Documents and Language Samples / References 16 NYSE and NYSE American Equities Membership Application - October 2019 1 APPLICATION PROCESS Filing Requirements Prior to submitting the Application for New York Stock Exchange LLC (“NYSE”) and/or NYSE American LLC (“NYSE American”) membership, an Applicant Firm must file a Uniform Application for Broker-Dealer Registration (Form BD) with the Securities and Exchange Commission and register with the FINRA Central Registration Depository (“Web CRD®”). Application Submission Applicant Firm must complete and submit all applicable materials addressed within the application as well as the additional required documentation noted in Section 6 of the application. Application and supplemental materials should be sent electronically to [email protected]. Please ensure all attachments are clearly labeled. NYSE Applicant Firm pays one of the below application fees (one-time fee and non-refundable): Clearing Firm $20,000 (Self-Clearing firm or Clears for other firms) Introducing Firm $ 7,500 (All other firms fall within this category) Non-Public Firm $ 2,500 (On-Floor firms and Proprietary firms) Kindly make check payable to “NYSE Market (DE), Inc.” and submit the check with your initial application. -

Nord-Pool-Spot-Glossary.Pdf

GLOSSARY Issued by Nord Pool Spot Date: September 29, 2011 Glossary Nord Pool Spot Area Price Whenever there are grid congestions, the Elspot area is divided into two or more price areas. Each of these prices are referred to as area prices. Balancing market A market system for maintaining the operational balance between consumption and generation of electricity in the overall power system. Also called regulating power market. Bidding area The area for which a bid is posted. There are at least six bidding areas: Sweden, Finland, Denmark East, Denmark West, and at least two Norwegian areas. Bilateral contract A contract between two parties, as opposed to a trade on the exchange. Block bid The block bid is an aggregated bid for several hours, with a fixed price and volume throughout these hours. The purchase/sale is activated if the average price over the given time period is lower (for a purchase bid) or higher (for a sales bid) than the bid price. Clearing customer Responsible for settlement, but their trading and clearing representative performs the trade. Cross border Cross border optimization (CBO) was a service offered by Nord Pool Spot to optimization improve effeciency of the cross border trade between Jutland and Germany until the German - Danish market coupling was introduced. Curtailment Curtailment of the bids in Elspot will take place in a situation where the aggregated supply and bid curves within a price area do not intersect. Delivery hour The hour when the power is produced and consumed Direct participant A direct participant trades on their own behalf and are responsible for settlement. -

The History of Joint-Stock Companies in the Second

STUDIA HISTORIAE OECONOMICAE UAM Vol. 36 Poznań 2018 zhg.amu.edu.pl/sho Mariusz W. M a j e w s k i (Katowice) ORCID 0000-0002-9599-4006 [email protected] THE HISTORY OF JOINT-STOCK COMPANIES IN THE SECOND POLISH REPUBLIC AS EXEMPLIFIED BY WSPÓLNOTA INTERESÓW GÓRNICZO–HUTNICZYCH SA (MINING AND METALLURGY COMMUNITY OF INTERESTS JOINT STOCK COMPANY) Abstract: The article focuses on problems related to capital in Katowicka Spółka Akcyjna dla Gór nictwa i Hutnictwa SA (Katowice Mining and Metallurgy Joint Stock Company) and Górnośląskie Zjednoczone Huty “Królewska” i “Laura” (Upper Silesian United Metallurgical Plants “Królewska” and “Laura”) in the years 1918–1939. The article examines particular issues of the Upper Silesian industry after the Great War, namely: concentration of foreign capital in the mining and metallur gical industries; great mining and metallurgical enterprises in the periods of both industrial pros perity and crisis; attempts to limit the influence of foreign capital following the introduction of ju dicial supervision over Katowicka Spółka Akcyjna dla Górnictwa i Hutnictwa SA and Górnośląskie Zjednoczone Huty “Królewska” i “Laura” SA; the emergence of Wspólnota Interesów Górniczo– Hutniczych SA (Mining and Metallurgy Community of Interests Joint Stock Company) in the fi nal years of the Second Polish Republic. Key words: Second Polish Republic, mining and metallurgical industry, foreign capital, Wspólnota Interesów Górniczo–Hutniczych SA. doi:10.2478/sho-2018-0003 INTRODUCTION. THE CONDITION OF INDUSTRY IN UPPER SILESIA AFTER THE GREAT WAR On May 15, 1922, the Geneva convention on Upper Silesia was signed. As a result, mining and metallurgical enterprises, which up to that point had successfully functioned within the same structures, found themselves 44 Mariusz W. -

Execution Venues List

Execution Venues List This list should be read in conjunction with the Best Execution policy for Credit Suisse AG (excluding branches and subsidiaries), Credit Suisse (Switzerland) Ltd, Credit Suisse (Luxembourg) S.A, Credit Suisse (Luxembourg) S.A. Zweigniederlassung Österreichand, Neue Aargauer Bank AG published at www.credit-suisse.com/MiFID and https://www.credit-suisse.com/lu/en/private-banking/best-execution.html The Execution Venues1) shown enable the in scope legal entities to obtain on a consistent basis the best possible result for the execution of client orders. Accordingly, where the in scope legal entities may place significant reliance on these Execution Venues. Equity Cash & Exchange Traded Funds Country/Liquidity Pool Execution Venue1) Name MIC Code2) Regulated Markets & 3rd party exchanges Europe Austria Wiener Börse – Official Market WBAH Austria Wiener Börse – Securities Exchange XVIE Austria Wiener Börse XWBO Austria Wiener Börse Dritter Markt WBDM Belgium Euronext Brussels XBRU Belgium Euronext Growth Brussels ALXB Czech Republic Prague Stock Exchange XPRA Cyprus Cyprus Stock Exchange XCYS Denmark NASDAQ Copenhagen XCSE Estonia NASDAQ Tallinn XTAL Finland NASDAQ Helsinki XHEL France EURONEXT Paris XPAR France EURONEXT Growth Paris ALXP Germany Börse Berlin XBER Germany Börse Berlin – Equiduct Trading XEQT Germany Deutsche Börse XFRA Germany Börse Frankfurt Warrants XSCO Germany Börse Hamburg XHAM Germany Börse Düsseldorf XDUS Germany Börse München XMUN Germany Börse Stuttgart XSTU Germany Hannover Stock Exchange XHAN -

Intraday Herding on a Cross-Border Exchange

CORE Metadata, citation and similar papers at core.ac.uk Provided by CURVE/open Intraday Herding on a Cross-Border Exchange Andrikopoulos, P, Kallinterakis, V, Pedro Leite Ferreira, M & Verousis, T Author post-print (accepted) deposited by Coventry University’s Repository Original citation & hyperlink: Andrikopoulos, P, Kallinterakis, V, Pedro Leite Ferreira, M & Verousis, T 2017, 'Intraday Herding on a Cross-Border Exchange' International Review of Financial Analysis, vol 53, pp. 25-36 https://dx.doi.org/10.1016/j.irfa.2017.08.010 DOI 10.1016/j.irfa.2017.08.010 ISSN 1057-5219 Publisher: Elsevier NOTICE: this is the author’s version of a work that was accepted for publication in International Review of Financial Analysis. Changes resulting from the publishing process, such as peer review, editing, corrections, structural formatting, and other quality control mechanisms may not be reflected in this document. Changes may have been made to this work since it was submitted for publication. A definitive version was subsequently published in International Review of Financial Analysis, [53, (2017)] DOI: 10.1016/j.irfa.2017.08.010 © 2017, Elsevier. Licensed under the Creative Commons Attribution- NonCommercial-NoDerivatives 4.0 International http://creativecommons.org/licenses/by-nc-nd/4.0/ Copyright © and Moral Rights are retained by the author(s) and/ or other copyright owners. A copy can be downloaded for personal non-commercial research or study, without prior permission or charge. This item cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder(s). The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. -

2009 Annual Report

2009 ANNUAL REPORT UNIBAIL-RODAMCO / 2009 ANNUAL REPORT 1 Profile 2 Message from the CEO 4 Message from the Chairman of the Supervisory Board 6 Strategy & key figures Stock market performance PROFILE 10 & shareholding structure 2009 Unibail-Rodamco is Europe’s leading listed commercial property company ANNUAL with a portfolio valued at €22.3 billion on December 31, 2009. REPORT A clear strategy The Group is the leading investor, operator and developer of large shopping centres in 14 An unprecedented climate Europe. Its 95 shopping centres, 47 of which receive more than 7 million visits per annum, 12 16 Expertise in retail operations are generally located in major continental European cities with superior purchasing power 18 Differentiation: the key to success and extensive catchment areas. The Group continuously reinforces the attractiveness of 22 An attractive development pipeline 24 Financial firepower for future growth its assets by upgrading the layout, renewing the tenant mix and enhancing the shopping 26 Talented, motivated teams experience. Present in 12 European Union countries, Unibail-Rodamco is a natural business partner for any retailer seeking to penetrate or expand in this market and for any public or Business private institution interested in developing large, integrated retail schemes. Overview A commitment to value creation The Group is also a key player in the Paris region office market, where it focuses on modern, efficient buildings of more than 10,000 m2. Finally, in joint venture with the Paris Chamber 32 Shopping Centres of Commerce and Industry, Unibail-Rodamco owns, operates and develops the major 30 34 France 36 Netherlands convention and exhibition centres of the Paris region. -

Filed by the NASDAQ OMX Group, Inc

Filed by The NASDAQ OMX Group, Inc. (Commission File No. 000-32651) Pursuant to Rule 425 under the Securities Act of 1933, as amended Subject Company: NYSE Euronext (Commission File No. 001-33392) NASDAQ OMX and ICE Issue Joint Statement on Superior Proposal New York, NY and Atlanta, GA (April 25, 2011) NASDAQ OMX (NDAQ) and IntercontinentalExchange (ICE) today issued a joint statement with regard to their superior proposal for NYSE Euronext: NYSE Euronext investors should be highly skeptical that after two years of exploratory merger discussions, including more than six months dedicated to finalizing the transaction, NYSE Euronext has suddenly found a reported €100 million in additional synergies. This increase appears not to be a matter of sharpening a pencil, but an unexplained shift in strategy. The discovery that initial synergies having been understated by one-third comes after receiving a superior proposal from NASDAQ OMX and ICE that achieves greater synergies. Importantly, if there are additional synergies to be found after the merger economics have been agreed, then it has to come at the expense of NYSE Euronext stockholders because there has been no increase in the price they are being offered. NYSE Euronext should describe these newly-found synergies in detail in order to support the credibility of these revised estimates, particularly in light of commitments to retain two technology platforms and two headquarters. Increasingly it appears that NYSE Euronext is more focused on protecting the transaction than its stockholders. NASDAQ OMX and ICE have described in detail our proven and focused long-term strategy from which stockholders would benefit and our companies demonstrated outperformance relative to their proposed strategy of creating a financial supermarket. -

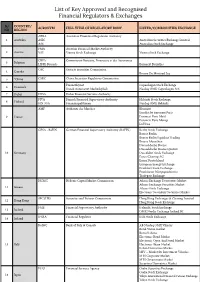

List of Key Approved and Recognised Financial Regulators & Exchanges

List of Key Approved and Recognised Financial Regulators & Exchanges S/ COUNTRY/ ACRONYM FULL TITLE OF REGULATORY BODY LISTED/COMMODITIES EXCHANGE NO REGION APRA Australian Prudential Regulation Authority 1 Australia ASIC Australian Securities Exchange Limited ASE Australian Stock Exchange FMA Austrian Financial Market Authority 2 Austria VSE Vienna Stock Exchange Vienna Stock Exchange CBFA Commission Bancaire, Financiere et des Assurances 3 Belgium LIFFE Brussels Euronext Bruxelles OSC Ontario Securities Commission 4 Canada Bourse De Montreal Inc 5 *China CSRC China Securities Regulatory Commission Finanstilsynet Copenhagen Stock Exchange 6 Denmark Dansk Autoriseret Markedsplads Nasdaq OMX Copenhagen A/S 7 Dubai DFSA Dubai Financial Services Authority FIVA Finnish Financial Supervisory Authority Helsinki Stock Exchange 8 Finland FIN-FSA Finansinspektionen Nasdaq OMX Helsinki AMF Authorite des Marches Bluenext Eurolist by Euronext Paris 9 France Euronext Paris Matif Euronext Paris Monep LCH SA GFSA - BaFIN German Financial Supervisory Authority (BAFIN) Berlin Stock Exchange Boerse Berlin Boerse Berlin Equiduct Trading Boerse Muenchen Duesseldorfer Boerse Duesseldorfer Boerse Quotrix 10 Germany Dusseldorf Stock Exchange Eurex Clearing AG Eurex Deutschland European Energy Exchange Frankfurt Stock Exchange Frankfurter Wertpapierboerse Tradegate Exchange HCMC Hellenic Capital Market Commission Athens Exchange Derivatives Market Athens Exchange Securities Market 11 Greece Athens Stock Exchange Electronic Secondary Securities Market SFC (HK) -

In the Matter of New York Stock Exchange LLC, and NYSE Euronext

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 67857 / September 14, 2012 ADMINISTRATIVE PROCEEDING File No. 3-15023 In the Matter of ORDER INSTITUTING ADMINISTRATIVE AND CEASE-AND-DESIST PROCEEDINGS New York Stock Exchange LLC, and PURSUANT TO SECTIONS 19(h)(1) AND 21C NYSE Euronext, OF THE SECURITIES EXCHANGE ACT OF 1934, MAKING FINDINGS AND IMPOSING Respondents. SANCTIONS AND A CEASE-AND-DESIST ORDER I. The Securities and Exchange Commission (“Commission”) deems it appropriate and in the public interest that public administrative and cease-and-desist proceedings be, and hereby are, instituted pursuant to Sections 19(h)(1) and 21C of the Securities Exchange Act of 1934 (“Exchange Act”) against the New York Stock Exchange LLC (“NYSE”) and NYSE Euronext (collectively, “Respondents”). II. In anticipation of the institution of these proceedings, Respondents have submitted Offers of Settlement (the “Offers”) that the Commission has determined to accept. Solely for the purpose of these proceedings and any other proceedings brought by or on behalf of the Commission, or to which the Commission is a party, and without admitting or denying the findings herein, except as to the Commission’s jurisdiction over them and the subject matter of these proceedings, which are admitted, Respondents consent to the entry of this Order Instituting Administrative and Cease-and-Desist Proceedings Pursuant to Sections 19(h)(1) and 21C of the Securities Exchange Act of 1934, Making Findings and -

Annotated Presentation of Regulated Markets and National Provisions

15.7.2011 EN Official Journal of the European Union C 209/21 Annotated presentation of regulated markets and national provisions implementing relevant requirements of MiFID (Directive 2004/39/EC of the European Parliament and of the Council) (2011/C 209/13) Article 47 of the Markets in Financial Instruments Directive (Directive 2004/39/EC, OJ L 145, 30.4.2004) authorises each Member State to confer the status of ‘regulated market’ on those markets constituted on its territory and which comply with its regulations. Article 4, paragraph 1, point 14 of Directive 2004/39/EC defines a ‘regulated market’ as a multilateral system operated and/or managed by a market operator, which brings together or facilitates the bringing together of multiple third-party buying and selling interests in financial instruments — in the system and in accordance with its non-discretionary rules — in a way that results in a contract, in respect of the financial instruments admitted to trading under its rules and/or systems, and which is authorised and functions regularly and in accordance with the provisions of Title III of Directive 2004/39/EC. Article 47 of Directive 2004/39/EC requires that each Member State maintains an updated list of regulated markets authorised by it. This information should be communicated to other Member States and the European Commission. Under the same article (Article 47 of Directive 2004/39/EC), the Commission is required to publish a list of regulated markets, notified to it, on a yearly basis in the Official Journal of the European Union. The present list has been compiled pursuant to this requirement. -

Recent Acquisitions and Other Transactions NYSE Bluetm On

Recent Acquisitions and Other Transactions NYSE BlueTM On September 7, 2010 NYSE Euronext announced plans to create NYSE BlueTM (which is referred to in this section as “NYSE Blue”), a joint venture focusing on environmental and sustainable energy markets. NYSE Blue includes NYSE Euronext’s existing investment in BlueNext, the spot market in carbon credits, and APX, Inc. (which is referred to in this section as “APX”), a provider of regulatory infrastructure and services for the environmental and sustainable energy markets. NYSE Euronext is majority owner of NYSE Blue. Shareholders of APX, which include Goldman Sachs, Mission Point Capital Partners, and ONSET Ventures, received a minority equity interest in NYSE Blue in return for their shares in APX. The NYSE Blue joint venture formation closed on February 18, 2011. National Stock Exchange of India On May 3, 2010, NYSE Euronext completed the sale of its 5% equity interest in the National Stock Exchange of India for gross proceeds of $175 million. A $56 million gain was included in “Other income” in its consolidated statement of operations for year ended December 31, 2010 as a result of this transaction. NYFIX, Inc. On November 30, 2009, NYSE Euronext acquired NYFIX, Inc. which is a leading provider of innovative solutions that optimize trading efficiency. The total value of this acquisition was approximately $144 million. Infix’s FIX business and FIX Software business were added to the Information Services and Technology Solutions segment. The NYFIX Transaction Services U.S. electronic agency execution business, comprised of its direct market access and algorithmic products, and the Millennium Alternative Trading System was sold to BNY ConvergEX subsequent to the NYFIX acquisition. -

Coming Early to the Party: High Frequency Traders in the Pre-Opening Phase and the Opening Auction of NYSE Euronext Paris

Coming Early to the Party: High Frequency Traders in the Pre-Opening Phase and the Opening Auction of NYSE Euronext Paris Mario Bellia, SAFE - Goethe University Frankfurt ∗ Loriana Pelizzon, SAFE - Goethe University Frankfurt † Marti G. Subrahmanyam, Leonard N. Stern School of Business - New York University ‡ Jun Uno, Waseda University Tokyo § Darya Yuferova, Norwegian School of Economics ¶k First Version: March 15, 2017 This Version: August 23, 2017 Abstract This paper examines the strategic behavior of High Frequency Traders (HFTs) during the pre-opening phase and the opening auction of the NYSE Euronext Paris exchange. Using data provided by the Base Européenne de Données Financières à Haute Fréquence (BEDOFIH), we find that HFTs actively participate in the pre-opening phase. Contrary to common wisdom, HFTs do not delay their order submission decisions until the very last moment of the pre-opening phase of the trading day. They are able to successfully extract information from the pre-opening order flow, as manifested by the potential profits they make on the positions they take in the opening auction. However, HFTs participate in the pre-opening phase also to post “flash crash” orders, with the aim of gaining time priority under extreme market conditions. Furthermore, HFTs make profits on orders submitted in the last second before the opening auction; however, so do slow traders, suggesting that speed is not a necessary condition to make profits in these last second orders. HFTs lead the price discovery process during the pre-opening phase, and neither harm nor improve liquidity provision in the opening auction. Our analysis highlights that HFTs who “come early to the party” enjoy the party (they make profits), however, they also help the other market participants enjoy the party (they improve market quality) and do not have a privileged entrance to the party (their speed advantage is not a necessary condition to make profits).