SEC Adopts New Short Sale Rules

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

North American Company Profiles 8X8

North American Company Profiles 8x8 8X8 8x8, Inc. 2445 Mission College Boulevard Santa Clara, California 95054 Telephone: (408) 727-1885 Fax: (408) 980-0432 Web Site: www.8x8.com Email: [email protected] Fabless IC Supplier Regional Headquarters/Representative Locations Europe: 8x8, Inc. • Bucks, England U.K. Telephone: (44) (1628) 402800 • Fax: (44) (1628) 402829 Financial History ($M), Fiscal Year Ends March 31 1992 1993 1994 1995 1996 1997 1998 Sales 36 31 34 20 29 19 50 Net Income 5 (1) (0.3) (6) (3) (14) 4 R&D Expenditures 7 7 7 8 8 11 12 Capital Expenditures — — — — 1 1 1 Employees 114 100 105 110 81 100 100 Ownership: Publicly held. NASDAQ: EGHT. Company Overview and Strategy 8x8, Inc. is a worldwide leader in the development, manufacture and deployment of an advanced Visual Information Architecture (VIA) encompassing A/V compression/decompression silicon, software, subsystems, and consumer appliances for video telephony, videoconferencing, and video multimedia applications. 8x8, Inc. was founded in 1987. The “8x8” refers to the company’s core technology, which is based upon Discrete Cosine Transform (DCT) image compression and decompression. In DCT, 8-pixel by 8-pixel blocks of image data form the fundamental processing unit. 2-1 8x8 North American Company Profiles Management Paul Voois Chairman and Chief Executive Officer Keith Barraclough President and Chief Operating Officer Bryan Martin Vice President, Engineering and Chief Technical Officer Sandra Abbott Vice President, Finance and Chief Financial Officer Chris McNiffe Vice President, Marketing and Sales Chris Peters Vice President, Sales Michael Noonen Vice President, Business Development Samuel Wang Vice President, Process Technology David Harper Vice President, European Operations Brett Byers Vice President, General Counsel and Investor Relations Products and Processes 8x8 has developed a Video Information Architecture (VIA) incorporating programmable integrated circuits (ICs) and compression/decompression algorithms (codecs) for audio/video communications. -

LIST of SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 Ivmool

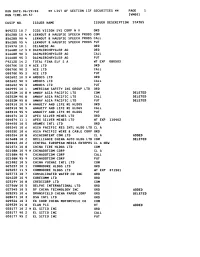

RUN DATE:06/29/00 ** LIST OF SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 IVMOOl CUSIP NO. ISSUER NAME ISSUER DESCRIPTION STATUS B49233 10 7 ICOS VISION SYS CORP N V ORD B5628B 10 4 * LERNOUT & HAUSPIE SPEECH PRODS COM B5628B 90 4 LERNOUT & HAUSPIE SPEECH PRODS CALL B5628B 95 4 LERNOUT 8 HAUSPIE SPEECH PRODS PUT D1497A 10 1 CELANESE AG ORD D1668R 12 3 * DAIMLERCHRYSLER AG ORD D1668R 90 3 DAIMLERCHRYSLER AG CALL D1668R 95 3 DAIMLERCHRYSLER AG PUT F9212D 14 2 TOTAL FINA ELF S A WT EXP 080503 G0070K 10 3 * ACE LTD ORD G0070K 90 3 ACE LTD CALL G0070K 95 3 ACE LTD PUT GO2602 10 3 * AMDOCS LTD ORD GO2602 90 3 AMDOCS LTD CALL GO2602 95 3 AMDOCS LTD PUT GO2995 10 1 AMERICAN SAFETY INS GROUP LTD ORD G0352M 10 8 * AMWAY ASIA PACIFIC LTD COM DELETED G0352M 90 8 AMWAY ASIA PACIFIC LTD CALL DELETED G0352M 95 8 AMWAY ASIA PACIFIC LTD PUT DELETED GO3910 10 9 * ANNUITY AND LIFE RE HLDGS ORD GO3910 90 9 ANNUITY AND LIFE RE HLDGS CALL GO3910 95 9 ANNUITY AND LIFE RE HLDGS PUT GO4074 10 3 APEX SILVER MINES LTD ORD GO4074 11 1 APEX SILVER MINES LTD WT EXP 110402 GO4450 10 5 ARAMEX INTL LTD ORD GO5345 10 6 ASIA PACIFIC RES INTL HLDG LTD CL A G0535E 10 6 ASIA PACIFIC WIRE & CABLE CORP ORD GO5354 10 8 ASIACONTENT COM LTD CL A ADDED G1368B 10 2 BRILLIANCE CHINA AUTO HLDG LTD COM DELETED 620045 20 2 CENTRAL EUROPEAN MEDIA ENTRPRS CL A NEW G2107X 10 8 CHINA TIRE HLDGS LTD COM G2108N 10 9 * CHINADOTCOM CORP CL A G2108N 90 9 CHINADOTCOM CORP CALL G2lO8N 95 9 CHINADOTCOM CORP PUT 621082 10 5 CHINA YUCHAI INTL LTD COM 623257 10 1 COMMODORE HLDGS LTD ORD 623257 11 -

1 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: September 30, 2000 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries Institutional Investment Manager Filing this Report: Name: AMERICAN INTERNATIONAL GROUP, INC. Address: 70 Pine Street New York, New York 10270 Form 13F File Number: 28-219 The Institutional Investment Manager filing this report and the person by whom it is signed represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Edward E. Matthews Title: Vice Chairman -- Investments and Financial Services Phone: (212) 770-7000 Signature, Place, and Date of Signing: /s/ Edward E. Matthews New York, New York November 14, 2000 - ------------------------------- ------------------------ ----------------- (Signature) (City, State) (Date) Report Type (Check only one.): [X] 13F HOLDINGS REPORT. (Check if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check if no holdings reported are in this report, and all holdings are reported in this report and a portion are reported by other reporting manager(s).) [ ] 13F COMBINATION REPORT. (Check -

U.S. Technology, Media & Telecom Industry

Technology, Media & Telecom Industry Update May 2012 Member FINRA/SIPC www.harriswilliams.com Table of Contents Technology, Media & Telecom What We've Been Reading…………………………………………………………………………………………1 Bellwethers……………………………………………………………………………………………2 TMT Public Market Trading Statistics………………………………………………………………………..…………………..3 Recent TMT M&A Activity…………………………………………………………………………………………….4 Recent U.S. TMT Initial Public Offerings………………………………………………………………………….………………...………..5 Public and M&A Market Overview by Sector Data and Information Services………………………………………………………………..…………..6 Financial Technology…………………………………………………………………………8 Internet & Digital Media……………………………………………………..…………………..10 IT and Tech-Enabled Services………………………………………………………………..13 Software – Application…………………………………………………….…………………..15 Software – Infrastructure……………………………………………………..…………………..18 Software – SaaS……………………………………………………………………………………………………..20 Tech Hardware……………………………………………………………………..…………………..22 Telecom………………………………………………………………………………………………..25 Selected HW&Co. TMT Transactions…………………………………………………………………………………………..28 TMT Group Overview and Disclosures…………………………………………………………………………………………..29 Note: All market data in the following materials is as of April 30, 2012. What We’ve Been Reading How The Bush Tax Cuts Could Lead To A Crazy Year For M&A Business Insider 4/30/2012 An increased amount of M&A activity is expected in the remainder of 2012 as potential changes in the capital gains tax policies are motivating firms to exit investments before the end of the year when the Bush Tax Cuts expire. -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 0XF8 Limited 10737 1MORE INC

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 0XF8 Limited 10737 1MORE INC. 12048 360fly, Inc. 11161 3C TEK CORP. 9397 3D Imaging & Simulations Corp. (3DISC) 11190 3D Systems Corporation 10632 3DRUDDER 11770 3eYamaichi Electronics Co., Ltd. 8709 3M Cogent, Inc. 7717 3M Scott 8463 3T B.V. 11721 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 89 North, Inc. 12070 Shenzhen 8Bitdo Tech Co., Ltd. 11720 90meter Solutions, Inc. 12086 A‐FOUR TECH CO., LTD. 2522 A‐One Co., Ltd. 10116 A‐Tec Subsystem, Inc. 2164 A‐VEKT K.K. 11459 A. Eberle GmbH & Co. KG 6910 a.tron3d GmbH 9965 A&T Corporation 11849 Aaronia AG 12146 abatec group AG 10371 ABB India Limited 11250 ABILITY ENTERPRISE CO., LTD. 5145 Abionic SA 12412 AbleNet Inc. 8262 Ableton AG 10626 ABOV Semiconductor Co., Ltd. 6697 Absolute USA 10972 AcBel Polytech Inc. 12335 Access Network Technology Limited 10568 ACCUCOMM, INC. 10219 Accumetrics Associates, Inc. 10392 Accusys, Inc. 5055 Ace Karaoke Corp. 8799 ACELLA 8758 Acer, Inc. 1282 Aces Electronics Co., Ltd. 7347 Aclima Inc. 10273 ACON, Advanced‐Connectek, Inc. 1314 Acoustic Arc Technology Holding Limited 12353 ACR Braendli & Voegeli AG 11152 Acromag Inc. 9855 Acroname Inc. 9471 Action Industries (M) SDN BHD 11715 Action Star Technology Co., Ltd. 2101 Actions Microelectronics Co., Ltd. 7649 Actions Semiconductor Co., Ltd. 4310 Active Mind Technology 10505 Qorvo, Inc 11744 Activision 5168 Acute Technology Inc. 10876 Adam Tech 5437 Adapt‐IP Company 10990 Adaptertek Technology Co., Ltd. 11329 ADATA Technology Co., Ltd. -

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par

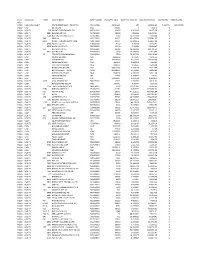

Fund Asset Class Ticker Security Name CUSIP Number Shares/Par Value Base Price Amount Base Market Value Interest Rate Maturity Date NQ11 ' NQ20 CASH EQUIVALENT STATE STREET BANK + TRUST CO '8611239B5 459562.42 100 459562.42 0.155781 12/31/2030 NQ20 CASH US DOLLAR 'USD -3168.1 1 -3168.1 0 NQ2A EQUITY 316 ORIENT OVERSEAS INTL LTD '665911905 10000 4.847328 48473.28 0 NQ2A EQUITY 9997 BELLUNA CO LTD '607035904 19000 7.883193 149780.67 0 NQ2A EQUITY 7518 NET ONE SYSTEMS CO LTD '603654906 3600 13.247274 47690.19 0 NQ2A EQUITY EAD EADS NV '401225909 63129 35.457258 2238381.23 0 NQ2A EQUITY IFS B_ INDUST + FINANCIAL SYSTEM B '508170909 10371 15.682951 162647.88 0 NQ2A EQUITY 6406 FUJITEC CO LTD '635682008 4000 6.35418 25416.72 0 NQ2A EQUITY 8056 NIHON UNISYS LTD '664268000 35100 7.30668 256464.47 0 NQ2A EQUITY BLT BHP BILLITON PLC '005665906 32542 28.326213 921791.61 0 NQ2A EQUITY 7631 MACNICA INC '620789909 1100 22.358692 24594.56 0 NQ2A EQUITY TD TORONTO DOMINION BANK '891160954 7500 78.159792 586198.44 0 NQ2A CASH POUND STERLING 'GBP 28911.69 1.56845 45346.55 0 NQ2A CASH JAPANESE YEN 'JPY 35926970 0.012533 450269.08 0 NQ2A CASH CANADIAN DOLLAR 'CAD 5601.52 0.980921 5494.65 0 NQ2A CASH AUSTRALIAN DOLLAR 'AUD 73410.53 1.02505 75249.48 0 NQ2A CASH HONG KONG DOLLAR 'HKD 308101.62 0.128918 39719.94 0 NQ2A CASH MEXICAN PESO (NEW) 'MXN 803148.56 0.074483 59820.84 0 NQ2A CASH NORWEGIAN KRONE 'NOK 240817.9 0.168224 40511.38 0 NQ2A CASH SWEDISH KRONA 'SEK 725.52 0.144877 105.11 0 NQ2A CASH SWISS FRANC 'CHF 122129.07 1.056524 129032.3 0 NQ2A EQUITY AGFB AGFA GEVAERT NV '568905905 29401 1.637075 48131.63 0 NQ2A CASH NEW ZEALAND DOLLAR 'NZD 7307.71 0.80375 5873.57 0 NQ2A EQUITY 7729 TOKYO SEIMITSU CO LTD '689430007 3500 17.646322 61762.13 0 NQ2A EQUITY HSBA HSBC HOLDINGS PLC '054052907 131069 8.800575 1153482.52 0 NQ2A EQUITY RIO RIO TINTO PLC '071887004 39671 47.351515 1878481.94 0 NQ2A EQUITY BP. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 13F Form 13F COVER PAGE Report for the Calendar Year or Quarter Ended: December 31, 2002 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries. Institutional Investment Manager Filing this Report: Name: Putnam Investment Management, LLC Address: One Post Office Square Boston, MA 02109 Form 13F File Number: 28 - 90 The institutional investment manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete , and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Andrew J. Hachey Title: Vice President Phone: (617) 760-8235 Signature, Place and Date of Signing: /s/ Andrew J. Hachey Boston, MA__________________ _2/15/2003 [Signature] [City, State] [Date] Report Type (Check only one.): [ X ] 13F HOLDINGS REPORT. (Check here if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check here if no holdings reported are in this report, and all holdings are reported by other reporting manager (s).) [ ] 13F COMBINATION REPORT. (Check here if a portion of the holdings for this reporting manager are reported in this report and a portion are reported by other reporting manager (s).) FORM 13F SUMMARY PAGE Report Summary: Number of Other Included Managers: 3 Form 13F Information Table Entry Total: 4,012 Form 13F Information Table Value Total: $ 124,441,614 (thousands) List of Other Included Managers: Provide a numbered list of the name(s) and Form 13F file number(s) of all institutional investment managers with respect to which this report is filed, other than the manager filing this report. -

![[X] Annual Report Pursuant to Section 15(D) of the Securities Exchange Act of 1934 for the Fiscal Year Ended December 31, 2002](https://docslib.b-cdn.net/cover/7326/x-annual-report-pursuant-to-section-15-d-of-the-securities-exchange-act-of-1934-for-the-fiscal-year-ended-december-31-2002-4827326.webp)

[X] Annual Report Pursuant to Section 15(D) of the Securities Exchange Act of 1934 for the Fiscal Year Ended December 31, 2002

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Form 11-K [X] Annual Report Pursuant To Section 15(d) Of The Securities Exchange Act of 1934 For the fiscal year ended December 31, 2002 OR [ ] Transition Report Pursuant To Section 15(d) Of The Securities Exchange Act of 1934 For the transition period from ________ to _________ Commission File # 0-16093 (A) Full title of the plan and the address of the plan, if different from that of the issuer named below: CONMED CORPORATION Retirement Savings Plan (B) Name of issuer of the securities held pursuant to the plan and the address of its principal executive office: CONMED CORPORATION 525 French Road Utica, New York 13502 SIGNATURES THE PLAN. Pursuant to the requirements of the Securities Exchange Act of 1934, the Plan Administrator has duly caused this Annual Report to be signed by the undersigned hereunto duly authorized. CONMED CORPORATION Retirement Savings Plan By: /s/ Robert D. Shallish, Jr. ------------------------ Robert D. Shallish, Jr. Vice President - Finance CONMED Corporation Date: June 25, 2003 CONMED Corporation Retirement Savings Plan Index Page Report of Independent Auditors ......................................... 1 Financial Statements: Statements of Net Assets Available for Benefits at December 31, 2002 and 2001 ............................ 2 Statements of Changes in Net Assets Available for Benefits for the Year Ended December 31, 2002 and 2001 ............ 3 Notes to Financial Statements ....................................... 4-8 Supplemental Schedule: * Schedule of Assets Held for Investment Purposes (Schedule H, Part IV, Item (i))at December 31, 2002 ............... 9-23 Consent of Independent Auditors........................................ 24 Certification........................................................... 25 * Other schedules required by Section 2520.103-10 of the Department of Labor Rules and Regulations for Reporting and Disclosure under ERISA have been omitted because they are not applicable. -

SOES Order Sizes

NASD Notice to Members 99-80 block volume of less than 1,000 ACTION REQUIRED Executive Summary Effective October 1, 1999, the maxi- shares a day, a bid price of less than or equal to $250, and two mum Small Order Execution Sys- or more Market Makers. temSM (SOESSM) order sizes for 420 SOES Order Nasdaq National Market® (NNM) Sizes securities will be revised in accor- In accordance with Rule 4710, Nas- dance with National Association of daq periodically reviews the maxi- ® Maximum SOES Order Securities Dealers, Inc. (NASD ) mum SOES order size applicable to Rule 4710(g). each NNM security to determine if Sizes Set To Change the trading characteristics of the For more information, please con- issue have changed so as to war- October 1, 1999 ® tact Nasdaq Market Operations at rant an adjustment. Such a review (203) 378-0284. was conducted using data as of June 30, 1999, pursuant to the SUGGESTED ROUTING aforementioned standards. The Description maximum SOES order-size The Suggested Routing function is meant to changes called for by this review aid the reader of this document. Each NASD Under Rule 4710, the maximum are being implemented with three member firm should consider the appropriate SOES order size for an NNM secu- exceptions. distribution in the context of its own rity is 1,000, 500, or 200 shares, organizational structure. depending on the trading character- • First, issues were not permitted • Legal & Compliance istics of the security. The Nasdaq to move more than one size Workstation II® (NWII) indicates the level. For example, if an issue • Op e r a t i o n s maximum SOES order size for each was previously categorized in • Sy s t e m s NNM security. -

List of Section 13F Securities, First Quarter

List of Section 13F Securities First Quarter FY 2013 Copyright (c) 2013 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2013, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2013. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by [ Section 13(f)(1) and Rule 13f-1] thereunder. -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 01Db-Stell 3151 0XF8 Limited 10737 103M

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 01dB-Stell 3151 0XF8 Limited 10737 103mm Tech 8168 1064138 Ontario Ltd. O/A UNI-TEC ELECTRONICS 8219 11 WAVE TECHNOLOGY, INC. 4375 1417188 Ontario Ltd. 4835 1C Company 5288 1MORE INC. 12048 2D Debus & Diebold Messsysteme GmbH 8539 2L international B.V. 4048 2N TELEKOMUNIKACE a.s. 7303 2-Tel B.V. 2110 2WCOM GmbH 7343 2Wire, Inc 2248 360 Electrical, LLC 12686 360 Service Agency GmbH 12930 360fly, Inc. 11161 3Brain GmbH 9818 3C TEK CORP. 9397 3Cam Technology, Inc 1928 3Com Corporation 1286 3D CONNEXION SAM 9583 3D Imaging & Simulations Corp. (3DISC) 11190 3D INNOVATIONS, LLC 7907 3D Robotics Inc. 9900 3D Systems Corporation 10632 3D Technologies Ltd 12655 3DM Devices Inc 2982 3DRUDDER 11770 3DSP 7513 3DV Systems Ltd. 6963 3eYamaichi Electronics Co., Ltd. 8709 3i Corporation 9806 3i techs Development Corp 4263 3layer Engineering 7123 3M Canada 2200 3M CMD (Communication Markets Division) 7723 3M Cogent, Inc. 7717 3M Germany 2597 3M Home Health Systems 2166 3M Library Systems 3372 3M Scott 8463 3M Touch Systems 1430 3Pea Technologies, Inc. 3637 3Shape A/S 6303 3T B.V. 11721 4G Systems GmbH 6485 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 8086 Consultancy 12657 89 North, Inc. 12070 8D TECHNOLOGIES INC. 8845 8devices 9599 90meter Solutions, Inc. 12086 A & G Souzioni Digitali 4757 A & R Cambridge Ltd. 9668 A C S Co., Ltd. 9454 A Global Partner Corporation 3689 A W Electronics, Inc. -

Number of H-1B Petitions Approved by Uscis in Fy 2008 for Initial Beneficiaries Source: Dhs

NUMBER OF H-1B PETITIONS APPROVED BY USCIS IN FY 2008 FOR INITIAL BENEFICIARIES SOURCE: DHS EMPLOYER INITIAL BENEFICIARIES INFOSYS TECHNOLOGIES LIMITED 4,559 WIPRO LIMITED 2,678 SATYAM COMPUTER SERVICES LIMITED 1,917 TATA CONSULTANCY SERVICES LIMITED 1,539 MICROSOFT CORP 1,037 ACCENTURE LLP 731 COGNIZANT TECH SOLUTIONS US CORP 467 CISCO SYSTEMS INC 422 LARSEN & TOUBRO INFOTECH LIMITED 403 IBM INDIA PRIVATE LIMITED 381 INTEL CORP 351 ERNST & YOUNG LLP 321 PATNI AMERICAS INC 296 TERRA INFOTECH INC 281 QUALCOMM INCORPORATED 255 MPHASIS CORPORATION 251 KPMG LLP 245 PRINCE GEORGES COUNTY PUBLIC SCHS 239 BALTIMORE CITY PUBLIC SCH SYSTEM 229 DELOITTE CONSULTING LLP 218 GOLDMAN SACHS & CO 211 VERINON TECHNOLOGY SOLUTIONS LTD 208 EVEREST BUSINESS SOLUTIONS INC 208 GOOGLE INC 207 EAST BATON ROUGE PARISH SCHOOL SYS 205 DELOITTE & TOUCHE LLP 195 UNIVERSITY OF MARYLAND 191 UNIVERSITY OF PENNSYLVANIA 186 UNIV OF MICHIGAN 183 MARLABS INC 177 ORACLE USA INC 168 UNIV OF ILLINOIS AT CHICAGO 168 ALLIED SOLUTIONS GROUP INC 166 RITE AID CORPORATION 161 V-SOFT CONSULTING GROUP INC 161 CUMMINS INC 159 THE JOHNS HOPKINS MED INSTS OIS 157 VEDICSOFT SOLUTIONS INC 156 UNIV OF WISCONSIN MADISON 151 JPMORGAN CHASE & CO 150 I-FLEX SOLUTIONS INC 148 CLERYSYS INC 147 YALE UNIVERSITY 145 STATE UNIV OF NY AT STONY BROOK 143 HARVARD UNIVERSITY 143 DIS NATIONAL INSTITUTES OF HEALTH 141 YAHOO INC 139 STANFORD UNIV 138 CDC GLOBAL SERVICES INC 135 GLOBAL CONSULTANTS INC 131 LEHMAN BROTHERS INC 130 UNIV OF MINNESOTA 128 THE OHIO STATE UNIV 128 MORGAN STANLEY & CO INC 125 TEXAS