Guide to Indiana County Government

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simultaneous Cabinet Further Transformation In

6 SIMULTANEOUS CABINET Monday 13 November 2017 FURTHER TRANSFORMATION IN EAST SUFFOLK (REP1629) EXECUTIVE SUMMARY 1. Suffolk Coastal District Council and Waveney District Council agreed in January 2017 to create a new Council for east Suffolk. This was preceded by an intensive period of public consultation in November 2016, the results of which demonstrated that the majority of residents were in favour of one district Council in east Suffolk. 2. The decision to create a new Council for east Suffolk was both ambitious and ground breaking. A “super district” Council will be formed which will be the largest in England in terms of population. The creation of a new Council follows the successful legacy of both Councils working closely together for many years. Officers of all levels of seniority are shared, a joint Business Plan has been adopted and other key policies such as the Housing Strategy are shared. The Councils already share one website under the “East Suffolk” banner and Councillors from both authorities have attended meetings of each Council’s Cabinets since 2010. Cabinet portfolios are aligned and members have shared representation on various outside bodies. 3. The creation of a new Council will be a model other authorities follow as they decide how best to grapple with the significant challenges facing local government. Councils need to be of a scale large enough to face these challenges by having a loud enough voice, a strong bargaining position, a healthy balance sheet and a resilient workforce, yet small enough to feel connected to their residents. The creation of the new Council for east Suffolk will strike that balance. -

List of Councils in England by Type

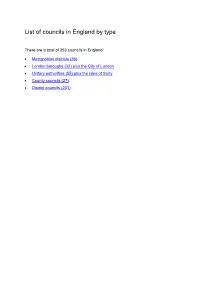

List of councils in England by type There are a total of 353 councils in England: Metropolitan districts (36) London boroughs (32) plus the City of London Unitary authorities (55) plus the Isles of Scilly County councils (27) District councils (201) Metropolitan districts (36) 1. Barnsley Borough Council 19. Rochdale Borough Council 2. Birmingham City Council 20. Rotherham Borough Council 3. Bolton Borough Council 21. South Tyneside Borough Council 4. Bradford City Council 22. Salford City Council 5. Bury Borough Council 23. Sandwell Borough Council 6. Calderdale Borough Council 24. Sefton Borough Council 7. Coventry City Council 25. Sheffield City Council 8. Doncaster Borough Council 26. Solihull Borough Council 9. Dudley Borough Council 27. St Helens Borough Council 10. Gateshead Borough Council 28. Stockport Borough Council 11. Kirklees Borough Council 29. Sunderland City Council 12. Knowsley Borough Council 30. Tameside Borough Council 13. Leeds City Council 31. Trafford Borough Council 14. Liverpool City Council 32. Wakefield City Council 15. Manchester City Council 33. Walsall Borough Council 16. North Tyneside Borough Council 34. Wigan Borough Council 17. Newcastle Upon Tyne City Council 35. Wirral Borough Council 18. Oldham Borough Council 36. Wolverhampton City Council London boroughs (32) 1. Barking and Dagenham 17. Hounslow 2. Barnet 18. Islington 3. Bexley 19. Kensington and Chelsea 4. Brent 20. Kingston upon Thames 5. Bromley 21. Lambeth 6. Camden 22. Lewisham 7. Croydon 23. Merton 8. Ealing 24. Newham 9. Enfield 25. Redbridge 10. Greenwich 26. Richmond upon Thames 11. Hackney 27. Southwark 12. Hammersmith and Fulham 28. Sutton 13. Haringey 29. Tower Hamlets 14. -

![Written Evidence Submitted by East Sussex County Council [ASC 021]](https://docslib.b-cdn.net/cover/0523/written-evidence-submitted-by-east-sussex-county-council-asc-021-280523.webp)

Written Evidence Submitted by East Sussex County Council [ASC 021]

Written evidence submitted by East Sussex County Council [ASC 021] • How has Covid-19 changed the landscape for long-term funding reform of the adult social care sector? The challenges facing the adult social care market prior to the pandemic are well documented and, in many cases, have been brought into sharp focus over the last 12 months. Local Authority published rates; contract arrangements (e.g. block arrangements); commissioning approaches (e.g. strategic partners) and CCG funding agreements including Better Care Fund allocations are all key funding reform considerations which sit alongside the necessity to offer choice, personalised care and high quality, safe services. Residential and nursing care There are 306 registered care homes in East Sussex – the majority are small independently run homes, which don’t have the wrap-around organisational infrastructure enjoyed by larger / national providers. In East Sussex, Local Authority placements are made across around one-third of the residential and nursing care market. At the peak of the second wave over 100 care homes in East Sussex were closed to admissions due to Covid outbreaks. Week commencing 04/01/21 there were 853 confirmed cases of Covid19 in East Sussex care home settings. During 2021, as of the week ending 19/03/2021, East Sussex has had 2,404 deaths registered in total and 1,110 of these have been attributable to COVID-19, of which 597 have occurred in hospital and 436 have occurred in care homes (LG reform data). In the two years up to April 2019, there were 26 residential and nursing home closures in East Sussex resulting in a loss of 435 beds, across all care groups. -

IPPR | Empowering Counties: Unlocking County Devolution Deals ABOUT the AUTHORS

REPORT EMPOWERING COUNTIES UNLOCKING COUNTY DEVOLUTION DEALS Ed Cox and Jack Hunter November 2015 © IPPR 2015 Institute for Public Policy Research ABOUT IPPR IPPR, the Institute for Public Policy Research, is the UK’s leading progressive thinktank. We are an independent charitable organisation with more than 40 staff members, paid interns and visiting fellows. Our main office is in London, with IPPR North, IPPR’s dedicated thinktank for the North of England, operating out of offices in Newcastle and Manchester. The purpose of our work is to conduct and publish the results of research into and promote public education in the economic, social and political sciences, and in science and technology, including the effect of moral, social, political and scientific factors on public policy and on the living standards of all sections of the community. IPPR 4th Floor 14 Buckingham Street London WC2N 6DF T: +44 (0)20 7470 6100 E: [email protected] www.ippr.org Registered charity no. 800065 This paper was first published in November 2015. © 2015 The contents and opinions in this paper are the authors ’ only. POSITIVE IDEAS for CHANGE CONTENTS Summary ............................................................................................................3 1. Devolution unleashed .....................................................................................9 2. Why devolve to counties? ............................................................................11 2.1 Counties and their economic opportunities ................................................... -

985 EDUCATION (2) That the Revised Estimates Of

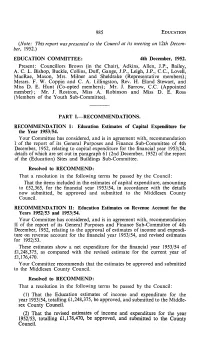

985 EDUCATION (Note: This report was presented to the Council at its meeting on \2th Decem ber, 1952.) EDUCATION COMMITTEE: 4th December, 1952. Present: Councillors Brown (in the Chair), Adkins, Alien, J.P., Bailey, A. C. L. Bishop, Buckle, Collins, Duff, Gange, J.P., Leigh, J.P., C.C., Lovell, MacRae, Mason, Mrs. Milner and Sheldrake (Representative members); Messrs. F. W. Coppin and C. A. Lillingston, Rev. H. Eland Stewart, and Miss D. E. Hunt (Co-opted members); Mr. J. Barrow, C.C. (Appointed member); Mr. J. Rostron, Miss A. Robinson and Miss D. E. Ross (Members of the Youth Sub-Committee). PART I.—RECOMMENDATIONS. RECOMMENDATION I: Education Estimates of Capital Expenditure for the Year 1953/54. Your Committee has considered, and is in agreement with, recommendation I of the report of its General Purposes and Finance Sub-Committee of 4th December, 1952, relating to capital expenditure for the financial year 1953/54, details of which are set out in paragraph 61 (2nd December, 1952) of the report of the (Education) Sites and Buildings Sub-Committee. Resolved to RECOMMEND: That a resolution in the following terms be passed by the Council: That the items included in the estimates of capital expenditure, amounting to £52,365, for the financial year 1953/54, in accordance with the details now submitted, be approved and submitted to the Middlesex County Council. RECOMMENDATION II: Education Estimates on Revenue Account for the Years 1952/53 and 1953/54. Your Committee has considered, and is in agreement with, recommendation II of the report of its General Purposes and Finance Sub-Committee of 4th December, 1952, relating to the approval of estimates of income and expendi ture on revenue account for the financial year 1953/54, and revised estimates for 1952/53. -

Blaenau Gwent County Borough Council Bridgend County Borough Council Caerphilly County Borough Council the City of Cardiff Counc

Welsh Local Authorities gritting information (alphabetical order) Blaenau Gwent Info and map of http://www.blaenau-gwent.gov.uk/resident/highways- County Borough gritting routes cleansing/winter-gritting/winter-gritting-routes-salt-bins/ Council http://www.blaenau- gwent.gov.uk/resident/emergencies-crime- prevention/preparing-for-winter/ Bridgend County Info and map of http://www.bridgend.gov.uk/winter.aspx Borough Council gritting routes http://www.bridgend.gov.uk/services/highways.aspx Caerphilly County Info and map of http://www.caerphilly.gov.uk/Services/Roads-and- Borough Council gritting routes pavements/Gritting-and-snow-clearing/Winter-Service- Plan http://www.news.wales/south/caerphilly-county- borough-council/caerphilly-council-is-monitoring- weather-conditions-2017-01-25740.html The City of Cardiff Info and map of https://www.cardiff.gov.uk/ENG/resident/Parking-roads- Council gritting routes and-travel/Winter-maintenance/Pages/Winter- Location of salt maintenance.aspx bins https://www.cardiff.gov.uk/ENG/resident/Community- safety/Severe-winter- weather/Documents/winter%20weather%20guide.pdf Carmarthenshire Info and map of http://www.carmarthenshire.gov.wales/home/residents/t County Council gritting routes ravel-roads-parking/gritting/#.WH4UVk1DT9Q Twitter https://twitter.com/CarmsCouncil/status/7992671481998 25409 Ceredigion County Info and map of https://www.ceredigion.gov.uk/English/Resident/Travel- Council gritting routes Roads-Parking/Highways-During- Twitter Winter/Pages/default.aspx https://www.ceredigion.gov.uk/English/Resident/Travel- -

List of Elected Officials

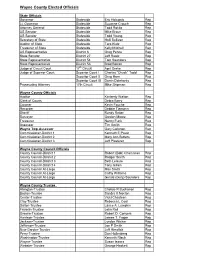

Wayne County Elected Officials State Officials Governor Statewide Eric Holcomb Rep Lt. Governor Statewide Suzanne Crouch Rep Attorney General Statewide Todd Rokita Rep US Senator Statewide Mike Braun Rep US Senator Statewide Todd Young Rep Secretary of State Statewide Holli Sullivan Rep Auditor of State Statewide Tera Klutz Rep Treasurer of State Statewide Kelly Mitchell Rep US Representative District 6 Greg Pence Rep State Senator District 27 Jeff Raatz Rep State Representative District 54 Tom Saunders Rep State Representative District 56 Brad Barrett Rep Judge of Circuit Court 17th Circuit April Drake Rep Judge of Superior Court Superior Court I Charles “Chuck” Todd Rep Superior Court II Greg Horn Rep Superior Court III Darrin Dolehanty Rep Prosecuting Attorney 17th Circuit Mike Shipman Rep Wayne County Officials Auditor Kimberly Walton Rep Clerk of Courts Debra Berry Rep Coroner Kevin Fouche Rep Recorder Debbie Tiemann Rep Sheriff Randy Retter Rep Surveyor Gordon Moore Rep Treasurer Nancy Funk Rep Assessor Tim Smith Rep Wayne Twp-Assessor Gary Callahan Rep Commissioner-District 1 Kenneth E Paust Rep Commissioner-District 2 Mary Ann Butters Rep Commissioner-District 3 Jeff Plasterer Rep Wayne County Council Officials County Council-District 1 Robert (Bob) Chamness Rep County Council-District 2 Rodger Smith Rep County Council-District 3 Beth Leisure Rep County Council-District 4 Tony Gillam Rep County Council At-Large Max Smith Rep County Council At-Large Cathy Williams Rep County Council At-Large Gerald (Gary) Saunders Rep Wayne County Trustee Abington-Trustee Chelsie R Buchanan Rep Boston-Trustee Sandra K Nocton Rep Center-Trustee Vicki Chasteen Rep Clay-Trustee Rebecca L Cool Rep Dalton-Trustee Lance A. -

Caerphilly County Borough Council by Email Only [email protected] Dear Councillor Poole

Our ref: NB Ask for: Communications 01656 641150 Date: 7 September 2020 Communications @ombudsman-wales.org.uk Councillor David Poole Council Leader Caerphilly County Borough Council By Email Only [email protected] Dear Councillor Poole Annual Letter 2019/20 I am pleased to provide you with the Annual letter (2019/20) for Caerphilly County Borough Council. I write this at an unprecedented time for public services in Wales and those that use them. Most of the data in this correspondence relates to the period before the rapid escalation in Covid-19 spread and before restrictions on economic and social activity had been introduced. However, I am only too aware of the impact the pandemic continues to have on us all. I am delighted to report that, during the past financial year, we had to intervene in (uphold, settle or resolve early) a smaller proportion of complaints about public bodies: 20% compared to 24% last year. We also referred a smaller proportion of Code of Conduct complaints to a Standards Committee or the Adjudication Panel for Wales: 2% compared to 3% last year. With regard to new complaints relating to Local Authorities, the overall number has decreased by 2.4% compared to the previous financial year. I am also glad that we had to intervene in a smaller proportion of the cases closed (13% compared to 15% last year). That said, I am concerned that complaint handling persists as one of the main subjects of our complaints again this year. Amongst the main highlights of the year, in 2019 the National Assembly for Wales (now Senedd Cymru Welsh Parliament) passed our new Act. -

THE SANITARY FUNCTIONS of COUNTY COUNCILS. General

428 MTDICBALPJTURAL I SANITARY FUNCTIONS OF COUNTY COUNCILS. [FEB. 23, 1895. traces. Then, again, the line between giving IIa faint opal- Reports under the Housing of the'.Working Classes escence," " giving a very slight precipitate," and " giving no Aet. precipitate," is very difficult to draw, especially when no Applications and questions under the Isolation Hos- strength is given for the solutions nor limit of time for the pitals Act. formation ot a precipitate. It would be a very lengthy task Appeals by parish councils in case of default in sani- indeed to point out these defects in detail, but a comparison tary matters on the part of the rural district council. of the British with other more modern Pharmacopceias will 3. Whether any county medical officer of health had been soon show how much more minute are the instructions given appointed. for testing in these latter. In the first place fourteen administrative counties, accord- To these and similar criticisms from a manufacturer's ing to the returns furnished by the respective clerks, have standpoint there are two objections that are likely to be appointed county medical officers of health. These pioneer taken: first, that they are mere details which it is the counties are: business of the manufacturer to attend to; and, secondly, Bedfordshire Lancasllire Surrey that an absolute standard of should be Cheshire London Worcestershire purity set up and Derbyshire Northumberland Yorkshire, N. Riding adlhered to at any cost. To the first objection it may fairly be Durham Shropshire Yorkslhire, -

Advocacy Guide

Advocacy Guide There are many ways to make a difference as an advocate for people with disabilities. Let Your Local Officials Hear Your Opinion As a citizen, your opinions help elected officials decide how to vote on issues. Let your elected officials know your opinions through letters, e-mails, phone calls, etc. Remember, they are very busy and you want your message to have as much impact as possible. For the most impact, your communication should be brief, clear and focused on just one issue. Attend Public Meetings Meetings of the city council, county council, Indiana General Assembly, school board, etc. are open to the public. Attending these meetings helps keep you informed of the way public business is transacted and how the various elected officials interact. In addition, public meetings give citizens a good opportunity to give their opinions by speaking during the public feedback section of the meetings. Nearly all elected officials host public meetings. They are at schools, libraries, churches, etc. This is your opportunity to hear from your elected official what they are working on and to give your input on issues. Letters to the Editor Writing a letter to the editor is an effective way to publicly discuss an issue and influence the decisions of local officials. Every newspaper has different requirements for letters to the editor. In general, as with letters to elected officials, it is important to be brief, clear, and concise and focus on just one issue. Join an Advocacy Group Joining an advocacy group is one way to increase your awareness to elected officials. -

Indiana Law Review Volume 52 2019 Number 3

Indiana Law Review Volume 52 2019 Number 3 NOTES PUBLIC BUSINESS IS THE PUBLIC’S BUSINESS: KOCH’S IMPLICATIONS FOR INDIANA’S ACCESS TO PUBLIC RECORDS ACT COURTNEY ABSHIRE* INTRODUCTION “Public business is the public’s business. The people have the right to know. Freedom of information is their just heritage. Without that the citizens of a democracy have but changed their kings.” – Harold L. Cross1 In 2016, the Indiana Supreme Court faced the question of whether records requested pursuant to the Access to Public Records Act (“APRA”) could be withheld on the basis of the legislative work product exemption in APRA, and the Court held for the first time that APRA applied to the Indiana General Assembly.2 But the Court declined to review the question of whether the Indiana House Republican Caucus properly denied the requested records out of concern that doing so would violate the distribution of powers provision in the Indiana Constitution.3 The Court principally relied on two precedent cases involving the Indiana Constitution’s distribution of powers provision, Masariu v. Marion Superior Court and Berry v. Crawford, to formulate its holding in Citizens Action Coalition v. Koch.4 Shortly after the Indiana Supreme Court decided Koch, the Indiana Court of Appeals heard a case involving nondisclosure of records by the Governor’s *. J.D. Candidate, 2019, Indiana University Robert H. McKinney School of Law; MPA 2016, Indiana University Purdue University Indianapolis – Indianapolis, Indiana; B.A. 2012, Indiana University Purdue University Indianapolis – Indianapolis, Indiana. I would like to thank Professor Cynthia Baker for her continued guidance and support throughout the Note-writing process. -

52A County and County Borough Councils: Duties of Leaders of Political Groups in Relation to Standards of Conduct

Atodiad 2 /Appendix 2 “52A County and county borough councils: duties of leaders of political groups in relation to standards of conduct (1) A leader of a political group consisting of members of a county council or county borough council in Wales— (a) must take reasonable steps to promote and maintain high standards of conduct by the members of the group, and (b) must co-operate with the council’s standards committee (and any sub-committee of the committee) in the exercise of the standards committee’s functions. (2) In complying with subsection (1), a leader of a political group must have regard to any guidance about the functions under that subsection issued by the Welsh Ministers. (3) The Welsh Ministers may by regulations make provision for the purposes of this section about the circumstances in which— (a) members of a county council or county borough council in Wales are to be treated as constituting a political group; (b) a member of a political group is to be treated as a leader of the group. (4) Before making regulations under subsection (3), the Welsh Ministers must consult such persons as they think appropriate.” ------------------------------------------------------- “(2A) A standards committee of a county council or county borough council in Wales also has the specific functions of— (a) monitoring compliance by leaders of political groups on the council with their duties under section 52A(1), and (b) advising, training or arranging to train leaders of political groups on the council about matters relating to those duties.” ----------------------------------------------------------- “56B Annual reports by standards committees (1) As soon as reasonably practicable after the end of each financial year, a standards committee of a relevant authority must make an annual report to the authority in respect of that year.