And Early Twentieth Centuries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Freeman 1999

Ideas On Liberty July 1999 Vol. 49, No.7 I 8 THOUGHTS on FREEDOM-Outside the Limits by Donald J. Boudreaux 8 Immoral, Unconstitutional War by David N Mayer 1 12 The Kosovo Tangle by Gary Dempsey 16 Remembering and Inventing: A Short History of the Balkans by Peter Mentzel 21 POTOMAC PRINCIPLES-Warmongering for Peace by Doug Bandow 23 Isolationism by Frank Chodorov 26 How War Amplified Federal Power in the Twentieth Century by Robert Higgs 30 Another Place, Another War by Michael Palmer 32 War's Other Casualty by Wendy McElroy 137 Spontaneous Order by Nigel Ashford 43 Storm Trooping to Equality by James Bovard 48 Croaking Frogs by Brian Doherty 81 Noah Smithwick: Pioneer Texan and Monetary Critic by Joseph R. Stromberg 38 IDEAS and CONSEQUENCES-Clinton versus Cleveland and Coolidge on Taxes by Lawrence W. Reed 41 THE THERAPEUTIC STATE-Suicide as a Moral Issue by Thomas Szasz 148 ECONOMIC NOTIONS-In the Absence ofPrivate Property Rights by Dwight R. Lee 54 ECONOMICS on TRIAL-Dismal Scientists Score Another Win by Mark Skousen 63 THE PURSUIT of HAPPINESS-Ignorance Is Bliss-Maybe by Walter Williams 2 Perspective-Operation Legacy by Sheldon Richman 4 Tax Cuts Are Unfair? It Just Ain't So! by David Kelley 58 Book Reviews Overcoming Welfare: Expecting More from the Poor and Ourselves by James L. Payne, reviewed by Robert Batemarco; Coolidge: An American Enigma by Robert Sobel and The Presidency of Calvin Coolidge by Robert Ferrell, reviewed by Raymond 1. Keating; H. L. Mencken Revisited by William H. A. Williams, reviewed by George C. -

Developments in Finance and Domestic and International Trade: 1920-1940

CHAPTER 5 DEVELOPMENTS IN FINANCE AND DOMESTIC AND INTERNATIONAL TRADE: 1920-1940 Domestic Trade retailer and the purchaser. Prices were reduced with a smaller markup over the wholesale price, and a large Suppose that each time we wanted to discover the sales volume and a quicker turnover of the store’s price of or purchase a good we had to travel to the inventory generated profits. producer’s site. In such cases the cost of purchasing each good would be much higher than its price at the Mail Order Firms producer’s location. Of course, this does not happen What changed the department store field in the because a complex network of wholesale and retail twenties was the entrance of Sears Roebuck and firms exists to lower the costs of distributing goods Montgomery Ward, the two dominant mail order and to lower the costs of negotiating transactions. firms in the United States.5 Both firms had begun in Though we sometimes overlook the role of these the late nineteenth century and by 1914 the younger intermediaries, they have, in fact, played an Sears Roebuck had surpassed Montgomery Ward. important role in improving efficiency in the Both located in Chicago due to its central location in economy. the nation’s rail network and both had benefited from In the nineteenth century, a complex array of the advent of Rural Free Delivery in 1896 and low wholesalers, jobbers, and retailers had developed, but cost Parcel Post Service in 1912. changes in the postbellum period reduced the role of In 1924 Sears hired Robert C. -

Chaos Theory: the Essential for Military Applications

U.S. Naval War College U.S. Naval War College Digital Commons Newport Papers Special Collections 10-1996 Chaos Theory: The Essential for Military Applications James E. Glenn Follow this and additional works at: https://digital-commons.usnwc.edu/usnwc-newport-papers Recommended Citation Glenn, James E., "Chaos Theory: The Essential for Military Applications" (1996). Newport Papers. 10. https://digital-commons.usnwc.edu/usnwc-newport-papers/10 This Book is brought to you for free and open access by the Special Collections at U.S. Naval War College Digital Commons. It has been accepted for inclusion in Newport Papers by an authorized administrator of U.S. Naval War College Digital Commons. For more information, please contact [email protected]. The Newport Papers Tenth in the Series CHAOS ,J '.' 'l.I!I\'lt!' J.. ,\t, ,,1>.., Glenn E. James Major, U.S. Air Force NAVAL WAR COLLEGE Chaos Theory Naval War College Newport, Rhode Island Center for Naval Warfare Studies Newport Paper Number Ten October 1996 The Newport Papers are extended research projects that the editor, the Dean of Naval Warfare Studies, and the President of the Naval War CoJIege consider of particular in terest to policy makers, scholars, and analysts. Papers are drawn generally from manuscripts not scheduled for publication either as articles in the Naval War CollegeReview or as books from the Naval War College Press but that nonetheless merit extensive distribution. Candidates are considered by an edito rial board under the auspices of the Dean of Naval Warfare Studies. The views expressed in The Newport Papers are those of the authors and not necessarily those of the Naval War College or the Department of the Navy. -

For Want of a Nail: If Burgoyne Had Won at Saratoga

For Want of a Nail: If Burgoyne Had Won at Saratoga 1853675040, 9781853675041. 442 pages. Greenhill Books/Lionel Leventhal, Limited, 2002. 2002. Robert Sobel. For Want of a Nail: If Burgoyne Had Won at Saratoga. For Want of a Nail is an alternate history classic. The outcome of one battle in the American Revolution diverges from reality, and sparks an unstoppable chain of events which affects the history of the whole North American continent. In reality, the British general John Burgoyne, heavily outnumbered by American troops, surrendered his army to General Horatio Gates at the Battle of Saratoga in 1777, a major turning-point of the Revolution. Robert Sobel takes a step sideways and presents the alternative version: reinforcements arrive at Saratoga, Gates' men flee, and Burgoyne is victorious. Rather than openly allying itself with the American rebels, France withdraws its support, as does Spain, and the colonies surrender. Those former rebels who refuse to live in the Confederation of North America established by the British leave their homes and settle in what becomes the United States of Mexico. From then on the two continental nations find themselves constant rivals, locked in military, political and economic conflict. Sobel provides a detailed, intricately documented insight into two warring powers that develop in such dramatically different ways from their shared origins. file download neveh.pdf Stirling. The Domination. Fiction. ISBN:0671577948. 784 pages. In this "tour de force" of alternate history and military science fiction, Stirling imagines a world where only the United States stands between the Draka and their dream of an. -

Activist Shareholders, Corporate Directors, and Institutional Investment: Some Lessons from the Robber Barons Allen D

Washington and Lee Law Review Volume 50 | Issue 3 Article 4 Summer 6-1-1993 Activist Shareholders, Corporate Directors, And Institutional Investment: Some Lessons From The Robber Barons Allen D. Boyer Follow this and additional works at: https://scholarlycommons.law.wlu.edu/wlulr Part of the Business Organizations Law Commons Recommended Citation Allen D. Boyer, Activist Shareholders, Corporate Directors, And Institutional Investment: Some Lessons From The Robber Barons, 50 Wash. & Lee L. Rev. 977 (1993), https://scholarlycommons.law.wlu.edu/wlulr/vol50/iss3/4 This Article is brought to you for free and open access by the Washington and Lee Law Review at Washington & Lee University School of Law Scholarly Commons. It has been accepted for inclusion in Washington and Lee Law Review by an authorized editor of Washington & Lee University School of Law Scholarly Commons. For more information, please contact [email protected]. ARTICLES ACTIVIST SHAREHOLDERS, CORPORATE DIRECTORS, AND INSTITUTIONAL INVESTMENT: SOME LESSONS FROM THE ROBBER BARONS ALLEN D. BOYER* History never repeats itself, but it rhymes. -Mark Twain I. INTRODUCTION American business has crossed, with little celebration, an economic watershed. As of this decade, 53 percent of the equity in American cor- porations has passed into the hands of institutional shareholders: public pension funds, private pension funds, mutual funds, insurance companies, foundations, and managed trust funds.' In the nation's largest fifty companies, institutional investors own 50.1 percent of outstanding shares. In the next largest fifty companies, they own 59.2 percent of the shares. In some leading industries, the concentration is higher: 56 percent of the aerospace industry, 59 percent of the electrical industry, and 61 percent of the transportation industry. -

Nomination Form

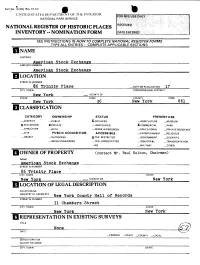

Horm No. 10-300 (Rev. 10-74) UNITED STAThSDHPARTMr OF THE INTERIOR NATIONAL PARK SERVICE NATIONAL REGISTER OF HISTORIC PLACES INVENTORY -- NOMINATION FORM SEE INSTRUCTIONS IN HOWTO COMPLETE NATIONAL REGISTER FORMS TYPE ALL ENTRIES -- COMPLETE APPLICABLE SECTIONS HNAME HISTORIC American Stock Exchange AND/OR COMMON __American Stock Exchange LOCATION STREET & NUMBER 66 Trinity Place _NOT FOR PUBLICATION 17 CITY. TOWN CONGRESSIONAL DISTRICT New York —. VICINITY OF STATE CODE COUNTY CODE New York 36 New York 06l HCLASSIFICATION CATEGORY OWNERSHIP STATUS PRESENT USE . _ DISTRICT _ PUBLIC X.OCCUPIED —AGRICULTURE —MUSEUM X-BuiLDiNG(S) XPRIVATE —UNOCCUPIED X.COMMERCIAL _ PARK —STRUCTURE _BOTH —WORK IN PROGRESS — EDUCATIONAL _ PRIVATE RESIDENCE —SITE PUBLIC ACQUISITION ACCESSIBLE _ ENTERTAINMENT —RELIGIOUS —OBJECT __IN PROCESS X-YES: RESTRICTED _ GOVERNMENT _ SCIENTIFIC _ BEING CONSIDERED — YES: UNRESTRICTED —INDUSTRIAL —TRANSPORTATION _NO —MILITARY _ OTHER: OWNER OF PROPERTY (contact Mr. Paul Kolton, Chairman) NAME American Stock Exchange STREET & NUMBER 86 Trinity Place CITY, TOWN STATE New York VICINITY OF New York LOCATION OF LEGAL DESCRIPTION COURTHOUSE, REGISTRY OF DEEDS, ETC. New York County Hall of Records STREET & NUMBER 31 Chambers-Street CITY. TOWN STATE New York New York REPRESENTATION IN EXISTING SURVEYS TITLE None DATE —FEDERAL —STATE —COUNTY —LOCAL DEPOSITORY FOR SURVEY RECORDS CITY. TOWN STATE DESCRIPTION CONDITION CHECK ONE CHECK ONE X_EXCELLENT _DETERIORATED _UNALTERED X-ORIGINAL SITE __GOOD _RUINS X-ALTERED _MOVED DATE_______ __FAIR _UNEXPOSED ———————————DESCRIBE THE PRESENT AND ORIGINAL (IF KNOWN) PHYSICAL APPEARANCE The present headquarters building of the American Stock Exchange is the only one it has ever occupied. Although the Exchange traces its origins to 18*19, it remained an outdoor market with little formal organization until 1921, when it moved into this newly erected structure at 86 Trinity Place. -

1 David B. Sicilia

David B. Sicilia – curriculum vitae (revised Jan. 2015) Associate Professor email: [email protected] Department of History tel: (011) 301‐405‐7778 Francis Scott Key Hall fax: (011) 301‐314‐9399 www.history.umd.edu/Faculty/DSicilia/ Henry Kaufman Fellow in Business History Center for Financial Policy University of Maryland Robert H. Smith School of Business College Park, MD, USA 20742 RESEARCH AND TEACHING SPECIALTIES American business, economic, and technology history since colonial times U.S. history since 1865 global capitalism since 1450 EDUCATION B.A., New College of Hofstra University, magna cum laude, 1976 Social Sciences Thesis: “A. T. Stewart and the Origins of the Department Store.” Directed by Robert Sobel. Awarded Honors. Humanities Thesis: “Seasons in Retrograde.” Directed by Ignacio Götz. Awarded Honors. Ph.D., Brandeis University, History of American Civilization, 1991 Dissertation: "Selling Power: Marketing and Monopoly at Boston Edison, 1886‐1929." Directed by Alfred D. Chandler, Jr. (Harvard University) and Morton Keller (Brandeis University). Awarded Distinction. PROFESSIONAL APPOINTMENTS Affiliate Faculty Member, Management and Organization, Robert H. Smith School of Business, 2011 Associate Professor, Department of History, University of Maryland, College Park, 2000 Assistant Professor, Department of History, University of Maryland, College Park, 1994 Visiting Assistant Professor, The Ohio State University, 1991‐1992 1 FELLOWSHIPS, GRANTS, AND AWARDS Henry Kaufman Fellow in Business History, Center for Financial Policy, Robert H. Smith School of Business, University of Maryland, College Park, 2010‐present Fulbright Scholar, Department of Intercultural Communication and Management and Department of English, Copenhagen Business School, Denmark, spring 2003 Alfred P. Sloan Foundation grant for research and conferences on The Corporation as a Social and Political Institution, 2001‐2002 Gordon Cain Fellow in Technology, Policy, and Entrepreneurship, Chemical Heritage Foundation, Philadelphia, 1999‐2000 Alfred P. -

The Hudson River Valley Review

THE HUDSON RIVER VA LLEY REVIEW A Journal of Regional Studies The Hudson River Valley Institute at Marist College is supported by a major grant from the National Endowment for the Humanities. Publisher Thomas S. Wermuth, Vice President for Academic Affairs, Marist College Editors Christopher Pryslopski, Program Director, Hudson River Valley Institute, Marist College Reed Sparling, Writer, Scenic Hudson Editorial Board The Hudson River Valley Review Myra Young Armstead, Professor of History, (ISSN 1546-3486) is published twice Bard College a year by The Hudson River Valley Institute at Marist College. BG (Ret) Lance Betros, Dean of Academics, U.S. Army War College Executive Director Kim Bridgford, Professor of English, James M. Johnson, West Chester University Poetry Center The Dr. Frank T. Bumpus Chair in and Conference Hudson River Valley History Michael Groth, Professor of History, Wells College Research Assistants A lex Gobright Susan Ingalls Lewis, Associate Professor of History, Marygrace Navarra State University of New York at New Paltz Hudson River Valley Institute COL Matthew Moten, Professor and Head, Advisory Board Department of History, U.S. Military Alex Reese, Chair Academy at West Point Barnabas McHenry, Vice Chair Sarah Olson, Superintendent, Roosevelt- Peter Bienstock Vanderbilt National Historic Sites Margaret R. Brinckerhoff Roger Panetta, Professor of History, Dr. Frank T. Bumpus Fordham University Frank J. Doherty BG (Ret) Patrick J. Garvey H. Daniel Peck, Professor of English Emeritus, Shirley M. Handel Vassar College Maureen Kangas Robyn L. Rosen, Associate Professor of History, Mary Etta Schneider Marist College Gayle Jane Tallardy David Schuyler, Professor of American Studies, Robert E. Tompkins Sr. -

Dane Stangler

Dane Stangler Creative Discovery Reconsidering the Relationship Between Entrepreneurship and Innovation The severe recession of 2008–09 has brought to the fore deep concerns regarding the U.S. economy’s ability to continue to grow, let alone to keep pace with emerg- ing nations such as India and China. The scale of job losses and the woes of sec- tors that are emblematic of the recession—particularly finance and automakers— have left many worrying about a bleak American economic future. Even those who expect a return to growth worry about the United States’ capacity to supply two essential ingredients: innovation and entrepreneurship. Such concerns have spurred increasing investment in broadband Internet connections, additional funding for research and development (R&D), and the largest-ever federal invest- ment in public education—all steps meant to help build a new foundation for eco- nomic growth. Public-sector efforts of this type are nothing new in U.S. history. They date back at least to the Morrill and Hatch acts in the late 1800s and continue through the massive expansion of federal investment in R&D after World War II.1 Such actions are generally credited with helping to ignite bursts of innovation and maintain steady rates of economic growth. In its renewed efforts today, the United States joins Singapore, the European Union, and others in forming deliberate strategies to provide what are considered semipublic goods: the knowledge and the people necessary for productive firms to innovate, create jobs, and boost econom- ic growth.2 It’s far from clear, however, whether the phenomena of innovation and entrepreneurship are adequately understood for these entities to be making such large commitments. -

John Burgoyne - Wikipedia, the Free Encyclopedia

John Burgoyne - Wikipedia, the free encyclopedia https://en.wikipedia.org/wiki/John_Burgoyne From Wikipedia, the free encyclopedia General John Burgoyne (24 February 1722 – 4 August 1792) was a British army officer, politician and dramatist. John Burgoyne He first saw action during the Seven Years' War when he participated in several battles, most notably during the Portugal Campaign of 1762. John Burgoyne is best known for his role in the American Revolutionary War. He designed an invasion scheme and was appointed to command a force moving south from Canada to split away New England and end the rebellion. Burgoyne advanced from Canada but his slow movement allowed the Americans to concentrate their forces. Instead of coming to his aid according to the overall plan, the British Army in New York City moved south to capture Philadelphia. Surrounded, Burgoyne fought two small battles near Saratoga to break out. Trapped by superior American forces, with no relief in sight, Burgoyne surrendered his entire army of 6,200 men on 17 October Portrait by Joshua Reynolds, c. 1766 1777. His surrender, says historian Edmund Morgan, "was a Nickname(s) Gentleman Johnny great turning point of the war, because it won for Americans Born 24 February 1722 the foreign assistance which was the last element needed for Sutton, Bedfordshire, England victory".[1] He and his officers returned to England; the enlisted men became prisoners of war. Burgoyne came under Died 4 August 1792 (aged 70) sharp criticism when he returned to London, and never held Mayfair, London, England another active command. Buried at Westminster Abbey Burgoyne was also an accomplished playwright known for Allegiance Great Britain his works such as The Maid of the Oaks and The Heiress, Service/branch British Army but his plays never reached the fame of his military career. -

Financial Fraud Throughout History: a Forensic Approach

FINANCIAL FRAUD THROUGHOUT HISTORY: A FORENSIC APPROACH MGT 848 01 (SP13) Mondays, March 23 to May 4, 2014 Time: 2:40 p.m. to 5:40 p.m. Room: EVANS 4200 Lecturer in Finance James S. Chanos (YC ‘80) Contact Information: c/o Alexis Israel Kynikos Associates LP (212) 649-0200 [email protected] Faculty Assistants: Rhona J. Ceppos James D. Spellman (203) 436-8861 (202) 232-3860 [email protected] [email protected] Mobile: (202) 679 1692 OVERVIEW________________________________________________ Financial frauds occur often, leaving investors to suffer huge losses while undermining public trust and confidence in capital markets. As Howard M. Schilit and Jeremy Perler write in their book Financial Shenanigans, “dishonest companies continue to find new tricks (and recycle old favorites) to fool investors,” taking advantage of “grey areas” in the accounting rules to exaggerate the positive and downplay the negative. What constitutes “financial fraud?” Is there “legal fraud,” as author Bethany McLean posits? How does “control fraud,” William Black’s concept, work? Are “willful blindness” (intentionally putting yourself in a position where you will be unaware of facts that could render you liable; “What could you have known?”) and “conscious disregard” (intentionally looking the other way) useful doctrines (tools) for the prosecution? The effective counter-arguments from the defense? What types of financial fraud have been most prevalent throughout history? What models can financial detectives use to detect fraud? What financial and nonfinancial -

Viewpoint of His Administration and the Resulting War Almost Vacant

TROUBLE ALONG THE BORDER: THE TRANSFORMATION OF THE U.S.-MEXICAN BORDER DURING THE NINETEENTH CENTURY Ryan Duffy A Thesis Submitted to the Graduate College of Bowling Green State University in partial fulfillment of the requirements for the degree of MASTERS OF ARTS: August 2013: Committee: Dr. Amílcar Challú, Advisor Dr. Scott Martin Dr. Rebecca Mancuso © 2013 Ryan Duffy All Rights Reserved iii ABSTRACT Dr. Amílcar Challú, Advisor The purpose of this thesis is to analyze the transformation of U.S.-Mexican relations throughout the nineteenth century and its impact on the border during the administrations of James K. Polk and Rutherford B. Hayes. This transformation is exemplified by the movement away from hostile interactions during Polk’s presidency to the cooperative nature that arose between Hayes and, then President of Mexico, Porfirio Díaz. In addition, another aim was to place the importance of the public sphere in framing the policy making of the United States and Mexican governments. The thesis focused upon the research surrounding Polk, Hayes, and their interactions with Mexico during their terms as president. The secondary materials were supplemented with corresponding primary source material from the presidents as well as their close advisors such as newspaper articles, correspondences, and speeches from both the United States and Mexico. The conclusion of the work demonstrates that the transformation in the border, first, the United States to become the dominant power on the continent, ending its rivalry with Mexico. Second, the ability of Porfirio Díaz to bring some stability to the Mexican political structure that permitted him to work in conjunction with the United States to control the border in exchange for recognition.