Go Air (Go First) IPO DRHP Takeaways

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Go Air – an Airline Operations Review

International Journal of Scientific Research and Engineering Development-– Volume 3 Issue 2, Mar-Apr 2020 Available at www.ijsred.com RESEARCH ARTICLE OPEN ACCESS Go Air – An Airline Operations Review Anuj Modgil*, Kanishk Rastogi**, Mohit Mohan Saxena***, Epari Shravan****, Prof. Vidhya Srinivas***** *(Student, Universal Business School, Mumbai Email: [email protected]) ** (Student, Universal Business School, Mumbai Email :[email protected]) ***(Student, Universal Business School, Mumbai Email: [email protected]) **** (Student, Universal Business School, Mumbai Email : [email protected]) ***** (Professor, Universal Business School, Mumbai Email : [email protected]) ---------------------------------------- ************************ ---------------------------------- Abstract: GoAir is an international carrier based in Mumbai, Maharashtra, India. It is a low-cost carrier, owned by Wadia Group. The airline company has 9% market share in the Indian domestic carrier market. GoAir started its operations back in 2005 with the first flight being operated on Mumbai - Ahmedabad sector on 4 - November - 2005. The airline was one of the first in India to operate the Airbus A320 aircraft in an all economy setup. Initially GoAir operated just a single aircraft and was able to cover four destinations across India. As of January 2019, GoAir owned a fleet of 48 Airbus A320 aircrafts with 114 more on order. The airline operates 230+ daily flights which are spread across 26 destinations (24 domestic and 2 international). This paper is an operations review of the airlines. Keywords —GoAir, Airlines, Aviation, Operations, Management, Fleet, Airport, Industry . ---------------------------------------- ************************ ---------------------------------- next set of passengers are ready to board the aircraft I. INTRODUCTION for the next destination on the route. This gives a GoAir has a reputation of being Slow, Very Slow mere 20 minutes to the ground staff to prepare the in expanding its business. -

Starview E-Paper

Mahindra Logistics Limited Mahindra Unit No. 3 & 4, '77 th Floor,F lo o r, TechniplexT ec h n iplex 2,2, Techniplex Complex, Veer Savarkar Marg, LOGISTICS Goregaon (West), Mumbai —– 400 062 Tel: + 91 22 28715500 Our Ref: MLLSEC/MLLSEC/107/2021107/2021 Toll Free: 1800 258 6787 www.mahindralogistics.com 18 June 20220211 Regd Office Mahindra Towers, P. K. Kurne Chowk, Worli, To, Mumbai —– 400 018 BSE Limited, (Security Code: 540768) C1N:CIN: L63000MH2007PLC173466 Phiroze Jeejeebhoy Towers, Dalal Street, Fort, E-mailE-mail Id: cs.mll(&,[email protected] MumbaiMumbai— – 400 001.001. National Stock Exchange of India Ltd., (Symbol: MAHLOG) Exchange Plaza, 55thth Floor, Plot No. C/1, “G”"G" Block, Bandra -Kurla-Kurla Complex, Bandra (East), Mumbai —– 400 051051.. Dear Sirs, Sub: ExExtracttract of Newspaper publication —– SecuritiesSecurities and EExchangexchange BBoardoard of IIndiandia (Listing(Listing Obligations aandnd Disclosure RequirementsRequirements)) RegulationsRegulations,, 2015 (“("ListingListing RegulationsRegulations")”) In furtherance to our letter dated 17 June 20220211 and iinn compliance with Regulation 47 and other applicable provisions of the Listing RegulationsRegulations,, please find enclosed the extract of the public notice published today, viz.viz. FriFriday,day, 18 June 20220211 in the Business Standard (in English language) and Sakal (in Marathi language) inin print and electronic versions. This intimation is also being upuploadedloaded on website of the Company: www.mahindralogistics.com. Kindly take the above on record and acknowledge receipt of the samesame.. Thanking you, Yours faithfully, For Mahindra Logistics Limited Brijbala Batwal Company Secretary EnclEnclosures:osures: As above Business Standard MUMBAIMUMBAI I| FRIDAY, 1818 JUNE 2021 COMPANIES 3 . < Mahindra LOGISTICS MAHINDRA LOGISTICS LIMITED Jet shareholders reject Registered Office: Mahindra Towers, P. -

AGM NOTICE 2019.Pdf

Go Airlines (India) Limited Go Airlines (India) Limited Regd. Office: C/o Britannia Industries Limited, A-33 Lawrence Road Industrial Area, New Delhi-110035 Corporate Office: C-1, Wadia International Centre (WIC), Pandurang Budhkar Marg, Worli, Mumbai-400025 CIN: U63013DL2004PLC217305 Phone: +91 22 6741000; Fax: +91 22 67410001, Website: www.GoAir.in NOTICE Notice is hereby given that the 15th Annual General Meeting of the Members of Go Airlines (India) Limited will be held at 56, Jor Bagh, New Delhi-110001 on Monday, 30th September 2019 at 12 Noon to transact the following business: ORDINARY BUSINESS 1. To receive, consider and adopt the Standalone and Consolidated Audited Financial Statements of the Company for the Financial Year ended 31st March 2019, together with the report of Board of Directors and Auditors thereon; 2. To appoint a Director in place of Mr. Nusli N. Wadia (DIN: 00015731), who retires by rotation in terms of section 152(6) of the Companies Act, 2013 and being eligible, offers himself for re-appointment; 3. To approve appointment of M/s. Walker Chandiok & Co LLP, Chartered Accountants, as the Statutory Auditors of the Company To consider and if thought fit, to pass the following resolution as an “Ordinary Resolution”: “RESOLVED THAT pursuant to the provisions of Section 139(1) and all other applicable provisions of the Companies Act, 2013 read with the Companies (Audit and Auditors) Rules, 2014, (each including any statutory modification(s) or re-enactment(s) thereof), for the time being in force to the extent applicable, consent and approval of the members of the Company be and are hereby accorded for appointment of M/s. -

Press Release the Bombay Burmah Trading Corporation

Press Release The Bombay Burmah Trading Corporation Limited April 3, 2020 Ratings Facilities Amount Rating1 Rating Action (Rs. crore) Long term Bank Facilities 7.11 CARE AA; Stable Reaffirmed (Double A; Outlook: Stable) Long term Bank Facilities 49.00 CARE AA; Stable Reaffirmed (enhanced from 29.00) (Double A; Outlook: Stable) Short-term Bank Facilities 1.00 CARE A1+ Reaffirmed (A One Plus) Total 57.11 (Rs. Fifty Seven Crore and Eleven Lakhs only) Details of instruments/facilities in Annexure-1 Detailed Rationale & Key Rating Drivers The reaffirmation of ratings assigned to the bank facilities of The Bombay Burmah Trading Corporation Limited (BBTCL) continues to derive strength from it being one of the holding company of Wadia Group. BBTCL has equity investments in group companies like Britannia Industries Limited (BIL) and The Bombay Dyeing & Manufacturing Company Limited (BMCL) that have significant market value. The rating also factors in the reputed and well-established promoter group, its presence in diversified businesses, expected monetization of real estate assets towards reduction of debt and issuance of NCDs to refinance its existing term loan facilities. However, these rating strengths continue to be partially offset by moderation in operational performance resulting in moderate financial risk profile in FY19 (refers to period April 01, to March 31,) and 9MFY20 (April 01 to December 31). Any large debt fund capital expenditure impacting financial risk profile of the company, dilution of stake in BIL, ability to recover the inter-corporate deposits (ICDs) from its group companies in a timely manner and delay in monetization of real estate assets would be key rating sensitivities. -

5 to Be Signed by

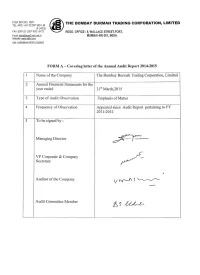

POST BOX NO. 10077 THE BOMBAY BURMAH TRADING CORPORATION , LIMITED TEL. NOS.: +91 22 2207 9351- 54 (4 LINES) FAX :0091-22- 2207 1612 / 6772 REGD. OFFICE: 9, WALLACE STREET,FORT, Email: bbtcl(@bom2. vsn1.net.in MUMBAI 400 001 , INDIA. Website : www.bbtcl com CIN: L99999MH1863PL0000002 FORM A - Covering letter of the Annual Audit Report 2014-2015 1 Name of the Company The Bombay Burmali Trading Corporation, Limited 2 Annual Financial Statements for the year ended 31St March,2015 3 Type of Audit Observation Emphasis of Matter 4 Frequency of Observation Appeared since Audit Report pertaining to FY 2011-2012 5 To be signed by : Managing Director V P Corporate & Company Secretary Auditor of the Company Audit Committee Member 1) The Bombay Burmah Trading Corporation, Ltd A Wadia Enterprise 2015 th 014 - ort 2 150 Rep al nu An rust n of T A Traditio Contents Location of Corporation’s Estates and Factories 2 Notice of Annual General Meeting 3-15 Directors’ Report 16-55 Management Discussion and Analysis 56-60 Auditors’ Report on Standalone Financial Statements 61-65 Financial Statements - Standalone 66-69 Notes forming part of Standalone Financial Statements 70-109 Auditors’ Report on Consolidated Financial Statements 110-111 Consolidated Financial Statements 112-115 Notes forming part of the Consolidated Financial Statements 116-157 Statement under section 129 (3) of the Companies Act, 2013 158-161 10 Years’ Financial Review 162 Proxy Form 163-164 150th Annual General Meeting Wednesday, 5th August 2015, 3.45 pm; Y B Chavan Auditorium, Gen Jagannath Bhosale Marg, Nariman Point, Mumbai – 400 021. -

Interglobe Aviation

Initiating Coverage | 10 December 2015 Sector: Aviation InterGlobe Aviation Aiming for higher altitudes Harshad Borawake ([email protected]); +91 22 3982 5432 Rajat Agarwal ([email protected]); +91 22 3982 5558 InterGlobe Aviation InterGlobe Aviation: Aiming for higher altitudes Aiming for higher altitudes ............................................................................................. 3 Story in charts ................................................................................................................ 5 Indian aviation market set to become 3rd largest ........................................................... 7 Indigo to remain market leader by a distance ............................................................... 16 Profitability way ahead of peers ................................................................................... 23 Some key things to know ............................................................................................. 23 Initiate coverage with a Buy; TP at INR1,478 ................................................................ 35 Key risks ...................................................................................................................... 40 Company background .................................................................................................. 41 Annexures ................................................................................................................... 44 Financials and valuations ............................................................................................ -

Nicholas & Tomasevicllp

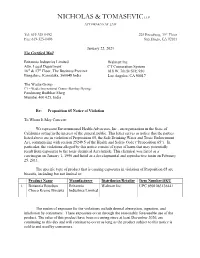

NICHOLAS & TOMASEVIC LLP ATTORNEYS AT LAW Tel: 619-325-0492 225 Broadway, 19th Floor Fax: 619-325-0496 San Diego, CA 92101 January 22, 2021 Via Certified Mail Britannia Industries Limited Walmart Inc. Attn. Legal Department CT Corporation System 16th & 17th Floor, The Business Precinct 818 W. 7th St STE 930 Bangalore, Karnataka, 560048 India Los Angeles, CA 90017 The Wadia Group C1 – Wadia International Centre (Bombay Dyeing) Pandurang Budhkar Marg Mumbai 400 025, India Re: Proposition 65 Notice of Violation To Whom It May Concern: We represent Environmental Health Advocates, Inc., an organization in the State of California acting in the interest of the general public. This letter serves as notice that the parties listed above are in violation of Proposition 65, the Safe Drinking Water and Toxic Enforcement Act, commencing with section 25249.5 of the Health and Safety Code (“Proposition 65”). In particular, the violations alleged by this notice consist of types of harm that may potentially result from exposures to the toxic chemical Acrylamide. This chemical was listed as a carcinogen on January 1, 1990 and listed as a developmental and reproductive toxin on February 25, 2011. The specific type of product that is causing exposures in violation of Proposition 65 are biscuits, including but not limited to: Product Name Manufacturer Distributor/Retailer Item Number/SKU 1. Britannia Bourbon Britannia Walmart Inc. UPC 8901063136441 Choco Kreme Biscuits Industries Limited The routes of exposure for the violations include dermal absorption, ingestion, and inhalation by consumers. These exposures occur through the reasonably foreseeable use of the product. The sales of this product have been occurring since at least December 2020, are continuing to this day and will continue to occur as long as the product subject to this notice is sold to and used by consumers. -

CENTRAL INFORMATION COMMISSION (Under Sec 19 of the Right to Information Act 2005) B Block, August Kranti Bhawan, New Delhi 1100065

Appeal No.CIC/OK/A/2007/001392 CENTRAL INFORMATION COMMISSION (Under Sec 19 of the Right to Information Act 2005) B Block, August Kranti Bhawan, New Delhi 1100065 Name of the Appellant - Shri Nusli Wadia, Mumbai Name of the Public Authority - Ministry of External Affairs (MEA) Respondent South Block, New Delhi-110011 Date of Hearing 21.12.2007 Date of Decision 16.01.2008 Facts: 1. By an application of 6-6-’07 submitted on 12-6-07 Shri Nusli Wadia of Mumbai sought the following information from the CPIO, MEA (i) “documents, notes of meeting and file notes relating to or arising out of the letter dated July 06, 2001 sent by Mrs. Dina Wadia to the Hon’ble Prime Minister of India including notes of or documents relating to the discussion between the Hon’ble Prime Minister of India and the Hon’ble External Affairs Minister referred to in the letter no. 757/PSBPM/2001 dated July 13, 2001; (ii) copies of all documents, notes of meetings, file notings, including inter-ministerial notes, advice sought or given including all approvals, proposals, recommendations from the concerned ministers/ICCR including those to and from the Hon’ble Prime Minister; (iii) minutes of meetings with the Hon’ble Prime Minister and any other Ministers/Officials on the matter; and (iv) Opinions given by any authority or person, including legal advice.” 2. To this he received a response on 12-7-07 that the information from CPIO Shri A.K. Nag, JS, (Welfare & Information) was being collected and sought more 1 time. -

Common Spoken Tamil Made Easy

COMMON SPOKEN TAMIL MADE EASY Third Edition by T. V. ADIKESAVALU Digital Version CHRISTIAN MEDICAL COLLEGE VELLORE Adi’s Book. COMMON SPOKEN TAMIL MADE EASY Third Edition by T. V. ADIKESAVALU Digital Version 2007 This book was prepared for the staff and students of Christian Medical College Vellore, for use in the Tamil Study Programme. No part may be reproduced without permission of the General Superintendent. 2 Adi’s Book. CONTENTS FOREWORD. 6 PREFACE TO SECOND EDITION. 7 THIRD EDITION: UPDATE. 8 I. NOTES FOR PRONUNCIATION & KEY FOR ABBREVIATIONS. 9 II. GRAMMAR LESSONS: Lesson No. Page. 1. Greetings and Forms of Address. 10 2. Pronouns, Interrogative and Demonstrative. 12 3. Pronouns, Personal. 15 4. The Verb ‘to be’, implied. 17 5. Cardinal Numbers 1 to 10, and Verbs - introduction. 19 6. Verbs - Positive Imperatives. 21 7. Verbs - Negative Imperatives, Weak & Strong Verbs, & Medials. 23 8. Nouns - forming the plural. 28 9. Nouns and Personal Pronouns - Accusative (Object) case. 30 10. Nouns and Personal Pronouns - Genitive (Possessive) Case. 34 11. Review, (Revision) No.I. 38 12. Verbs - Infinitives. 40 13. Nouns and Personal Pronouns, Dative Case, ‘to’ or ‘for’ & Verbs - Defective. 43 14. Verbs - defective (continued). 47 15. Cardinal Numbers 11 to 1000 & Time. 50 16. Verbs - Present tense, Positive. 54 17. Adjectives and Adverbs. 58 18. Post-Positions. 61 19. Nouns - Locative Case, 'at' or 'in'. 64 20. Post positions, (Continued). 67 21. Verbs - Future Tense, Positive, and Ordinal Numbers. 70 3 Adi’s Book. 22. Verbs - Present and Past, Negative, Page. and Potential Form to express 'may' 75 23. -

A Historical Overview of the Parsi Settlement in Navsari 62 9

Samuel Jordan Center for Persian Studies and Culture www.dabirjournal.org Digital Archive of Brief notes & Iran Review ISSN: 2470-4040 Vol.01 No.04.2017 1 xšnaoθrahe ahurahe mazdå Detail from above the entrance of Tehran’s fire temple, 1286š/1917–18. Photo by © Shervin Farridnejad The Digital Archive of Brief Notes & Iran Review (DABIR) ISSN: 2470-4040 www.dabirjournal.org Samuel Jordan Center for Persian Studies and Culture University of California, Irvine 1st Floor Humanities Gateway Irvine, CA 92697-3370 Editor-in-Chief Touraj Daryaee (University of California, Irvine) Editors Parsa Daneshmand (Oxford University) Arash Zeini (Freie Universität Berlin) Shervin Farridnejad (Freie Universität Berlin) Judith A. Lerner (ISAW NYU) Book Review Editor Shervin Farridnejad (Freie Universität Berlin) Advisory Board Samra Azarnouche (École pratique des hautes études); Dominic P. Brookshaw (Oxford University); Matthew Canepa (University of Minnesota); Ashk Dahlén (Uppsala University); Peyvand Firouzeh (Cambridge University); Leonardo Gregoratti (Durham University); Frantz Grenet (Collège de France); Wouter F.M. Henkelman (École Pratique des Hautes Études); Rasoul Jafarian (Tehran University); Nasir al-Ka‘abi (University of Kufa); Andromache Karanika (UC Irvine); Agnes Korn (Goethe Universität Frankfurt am Main); Lloyd Llewellyn-Jones (University of Edinburgh); Jason Mokhtarain (University of Indiana); Ali Mousavi (UC Irvine); Mahmoud Omidsalar (CSU Los Angeles); Antonio Panaino (Univer- sity of Bologna); Alka Patel (UC Irvine); Richard Payne (University of Chicago); Khodadad Rezakhani (Princeton University); Vesta Sarkhosh Curtis (British Museum); M. Rahim Shayegan (UCLA); Rolf Strootman (Utrecht University); Giusto Traina (University of Paris-Sorbonne); Mohsen Zakeri (Univer- sity of Göttingen) Logo design by Charles Li Layout and typesetting by Kourosh Beighpour Contents Articles & Notes 1. -

Assets Management Efficiency of Indian Textile Companies - a Comparative Analysis

IJRIM Volume 6, Issue 4 (April, 2016) (ISSN 2231-4334) International Journal of Research in IT & Management (IMPACT FACTOR – 5.96) Assets Management Efficiency of Indian Textile companies - A Comparative Analysis Dr. B. MADHUSUDHAN REDDY Professor in Finance Department of Management Studies, Guru Nanak Institute of Technology, Hyderabad, India ABSTRACT The Textile Sector in India ranks next to Agriculture. Textile is one of India’s oldest industries and has a formidable presence in the national economy. The textile industry occupies a unique place in our country. One of the earliest to come into existence in India, it accounts for 14% of the total Industrial production, contributes to nearly 27% of the total exports and is the second largest employment generator after agriculture. Like other organizations, all textile companies keep various assets such as inventory, debtors, fixed assets, investments etc. to carry out the business operations effectively and efficiently. However, managing these assets effectively is a crucial thing. Asset Management Ratios attempt to measure the firm's success in managing its assets to generate sales. These ratios can provide insight into the success of the firm's credit policy and inventory management. These ratios are also known as Activity or Turnover Ratios. This paper represents an empirical study which examines the assets management in textile companies in India with a data of 5 years. For the purpose of the study secondary data is used. For the purpose of analysis ratios and arithmetic mean have been used and to test hypothesis, ANOVA test (F test) has been applied. Key words: Assets management, Inventory turnover ratio, Debtors turnover ratio, Fixed assets turnover ratio, Total assets turnover ratio and ANOVA test. -

Britannia Industries Limited

BRITANNIA INDUSTRIES LIMITED (Corporate Identity Number: L15412WB1918PLC002964) Registered Office: 5/1A, Hungerford Street, Kolkata - 700 017 Phone : 033 22872439/2057; 080 39400080 Fax : 033 22872501; 080 25063229 Website: www.britannia.co.in E-mail ID: [email protected] NOTICE Notice is hereby given that the Ninety-sixth Annual General NOTES: Meeting (AGM) of the Members of Britannia Industries a. A MEMBER ENTITLED TO ATTEND AND VOTE Limited will be held on Tuesday, 4 August 2015, at 11 a.m. AT THE MEETING IS ENTITLED TO APPOINT A at the Hyatt Regency, JA-1, Sector 3, Salt Lake City, Kolkata - 700 098 to transact the following business: PROXY/ PROXIES TO ATTEND AND VOTE INSTEAD OF HIMSELF/HERSELF. SUCH A PROXY/ PROXIES ORDINARY BUSINESS: NEED NOT BE A MEMBER OF THE COMPANY. 1. To receive, consider and adopt the Audited Statement of Profit and Loss for the Financial Year ended 31 March A person can act as proxy on behalf of Members not 2015 and the Balance Sheet as on that date and the exceeding fifty (50) and holding in the aggregate not Reports of the Directors and the Auditors thereon. more than ten percent of the total Share Capital of the 2. To declare dividend for the Financial Year ended Company. In case a proxy is proposed to be appointed 31 March 2015. by a Member holding more than 10% of the total Share Capital of the Company carrying voting rights, 3. To appoint a Director in place of Mr. Ness N Wadia (holding DIN: 00036049), who retires by rotation in then such proxy shall not act as a proxy for any other terms of Section 152(6) of the Companies Act, 2013 and person or Member.