Darren Alkins

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Other Statutory Disclosures Continued

Other statutory disclosures continued Strategic reportGroup companies Governance & remuneration Financial statements In accordance with Section 409 of the Companies Act 2006 a full list of subsidiaries, associates, joint ventures and joint arrangements, the country of incorporation and effective percentage of equity owned, as at 31 December 2015 are disclosed below. Unless otherwise stated the share capital disclosed comprises ordinary shares which are indirectly held by GlaxoSmithKline plc. All subsidiary companies are resident for tax purposes in their country of incorporation unless otherwise stated. Country of Effective % % Held by Name incorporation Ownership Security Class of Share Wholly owned subsidiaries 1506369 Alberta ULC Canada 100 Common 100 Action Potential Venture Capital Limited England & Wales 100 Ordinary 100 Adechsa GmbH Switzerland 100 Ordinary 100 Affymax Research Institute United States 100 Common 100 Alenfarma – Especialidades Farmaceuticas, Limitada (iv) Portugal 100 Ordinary Quota 100 Allen & Hanburys Limited (iv) England & Wales 100 Ordinary 100 Allen & Hanburys Pharmaceutical Nigeria Limited Nigeria 100 Ordinary 100 Allen Farmaceutica, S.A. Spain 100 Ordinary 100 Allen Pharmazeutika Gesellschaft m.b.H. Austria 100 Ordinary 100 Aners S.A (iv) Argentina 100 Non-endorsable Nominative Ordinary 100 Barrier Therapeutics, Inc. United States 100 Common 100 Beecham Group p l c England & Wales 100 20p Shares 'A'; 5p Shares B 100 Beecham Pharmaceuticals (Pte) Limited Singapore 100 Ordinary 100 Beecham Pharmaceuticals S.A (iv) (vi) Ecuador 100 Nominative 100 Beecham Portuguesa-Produtos Farmaceuticos e Quimicos, Lda Portugal 100 Ordinary Quota 100 Beecham S.A. (iv) Belgium 100 Ordinary 100 Biddle Sawyer Limited India 100 Equity 100 Biovesta Ilaçlari Ltd. Sti. Turkey 100 Nominative 100 Burroughs Wellcome & Co (Australia) Pty Limited (iv) (vi) Australia 100 Ordinary 100 Burroughs Wellcome & Co (Bangladesh) Limited Bangladesh 100 Ordinary 100 Burroughs Wellcome International Limited England & Wales 100 Ordinary 100 Caribbean Chemical Company, Ltd. -

In This Section

Strategic report In this section Chairman’s statement 2 CEO’s review 4 Business overview 6 The global context 8 Our business model 12 Our strategic priorities 14 How we performed 16 Risk management 18 Grow 20 Deliver 32 Simplify 44 Our financial architecture 48 Responsible business 50 Financial review 58 Strategic report Chairman’s statement Chairman’s statement To shareholders The value of the significant changes that have been made in recent years is evidenced in our performance this year “ Since Sir Andrew became It is clear from the following pages that Through the Audit & Risk Committee, we the Group made good progress against oversee the issues and challenges faced by CEO, the company has its strategy in 2013. management, and encourage the creation of an environment in which GSK can achieve The Board believes the business is seeing returned £30 billion its strategic ambitions in a responsible and the benefits of the significant changes the sustainable manner. to shareholders.” management team has driven over recent years to deliver sustainable growth, reduce risk and I have no doubt that commercial success is enhance returns to shareholders. directly linked to operating in a responsible way and which meets the changing expectations of The notably strong performance from the society. In this respect, the company continues R&D organisation in 2013 – with six major to adopt industry-leading positions on a range new product approvals in areas including of issues. respiratory disease, HIV and cancer – is critical to the longer-term prospects of the The announcement of plans during 2013 to Group. -

Laws of Trinidad and Tobago Ministry of Legal Affairs

LAWS OF TRINIDAD AND TOBAGO MINISTRY OF LEGAL AFFAIRS www.legalaffairs.gov.tt FOOD AND DRUGS ACT CHAPTER 30:01 Act 8 of 1960 Amended by 39 of 1968 156/1972 *31 of 1980 16 of 1986 12 of 1987 6 of 1993 16 of 1998 6 of 2005 *See Note on Validation at page 2 Current Authorised Pages Pages Authorised (inclusive) by L.R.O. 1–2 .. 3–20 .. 21–245 .. UNOFFICIAL VERSION L.R.O. UPDATED TO DECEMBER 31ST 2014 LAWS OF TRINIDAD AND TOBAGO MINISTRY OF LEGAL AFFAIRS www.legalaffairs.gov.tt 2 Chap. 30:01 Food and Drugs Index of Subsidiary Legislation Page Food and Drugs Regulations (GN 130/1964) … … … … 25 Official Method Notification (GN 54/1972) … … … … 124 *Approval of New Drugs Notification … … … … … 129 †Withdrawal of Approval of New Drugs Notification (GN 51/1969) … … 200 Fish and Fishery Products Regulations (LN 220/1998)…………201 †This Notification (i.e. 51/1969) has been amended by LNs 99 and 114/1984 which have been omitted. *Note on Approval of New Drugs Notification The list of new drugs set out in the Schedule to this Notification has been consolidated as at 31st December 1977. This list is so voluminous and changes to it so frequent that, especially in view of its very limited use by the general public, it is not practicable to update it annually. The references to the amendments to this list since 31st December 1977 are contained in the Current Consolidated Index of Acts and Subsidiary Legislation. †Note on Withdrawal of Approval of New Drugs Notification For references to the Withdrawal of Approval of New Drugs Notifications subsequent to the year 1969 — See the current Consolidated Index of Acts and Subsidiary Legislation. -

E-Binder November 2014

STATE OF NEVADA ROMAINE GILLILAND DEPARTMENT OF HEALTH AND HUMAN SERVICES Director DIVISION OF HEALTH CARE FINANCING AND POLICY 1100 E. William Street, Suite 101 LAURIE SQUARTSOFF Administrator BRIAN SANDOVAL Carson City, Nevada 89701 Governor www.dhcfp.nv.gov NOTICE OF OPEN PUBLIC MEETING The Division of Health Care Financing and Policy (DHCFP) Pharmacy and Therapeutics Committee will conduct a public meeting on November 13, 2014, beginning at 1:00 p.m. at the following location: JW Marriott Las Vegas Resort and Spa Grand Ballroom A 221 N. Rampart Blvd Las Vegas, NV 89145 702-869-7777 This meeting will be held only in Las Vegas, NV, there will be no teleconference to Carson City, NV. Reasonable efforts will be made to assist and accommodate physically challenged persons desiring to attend the meeting. Please call Rita Mackie at: 775-684-3681 or email [email protected] in advance, but no later than two working days prior to the meeting, so that arrangements may be conveniently made. Items may be taken out of order. Items may be combined for consideration by the public body. Items may be pulled or removed from the agenda at any time. Public comment is limited to 5 minutes per individual, organization, or agency, but may be extended at the discretion of the Chairperson. AGENDA I. CALL TO ORDER AND ROLL CALL II. PUBLIC COMMENT No action may be taken on a matter raised under this item of the agenda until the matter itself has been specifically included on the agenda as an item upon which action can be taken. -

![Active Ingredient Dosage Strength and Form Comparator Drug1 Marketing Authorization Holder [Manufacturer] Registration Number A](https://docslib.b-cdn.net/cover/1849/active-ingredient-dosage-strength-and-form-comparator-drug1-marketing-authorization-holder-manufacturer-registration-number-a-2481849.webp)

Active Ingredient Dosage Strength and Form Comparator Drug1 Marketing Authorization Holder [Manufacturer] Registration Number A

Republic of the Philippines Department of Health FOOD AND DRUG ADMINISTRATION CENTER FOR DRUG REGULATION AND RESEARCH Provisional List of Comparator Products for in vivo and/or in vitro Equivalence Studies (as of 11 July 2019) Active Ingredient Dosage Strength Comparator Marketing Registration and Form Drug1 Authorization Holder Number [Manufacturer] Abacavir (as sulfate) 300mg Tablet ZIAGEN ViiV Healthcare UK Ltd.2 Not available ViiV Healthcare Co.3 locally Abacavir (as sulfate) 600mg/300mg KIVEXA ViiV Healthcare UK Ltd.2 Not available + Lamivudine Tablet EPZICOM ViiV Healthcare Co.3 locally Abacavir (as sulfate) 300mg/150mg/30 TRIZIVIR ViiV Healthcare UK Ltd.2 Not available + Lamivudine + 0mg Tablet ViiV Healthcare Co.3 locally Zidovudine Abacavir (as sulfate) 600mg/50mg/300 TRIUMEQ ViiV Healthcare UK Ltd.2 Not available + Dolutegravir (as mg Tablet ViiV Healthcare Co.3 locally sodium) + Lamivudine Abiraterone Acetate 250mg Tablet ZYTIGA Johnson & Johnson DR-XY41696 (Phils.), Inc. [Patheon Inc. – Canada] 500mg Tablet ZYTIGA Janssen-Cilag Ltd.2 Not available Janssen Biotech Inc.3 locally Acarbose 25mg Tablet PRECOSE Bayer Healthcare Not available Pharmaceuticals Inc.3 locally 50mg Tablet GLUCOBAY Bayer Philippines, Inc. DRP-3657 [Bayer Pharma AG – Germany] 100mg Tablet GLUCOBAY Bayer Philippines, Inc. DRP-3658 [Bayer Pharma AG – Germany] Aceclofenac 100 mg Film- PRESERVEX Almirall Limited – UK2 Not available Coated Tablet locally Acetazolamide 250 mg Tablet DIAMOX Wyeth Phils., Inc. [Wyeth DR-2928 Lederle Ltd. – India] Acetylcysteine Capsule Available orally administered dosage forms of the comparator Powder or product/reference drug (FLUIMUCIL of The Cathay Drug Co., Granules for Oral Inc. manufactured by Zambon Switzerland Ltd.) are in Suspension effervescent tablet and powder or granules for oral solution. -

Other Statutory Disclosures Continued

272 GSK Annual Report 2016 Other statutory disclosures continued Group companies In accordance with Section 409 of the Companies Act 2006 a full list of subsidiaries, associates, joint ventures and joint arrangements, the address of the registered office and effective percentage of equity owned, as at 31 December 2016 are disclosed below. Unless otherwise stated the share capital disclosed comprises ordinary shares which are indirectly held by GlaxoSmithKline plc. The percentage held by class of share is stated where this is less than 100%. Unless otherwise stated, all subsidiary companies have their registered office in their country of incorporation. All subsidiary companies are resident for tax purposes in their country of incorporation unless otherwise stated. Name Security Registered address Wholly owned subsidiaries 1506369 Alberta ULC Common 3500 855-2nd Street SW, Calgary, AB, T2P 4J8, Canada Action Potential Venture Capital Limited Ordinary 980 Great West Road, Brentford, Middlesex, TW8 9GS, England Adechsa GmbH (iv) Ordinary c/o PRV Provides Treuhandgesellschaft AG, Dorfstrasse 38, Baar, 6341, Switzerland Affymax Research Institute Common Corporation Service Company, 2710 Gateway Oaks Drive, Suite 150N, Sacramento, California, CA, 95833, United States Alenfarma – Especialidades Farmaceuticas, Ordinary Quota Rua Dr Antonio Loureiro Borges No 3, Arquiparque, Miraflores, Alges, Limitada (iv) 1495-131, Portugal Allen & Hanburys Limited (iv) Ordinary 980 Great West Road, Brentford, Middlesex, TW8 9GS, England Allen & Hanburys Pharmaceutical Nigeria Limited Ordinary 24 Abimbola Way, Ilasamaja, Isolo, Lagos, Nigeria Allen Farmaceutica, S.A. Ordinary Severo Ochoa, 2, Parque Tecnologico de Madrid, Tres Cantos, Madrid, 28760, Spain Allen Pharmazeutika Gesellschaft m.b.H. Ordinary Wagenseilgasse 3, Euro Plaza, Gebäude I, 4. -

Annual Report 2015

Annual Report 2015 2015 saw substantial progress to accelerate new product sales growth and strengthen our Pharmaceuticals, Vaccines and Consumer Healthcare businesses Overview of 2015 Strategic report “ In 2015, we made substantial progress to accelerate new product sales growth, integrate new businesses in Vaccines and Consumer Healthcare and restructure our global Pharmaceuticals business. This progress means the Group is well positioned to return to core earnings growth in 2016.” Sir Andrew Witty, Chief Executive Officer Governance & remunerationPerformance Financial statements summary Investor information £23.9bn £10.3bn £5.7bn £3.9bn Group turnover Total operating profit Core operating profit Cash dividends paid (up 6% CER/up 1% CER (up >100% CER) a (down 9% CER/down 3% in 2015 pro-forma) a CER pro-forma)a £2.0bn 174.3p 75.7p 10 0 % New product sales b Total earnings per share Core earnings per share Markets now operating (up >100%) (up >100%, primarily (down 15% CER, primarily new commercial model reflecting impact of reflecting short-term dilution transaction gains) of the Novartis transaction)a ~40 20 ~13 % 1st Potential new medicines Potential to file up to Estimated internal In Access to Medicine and vaccines profiled at R&D 20 assets with regulators rate of return in R&D Index event, 80% of which have by 2020 in 2015 potential to be first-in-classc Footnotes a We use a number of adjusted measures to report the performance of our business, as described on page 54. These include core results, CER growth rates and pro-forma CER growth rates. A reconciliation of total results to core results is set out on page 62. -

Crystal Reports Activex Designer

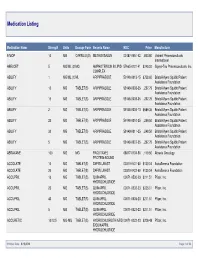

Medication Listing Medication Name Strength Units Dosage Form Generic Name NDC Price Manufacturer 8-MOP 10 MG CAPSULE(S) METHOXSALEN 00187-0651-42 1,843.80 Valeant Pharmaceuticals International ABELCET 5 MG/ML (20MG AMPHOTERICIN B LIPID 57665-0101-41 $240.00 Sigma-Tau Pharmaceuticals, Inc. COMPLEX ABILIFY 1 MG/ML (150ML ARIPIPRAZOLE 59148-0013-15 $758.60 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 10 MG TABLET(S) ARIPIPRAZOLE 59148-0008-35 2,297.75 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 15 MG TABLET(S) ARIPIPRAZOLE 59148-0009-35 2,297.75 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 2 MG TABLET(S) ARIPIPRAZOLE 59148-0006-13 $689.36 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 20 MG TABLET(S) ARIPIPRAZOLE 59148-0010-35 3,249.50 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 30 MG TABLET(S) ARIPIPRAZOLE 59148-0011-35 3,249.50 Bristol-Myers Squibb Patient Assistance Foundation ABILIFY 5 MG TABLET(S) ARIPIPRAZOLE 59148-0007-35 2,297.75 Bristol-Myers Squibb Patient Assistance Foundation ABRAXANE 100 MG MG PACLITAXEL 68817-0134-50 1,119.60 Abraxis Oncology PROTEIN-BOUND ACCOLATE 10 MG TABLET(S) ZAFIRLUKAST 00310-0401-60 $130.04 AstraZeneca Foundation ACCOLATE 20 MG TABLET(S) ZAFIRLUKAST 00310-0402-60 $130.04 AstraZeneca Foundation ACCUPRIL 10 MG TABLET(S) QUINAPRIL 00071-0530-23 $211.51 Pfizer, Inc. HYDROCHLORIDE ACCUPRIL 20 MG TABLET(S) QUINAPRIL 00071-0532-23 $235.01 Pfizer, Inc. HYDROCHLORIDE ACCUPRIL 40 MG TABLET(S) QUINAPRIL 00071-0535-23 $211.51 Pfizer, Inc. HYDROCHLORIDE ACCUPRIL 5 MG TABLET(S) QUINAPRIL 00071-0527-23 $211.51 Pfizer, Inc. -

Frequency of Application of Topical Corticosteroids for Atopic Eczema

Frequency of application of topical corticosteroids for atopic eczema Issued: August 2004 NICE technology appraisal guidance 81 guidance.nice.org.uk/ta81 © NICE 2004 Frequency of application of topical corticosteroids for NICE technology appraisal atopic eczema guidance 81 Contents 1 Guidance ................................................................................................................................... 3 2 Clinical need and practice ......................................................................................................... 4 3 The technology.......................................................................................................................... 8 4 Evidence and interpretation....................................................................................................... 10 4.1 Clinical effectiveness......................................................................................................................... 10 4.2 Cost effectiveness ............................................................................................................................. 15 4.3 Consideration of the evidence........................................................................................................... 17 5 Recommendations for further research..................................................................................... 19 6 Implications for the NHS............................................................................................................ 20 7 Implementation -

Appendix B - Product Name Sorted by Applicant

JUNE 2021 - APPROVED DRUG PRODUCT LIST B - 1 APPENDIX B - PRODUCT NAME SORTED BY APPLICANT ** 3 ** 3D IMAGING DRUG * 3D IMAGING DRUG DESIGN AND DEVELOPMENT LLC AMMONIA N 13, AMMONIA N-13 FLUDEOXYGLUCOSE F18, FLUDEOXYGLUCOSE F-18 SODIUM FLUORIDE F-18, SODIUM FLUORIDE F-18 3M * 3M CO PERIDEX, CHLORHEXIDINE GLUCONATE * 3M HEALTH CARE INC AVAGARD, ALCOHOL (OTC) DURAPREP, IODINE POVACRYLEX (OTC) 3M HEALTH CARE * 3M HEALTH CARE INFECTION PREVENTION DIV SOLUPREP, CHLORHEXIDINE GLUCONATE (OTC) ** 6 ** 60 DEGREES PHARMS * 60 DEGREES PHARMACEUTICALS LLC ARAKODA, TAFENOQUINE SUCCINATE ** A ** AAA USA INC * ADVANCED ACCELERATOR APPLICATIONS USA INC LUTATHERA, LUTETIUM DOTATATE LU-177 NETSPOT, GALLIUM DOTATATE GA-68 AAIPHARMA LLC * AAIPHARMA LLC AZASAN, AZATHIOPRINE ABBVIE * ABBVIE INC ANDROGEL, TESTOSTERONE CYCLOSPORINE, CYCLOSPORINE DEPAKOTE ER, DIVALPROEX SODIUM DEPAKOTE, DIVALPROEX SODIUM GENGRAF, CYCLOSPORINE K-TAB, POTASSIUM CHLORIDE KALETRA, LOPINAVIR NIASPAN, NIACIN NIMBEX PRESERVATIVE FREE, CISATRACURIUM BESYLATE NIMBEX, CISATRACURIUM BESYLATE NORVIR, RITONAVIR SYNTHROID, LEVOTHYROXINE SODIUM ** TARKA, TRANDOLAPRIL TRICOR, FENOFIBRATE TRILIPIX, CHOLINE FENOFIBRATE ULTANE, SEVOFLURANE ZEMPLAR, PARICALCITOL ABBVIE ENDOCRINE * ABBVIE ENDOCRINE INC LUPANETA PACK, LEUPROLIDE ACETATE ABBVIE ENDOCRINE INC * ABBVIE ENDOCRINE INC LUPRON DEPOT, LEUPROLIDE ACETATE LUPRON DEPOT-PED KIT, LEUPROLIDE ACETATE ABBVIE INC * ABBVIE INC DUOPA, CARBIDOPA MAVYRET, GLECAPREVIR NORVIR, RITONAVIR ORIAHNN (COPACKAGED), ELAGOLIX SODIUM,ESTRADIOL,NORETHINDRONE ACETATE -

Connecticut Department of Public Health, AIDS Drug Assistance

Connecticut Department of Public Health, AIDS Drug Assistance Program (ADAP) Formulary by Class Effective Date: September 21, 2021 Phone: 1-800-424-3310 https://ctdph.magellanrx.com/ Prior Authorization Fax: 1-855-461-2759 CT DPH mandates the use of generic products whenever possible in accordance with applicable law or regulations. Exceptions are noted by drug. Generic Name Brand Name Restrictions ANTIRETROVIRALS Multiclass Single Tablet Regimens abacavir/lamivudine/dolutegravir Triumeq bictegravir/emtricitabine/tenofovir Biktarvy alafenamide cabotegravir/rilpivirine Cabenuva 600 mg/900 mg Strength: Maximum quantity per fill of 6.0 ml 400 mg/600 mg Strength: Maximum quantity per fill of 4.0 ml darunavir/cobicstat/emtricitabine/tenofovir Symtuza alafenamide dolutegravir/lamivudine Dovato dolutegravir/rilpivirine Juluca doaravine/lamivudine/tenofovir disoproxil Delstrigo fumarate efavirenz/emtricitabine/tenofovir disoproxil Atripla ADAP only clients: Brand forms and generic NDC 69097021002 fumarate covered ADAP with insurance clients: Both brand and generic forms covered efavirenz/lamivudine/tenofovir disoproxil Symfi fumarate efavirenz/lamivudine/tenofovir disoproxil Symfi Lo fumarate elvitegravir/cobicistat/emtricitabine/ Genvoya tenofovir alafenamide elvitegravir/cobicistat/emtricitabine/ Stribild tenofovir disoproxil fumarate emtricitabine/rilpivirine/tenofovir alafenamide Odefsey emtricitabine/rilpivirine/tenofovir disoproxil Complera fumarate Combination Medications abacavir/lamivudine Epzicom abacavir/lamivudine/zidovudine Trizivir -

Group Companies

Strategic report Governance and remuneration Financial statements Investor information Other statutory disclosures continued Group companies In accordance with Section 409 of the Companies Act 2006 a full list of subsidiaries, associates, joint ventures and joint arrangements, the address of the registered office and effective percentage of equity owned, as at 31 December 2019 are disclosed below. Unless otherwise stated the share capital disclosed comprises Ordinary shares which are indirectly held by GlaxoSmithKline plc. The percentage held by class of share is stated where this is less than 100%. Unless otherwise stated, all subsidiary companies have their registered office and are tax resident in their country of incorporation. Name Security Registered address Wholly owned subsidiaries 1506369 Alberta ULC Common 3500 855-2nd Street SW, Calgary, AB, T2P 4J8, Canada Action Potential Venture Capital Limited Ordinary 980 Great West Road, Brentford, Middlesex, TW8 9GS, England Adechsa GmbH (ii) Ordinary c/o PRV Provides Treuhandgesellschaft AG, Dorfstrasse 38, Baar, 6341, Switzerland Affymax Research Institute Common Corporation Service Company, 2710 Gateway Oaks Drive, Suite 150N, Sacramento, California, 95833, United States Alenfarma – Especialidades Farmaceuticas, Limitada (ii) Ordinary Quota Rua Dr Antonio Loureiro Borges No 3, Arquiparque, Miraflores, Alges, 1495-131, Portugal Allen & Hanburys Limited (ii) Ordinary 980 Great West Road, Brentford, Middlesex, TW8 9GS, England Allen & Hanburys Pharmaceutical Nigeria Limited Ordinary 24 Abimbola Way, Ilasamaja, Isolo, Lagos, Nigeria Allen Farmaceutica, S.A. Ordinary Severo Ochoa, 2, Parque Tecnologico de Madrid, Tres Cantos, Madrid, 28760, Spain Allen Pharmazeutika Gesellschaft m.b.H. Ordinary Wagenseilgasse 3, Euro Plaza, Gebäude I, 4. Stock, Vienna, A-1120, Austria Barrier Therapeutics, Inc.