Federal Register/Vol. 68, No. 208/Tuesday, October 28, 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Form W-4, Employee's Withholding Certificate

Employee’s Withholding Certificate OMB No. 1545-0074 Form W-4 ▶ (Rev. December 2020) Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. ▶ Department of the Treasury Give Form W-4 to your employer. 2021 Internal Revenue Service ▶ Your withholding is subject to review by the IRS. Step 1: (a) First name and middle initial Last name (b) Social security number Enter Address ▶ Does your name match the Personal name on your social security card? If not, to ensure you get Information City or town, state, and ZIP code credit for your earnings, contact SSA at 800-772-1213 or go to www.ssa.gov. (c) Single or Married filing separately Married filing jointly or Qualifying widow(er) Head of household (Check only if you’re unmarried and pay more than half the costs of keeping up a home for yourself and a qualifying individual.) Complete Steps 2–4 ONLY if they apply to you; otherwise, skip to Step 5. See page 2 for more information on each step, who can claim exemption from withholding, when to use the estimator at www.irs.gov/W4App, and privacy. Step 2: Complete this step if you (1) hold more than one job at a time, or (2) are married filing jointly and your spouse Multiple Jobs also works. The correct amount of withholding depends on income earned from all of these jobs. or Spouse Do only one of the following. Works (a) Use the estimator at www.irs.gov/W4App for most accurate withholding for this step (and Steps 3–4); or (b) Use the Multiple Jobs Worksheet on page 3 and enter the result in Step 4(c) below for roughly accurate withholding; or (c) If there are only two jobs total, you may check this box. -

The Alternative Minimum Tax

Updated December 4, 2017 Tax Reform: The Alternative Minimum Tax The U.S. federal income tax has both a personal and a Individual AMT corporate alternative minimum tax (AMT). Both the The modern individual AMT originated with the Revenue corporate and individual AMTs operate alongside the Act of 1978 (P.L. 95-600) and operated in tandem with an regular income tax. They require taxpayers to calculate existing add-on minimum tax prior to its repeal in 1982. their liability twice—once under the rules for the regular Table 2 details selected key individual AMT parameters. income tax and once under the AMT rules—and then pay the higher amount. Minimum taxes increase tax payments Table 2. Selected Individual AMT Parameters, 2017 from taxpayers who, under the rules of the regular tax system, pay too little tax relative to a standard measure of Single/ Married their income. Head of Filing Married Filing Household Jointly Separately Corporate AMT Exemption $54,300 $84,500 $42,250 The corporate AMT originated with the Tax Reform Act of 1986 (P.L. 99-514), which eliminated an “add-on” 28% bracket 187,800 187,800 93,900 minimum tax imposed on corporations previously. The threshold corporate AMT is a flat 20% tax imposed on a Source: Internal Revenue Code. corporation’s alternative minimum taxable income less an exemption amount. A corporation’s alternative minimum The individual AMT tax base is broader than the regular taxable income is the corporation’s taxable income income tax base and starts with regular taxable income and determined with certain adjustments (primarily related to adds back various deductions, including personal depreciation) and increased by the disallowance of a exemptions and the deduction for state and local taxes. -

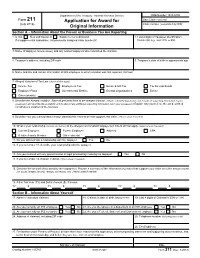

Form 211, Application for Award for Original Information

Department of the Treasury - Internal Revenue Service OMB Number 1545-0409 Form 211 Application for Award for Date Claim received (July 2018) Claim number (completed by IRS) Original Information Section A – Information About the Person or Business You Are Reporting 1. Is this New submission or Supplemental submission 2. Last 4 digits of Taxpayer Identification If a supplemental submission, list previously assigned claim number(s) Number(s) (e.g., SSN, ITIN, or EIN) 3. Name of taxpayer (include aliases) and any related taxpayers who committed the violation 4. Taxpayer's address, including ZIP code 5. Taxpayer's date of birth or approximate age 6. Name and title and contact information of IRS employee to whom violation was first reported, if known 7. Alleged Violation of Tax Law (check all that apply) Income Tax Employment Tax Estate & Gift Tax Tax Exempt Bonds Employee Plans Governmental Entities Exempt Organizations Excise Other (identify) 8. Describe the Alleged Violation. State all pertinent facts to the alleged violation. (Attach a detailed explanation and include all supporting information in your possession and describe the availability and location of any additional supporting information not in your possession.) Explain why you believe the act described constitutes a violation of the tax laws 9. Describe how you learned about and/or obtained the information that supports this claim. (Attach sheet if needed) 10. What is your relationship (current and former) to the alleged noncompliant taxpayer(s)? Check all that apply. (Attach sheet if needed) Current Employee Former Employee Attorney CPA Relative/Family Member Other (describe) 11. Do you still maintain a relationship with the taxpayer Yes No 12. -

2021 Instructions for Form 6251

Note: The draft you are looking for begins on the next page. Caution: DRAFT—NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information. Do not file draft forms and do not rely on draft forms, instructions, and publications for filing. We do not release draft forms until we believe we have incorporated all changes (except when explicitly stated on this coversheet). However, unexpected issues occasionally arise, or legislation is passed—in this case, we will post a new draft of the form to alert users that changes were made to the previously posted draft. Thus, there are never any changes to the last posted draft of a form and the final revision of the form. Forms and instructions generally are subject to OMB approval before they can be officially released, so we post only drafts of them until they are approved. Drafts of instructions and publications usually have some changes before their final release. Early release drafts are at IRS.gov/DraftForms and remain there after the final release is posted at IRS.gov/LatestForms. All information about all forms, instructions, and pubs is at IRS.gov/Forms. Almost every form and publication has a page on IRS.gov with a friendly shortcut. For example, the Form 1040 page is at IRS.gov/Form1040; the Pub. 501 page is at IRS.gov/Pub501; the Form W-4 page is at IRS.gov/W4; and the Schedule A (Form 1040/SR) page is at IRS.gov/ScheduleA. -

The Viability of the Fair Tax

The Fair Tax 1 Running head: THE FAIR TAX The Viability of The Fair Tax Jonathan Clark A Senior Thesis submitted in partial fulfillment of the requirements for graduation in the Honors Program Liberty University Fall 2008 The Fair Tax 2 Acceptance of Senior Honors Thesis This Senior Honors Thesis is accepted in partial fulfillment of the requirements for graduation from the Honors Program of Liberty University. ______________________________ Gene Sullivan, Ph.D. Thesis Chair ______________________________ Donald Fowler, Th.D. Committee Member ______________________________ JoAnn Gilmore, M.B.A. Committee Member ______________________________ James Nutter, D.A. Honors Director ______________________________ Date The Fair Tax 3 Abstract This thesis begins by investigating the current system of federal taxation in the United States and examining the flaws within the system. It will then deal with a proposal put forth to reform the current tax system, namely the Fair Tax. The Fair Tax will be examined in great depth and all aspects of it will be explained. The objective of this paper is to determine if the Fair Tax is a viable solution for fundamental tax reform in America. Both advantages and disadvantages of the Fair Tax will objectively be pointed out and an educated opinion will be given regarding its feasibility. The Fair Tax 4 The Viability of the Fair Tax In 1986 the United States federal tax code was changed dramatically in hopes of simplifying the previous tax code. Since that time the code has undergone various changes that now leave Americans with over 60,000 pages of tax code, rules, and rulings that even the most adept tax professionals do not understand. -

Form 1040 Page Is at IRS.Gov/Form1040; the Pub

Note: The draft you are looking for begins on the next page. Caution: DRAFT—NOT FOR FILING This is an early release draft of an IRS tax form, instructions, or publication, which the IRS is providing for your information. Do not file draft forms and do not rely on draft forms, instructions, and publications for filing. We do not release draft forms until we believe we have incorporated all changes (except when explicitly stated on this coversheet). However, unexpected issues occasionally arise, or legislation is passed—in this case, we will post a new draft of the form to alert users that changes were made to the previously posted draft. Thus, there are never any changes to the last posted draft of a form and the final revision of the form. Forms and instructions generally are subject to OMB approval before they can be officially released, so we post only drafts of them until they are approved. Drafts of instructions and publications usually have some changes before their final release. Early release drafts are at IRS.gov/DraftForms and remain there after the final release is posted at IRS.gov/LatestForms. All information about all forms, instructions, and pubs is at IRS.gov/Forms. Almost every form and publication has a page on IRS.gov with a friendly shortcut. For example, the Form 1040 page is at IRS.gov/Form1040; the Pub. 501 page is at IRS.gov/Pub501; the Form W-4 page is at IRS.gov/W4; and the Schedule A (Form 1040/SR) page is at IRS.gov/ScheduleA. -

![[REG-107100-00] RIN 1545-AY26 Disallowance of De](https://docslib.b-cdn.net/cover/2433/reg-107100-00-rin-1545-ay26-disallowance-of-de-1222433.webp)

[REG-107100-00] RIN 1545-AY26 Disallowance of De

[4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 [REG-107100-00] RIN 1545-AY26 Disallowance of Deductions and Credits for Failure to File Timely Return AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking by cross-reference to temporary regulations and notice of public hearing. SUMMARY: This document contains proposed regulations relating to the disallowance of deductions and credits for nonresident alien individuals and foreign corporations that fail to file a timely U.S. income tax return. The current regulations permit nonresident aliens and foreign corporations the benefit of deductions and credits only if they timely file a U.S. income tax return in accordance with subtitle F of the Internal Revenue Code, unless the Commissioner waives the filing deadlines. The temporary regulations revise the waiver standard. The text of the temporary regulations on this subject in this issue of the Federal Register also serves as the text of these proposed regulations set forth in this cross-referenced notice of proposed rulemaking. This document also provides notice of a public hearing on these proposed regulations. DATES: Written comments must be received by April 29, 2002. Requests to speak and outlines of topics to be discussed at the public hearing scheduled for June 3, 2002, at 10 a.m. must be received by May 13, 2002. ADDRESSES: Send submissions to: CC:ITA:RU (REG-107100-00), room 5226, Internal -2- Revenue Service, POB 7604, Ben Franklin Station, Washington, DC 20044. Submissions may be hand delivered Monday through Friday between the hours of 8 a.m. -

2021 Form 1099-MISC

Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file copy A downloaded from this website; a penalty may be imposed for filing with the IRS information return forms that can’t be scanned. See part O in the current General Instructions for Certain Information Returns, available at www.irs.gov/form1099, for more information about penalties. Please note that Copy B and other copies of this form, which appear in black, may be downloaded and printed and used to satisfy the requirement to provide the information to the recipient. To order official IRS information returns, which include a scannable Copy A for filing with the IRS and all other applicable copies of the form, visit www.IRS.gov/orderforms. Click on Employer and Information Returns, and we’ll mail you the forms you request and their instructions, as well as any publications you may order. Information returns may also be filed electronically using the IRS Filing Information Returns Electronically (FIRE) system (visit www.IRS.gov/FIRE) or the IRS Affordable Care Act Information Returns (AIR) program (visit www.IRS.gov/AIR). See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms. 9595 VOID CORRECTED PAYER’S name, street address, city or town, state or province, country, ZIP 1 Rents OMB No. -

Taxpayer Identification Number Certification Instructions

TAXPAYER IDENTIFICATION NUMBER CERTIFICATION INSTRUCTIONS (Section references are to the Internal Revenue Code.) 1. PURPOSE OF FORM A credit union that is required to file information returns with the Internal Revenue Service (IRS) must get the correct taxpayer identification numbers (TINs) of members in order to report to the IRS certain income paid to members (A TIN is either a social security number (SSN), an employee identification number (EIN), or an individual tax identification number (ITIN).) IRS Form W-9, Request for Taxpayer Identification Number and Certification, is used by credit unions to request correct TINs for members as well as to request that members certify certain claims. Form W-9 is used if members can certify that they are U.S. persons or resident aliens, that the TINs they provide are correct, and that they are not subject to backup withholding. Use Form W-9, Request For Taxpayer Identification Number And Certification or Credit Union’s qualifying signature card form to furnish your correct TIN to the requester (the person asking you to furnish your TIN), and, when applicable (1) to certify that the TIN you are furnishing is correct (or that you are waiting for a number to be issued, (2) to certify that you are not subject to backup withholding, and (3) to claim exemption from backup withholding if you are an exempt payee. Furnishing your correct TIN and making the appropriate certifications will prevent certain payments from being subject to the 28% backup withholding. Individuals who have an ITIN must provide it on Form W-9. -

![[4830-01-U] DEPARTMENT of THE](https://docslib.b-cdn.net/cover/9093/4830-01-u-department-of-the-1529093.webp)

[4830-01-U] DEPARTMENT of THE

[4830-01-u] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 31 [TD 8822] RIN 1545-AW28 Federal Employment Tax Deposits-De Minimis Rule AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Final regulations. SUMMARY: This document contains final regulations relating to the deposit of Federal employment taxes. The final regulations adopt the rules of temporary regulations that change the de minimis deposit rule for quarterly and annual return periods from $500 to $1,000. The regulations affect taxpayers required to make deposits of Federal employment taxes. DATES: Effective date: These regulations are effective June 17, 1999. Applicability date: For dates of applicability, see §31.6302-1(f)(4). FOR FURTHER INFORMATION CONTACT: Vincent Surabian, (202) 622- 4940 (not a toll-free number). SUPPLEMENTARY INFORMATION: Background This document contains amendments to 26 CFR part 31, Employment Taxes and Collection of Income Tax at Source. On June 16, 1998, temporary and final regulations (TD 8771) relating to the deposit of Federal employment taxes under section 6302 of the - 2 - Internal Revenue Code were published in the Federal Register (63 FR 32735). A notice of proposed rulemaking (REG-110403-98) cross-referencing the temporary regulations was published in the Federal Register for the same day (63 FR 32774). No comments were received from the public in response to the notice of proposed rulemaking. Explanation of Provisions These final regulations adopt the rules of the temporary regulations. Under these rules, a taxpayer that has accumulated Federal employment taxes of less than $1,000 for a return period (quarterly or annual, as the case may be) does not have to make deposits but may remit its full liability with a timely filed return for the return period. -

Revenge of the Tax Protesters

G THE B IN EN V C R H E S A N 8 D 8 B 8 A E 1 R SINC Web address: http://www.nylj.com VOLUME 234—NO. 52 WEDNESDAY, SEPTEMBER 14, 2005 TAX LITIGATION ISSUES BY JOHN J. TIGUE JR. AND JEREMY H. TEMKIN Revenge of the Tax Protesters ax protesters, or individuals noted that courts “have consistently who claim that they are not rejected …arguments [raised by tax legally required to pay taxes, protesters] and imposed substantial penal- have been around for a long ties on those taking these unsupportable T positions. Those potentially tempted by time. In recent years, however, the num- ber of tax protesters appears to have these schemes need to realize that they increased as numerous individuals and carry a heavy price for both the taxpayers 2 groups actively market and sell a variety of John J. Tigue Jr. Jeremy H. Temkin and the promoters.” As set forth in IRS materials supporting the claim that Notice 2005-30, civil and criminal American citizens are not obligated to pay penalties apply to taxpayers who make income taxes. As a result, the IRS has increased its frivolous arguments. Civil penalties Among the arguments raised by tax focus on prosecuting individuals who include a $500 penalty for filing a protesters are: (1) that the 16th make such arguments, which it views as frivolous income tax return and a penalty Amendment to the Constitution, which willful tax evasion. In March of this year, of up to $25,000 if a taxpayer pursues authorizes income taxes, was never IRS Commissioner Mark W. -

Fiscal Year 2020 Statutory Audit of Compliance with Legal Guidelines Prohibiting the Use of Illegal Tax Protester and Similar Designations

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Fiscal Year 2020 Statutory Audit of Compliance With Legal Guidelines Prohibiting the Use of Illegal Tax Protester and Similar Designations September 8, 2020 Reference Number: 2020-30-057 [email protected] | www.treasury.gov/tigta | 202-622-6500 This report has cleared the Treasury Inspector General for Tax Administration disclosure review process and information determined to be restricted from public release has been redacted from this document. Redaction Legend: 1 1 = Tax Return/Return Information To report fraud, waste, or abuse, please call us at 1-800-366-4484 HIGHLIGHTS: Fiscal Year 2020 Statutory Audit of Compliance With Legal Guidelines Prohibiting the Use of Illegal Tax Protester and Similar Designations Final Audit Report issued on September 8, 2020 Reference Number 2020-30-057 Why TIGTA Did This Audit What TIGTA Found This audit was initiated because Prior to enactment of the RRA 98, the IRS used Illegal Tax Protester Congress enacted the prohibition indicators on the Individual Master File to accelerate enforcement against Illegal Tax Protester activity for taxpayers whose tax returns or correspondence contained designations due to a concern specific indicators of noncompliance with the tax law, such as the use that some taxpayers were being of arguments repeatedly rejected by the courts. Section 3707 of the permanently labeled as Illegal Tax RRA 98 required the IRS to remove the existing Illegal Tax Protester Protesters even though they had designations from taxpayers’ accounts on the Individual Master File subsequently become compliant beginning January 1, 1999. TIGTA’s review of taxpayer accounts on with the tax laws.