Competing with the Nyse

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Freeman 1999

Ideas On Liberty July 1999 Vol. 49, No.7 I 8 THOUGHTS on FREEDOM-Outside the Limits by Donald J. Boudreaux 8 Immoral, Unconstitutional War by David N Mayer 1 12 The Kosovo Tangle by Gary Dempsey 16 Remembering and Inventing: A Short History of the Balkans by Peter Mentzel 21 POTOMAC PRINCIPLES-Warmongering for Peace by Doug Bandow 23 Isolationism by Frank Chodorov 26 How War Amplified Federal Power in the Twentieth Century by Robert Higgs 30 Another Place, Another War by Michael Palmer 32 War's Other Casualty by Wendy McElroy 137 Spontaneous Order by Nigel Ashford 43 Storm Trooping to Equality by James Bovard 48 Croaking Frogs by Brian Doherty 81 Noah Smithwick: Pioneer Texan and Monetary Critic by Joseph R. Stromberg 38 IDEAS and CONSEQUENCES-Clinton versus Cleveland and Coolidge on Taxes by Lawrence W. Reed 41 THE THERAPEUTIC STATE-Suicide as a Moral Issue by Thomas Szasz 148 ECONOMIC NOTIONS-In the Absence ofPrivate Property Rights by Dwight R. Lee 54 ECONOMICS on TRIAL-Dismal Scientists Score Another Win by Mark Skousen 63 THE PURSUIT of HAPPINESS-Ignorance Is Bliss-Maybe by Walter Williams 2 Perspective-Operation Legacy by Sheldon Richman 4 Tax Cuts Are Unfair? It Just Ain't So! by David Kelley 58 Book Reviews Overcoming Welfare: Expecting More from the Poor and Ourselves by James L. Payne, reviewed by Robert Batemarco; Coolidge: An American Enigma by Robert Sobel and The Presidency of Calvin Coolidge by Robert Ferrell, reviewed by Raymond 1. Keating; H. L. Mencken Revisited by William H. A. Williams, reviewed by George C. -

And Early Twentieth Centuries

A Broker's Duty of Best Execution in the Nineteenth and Early Twentieth Centuries Francis J. Facciolo' Introduction Although a broker-dealer's duty of best execution can now be located in federal common law, self-regulatory organization ("SRO") regulations, or state common law, the root of the doctrine is conventionally found in the third area, state law. In this view, the common law duty of best execution is a particular manifestation of a broker's more general duties as an agent to its customers.1 The duty of best execution may be broadly characterized as a fiduciary one, or as a2 limited duty, due with respect only to a particular purchase or sale. Even in jurisdictions where a broker is not a fiduciary, however, courts require brokers, as agents, to give best execution to their customers.3 One well known treatise has summarized the common law duty of best execution as consisting of three things: "the duty to execute promptly; the duty to execute in an appropriate market; and the duty to obtain the best price.'A Different types of customers put differing . Francis J. Facciolo is on the faculty of the St. John's University School of Law. The Author thanks Maria Boboris and David J. Grech for their research assistance; William H. Manz and the St. John's University School of Law library staff for their generous help in locating many obscure research materials; Dean Mary C. Daly for a summer research grant, which enabled me to start this article; and Professor James A. Fanto for his insightful comments on an earlier draft of this article that was presented at Pace Law School's Investor Rights Symposium. -

Developments in Finance and Domestic and International Trade: 1920-1940

CHAPTER 5 DEVELOPMENTS IN FINANCE AND DOMESTIC AND INTERNATIONAL TRADE: 1920-1940 Domestic Trade retailer and the purchaser. Prices were reduced with a smaller markup over the wholesale price, and a large Suppose that each time we wanted to discover the sales volume and a quicker turnover of the store’s price of or purchase a good we had to travel to the inventory generated profits. producer’s site. In such cases the cost of purchasing each good would be much higher than its price at the Mail Order Firms producer’s location. Of course, this does not happen What changed the department store field in the because a complex network of wholesale and retail twenties was the entrance of Sears Roebuck and firms exists to lower the costs of distributing goods Montgomery Ward, the two dominant mail order and to lower the costs of negotiating transactions. firms in the United States.5 Both firms had begun in Though we sometimes overlook the role of these the late nineteenth century and by 1914 the younger intermediaries, they have, in fact, played an Sears Roebuck had surpassed Montgomery Ward. important role in improving efficiency in the Both located in Chicago due to its central location in economy. the nation’s rail network and both had benefited from In the nineteenth century, a complex array of the advent of Rural Free Delivery in 1896 and low wholesalers, jobbers, and retailers had developed, but cost Parcel Post Service in 1912. changes in the postbellum period reduced the role of In 1924 Sears hired Robert C. -

Franklin D. Roosevelt

Louisiana State University LSU Digital Commons LSU Historical Dissertations and Theses Graduate School 1957 A Rhetorical Study of the Gubernatorial Speaking of Franklin D. Roosevelt. Paul Jordan Pennington Louisiana State University and Agricultural & Mechanical College Follow this and additional works at: https://digitalcommons.lsu.edu/gradschool_disstheses Recommended Citation Pennington, Paul Jordan, "A Rhetorical Study of the Gubernatorial Speaking of Franklin D. Roosevelt." (1957). LSU Historical Dissertations and Theses. 222. https://digitalcommons.lsu.edu/gradschool_disstheses/222 This Dissertation is brought to you for free and open access by the Graduate School at LSU Digital Commons. It has been accepted for inclusion in LSU Historical Dissertations and Theses by an authorized administrator of LSU Digital Commons. For more information, please contact [email protected]. A RHETORICAL STUD* OP THE GUBERNATORIAL SPEAKING OP FRANKLIN D. ROOSEVELT A Dissertation Submitted to the Graduate Faculty of the Louisiana State University and Agricultural and Meohanical College in partial fulfillment of the requirements for the degree of Doctor of Philosophy in The Department of Speech by Paul Jordan Pennington B. A., Henderson State Teachers College, 19U8 M. A., Oklahoma University, 1950 August, 1957 ACKNOWLEDGMENT The writer wishes to acknowledge the inspiration, guidance, and continuous supervision of Dr. Waldo W. Braden, Professor of Speech at Louisiana State University. As the writer1s major advisor, he has given generously of his time, his efforts, and his sound advice. Dr. Braden is in no way responsible for any errors or short-comings of this study, but his suggestions are largely responsible for any merits it may possess. Dr. C. M. Wise, Head of the Department of Speech, and Dr. -

Chaos Theory: the Essential for Military Applications

U.S. Naval War College U.S. Naval War College Digital Commons Newport Papers Special Collections 10-1996 Chaos Theory: The Essential for Military Applications James E. Glenn Follow this and additional works at: https://digital-commons.usnwc.edu/usnwc-newport-papers Recommended Citation Glenn, James E., "Chaos Theory: The Essential for Military Applications" (1996). Newport Papers. 10. https://digital-commons.usnwc.edu/usnwc-newport-papers/10 This Book is brought to you for free and open access by the Special Collections at U.S. Naval War College Digital Commons. It has been accepted for inclusion in Newport Papers by an authorized administrator of U.S. Naval War College Digital Commons. For more information, please contact [email protected]. The Newport Papers Tenth in the Series CHAOS ,J '.' 'l.I!I\'lt!' J.. ,\t, ,,1>.., Glenn E. James Major, U.S. Air Force NAVAL WAR COLLEGE Chaos Theory Naval War College Newport, Rhode Island Center for Naval Warfare Studies Newport Paper Number Ten October 1996 The Newport Papers are extended research projects that the editor, the Dean of Naval Warfare Studies, and the President of the Naval War CoJIege consider of particular in terest to policy makers, scholars, and analysts. Papers are drawn generally from manuscripts not scheduled for publication either as articles in the Naval War CollegeReview or as books from the Naval War College Press but that nonetheless merit extensive distribution. Candidates are considered by an edito rial board under the auspices of the Dean of Naval Warfare Studies. The views expressed in The Newport Papers are those of the authors and not necessarily those of the Naval War College or the Department of the Navy. -

For Want of a Nail: If Burgoyne Had Won at Saratoga

For Want of a Nail: If Burgoyne Had Won at Saratoga 1853675040, 9781853675041. 442 pages. Greenhill Books/Lionel Leventhal, Limited, 2002. 2002. Robert Sobel. For Want of a Nail: If Burgoyne Had Won at Saratoga. For Want of a Nail is an alternate history classic. The outcome of one battle in the American Revolution diverges from reality, and sparks an unstoppable chain of events which affects the history of the whole North American continent. In reality, the British general John Burgoyne, heavily outnumbered by American troops, surrendered his army to General Horatio Gates at the Battle of Saratoga in 1777, a major turning-point of the Revolution. Robert Sobel takes a step sideways and presents the alternative version: reinforcements arrive at Saratoga, Gates' men flee, and Burgoyne is victorious. Rather than openly allying itself with the American rebels, France withdraws its support, as does Spain, and the colonies surrender. Those former rebels who refuse to live in the Confederation of North America established by the British leave their homes and settle in what becomes the United States of Mexico. From then on the two continental nations find themselves constant rivals, locked in military, political and economic conflict. Sobel provides a detailed, intricately documented insight into two warring powers that develop in such dramatically different ways from their shared origins. file download neveh.pdf Stirling. The Domination. Fiction. ISBN:0671577948. 784 pages. In this "tour de force" of alternate history and military science fiction, Stirling imagines a world where only the United States stands between the Draka and their dream of an. -

Activist Shareholders, Corporate Directors, and Institutional Investment: Some Lessons from the Robber Barons Allen D

Washington and Lee Law Review Volume 50 | Issue 3 Article 4 Summer 6-1-1993 Activist Shareholders, Corporate Directors, And Institutional Investment: Some Lessons From The Robber Barons Allen D. Boyer Follow this and additional works at: https://scholarlycommons.law.wlu.edu/wlulr Part of the Business Organizations Law Commons Recommended Citation Allen D. Boyer, Activist Shareholders, Corporate Directors, And Institutional Investment: Some Lessons From The Robber Barons, 50 Wash. & Lee L. Rev. 977 (1993), https://scholarlycommons.law.wlu.edu/wlulr/vol50/iss3/4 This Article is brought to you for free and open access by the Washington and Lee Law Review at Washington & Lee University School of Law Scholarly Commons. It has been accepted for inclusion in Washington and Lee Law Review by an authorized editor of Washington & Lee University School of Law Scholarly Commons. For more information, please contact [email protected]. ARTICLES ACTIVIST SHAREHOLDERS, CORPORATE DIRECTORS, AND INSTITUTIONAL INVESTMENT: SOME LESSONS FROM THE ROBBER BARONS ALLEN D. BOYER* History never repeats itself, but it rhymes. -Mark Twain I. INTRODUCTION American business has crossed, with little celebration, an economic watershed. As of this decade, 53 percent of the equity in American cor- porations has passed into the hands of institutional shareholders: public pension funds, private pension funds, mutual funds, insurance companies, foundations, and managed trust funds.' In the nation's largest fifty companies, institutional investors own 50.1 percent of outstanding shares. In the next largest fifty companies, they own 59.2 percent of the shares. In some leading industries, the concentration is higher: 56 percent of the aerospace industry, 59 percent of the electrical industry, and 61 percent of the transportation industry. -

Nomination Form

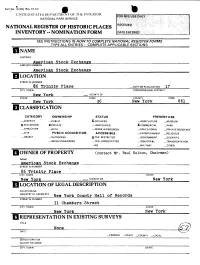

Horm No. 10-300 (Rev. 10-74) UNITED STAThSDHPARTMr OF THE INTERIOR NATIONAL PARK SERVICE NATIONAL REGISTER OF HISTORIC PLACES INVENTORY -- NOMINATION FORM SEE INSTRUCTIONS IN HOWTO COMPLETE NATIONAL REGISTER FORMS TYPE ALL ENTRIES -- COMPLETE APPLICABLE SECTIONS HNAME HISTORIC American Stock Exchange AND/OR COMMON __American Stock Exchange LOCATION STREET & NUMBER 66 Trinity Place _NOT FOR PUBLICATION 17 CITY. TOWN CONGRESSIONAL DISTRICT New York —. VICINITY OF STATE CODE COUNTY CODE New York 36 New York 06l HCLASSIFICATION CATEGORY OWNERSHIP STATUS PRESENT USE . _ DISTRICT _ PUBLIC X.OCCUPIED —AGRICULTURE —MUSEUM X-BuiLDiNG(S) XPRIVATE —UNOCCUPIED X.COMMERCIAL _ PARK —STRUCTURE _BOTH —WORK IN PROGRESS — EDUCATIONAL _ PRIVATE RESIDENCE —SITE PUBLIC ACQUISITION ACCESSIBLE _ ENTERTAINMENT —RELIGIOUS —OBJECT __IN PROCESS X-YES: RESTRICTED _ GOVERNMENT _ SCIENTIFIC _ BEING CONSIDERED — YES: UNRESTRICTED —INDUSTRIAL —TRANSPORTATION _NO —MILITARY _ OTHER: OWNER OF PROPERTY (contact Mr. Paul Kolton, Chairman) NAME American Stock Exchange STREET & NUMBER 86 Trinity Place CITY, TOWN STATE New York VICINITY OF New York LOCATION OF LEGAL DESCRIPTION COURTHOUSE, REGISTRY OF DEEDS, ETC. New York County Hall of Records STREET & NUMBER 31 Chambers-Street CITY. TOWN STATE New York New York REPRESENTATION IN EXISTING SURVEYS TITLE None DATE —FEDERAL —STATE —COUNTY —LOCAL DEPOSITORY FOR SURVEY RECORDS CITY. TOWN STATE DESCRIPTION CONDITION CHECK ONE CHECK ONE X_EXCELLENT _DETERIORATED _UNALTERED X-ORIGINAL SITE __GOOD _RUINS X-ALTERED _MOVED DATE_______ __FAIR _UNEXPOSED ———————————DESCRIBE THE PRESENT AND ORIGINAL (IF KNOWN) PHYSICAL APPEARANCE The present headquarters building of the American Stock Exchange is the only one it has ever occupied. Although the Exchange traces its origins to 18*19, it remained an outdoor market with little formal organization until 1921, when it moved into this newly erected structure at 86 Trinity Place. -

Franklin D. Roosevelt- "The Great Communicator" the Master Speech Files, 1898, 1910-1945

Franklin D. Roosevelt- "The Great Communicator" The Master Speech Files, 1898, 1910-1945 Series 1: Franklin D. Roosevelt's Political Ascension File No. 397 1930 October 20 Buffalo, NY - Campaign Speech lDDP.!S3 O.F GOV"~·!f)J, l'RIJl!LW ll. IOOSFVl"l.! Ar 91FHLO, 1IZll !0•.1 1 OC!OB!B 201 19)0 I •• gl~d tD COM bacll: to the City or fil!f do 'llbero I bne been ao oft en dlll'ini 111 ada1n1otrot1on or ~.., yeera o.a Gonmor of the Swu. In raet, I haYO - to t.bis ,.....,t ~ du1triel canter no oft ao tbLt o!le of ay p<rt.y ael d t'> ea aa we •re eoaing in!D the city, "We h• ve e11terocl a.r ralo rroa o.ll dlreo Uows. le bl!ve coae i n ft'Oa the South, Eut and llortbl i t 1a obout. tiM t o COlli" 1n by boRt or in ao •lrpl<ne. • I rec· ll .nt h plenure and m t lar.. euoa 111 nalt ber~> c urln& July lllleo thr Deaocn tic Pe rty or Brie Cowtty held it• unotficid. convonti~n. the eathu.si~>oa of t.ht aHtin&, th l•rro attondbnca und t.ho Wl£niaous encors011cat of our preoent Deroocretic Stlto odollniatr<tlon led "' to .,rodlot then 'llbat I now r""ff1ra, tb•t in this county the lleeeratlc caocll detaa ll7 last ..taU. to &ffDlo in thl' zontb or ~lliuat. wee to attend o convention of the Gut• Feda.-.tlon of I.obor. Thla e1ty prortd•s • lor,. -

An Examination of New Yorkâ•Žs Martin Act As a Tool To

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Digital Commons @ Boston College Law School Boston College Environmental Affairs Law Review Volume 44 | Issue 1 Article 5 4-6-2017 An Examination of New York’s Martin Act as a Tool to Combat Climate Change Ashley Poon Boston College Law School, [email protected] Follow this and additional works at: http://lawdigitalcommons.bc.edu/ealr Part of the Administrative Law Commons, Energy and Utilities Law Commons, Environmental Law Commons, and the Oil, Gas, and Mineral Law Commons Recommended Citation Ashley Poon, An Examination of New York’s Martin Act as a Tool to Combat Climate Change, 44 B.C. Envtl. Aff. L. Rev. 115 (2017), http://lawdigitalcommons.bc.edu/ealr/vol44/iss1/5 This Notes is brought to you for free and open access by the Law Journals at Digital Commons @ Boston College Law School. It has been accepted for inclusion in Boston College Environmental Affairs Law Review by an authorized editor of Digital Commons @ Boston College Law School. For more information, please contact [email protected]. AN EXAMINATION OF NEW YORK’S MARTIN ACT AS A TOOL TO COMBAT CLIMATE CHANGE ASHLEY POON* Abstract: Environmental statutes and regulations in the United States have largely failed to comprehensively control the human activities that cause cli- mate change. This Note examines a novel approach to the matter in the form of an investigation led by New York Attorney General Eric Schneiderman to discover how ExxonMobil incorporates its climate change research into its corporate governance, accounting, and business planning. -

1 the Association for Diplomatic Studies and Training Foreign Affairs

The Association for Diplomatic Studies and Training Foreign Affairs Oral History Project AMBASSADOR PHILIP M. KAISER Interviewed by: Charles Stuart Kennedy Initial interview date: May 4, 2005 Copyright 2006 ADST TABLE OF CONTENTS Background Born and raised in New York City University of Wisconsin The depression and liberalism La Follette Balliol College, Oxford University (,hodes Scholar- Hitler and appeasement Byron .Whi//er0 White Ambassador 1oseph 2ennedy America First organi/ation Federal ,eserve System 133351342 Board of Economic Warfare9 Chief, Project operations 134251346 State Department9 Chief, ,esearch, Planning Division 1346 U and speciali/ed agency affairs State Department9 Bureau of International Affairs 134651347 Assistant to the assistant Secretary State Department9 Director, Office of International Labor Affairs 134751343 Labor leaders Dean Acheson World Federation of Trade Unions Trade Union Advisory Committee Labor Attaches Assistant Secretary of Labor for International Affairs 134351353 Communist activities European trade unions International Labor Organi/ation (ILO- David Dubinsky 1 Marshall Plan Maurice Tobin General MacArthur Committee for Free Europe 1354 ,adio Free Europe Special Asst. to the Governor of New York, Averill Harriman 13555135A Labor issues Election campaign Adlai Stevenson Sue/ Crisis (1356- elson ,ockefeller Professor, American University 135A51361 Presidential election campaign Ambassador to Senegal and Mauritania 136151364 Senegal5Mali split The French Environment Cuban Missile Crisis Peace Corps -

Download Full Book

Neighbors in Conflict Bayor, Ronald H. Published by Johns Hopkins University Press Bayor, Ronald H. Neighbors in Conflict: The Irish, Germans, Jews, and Italians of New York City, 1929-1941. Johns Hopkins University Press, 1978. Project MUSE. doi:10.1353/book.67077. https://muse.jhu.edu/. For additional information about this book https://muse.jhu.edu/book/67077 [ Access provided at 27 Sep 2021 07:22 GMT with no institutional affiliation ] This work is licensed under a Creative Commons Attribution 4.0 International License. HOPKINS OPEN PUBLISHING ENCORE EDITIONS Ronald H. Bayor Neighbors in Conflict The Irish, Germans, Jews, and Italians of New York City, 1929–1941 Open access edition supported by the National Endowment for the Humanities / Andrew W. Mellon Foundation Humanities Open Book Program. © 2019 Johns Hopkins University Press Published 2019 Johns Hopkins University Press 2715 North Charles Street Baltimore, Maryland 21218-4363 www.press.jhu.edu The text of this book is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License: https://creativecommons.org/licenses/by-nc-nd/4.0/. CC BY-NC-ND ISBN-13: 978-1-4214-2990-8 (open access) ISBN-10: 1-4214-2990-X (open access) ISBN-13: 978-1-4214-3062-1 (pbk. : alk. paper) ISBN-10: 1-4214-3062-2 (pbk. : alk. paper) ISBN-13: 978-1-4214-3102-4 (electronic) ISBN-10: 1-4214-3102-5 (electronic) This page supersedes the copyright page included in the original publication of this work. NEIGHBORS IN CONFLICT THE JOHNS HOPKINS UNIVERSITY STUDIES IN HISTORICAL AND POLITICAL SCIENCE NINETY-SIXTH SEMES (1978) 1.