Annexure 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Órgão Oficial Da República De Angola

Sexta-feira, 29 de Junho de 2018 I Série – N.º 94 DIÁRIO DA REPÚBLICA ÓRGÃO OFICIAL DA REPÚBLICA DE ANGOLA Preço deste número - Kz: 1.780,00 !"#$% $% &"''()*"+#+&-$.% /0('% "[&-$2.% /0('% ASSINATURA [%*'( "%#(%&$#$%2-+H$%*0:2-&$#$%+")%7-'-")% '(2$3-4$% $% $++&-"% (% $))-+$30'$)% #"% E7-'-"% Ano #$%9(*:2-&$%MC9%(%JC9%) '-(% %#(%TUR%VXCOO%(%*$'$% #$% 9(*:2-&$F.% #(4(% )('% #-'-<-#$% % >?*'(+)$% K)%3')%) '-()% %CCCC CCC CCC CCC CCC CCC% TUR%PMM%VWWCXO $% NC9% ) '-(% TUR% WXCOO.% $&'()&-#"% #"% '()*(&3-4"% @$&-"+$2% A% BCDC.% (?% E0$+#$.% 90$% F(+'-/0(% #(% K%MC9%) '-(% %CCCC CCC CCC CCC CCC CCC% TUR%NPM%JVOCOO -?*")3"%#"%)(2".%#(*(+#(+#"%$%*0:2-&$ "%#$% G$'4$2H"% +C:% J.% G-#$#(%K23$.% G$-L$% D")3$2% MNOP.% QQQC-?*'(+)$+$&-"+$2C<"4C$"% A% B+#C% 3(2(<CR% K%JC9%) '-(% %CCCC CCC CCC CCC CCC CCC% TUR%MZW%MXOCOO NC9%) '-(%#(%#(*)-3"%*' 4-"%$%(_(&30$'%+$%3()"0A E>?*'(+)$FC K%NC9%) '-(% %CCCC CCC CCC CCC CCC CCC% TUR%MXO%MMMCOO '$'-$%#$%>?*'(+)$%@$&-"+$2%A%BC%DC SUMÁRIO ARTIGO 1.º (Aprovação) É aprovado o Plano de Desenvolvimento Nacional 2018- Presidente da República BCBB1'&$",*'&*'(3"4"$/"'D"-3"/*'53"4%!"$-%&)'"'!")"'(&3/"' Decreto Presidencial n.º 158/18: integrante. Aprova o Plano de Desenvolvimento Nacional 2018-2022. ARTIGO 2.º Decreto Presidencial n.º 159/18: (Dúvidas e omissões) Nomeia Elisa Rangel Nunes para o cargo de Juíza Conselheira do Tribunal de Contas, Joaquim Mande para o cargo de Juiz Conselheiro do Tribunal As dúvidas e omissões resultantes da interpretação e apli- de Contas e Rigoberto Kambovo para o cargo de Juiz Conselheiro cação do presente Diploma são resolvidas pelo Presidente da do Tribunal de Contas. República. ARTIGO 3.º PRESIDENTE DA REPÚBLICA (Entrada em vigor) O presente Decreto Presidencial entra em vigor na data da sua publicação. -

Annual Report & Financial Statements

2014 ANNUAL REPORT & FINANCIAL STATEMENTS EASTERN AND SOUTHERN AFRICAN TRADE AND DEVELOPMENT BANK TABLE OF CONTENTS LETTER OF TRANSMITTAL 3 CHAIRMAN’S STATEMENT 5 PRESIDENT’S STATEMENT 8 Strategic Overview 8 Operations 11 Project and Infrastructure Finance (PIF) 11 Trade Finance 11 Funds Management 11 Risk Management 11 Resource Mobilization 12 International Ratings 13 Financial Management 14 Human Resources and Administration 15 Conclusion 15 3 STATEMENT ON CORPORATE GOVERNANCE 16 SUSTAINABILITY REPORTING STATEMENT 20 ECONOMIC ENVIRONMENT 24 FINANCIAL MANAGEMENT & TREASURY 30 OPERATIONS 36 Project and Infrastructure Finance 38 Trade Finance 40 Funds Management 43 Portfolio Management 44 Compliance and Risk Management 45 Human Resources and Administration 47 2014 Annual Report & Financial Statements & Financial Annual Report 2014 Information Technology 48 ANNUAL REPORT & FINANCIAL STATEMENTS 2014 49-151 FINANCIAL HIGHLIGHTS 24% 30% LOAN ASSETS EQUITY CAPITAL US$ 2.51billion US$ 622 million 16% 31% NET PROFIT NON-PERFORMING US$ 77 million LOANS 3.04% LETTER OF TRANSMITTAL 5 The Chairman Board of Governors Eastern and Southern African Trade and Development Bank Dear Mr. Chairman, In accordance with Article 35(2) of the Bank’s Charter, I have the honour, on behalf of the Board of Directors, to submit herewith the Annual Report of the Bank for the period 1 January to 31 December 2014. The report covers the year’s activities and audited financial statements for the period. 2014 Annual Report & Financial Statements & Financial Annual Report 2014 Mr. Chairman, please accept the assurances of my highest consideration. MR. RUPERT HORACE SIMEON Chairman of the Board of Directors 6 2014 Annual Report & Financial Statements & Financial Annual Report 2014 CHAIRMAN’S STATEMENT Chairman’s Statement The African and International Economic Context subscribed up to 98% of the General Capital Increase launched in 2007. -

DEZEMBRO 2010 Centro De Documentação E Informação

DEZEMBRO 2010 Centro de Documentação e Informação O Extracto de notícias é um serviço do Centro de Documentação da DW (CEDOC) situado nas instalações da DW em Luanda. Redação O Centro foi criado em Agosto de 2003 com o objectivo de facilitar Helga Silveira a recolha, armazenamento, acesso e disseminação de informação sobre desenvol-vimento socio-economico do País. Conselho de Ediçao Allan Cain, Joyce Jose, Através da monitoria dos projectos da DW, estudos, pesquisas e outras Jose Tiago, Gelson Gaspar formas de recolha de informação, o Centro armazena uma quantidade e Massomba Dominique considerável de documentos entre relatórios, artigos, mapas e livros. A informação é arquivada física e eletronicamente, e está disponível Editado por para consulta para as entidades interessadas. Além da recolha e arma- Development Workshop – Angola zenamento de informação, o Centro tem a missão da disseminação de informação por vários meios. Um dos produtos principais do Endereço Centro é o Extracto de notícias. Este Jornal monitora a imprensa Rua Rei Katyavala 113, nacional e extrai artigos de interesse para os leitores com actividades C.P. 3360, Luanda – Angola de interesse no âmbito do desenvolvimento do País. O jornal traz artigos categorizados nos seguintes grupos principais: Telefone 1. Redução da Pobreza e Economia +(244 2) 448371 / 77 / 66 2. Microfinanças 3. Mercado Informal Email 4. OGE investimens públicos e transparência [email protected] 5. Governação descentralização e cidadania 6. Urbanismo e habitação Com apoio de 7. Terra NORAD, Embaixada da Noruega 8. Serviços básicos e LUPP (Programa de Redução 9. Género e Violência a Pobreza Urbana de Luanda) 10. -

2015 BROOKINGS FINANCIAL and DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage

WASHINGTON, DC | AUGUST 26, 2015 THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage BY JOHN D. VILLASENOR, DARRELL M. WEST, AND ROBIN J. LEWIS About the Center for Technology Innovation at Brookings The Center for Technology Innovation (CTI) at Brookings focuses on delivering research that impacts public debate and policymaking in the arena of U.S. and global technology innovation. CTI’s goals include: Identifying and analyzing key developments to increase innovation; developing and publicizing best practices to relevant stakeholders; briefing policymakers about actions needed to improve innovation; and enhancing the public and media’s understanding of technology innovation. About the Brookings Institution The Brookings Institution is a nonprofit organization devoted to independent research and policy solutions. Its mission is to conduct high-quality, independent research and, based on that research, to provide innovative, practical recommendations for policymakers and the public. The conclusions and recommendations of any Brookings publication are solely those of its author(s), and do not reflect the views of the Institution, its management, or its other scholars. WASHINGTON, DC | AUGUST 26, 2015 THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT Measuring Progress on Financial Access and Usage BY JOHN D. VILLASENOR, DARRELL M. WEST, AND ROBIN J. LEWIS Comments and feedback regarding the Financial and Digital Inclusion Project can be submitted to [email protected]. THE 2015 BROOKINGS FINANCIAL AND DIGITAL INCLUSION PROJECT REPORT 1 TABLE OF CONTENTS EXECUTIVE SUMMARY ............................................................ 2 THE IMPORTANCE OF FINANCIAL INCLUSION ............................... 7 MEASURING FINANCIAL INCLUSION .......................................... 10 DIMENSIONS OF EVALUATION ................................................... 12 Overall ranking on financial inclusion .................................. -

TO SURVIVE OR THRIVE? Domestic Payments Innovation in the Pandemic DOMESTICCONTENTS SCHEMES PROSPECTS

DOMESTIC PAYMENT SCHEMES JURY 2021 TO SURVIVE OR THRIVE? Domestic Payments Innovation in the Pandemic DOMESTICCONTENTS SCHEMES PROSPECTS Forewords 03 Executive Summary 04 The Jury 06 The Changing World of Domestic Payments 07 Systemic Innovation 13 The Pandemic Strikes 15 Effect on Innovation 18 Future Prospects 20 Additional information 25 3 Domestic Payments Schemes Jury 2021 FOREWORDS It is great to see John Chaplin Many domestic payment systems are embracing these continuing to dedicate time innovations and setting themselves on a new trajectory. and effort to the Payment The recently issued G20 cross-border payments roadmap Innovation Jury and Chris also refers to the role that well-functioning domestic Hamilton now joining this effort. payment systems and their international linkages can have on improving cross-border payments. At the same This pandemic brought out in time this crisis has also challenged the domestic payment stark relief the fundamental systems in their ability to handle a rapid surge in usage, the role of digital payments in the effectiveness of their business continuity plans and ability functioning of the economy. A to handle increasing sophistication of cyber threats and recent McKinsey report showed social engineering attacks. that countries with greater adoption of digital payments, a well-functioning payments This edition discusses the dual theme of how the domestic market and good ID infrastructure were able to respond payment systems are handling the crisis and how they are to the crisis faster and with greater ambition. Regulators navigating the rapid shifts underway. I am sure the insights across the world took several measures to enable presented in this report will be useful for the various the smooth functioning and fostering usage of digital stakeholders following the developments in the domestic payments. -

Report Annual 2015

ANNUAL REPORT2015 ANNUAL REPORT MILLENNIUM ANGOLA 2015 CONTENTS ANNUAL REPORT2015 2015r"//6"-3&1035rContents 5 CONTENTS 5 Message of the Chief Executive Officer 6 Main Highlights 7 Key Indicators 8 Executive Committee 9 Shareholder Structure and Governing Bodies 10 Economic Environment 20 Regulatory Changes to the Financial System 24 Business Summary 38 Distribution Network 46 Financial Statements 51 Notes to the Financial Statements 93 Proposed Appropriation of Net Income 94 Independent Auditors' Report 96 Opinion of the Supervisory Board on the Account of 2015 #BODP.JMMFOOJVN"OHPMB 4" MESSAGE OF THE CHIEF EXECUTIVE OFFICER ANNUAL REPORT2015 2015r"//6"-3&1035r.FTTBHFPGUIF$IJFG&YFDVUJWF0GàDFS 7 MESSAGE OF THE CHIEF EXECUTIVE OFFICER Throughout 2015 and in the wake of the constraints of the economic context of 2014, the Angolan economy was severely affected by the sharply declining price of the barrel of oil in international markets and, consequently, by the lack of foreign currency to fund imports, on which Angola is heavily dependent. This scenario has made it very clear that there is an imperative need for economic diversification, in order to facilitate the business environment and attract direct investment towards other activity sectors, outside the petroleum sector, which shall boost the Angolan economy in the medium term. The fall in the price of oil significantly reduced fiscal revenue and the obtaining of foreign currency. This evolution particularly constrained private consumption and public investment, and contributed to the GDP growth rate having shifted from 4.8% in 2014, to 3.5% in 2015, according to IMF forecasts. In this environment, the kwanza devalued sharply and the inflation rate exceeded 14%, imposing the need for a more restrictive monetary policy. -

FDH Bank Financials 2019 FINAL

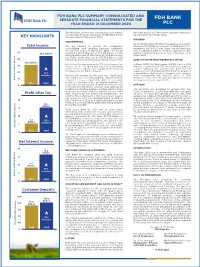

SUMMARY AUDITED FINANCIAL STATEMENTS FDH BANK FDH Bank FOR THE YEAR ENDED 31 DECEMBER 2019. LIMITED Main Highlights Net interest Income 7% Total Income Non Interest income 23% 10 40 K34.3 K7.8 Billion Corporate Social Responsibility 21% Billion K29 8 Billion a a 2019 K5.9 30 ach Billion 2019 ach Total Assets 24% Kw 6 Kw 2018 2018 20 4 Loan Book Growth 40% 10 Amount in Billion 2 32% Amount in Billion 18% Increase Increase Return on Equity 35% 0 0 NPL Ratio down to 0.80% K Customer Deposits Basic Earnings per Introduced WhatsApp Banking Share (Tambala) K137.1 Billion New Branch Goliati - Thyolo 150 2000 K112.5 1,696 Tambala a Billion 2019 1,289 Tambala ach 1500 Upgraded Branches Mulanje, Chiponde, Mzimba, Kw 100 2019 and Agencies Chitipa, Jenda & Neno 2018 ambala 2018 1000 50 Amount in T 500 Amount in Billion 22% 32% Increase Increase 0 0 FDH BANK LIMITED FINANCIAL RESULTS FOR Malawi GDP growth rate is projected to average between 5% and 6%, according to the Reserve Bank of Malawi. YEAR ENDED 31 DECEMBER 2019. Private sector credit annual growth in 2019 was 21.3% up from 11.5% in 2018. The The Directors present the audited summarised financial statements of FDH Bank stronger growth in private sector credit in 2019 is a reflection of reduced interest rates. Limited for the year ended 31 December 2019. We anticipate the low interest rates regime to continue and spur private sector credit growth in 2020. PERFORMANCE The Bank continues to consolidate and improve on the convenient delivery channels The Directors report a profit after tax of K7.846 billion for the year ended 31 through its digital products and providing innovative first class financial solutions. -

Innovació I Compromís Social 60 Anys D’Informatització I Creixement

Aquest estudi planteja d’una manera inèdita el paper de la tecnologia en el desenvolupament d’una entitat finan- cera, “la Caixa”, a través del que en aquest text es deno- io mina la seva «opció tecnològica». c nfulgen a La innovació i el desenvolupament tecnològic de “la Caixa” vier S a X han estat el resultat de l’acció de grups humans que van Foto: Foto: actuar en contextos i situacions molt variats. Com en Innovac 1950 tota trajectòria empresarial (“la Caixa” ja té més de cent J. Carles Maixé-Altés, natural de Tarragona, es va llicen- anys d’història), hi va haver temps heroics en què es van ciar en Història Moderna i Contemporània i també en i trencar esquemes, tal com va passar amb la introducció ó Ciències Econòmiques per la Universitat de Barcelona, i dels primers ordinadors al principi dels anys seixanta. soc compromís on es va doctorar en Història Econòmica (cum laude) el Poc després, a meitat de la dècada, va arribar el telepro- 1992. Actualment és professor titular d’universitat (De- cés, tecnologia en la qual l’entitat va ser líder a Europa. partament d’Economia Aplicada 1, Universitat de la Co- També hi va haver fases d’acceleració, en què, a cavall 2011 runya). La seva investigació s’adreça preferentment cap de les reformes política i financera, es van generar prou a l’estudi de la història financera i bancària europea (se- sinergies per canviar el rumb de l’empresa. Fins i tot en gles XVIII-XX) i el canvi tecnològic i organitzatiu en les moments crítics, com passa en la crisi actual, s’aprecia i finances detallistes des de 1950. -

Contents BRIEFS

25 November 2013 BRIEFS Contents IN-DEPTH: The IMF forecasts sub-Saharan GDP growth of 6% in 2014, up from 5% in 2013. Inflation is forecast at 6.3% in 2014, the - Assessing risk and opportunity in Africa 2 lowest annual average for the region in 30 years. - SOVEREIGN RATINGS 3 - African Development Bank 5 In 2012, an estimated 30m migrant sent cross-border INVESTMENTS 8 remittances worth $60bn to recipients in Africa. Africa's agribusiness will be worth $1 trillion by 2030. BANKING BANKS 9 AfDB has invested an additional $10m in the Atlantic Coast MARKETS 10 Regional Fund (ACRF) to support fragile states and low- income countries in Western and Central Africa. The ACRF is DEALS 13 a $72m regional fund focused on 29 countries on or near the TECH 14 African Coast of the Atlantic Ocean from Morocco to Angola. ENERGY 15 African water utilities lose as much as $800m a year or 35% of total production, due to leaks, fraud and unpaid bills. MINING 16 According to the World Bank, consumer spending accounted for more than 60% of sub-Saharan Africa's economic growth OIL & GAS 17 last year. INFRASTRUCTURE 18 In Lagos there are three malls for 20m inhabitants. Developers are rushing to build more malls to serve Africa's rapidly AGRIBUSINESS 19 expanding middle class but are struggling to keep pace with the demand for more consumption. TRADE 22 Mobile money in Kenya increased from $1.96bn recorded transactions in 2008 to $17.7bn in 2012 MARKETS INDICATORS 23 37% of Nigerians are unaware of mobile money services, a UPCOMING EVENTS 24 survey found . -

Financial Market Update I Week Ending 21 May 2021 Financial Market Highlights for the Week Ending 21 May 2021

Financial Market Update I Week ending 21 May 2021 Financial market highlights for the week ending 21 May 2021 The following highlights compare the week ending 21 May 2021 to the week ending 13 May 2021: Government securities market (Source: RBM) Equity market (Source: MSE) • A total of K12.73 billion was allotted during this week’s • The stock market was bullish this week as the MASI Treasury Bills (TBs) and 2-Year Treasury Note (TN) marginally increased to 33,606.87 points from 33,398.30 auctions. points in the previous week. This was due to share price • There were nil rejections during the TB auctions. gains for Airtel (to K32.50 from K31.02) and Standard bank • The 2-Year TN had a rejection rate of 13.37%. (to K1,200.15 from K1,200.14), which offset share price • The 364-days TB had the highest subscription rate of losses for MPICO (to K17.00 from K19.00), ICON (to K12.14 59.95%. from K12.16), TNM (to K16.34 from K16.35), and FDH bank (to K16.42 from K16.46), during the period under review. Currency market (Source: RBM) • The year-to-date return of the MASI was 3.75% at the close • Based on middle rates, the Malawi Kwacha marginally of this week. It was negative 5.78% in the previous year, depreciated against the USD by 0.14% to K802.22/USD from during the same period. K801.11/USD in the previous week. Financial market developments (Source: RBM & • Based on middle rates, the Kwacha also depreciated against the GBP (to K1,192.11/GBP from K1,175.77/GBP) , the EUR Company Financials) (to K1,040.81/EUR from K1,025.90/EUR) and the ZAR (to • The average overnight interbank rate maintained its position K61.19/ZAR from K60.45/ZAR), during the period under at 11.92% during the period under review. -

0809-001-112 Relatorio ING.Qxd

Banco BPI 1st Half 2009 This page was intentionally left blank. Report This page was intentionally left blank. Index REPORT Leading business indicators 4 Introduction 5 Governing bodies 7 Shareholders 8 Financial structure and business 9 Distribution channels 12 Human resources 13 Background to operations 14 Domestic commercial banking 22 Bancassurance 29 Asset Management 30 Investment banking 33 Private Equity 37 International banking activity 38 Financial review 41 Risk management 76 Rating 109 Banco BPI shares 110 FINANCIAL STATEMENTS AND NOTES Consolidated financial statements 113 Notes to the consolidated financial statements 119 Declaration 265 Audit Report issued by the Auditor registered with the CMVM 266 Leading business indicators (Consolidated figures in millions of euro, except where indicated otherwise) 30 Jun. 08 30 Jun. 09 Δ% Net total assets 39 745.2 43 531.8 9.5% Assets under management2 12 293.0 10 075.0 (18.0%) Business volume3 66 123.8 67 802.6 2.5% Loans to Customers (gross) and guarantees4 33 599.1 33 472.7 (0.4%) Total Customer resources 32 524.7 34 329.9 5.6% Business volume3 per Employee5 (thousands of euro) 6 999 7 200 2.9% Net operating revenue 529.4 565.7 6.9% Net operating revenue (1st half 2008 adjusted)1 602.4 565.7 (6.1%) Net operating revenue per Employee5 (thousands of euro) 56 60 6.6% Net operating revenue per Employee (1st half 2008 adjusted)1 64 60 (6.4%) Operating costs / Net operating revenue6 64.6% 61.4% Operating costs / Net operating revenue (1st half 2008 adjusted)1 56.7% 61.4% Net profit 9.1 89.0 880.2% Net profit (1st half 2008 adjusted)1 167.5 89.0 (46.9%) Adjusted data per share (euro)7 Net profit7 0.01 0.10 768.2% Net profit (1st half 2008 adjusted)1 0.21 0.10 (52.9%) Book value7 1.89 1.89 0.2% Weighted average no. -

Fdh Bank Plc Summary Consolidated and Separate Financial Statements for the Fdh Bank Year Ended 31 December 2020 Plc

FDH BANK PLC SUMMARY CONSOLIDATED AND SEPARATE FINANCIAL STATEMENTS FOR THE FDH BANK YEAR ENDED 31 DECEMBER 2020 PLC The Directors present the summarized consolidated per share and as at 31 December 2020 the share price and separate financial statements of FDH Bank Plc for had moved to K14.45 per share. KEY HIGHLIGHTS the year ended 31 December 2020. DIVIDEND PERFORMANCE On 8 February 2021, the Directors approved an interim Total Income We are pleased to present the summarized dividend of K3.0 billion in respect of 2020 profits, this consolidated and separate financial statements represents 43t (K0.43) per share. The dividend was for the year ended 31 December 2020. The Group paid on 26 March 2021 to members appearing in the 50 43.6 Billion reported a profit after tax of K14.368 billion and the register of the Company as at close of business on 12 Bank reported a profit after tax of K14.956 billion from March 2021. the Bank’s profit after tax of K5.193 billion in 2019 40 (Restated) amid a challenging operating environment. ACQUISITION OF MSB PROPERTIES LIMITED 30.6 Billion Net Interest Income went up by 77% on the back of an In March 2020, the Bank acquired 100% stake in MSB 30 increase in the loan book and other interest bearing Properties Limited from FDH Money Bureau Limited, assets. Interest expense went up by 15.8% reflecting a sister company. The consideration given for the the growth of the Bank’s deposits. acquisition was K5.599 billion. The Bank has prepared 20 42% a consolidated statement of comprehensive income Increase Non-interest Income in the year was significantly which incorporates the financial results of MSB 10 affected by the Covid-19 pandemic.