Your Appeal Rights and How to Prepare a Protest If You Don't Agree

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Taxpayer Advocate | 2014

Most Litigated Legislative Most Serious Appendices Case Advocacy Issues Recommendations Problems INTRODUCTION: Legislative Recommendations Section 7803(c)(2)(B)(ii)(VIII) of the Internal Revenue Code (IRC) requires the National Taxpayer Advocate to include in her Annual Report to Congress, among other things, legislative recommendations to resolve problems encountered by taxpayers. The chart immediately following this Introduction summarizes congressional action on recommendations the National Taxpayer Advocate proposed in her 2001 through 2013 Annual Reports.1 The National Taxpayer Advocate places a high priority on working with the tax-writing committees and other interested parties to try to resolve problems encountered by taxpayers. In addition to submitting legislative propos- als in each Annual Report, the National Taxpayer Advocate meets regularly with members of Congress and their staffs and testifies at hearings on the problems faced by taxpayers to ensure that Congress has an opportunity to receive and consider a taxpayer perspective. The following discussion highlights legislative activity during the 113th Congress relating to the National Taxpayer Advocate’s proposals. During the 113th Congress, the Senate Committee on Finance and the House Committee on Ways and Means both developed session drafts on proposed tax reform legislation that contained proposals similar to ones recommended by the National Taxpayer Advocate in her Annual Reports to Congress.2 The proposed legislation included the following: ■■ Repeal the Alternative Minimum Tax;3 ■■ Require returns of partnerships made on the basis of the calendar year to be filed on or before March 15th following the close of the calendar year, and returns made on the basis of a fiscal year to be filed on or before the 15th day of the third month following the close of the fiscal year;4 1 An electronic version of the chart is available on the TAS website at www.TaxpayerAdvocate.irs.gov/2014-Annual-Report. -

Form W-4, Employee's Withholding Certificate

Employee’s Withholding Certificate OMB No. 1545-0074 Form W-4 ▶ (Rev. December 2020) Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. ▶ Department of the Treasury Give Form W-4 to your employer. 2021 Internal Revenue Service ▶ Your withholding is subject to review by the IRS. Step 1: (a) First name and middle initial Last name (b) Social security number Enter Address ▶ Does your name match the Personal name on your social security card? If not, to ensure you get Information City or town, state, and ZIP code credit for your earnings, contact SSA at 800-772-1213 or go to www.ssa.gov. (c) Single or Married filing separately Married filing jointly or Qualifying widow(er) Head of household (Check only if you’re unmarried and pay more than half the costs of keeping up a home for yourself and a qualifying individual.) Complete Steps 2–4 ONLY if they apply to you; otherwise, skip to Step 5. See page 2 for more information on each step, who can claim exemption from withholding, when to use the estimator at www.irs.gov/W4App, and privacy. Step 2: Complete this step if you (1) hold more than one job at a time, or (2) are married filing jointly and your spouse Multiple Jobs also works. The correct amount of withholding depends on income earned from all of these jobs. or Spouse Do only one of the following. Works (a) Use the estimator at www.irs.gov/W4App for most accurate withholding for this step (and Steps 3–4); or (b) Use the Multiple Jobs Worksheet on page 3 and enter the result in Step 4(c) below for roughly accurate withholding; or (c) If there are only two jobs total, you may check this box. -

The Alternative Minimum Tax

Updated December 4, 2017 Tax Reform: The Alternative Minimum Tax The U.S. federal income tax has both a personal and a Individual AMT corporate alternative minimum tax (AMT). Both the The modern individual AMT originated with the Revenue corporate and individual AMTs operate alongside the Act of 1978 (P.L. 95-600) and operated in tandem with an regular income tax. They require taxpayers to calculate existing add-on minimum tax prior to its repeal in 1982. their liability twice—once under the rules for the regular Table 2 details selected key individual AMT parameters. income tax and once under the AMT rules—and then pay the higher amount. Minimum taxes increase tax payments Table 2. Selected Individual AMT Parameters, 2017 from taxpayers who, under the rules of the regular tax system, pay too little tax relative to a standard measure of Single/ Married their income. Head of Filing Married Filing Household Jointly Separately Corporate AMT Exemption $54,300 $84,500 $42,250 The corporate AMT originated with the Tax Reform Act of 1986 (P.L. 99-514), which eliminated an “add-on” 28% bracket 187,800 187,800 93,900 minimum tax imposed on corporations previously. The threshold corporate AMT is a flat 20% tax imposed on a Source: Internal Revenue Code. corporation’s alternative minimum taxable income less an exemption amount. A corporation’s alternative minimum The individual AMT tax base is broader than the regular taxable income is the corporation’s taxable income income tax base and starts with regular taxable income and determined with certain adjustments (primarily related to adds back various deductions, including personal depreciation) and increased by the disallowance of a exemptions and the deduction for state and local taxes. -

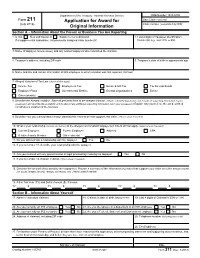

Form 211, Application for Award for Original Information

Department of the Treasury - Internal Revenue Service OMB Number 1545-0409 Form 211 Application for Award for Date Claim received (July 2018) Claim number (completed by IRS) Original Information Section A – Information About the Person or Business You Are Reporting 1. Is this New submission or Supplemental submission 2. Last 4 digits of Taxpayer Identification If a supplemental submission, list previously assigned claim number(s) Number(s) (e.g., SSN, ITIN, or EIN) 3. Name of taxpayer (include aliases) and any related taxpayers who committed the violation 4. Taxpayer's address, including ZIP code 5. Taxpayer's date of birth or approximate age 6. Name and title and contact information of IRS employee to whom violation was first reported, if known 7. Alleged Violation of Tax Law (check all that apply) Income Tax Employment Tax Estate & Gift Tax Tax Exempt Bonds Employee Plans Governmental Entities Exempt Organizations Excise Other (identify) 8. Describe the Alleged Violation. State all pertinent facts to the alleged violation. (Attach a detailed explanation and include all supporting information in your possession and describe the availability and location of any additional supporting information not in your possession.) Explain why you believe the act described constitutes a violation of the tax laws 9. Describe how you learned about and/or obtained the information that supports this claim. (Attach sheet if needed) 10. What is your relationship (current and former) to the alleged noncompliant taxpayer(s)? Check all that apply. (Attach sheet if needed) Current Employee Former Employee Attorney CPA Relative/Family Member Other (describe) 11. Do you still maintain a relationship with the taxpayer Yes No 12. -

2021 Instructions for Form 6251

Note: The draft you are looking for begins on the next page. Caution: DRAFT—NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information. Do not file draft forms and do not rely on draft forms, instructions, and publications for filing. We do not release draft forms until we believe we have incorporated all changes (except when explicitly stated on this coversheet). However, unexpected issues occasionally arise, or legislation is passed—in this case, we will post a new draft of the form to alert users that changes were made to the previously posted draft. Thus, there are never any changes to the last posted draft of a form and the final revision of the form. Forms and instructions generally are subject to OMB approval before they can be officially released, so we post only drafts of them until they are approved. Drafts of instructions and publications usually have some changes before their final release. Early release drafts are at IRS.gov/DraftForms and remain there after the final release is posted at IRS.gov/LatestForms. All information about all forms, instructions, and pubs is at IRS.gov/Forms. Almost every form and publication has a page on IRS.gov with a friendly shortcut. For example, the Form 1040 page is at IRS.gov/Form1040; the Pub. 501 page is at IRS.gov/Pub501; the Form W-4 page is at IRS.gov/W4; and the Schedule A (Form 1040/SR) page is at IRS.gov/ScheduleA. -

Pattern Criminal Jury Instructions for the District Courts of the First Circuit)

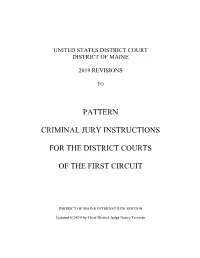

UNITED STATES DISTRICT COURT DISTRICT OF MAINE 2019 REVISIONS TO PATTERN CRIMINAL JURY INSTRUCTIONS FOR THE DISTRICT COURTS OF THE FIRST CIRCUIT DISTRICT OF MAINE INTERNET SITE EDITION Updated 6/24/19 by Chief District Judge Nancy Torresen PATTERN CRIMINAL JURY INSTRUCTIONS FOR THE FIRST CIRCUIT Preface to 1998 Edition Citations to Other Pattern Instructions How to Use the Pattern Instructions Part 1—Preliminary Instructions 1.01 Duties of the Jury 1.02 Nature of Indictment; Presumption of Innocence 1.03 Previous Trial 1.04 Preliminary Statement of Elements of Crime 1.05 Evidence; Objections; Rulings; Bench Conferences 1.06 Credibility of Witnesses 1.07 Conduct of the Jury 1.08 Notetaking 1.09 Outline of the Trial Part 2—Instructions Concerning Certain Matters of Evidence 2.01 Stipulations 2.02 Judicial Notice 2.03 Impeachment by Prior Inconsistent Statement 2.04 Impeachment of Witness Testimony by Prior Conviction 2.05 Impeachment of Defendant's Testimony by Prior Conviction 2.06 Evidence of Defendant's Prior Similar Acts 2.07 Weighing the Testimony of an Expert Witness 2.08 Caution as to Cooperating Witness/Accomplice/Paid Informant 2.09 Use of Tapes and Transcripts 2.10 Flight After Accusation/Consciousness of Guilt 2.11 Statements by Defendant 2.12 Missing Witness 2.13 Spoliation 2.14 Witness (Not the Defendant) Who Takes the Fifth Amendment 2.15 Definition of “Knowingly” 2.16 “Willful Blindness” As a Way of Satisfying “Knowingly” 2.17 Definition of “Willfully” 2.18 Taking a View 2.19 Character Evidence 2.20 Testimony by Defendant -

Charlie Way Kenneth Cosgrove Jimmy Addison Ben Kochenower Burnie Maybank Ray Stevens Brian Moody Jack Shuler Bob Steelman Don Weaver Ken Wingate

I. Welcome Meeting called to order at 11 AM. In attendance: Charlie Way Kenneth Cosgrove Jimmy Addison Ben Kochenower Burnie Maybank Ray Stevens Brian Moody Jack Shuler Bob Steelman Don Weaver Ken Wingate II. Adoption of Proposed Agenda Commissioner Way moves to adopt the proposed agenda and Commissioner Kochenower seconds his motion. The agenda is adopted by voice vote. III. Adoption of Minutes from Previous Meeting Commissioner Way moves to adopt the minutes from the previous meeting, Commissioner Kochenower seconds his motion. The minutes are adopted by voice vote. Chairman Maybank clarifies that only lobbyist principals are prohibited from contacting the commissioners. He also explains that the Commission has asked for a continuance from the legislature to allow them more time to complete their work. Chairman Maybank indicates to the Commission that they will need to begin work on subcommittees. These subcommittees can include, but are not limited to; ‘Simplified Sales and Use Tax,’ ‘Taxation of Services,’ and ‘Taxation of Intangibles.’ IV. FTA Presentation: State Sales Taxes and Services – Jim Eads *Mr. Eads notes that his comments are his own and not a representation of the members of the tax administrators.* Mr. Eads believes a tax system should be perceived as fair and perfection should be sought in terms of ‘fairness.’ Sales tax is the largest revenue component that most states have with a total of 45 states implementing a sales tax. Taxation of services is another method many states have begun to explore. South Carolina taxes about 35 of 160 services. This puts the state in line with neighboring states. -

State Tax Expenditure Limitation and Supermajority Requirement: New and Updated Data

State tax expenditure limitation and supermajority requirement: New and updated data State Tax and Expenditure Limitations and Supermajority Requirements: New and Updated Data Cody Kallen* American Enterprise Institute August 24, 2017 Abstract This paper conducts original primary source research on state-level tax and expenditure limitations and supermajority requirements to raise taxes. I update and correct the tax and expenditure limitation (TEL) index in Amiel, Deller and Stallman (2009), which covered the period from 1969 through 2005, to extend through 2015. This index should serve as a more effective measure of the restrictiveness of state TELs than the dummy variables often used in studies. I also provide a measure of the procedural difficulty of raising taxes. I describe the TEL history for each state, the specific details of each TEL, references to the text of the provisions and the measures that created them, and the scoring details. JEL Classification: H71, H72 Keywords: tax and expenditure limitations, supermajority vote requirements, state government, budget process *The author is a research associate at the American Enterprise Institute. He thanks Alan D. Viard for oversight and review and PEOPLE for helpful comments. Any errors in this paper are those of the author alone. I. Introduction How can citizens and legislators enforce fiscal discipline on current and future legislatures? The Tax Revolt of the 1970s brought to prominence the idea of imposing limits on the growth of government revenues and expenditures. These restraints, known as tax and expenditure limits (TELs), are currently active across the country and in states of all political persuasions. TELs are typically enacted either to limit the size of government or to rein in future government growth, and they can apply to the state government or to local governments. -

The Viability of the Fair Tax

The Fair Tax 1 Running head: THE FAIR TAX The Viability of The Fair Tax Jonathan Clark A Senior Thesis submitted in partial fulfillment of the requirements for graduation in the Honors Program Liberty University Fall 2008 The Fair Tax 2 Acceptance of Senior Honors Thesis This Senior Honors Thesis is accepted in partial fulfillment of the requirements for graduation from the Honors Program of Liberty University. ______________________________ Gene Sullivan, Ph.D. Thesis Chair ______________________________ Donald Fowler, Th.D. Committee Member ______________________________ JoAnn Gilmore, M.B.A. Committee Member ______________________________ James Nutter, D.A. Honors Director ______________________________ Date The Fair Tax 3 Abstract This thesis begins by investigating the current system of federal taxation in the United States and examining the flaws within the system. It will then deal with a proposal put forth to reform the current tax system, namely the Fair Tax. The Fair Tax will be examined in great depth and all aspects of it will be explained. The objective of this paper is to determine if the Fair Tax is a viable solution for fundamental tax reform in America. Both advantages and disadvantages of the Fair Tax will objectively be pointed out and an educated opinion will be given regarding its feasibility. The Fair Tax 4 The Viability of the Fair Tax In 1986 the United States federal tax code was changed dramatically in hopes of simplifying the previous tax code. Since that time the code has undergone various changes that now leave Americans with over 60,000 pages of tax code, rules, and rulings that even the most adept tax professionals do not understand. -

Information for Persons Representing Themselves Before the U.S. Tax Court

Information for Persons Representing Themselves Before the U.S. Tax Court United States Tax Court Washington, D.C. August 2010 INTRODUCTION This guide provides information, but not legal advice, for individuals who represent themselves before the Tax Court. It answers some of taxpayers' most frequent questions. It is a step-by-step explanation of the process of: Filing a petition to begin your Tax Court case Things that occur before trial Things that occur during trial Things that occur after trial Definition of terms (Glossary) For more detailed information, consult the Tax Court Rules of Practice and Procedure, available on the Court's Web site (www.ustaxcourt.gov). A copy of the Tax Court Rules (Rules) may be obtained for $20.00 by writing to the United States Tax Court, 400 Second Street, N.W., Washington, D.C. 20217, and enclosing a check or money order for that amount payable to the "Clerk, United States Tax Court." Please do not send cash. ADDRESS ALL MAIL TO: United States Tax Court 400 Second Street, N.W. Washington, D.C. 20217 CONTENTS ABOUT THE TAX COURT 1 What is the United States Tax Court? 1 What are the Tax Court's Hours of Operation? 1 STARTING A CASE 2 How do I start a case in the Tax Court? 2 Who can file a petition with the Tax Court? 2 Is there anyone who can help me file a petition and/or help me in my case against the IRS? 2 How can I find a tax clinic? 3 If I want to represent myself or if I don't qualify for representation by a tax clinic, can I represent myself? 3 What should I do if I don't speak and/or understand English very well? 3 Are there any circumstances where the Court will help pay for the cost of an interpreter at trial? 3 If I need an interpreter at trial what should I do? 4 I thought I came to an agreement with the IRS, but the IRS sent me notice of deficiency or a notice of determination stating that I have a right to file a petition with the Tax Court. -

Mazzei; Angelo L

No. 18-72451 IN THE UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT _______________________________ CELIA MAZZEI; ANGELO L. MAZZEI; MARY E. MAZZEI, Petitioners-Appellants v. COMMISSIONER OF INTERNAL REVENUE, Respondent-Appellee _______________________________ ON APPEAL FROM THE DECISIONS OF THE UNITED STATES TAX COURT _______________________________ BRIEF FOR THE APPELLEE _______________________________ RICHARD E. ZUCKERMAN Principal Deputy Assistant Attorney General TRAVIS A. GREAVES Deputy Assistant Attorney General GILBERT S. ROTHENBERG (202) 514-3361 TERESA E. MCLAUGHLIN (202) 514-4342 JUDITH A. HAGLEY (202) 514-8126 Attorneys Tax Division Department of Justice Post Office Box 502 Washington, D.C. 20044 -i- TABLE OF CONTENTS Page Table of contents .......................................................................................... i Table of authorities .................................................................................. iii Glossary ...................................................................................................viii Jurisdictional statement ............................................................................ 1 Statement of the issue ................................................................................ 1 Applicable statutes and regulations .......................................................... 2 Statement of the case ................................................................................. 2 A. Procedural overview ................................................................ -

Form 1040 Page Is at IRS.Gov/Form1040; the Pub

Note: The draft you are looking for begins on the next page. Caution: DRAFT—NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information. Do not file draft forms and do not rely on draft forms, instructions, and publications for filing. We do not release draft forms until we believe we have incorporated all changes (except when explicitly stated on this coversheet). However, unexpected issues occasionally arise, or legislation is passed—in this case, we will post a new draft of the form to alert users that changes were made to the previously posted draft. Thus, there are never any changes to the last posted draft of a form and the final revision of the form. Forms and instructions generally are subject to OMB approval before they can be officially released, so we post only drafts of them until they are approved. Drafts of instructions and publications usually have some changes before their final release. Early release drafts are at IRS.gov/DraftForms and remain there after the final release is posted at IRS.gov/LatestForms. All information about all forms, instructions, and pubs is at IRS.gov/Forms. Almost every form and publication has a page on IRS.gov with a friendly shortcut. For example, the Form 1040 page is at IRS.gov/Form1040; the Pub. 501 page is at IRS.gov/Pub501; the Form W-4 page is at IRS.gov/W4; and the Schedule A (Form 1040/SR) page is at IRS.gov/ScheduleA.