Federal Reserve Bank of Chicago

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Monetary Policy in Economies with Little Or No Money

NBER WORKING PAPER SERIES MONETARY POLICY IN ECONOMIES WITH LITTLE OR NO MONEY Bennett T. McCallum Working Paper 9838 http://www.nber.org/papers/w9838 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 July 2003 This paper was prepared for presentation at the December 16-17, 2002, meeting of the Hong Kong Economic Association. I am indebted to Marvin Goodfriend, Lok Sang Ho, Allan Meltzer, and Edward Nelson for helpful comments and suggestions. The views expressed herein are those of the authors and not necessarily those of the National Bureau of Economic Research ©2003 by Bennett T. McCallum. All rights reserved. Short sections of text not to exceed two paragraphs, may be quoted without explicit permission provided that full credit including © notice, is given to the source. Monetary Policy in Economies with Little or No Money Bennett T. McCallum NBER Working Paper No. 9838 July 2003 JEL No. E3, E4, E5 ABSTRACT The paper's arguments include: (1) Medium-of-exchange money will not disappear in the foreseeable future, although the quantity of base money may continue to decline. (2) In economies with very little money (e.g., no currency but bank settlement balances at the central bank), monetary policy will be conducted much as at present by activist adjustment of overnight interest rates. Operating procedures will be different, however, with payment of interest on reserves likely to become the norm. (3) In economies without any money there can be no monetary policy. The relevant notion of a general price level concerns some index of prices in terms of a medium of account. -

Is the International Role of the Dollar Changing?

Is the International Role of the Dollar Changing? Linda S. Goldberg Recently the U.S. dollar’s preeminence as an international currency has been questioned. The emergence of the euro, changes www.newyorkfed.org/research/current_issues ✦ in the dollar’s value, and the fi nancial market crisis have, in the view of many commentators, posed a signifi cant challenge to the currency’s long-standing position in world markets. However, a study of the dollar across critical areas of international trade January 2010 ✦ and fi nance suggests that the dollar has retained its standing in key roles. While changes in the global status of the dollar are possible, factors such as inertia in currency use, the large size and relative stability of the U.S. economy, and the dollar pricing of oil and other commodities will help perpetuate the dollar’s role as the dominant medium for international transactions. Volume 16, Number 1 Volume y many measures, the U.S. dollar is the most important currency in the world. IN ECONOMICS AND FINANCE It plays a central role in international trade and fi nance as both a store of value Band a medium of exchange. Many countries have adopted an exchange rate regime that anchors the value of their home currency to that of the dollar. Dollar holdings fi gure prominently in offi cial foreign exchange (FX) reserves—the foreign currency deposits and bonds maintained by monetary authorities and governments. And in international trade, the dollar is widely used for invoicing and settling import and export transactions around the world. -

Short-Term Currency in Circulation Forecasting for Monetary Policy Purposes: the Case of Poland

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Koziński, Witold; Świst, Tomasz Article Short-term currency in circulation forecasting for monetary policy purposes: The case of Poland e-Finanse: Financial Internet Quarterly Provided in Cooperation with: University of Information Technology and Management, Rzeszów Suggested Citation: Koziński, Witold; Świst, Tomasz (2015) : Short-term currency in circulation forecasting for monetary policy purposes: The case of Poland, e-Finanse: Financial Internet Quarterly, ISSN 1734-039X, University of Information Technology and Management, Rzeszów, Vol. 11, Iss. 1, pp. 65-75, http://dx.doi.org/10.14636/1734-039X_11_1_007 This Version is available at: http://hdl.handle.net/10419/147121 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

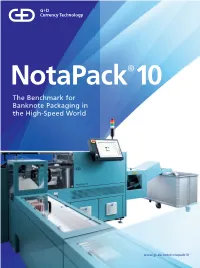

The Benchmark for Banknote Packaging in the High-Speed World

NotaPack®10 The Benchmark for Banknote Packaging in the High-Speed World www.gi-de.com/notapack10 2 NotaPack® 10 3 Concentrated packaging power NotaPack 10 is the leading banknote PHENOMENAL SECURITY MODULAR, COMPACT, FLEXIBLE FULLY AUTOMATIC – INCREASED PRODUCTIVITY – packaging system worldwide for cash Three main factors drive a high level With a high level of product modularity FULLY INTEGRATED INCREASED EFFICIENCY of security: First, intelligent features and optimum flexibility as a result of The G+D High-Speed World is character- NotaPack 10 packages up to 10 bundles centers and banknote printing works, that safeguard the unpackaged bank- over 30 different modules, NotaPack 10 ized by the perfect integration of every of 500 or 1,000 banknotes per minute – engineered in particular for the de- note bundle right up until it is fully can fulfill all key customer requirements. single element, so it is no surprise that quickly, reliably, and to a consistently manding requirements of the industry. shrink-wrapped. These include optical It also offers integration of up to five NotaPack 10 is designed for perfect high level of quality. The system’s energy It is the flawless packaging solution bundle inspection and advanced access BPS systems, and an extremely compact alignment and compatibility with BPS consumption is very low in comparison protection facilitated by continuous design that is suitable for very confined systems and G+D software. Thus, the to other systems. These considerations for the BPS M3, M5, M7, and X9 conveyor covers with locks and log file spaces (taking up floor space of just ideally alligned end-to-end process make the NotaPack 10 a highly efficient, High-Speed Systems, simultaneously writing (p. -

Frequently Asked Questions Coins and Notes July 2020

Frequently Asked Questions Coins and Notes July 2020 A. Currency Issuance 1. Under what authority does the Bangko Sentral ng Pilipinas (BSP) issue currency? The BSP is the sole government institution mandated by law to issue notes and coins for circulation in the Philippines. In Particular, Section 50 of Republic Act (R.A) No. 7653, otherwise known as The New Central Bank Act, as amended by Republic Act No. 11211, stipulates that the BSP shall have the sole power and authority to issue currency within the territory of the Philippines. It also issues legal tender commemorative notes and coins. 2. How does the BSP determine the volume/value of notes and coins to be issued annually? The annual volume/value of currency to be issue is projected based on currency demand that is estimated from a set of economic indicators which generally measure the country’s economic activity. Other variables considered in estimating currency order include: required currency reserves, unfit notes for replacement, and beginning inventory balance. The total amount of banknotes and coins that the BSP may issue should not exceed the total assets of the BSP. 3. How is currency issued to the public? Based on forecast of currency demand, denominational order of banknotes and coins is submitted to the Currency Production Sub-Sector (CPSS) for production of banknotes and coins. The CPSS delivers new BSP banknotes and coins to the Cash Department (CD) and the Regional Operations Sub-Sector (ROSS). In turn, CD services withdrawals of notes and coins of banks in the regions through its 22 Regional Offices/Branches. -

How Goldsmiths Created Money Page 1 of 2

Money: Banking, Spending, Saving, and Investing The Creation of Money How Goldsmiths Created Money Page 1 of 2 If you want to understand money, you have got to start with its history, and that means gold. Have you ever wondered why gold is so valuable? I mean, it is a really weak metal that does not have a lot of really practical uses. Maybe it is because it reminded people of the sun, which was worshipped in ancient times, that everyone decided they wanted it. Once everyone wants it, it is capable as serving as a medium of exchange. That is, gold can be used as money, and it is an ideal commodity to serve as a medium of exchange because it’s portable, it’s durable, it’s divisible, and it’s standardizable. Everybody recognizes what they want, it can be broken into little pieces, carried around, it doesn’t rot, and it is a great thing to serve as money. So, before long, gold is circulating in the form of coins. When gold circulates as coins, it is called commodity money, that is, money that has intrinsic value made out of something people want. Now, once gold coins begin to circulate as the medium of exchange, we have got another problem. That problem is security. Imagine that you are in the ancient world, lugging around bags and bags of gold. You are going to be pretty vulnerable to bandits. So what you want to do is make sure that there is a safe place to store your gold because you can store all of your wealth in the form of this valuable commodity, but you do not want it all lying around somewhere that it is easy for somebody else to pick off. -

Hyperinflationary Economies

Issue 175/October 2020 IFRS Developments Hyperinflationary economies (Updated October 2020) What you need to know Overview • We believe that IAS 29 should Accounting standards are applied on the assumption that the value of money (the be applied in 2020 by entities unit of measurement) is constant over time. However, when the rate of inflation is whose functional currency is the no longer negligible, a number of issues arise impacting the true and fair nature of currency of one of the following the accounts of entities that prepare their financial statements on a historical cost countries: basis, for example: • Argentina • Historical cost figures are less meaningful than they are in a low inflation • Islamic Republic of Iran environment • Lebanon • Holding gains on non-monetary assets that are reported as operating profits do not represent real economic gains • South Sudan • Current and prior period financial information is not comparable • Sudan • ‘Real’ capital can be reduced because profits reported do not take account of • Venezuela the higher replacement costs of resources used in the period • Zimbabwe To address such concerns, entities should apply IAS 29 Financial Reporting in Hyperinflationary Economies from the beginning of the period in which the • We believe the following existence of hyperinflation is identified. countries are not currently hyperinflationary, but should be IAS 29 does not establish an absolute inflation rate at which an economy is monitored in 2020: considered hyperinflationary. Instead, it considers a variety of non-exhaustive characteristics of the economic environment of a country that are seen as strong Angola • indicators of the existence of hyperinflation.This publication only considers the • Liberia absolute inflation rates. -

Nicholas Kaldor

PROFILES OF WORLD ECONOMISTS 26 NICHOLAS KALDOR NICHOLAS KALDOR – ONE OF THE FIRST CRITICS OF MONETARISM doc. Ing. Ján Iša, DrSc. Known in economic circles as one of the thought in several fields, but it was his work founders of Post-Keynesianism, Nicholas on the theory of distribution and economic Kaldor (1908–1986) ranks among the worl- growth that stirred the greatest reaction. d's foremost economists of the second half Less well-known, however, is Kaldor's con- of the 20th century. Kaldor contributed to tribution to monetary theory, which has long the development of modern economic been standing quietly in the background. Nicholas Kaldor was born in Budapest on 12 May 1908. rous Third World countries, as well as an advisor to central His father was a lawyer and his mother came from wealthy banks and to the United Nations Economic Commission for business family. Although his father had wanted him to Latin America. Most significant, however, was his role as an study law, Kaldor opted for economics. He began his studi- advisor to Labour finance ministers from 1964 to 1968 and es at the University of Berlin in 1925 and then after two 1974 to 1976. After completing his two-year mission in years moved to the London School of Economics (LSE), Geneva in 1949, Kaldor began to work at Cambridge Uni- from which he graduated in 1930. He remained at the LSE versity and became, as John Maynard Keynes had been, a as lecturer until 1947, during which time his colleagues inc- fellow of King's College, Cambridge. -

Deterioration and Conservation of Unstable Glass Beads on Native

Issue 63 Autumn 2013 Deterioration and Conservation of Unstable Glass Beads on Native American Objects Robin Ohern and Kelly McHugh lass disease is an important issue for (MAI), established in 1961 by financier George museums with Native American col- Gustav Heye. Heye’s personal collecting began in G lections, and at the National Museum 1903 and continued over a fifty-four year period, of the American Indian (NMAI) it is one of the resulting in one of the largest Native American most pervasive preservation problems. Of 108,338 collections in the world. The Smithsonian Insti- non-archaeological object records in NMAI’s col- tution took over the extensive MAI holdings in lection database, 9,687 (9%) contain glass beads. 1989, establishing the National Museum of the Of these, 200 object records (22%) mention the American Indian. While the collection originally presence of glass disease on the objects. Determin- served Heye’s mission, “The preservation of every- ing how quickly the unstable glass is deteriorating thing pertaining to our American tribes”, NMAI will help with long term collection preservation places its emphasis on partnerships with Native (Figure 1). Additionally, evaluating the effective- peoples and on their contemporary lives. ness of different cleaning techniques over several When the museum joined the Smithsonian years may help to develop better protocols for Institution, the decision was made to construct treating glass beads. This ongoing research project a new building on the National Mall and move will focus on continuing research on glass disease the collection from New York to a storage facil- on ethnographic beadwork in the collection of the ity near Washington, D.C. -

New Monetarist Economics: Methods∗

Federal Reserve Bank of Minneapolis Research Department Staff Report 442 April 2010 New Monetarist Economics: Methods∗ Stephen Williamson Washington University in St. Louis and Federal Reserve Banks of Richmond and St. Louis Randall Wright University of Wisconsin — Madison and Federal Reserve Banks of Minneapolis and Philadelphia ABSTRACT This essay articulates the principles and practices of New Monetarism, our label for a recent body of work on money, banking, payments, and asset markets. We first discuss methodological issues distinguishing our approach from others: New Monetarism has something in common with Old Monetarism, but there are also important differences; it has little in common with Keynesianism. We describe the principles of these schools and contrast them with our approach. To show how it works, in practice, we build a benchmark New Monetarist model, and use it to study several issues, including the cost of inflation, liquidity and asset trading. We also develop a new model of banking. ∗We thank many friends and colleagues for useful discussions and comments, including Neil Wallace, Fernando Alvarez, Robert Lucas, Guillaume Rocheteau, and Lucy Liu. We thank the NSF for financial support. Wright also thanks for support the Ray Zemon Chair in Liquid Assets at the Wisconsin Business School. The views expressed herein are those of the authors and not necessarily those of the Federal Reserve Banks of Richmond, St. Louis, Philadelphia, and Minneapolis, or the Federal Reserve System. 1Introduction The purpose of this essay is to articulate the principles and practices of a school of thought we call New Monetarist Economics. It is a companion piece to Williamson and Wright (2010), which provides more of a survey of the models used in this literature, and focuses on technical issues to the neglect of methodology or history of thought. -

ESTABLISHMENT of a DEPOSIT INSURANCE SYSTEM for the EASTERN CARIBBEAN CURRENCY UNION June 2020 Contents Toc43295216

Eastern Caribbean Central Bank ESTABLISHMENT OF A DEPOSIT INSURANCE SYSTEM FOR THE EASTERN CARIBBEAN CURRENCY UNION June 2020 Contents _Toc43295216 1.0 INTRODUCTION ................................................................................................................... 1 2.0 KEY MESSAGES ...................................................................................................................... 1 A. Policy Goals/Objective ........................................................................................................ 2 B. Summary of Proposed Core Design Features ................................................................ 2 3.0 BACKGROUND ...................................................................................................................... 4 4.0 CRITICAL ELEMENTS OF THE DEPOSIT INSURANCE FUND .................................. 6 4.1 Public Policy Objectives ..................................................................................................... 6 4.2 Mandate and Powers........................................................................................................... 7 4.3 Governance Structure ...................................................................................................... 11 4.4 Relationship with other Financial Safety Net Entities................................................. 13 4.5 Membership........................................................................................................................ 14 4.6 Qualifying Deposits and -

Mick-Vort-Ronald-Books.Pdf

AUSTRALIAN PAPER CURRENCY PUBLICATIONS by Michael P. Vort-Ronald . Period Title Year Pages Hard $ Soft $ Post $ 1803-1826 Aust. Colonial Promissory Notes 2nd 2012 136 36 5 1817-1914 Banks of Issue in Australia (Pvt. notes) 1982 331 30 20 15 (SA 12) 1817-1910 Aust. Private Banknote Pedigrees 2011 268 49 15 (SA 12) 1850-1950 Aust. Shinplasters, Calabashes 2nd ed. 2007 132 25 5 1850-2013 Australian Misc. & Political notes 2nd. 2013 144 36 5 1910-1914 Australian Superscribed Notes 2008 104 22 5 1913-1966 Australian Banknotes (£) 2nd ed. 1983 344 35 20 15 (SA 12) 1913-2012 Australian Specimen Banknotes 2nd ed. 2013 160 39 15 (SA 12) 1966-1997 Australian Decimal Banknotes 2nd ed 1995 416 49 39 15 (SA 12) 1975-2004 Aust. Banknote Pedigrees (sales 72-04) 2005 508 89 69 15 (SA 12) 1975-2014 2nd edition ₤ series $75, Decimal series 2016 188 42 15 (SA 12) 2006 and 7 Australian Banknote Sales 2005, 6 and 2007 ea 22 ea 5 2008-2013 Australian Banknote Sales 2010 to 2015 ea 27 ea 5 1988-2001 Aust. Modern Numismatic Banknotes 2014 116 30 5 1988-2011 Vort-Ronald Aust. Note Collections 2011 150 36 5 1975-2012 Australian Banknote Errors 2013 200 44 15 (SA 12) 2012-2014 Vort-Ronald in CAB magazine 2015 148 36 5 BANKNOTE ALBUM INTERLEAVES (for existing Lighthouse Vario albums) 1910-2009 Superscribed, uncut pairs, prefixes, polymer 4 th ed. ea 20 5 1913-1966 Australian Banknote Album (£) 2005 64 15 (SA 12) 1966-1996 Decimal Banknote Album (paper) 2007 54 15 (SA 12) 1988-2005 Specialist Album, red and black 2006 40 15 (SA 12) 1994-2000 Annually Dated, red and black 2006 25 5 Vario banknote clear pages ($1.50) each.