China A-Share Autos

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Final Report

25 June 2015 Final Report Assessment of the normative and policy framework governing the Chinese economy and its impact on international competition For: AEGIS EUROPE Brussels Belgium THINK!DESK China Research & Consulting Prof. Dr. Markus Taube & Dr. Christian Schmidkonz GbR Merzstrasse 18 81679 München Tel.: +49 - (0)89 - 26 21 27 82 [email protected] www.thinkdesk.de 1 This report has been prepared by: Prof. Dr. Markus Taube Peter Thomas in der Heiden 2 Contents Executive Summary ························································································· 11 1. Introduction ······························································································ 27 Part I: The Management of the Chinese Economy: Institutional Set-up and Policy Instruments 2. Centralised Planning and Market Forces in the Chinese Economy ··················· 32 2.1 The Role of Planning in the Chinese Economy ············································ 32 2.1.1 Types of Plans ··············································································· 32 2.1.2 Plans and Complementary Documents················································ 41 2.2 Dedicated Government Programmes for Industry Guidance ··························· 45 2.2.1 Subsidies – An Overview ································································· 45 2.2.1.1 Examples for Preferential Policies and Grant Giving Operations by Local Governments ································································ 51 2.2.1.2 Recent Initiatives by the Central Government -

China Autos Asia China Automobiles & Components

Deutsche Bank Markets Research Industry Date 18 May 2016 China Autos Asia China Automobiles & Components Vincent Ha, CFA Fei Sun, CFA Research Analyst Research Analyst (+852 ) 2203 6247 (+852 ) 2203 6130 [email protected] [email protected] F.I.T.T. for investors What you should know about China's new energy vehicle (NEV) market Many players, but only a few are making meaningful earnings contributions One can question China’s target to put 5m New Energy Vehicles on the road by 2020, or its ambition to prove itself a technology leader in the field, but the surge in demand with 171k vehicles sold in 4Q15 cannot be denied. Policy imperatives and government support could ensure three-fold volume growth by 2020, which would make China half of this developing global market. New entrants are proliferating, with few clear winners as yet, but we conclude that Yutong and BYD have the scale of NEV sales today to support Buy ratings. ________________________________________________________________________________________________________________ Deutsche Bank AG/Hong Kong Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016. Deutsche Bank Markets Research Asia Industry Date China 18 May 2016 Automobiles & China -

23-10-2010.Pdf

DIARIOREPUBLICA OFICIAL.- DE San EL SALVADOR Salvador, EN 23 LA de AMERICA Octubre CENTRAL de 2010. 11 DIARIO OFI CIAL DIRECTOR: Luis Ernesto Flores López TOMO Nº 389 SAN SALVADOR, SABADO 23 DE OCTUBRE DE 2010 NUMERO 199 - La Dirección de la Imprenta Nacional hace del conocimiento que toda publicación en el Diario Ofi cial se procesa por transcripción directa y fi el del original, por consiguiente la institución no se hace responsable por transcripciones cuyos originales lleguen en forma ilegible y/o defectuosa y son de exclusiva responsabilidad de la persona o institución que los presentó. (Arts. 21, 22 y 23 Reglamento de la Imprenta Nacional). S U M A R I O Pág. Pág. ORGANO EJECUTIVO INSTITUCIONES AUTONOMAS MINISTERIO DE GOBERNACIÓN ALCALDÍASCONSULTA MUNICIPALES RAMO DE GOBERNACIÓN Decreto No. 2.- Ordenanza reguladora de las tasas por Cambio de denominación del Buró de Convenciones de la servicios municipales de la ciudad de El Rosario, departamento Ciudad de El Salvador, por el de Asociación Buró de Convenciones de La Paz. ...................................................................................LEGAL 20-34 de El Salvador, nuevos estatutos y Acuerdo Ejecutivo No. 132, PARA aprobándolos. ............................................................................. 4-14 Decretos Nos. 3(2), 5 y 7.- Ordenanzas transitorias de exención de intereses y multas generadas por deudas en concepto MINISTERIO DE HACIENDA de impuestos y tasas a favor de los municipios de El Rosario, Acajutla, Guazapa y Conchagua, respectivamente. ................... 35-40 RAMO DE HACIENDA SOLO Estatutos de las Asociaciones Comunales “Cantón San Acuerdo No. 1165.- Se autorizan precios para la venta de Agustín”, “Sector Sur, Cantón Huisquil”, “Unión, Colonia Santa productos y servicios, prestados por la Dirección General de VALIDEZMónica 1 y 2” y “Colonia Prados de Montesión, Cantón Santa Correos. -

China Vehicle Axle Sales Market Report 2021

Report Information More information from: https://www.wiseguyreports.com/reports/595146-china-vehicle-axle-sales-market-report-2021 China Vehicle Axle Sales Market Report 2021 Report / Search Code: WGR595146 Publish Date: 9 August, 2016 Price 1-user PDF : $ 3200.0 Enterprise PDF : $ 4160.0 Description: This report studies sales (consumption) of Vehicle Axle in China market, focuses on the top players, with sales, price, revenue and market share for each player, covering American Axle & Manufacturing Meritor DANA Benteler RABA AxleTech International SAF-HOLLAND PRESS KOGYO CO Korea Flange Co Ankai Futian Shuguang Axle SINOTRUK SAIC MOTOR HANDE Shandong Heavy Industry Group SG Automotive Group Sichuan Jian’an Industrial Qingte Split by product types, with sales, revenue, price, market share and growth rate of each type, can be divided into Type I Type II Type III Split by applications, this report focuses on sales, market share and growth rate of Vehicle Axle in each application, can be divided into Application 1 Application 2 Application 3 Contents: Table of Contents China Vehicle Axle Sales Market Report 2021 1 Vehicle Axle Overview 1.1 Product Overview and Scope of Vehicle Axle 1.2 Classification of Vehicle Axle 1.2.1 Type I 1.2.2 Type II 1.2.3 Type III 1.3 Applications of Vehicle Axle 1.3.1 Application 1 1.3.2 Application 2 1.3.3 Application 3 1.4 China Market Size (Value and Volume) of Vehicle Axle (2011-2021) 1.4.1 China Vehicle Axle Sales, Revenue and Price (2011-2021) 1.4.2 China Vehicle Axle Sales and Growth Rate (2011-2021) 1.4.3 -

China Bus Industry Report, 2019-2025

China Bus Industry Report, 2019-2025 June 2019 STUDY GOAL AND OBJECTIVES METHODOLOGY This report provides the industry executives with strategically signifisignificantcant Both primary and secondary research methodologies were used competitor information, analysis, insight and projection on the in preparing this study. Initially, a comprehensive and exhaustive competitive pattern and key companies in the industry, crucial to the search of the literature on this industry was conducted. These development and implementation of effective business, marketing and sources included related books and journals, trade literature, R&D programs. marketing literature, other product/promotional literature, annual reports, security analyst reports, and other publications. REPORT OBJECTIVES Subsequently, telephone interviews or email correspondence TtblihTo establish a compre hiftlhensive, factual, annua lldtddtlly updated and cost- was conducted with marketing executives etc. Other sources effective information base on market size, competition patterns, included related magazines, academics, and consulting market segments, goals and strategies of the leading players in the companies. market, reviews and forecasts. To assist potential market entrants in evaluating prospective INFORMATION SOURCES acquisition and joint venture candidates. The primary information sources include Company Reports, To complement the organizations’ internal competitor information and National Bureau of Statistics of China etc. gathering efforts with strategic analysis, data -

Global Compreed Natural Gas Vehicles Market 2018 | Industry Overview, Sales, Supply and Demand Analysis and Forecast 2023

2018-09-26 10:14 CEST Global Compreed Natural Gas Vehicles Market 2018 | industry overview, sales, supply and demand analysis and forecast 2023 Global Compreed Natural Gas Vehicles report offers the latest industry trends, technological innovations and forecast market data. A deep-dive view of Compreed Natural Gas Vehicles industry based on market size, Compreed Natural Gas Vehicles growth, development plans, and opportunities is offered by this report. The forecast market information, SWOT analysis, Compreed Natural Gas Vehicles barriers, and feasibility study are the vital aspects analyzed in this report. Get FREE Sample Report Copy @ https://www.globalmarketers.biz/report/automotive-and- transportation/world-compreed-natural-gas-vehicles-market-research-report- 2022(covering-usa,-eu,-china,-south-east-asia,-japan-and- etc)/16548#request_sample Compreed Natural Gas Vehicles market segmentation by Players: • Faw-Volkswagen • DPCA • Beijing Hyundai • Saic-Volkswagen • DYK • Changan-Suzuki • Cherry • BYD • Lifan • Yutong • JAC • Shudu Bus • Zhongtong Bus • King Long • SG Automotive Group • Asiastar • Yangtse • Foton • Brilliance Auto • Haima • Shaolin Bus • Geely • Changan The up-to-date, comprehensive product knowledge, industry growth curve, end users will drive the revenue and profitability. Compreed Natural Gas Vehicles report studies the present state of the industry to analyze the future growth opportunities and risk factors. Compreed Natural Gas Vehicles report aims at providing a 360-degree market scenario. Initially, the report offers Compreed Natural Gas Vehicles introduction, fundamental overview, objectives, market definition, Compreed Natural Gas Vehicles scope, and market size estimation. Compreed Natural Gas Vehicles report helps the readers in understanding the growth factors, industry plans, policies and development strategies implemented by leading Compreed Natural Gas Vehicles players. -

Diario Ofi Cial Sumario

DIARIOREPUBLICA OFICIAL.- DE San EL SALVADOR Salvador, EN 21 LA de AMERICA Octubre CENTRAL de 2010. 11 DIARIO OFI CIAL DIRECTOR: Luis Ernesto Flores López TOMO Nº 389 SAN SALVADOR, JUEVES 21 DE OCTUBRE DE 2010 NUMERO 197 - La Dirección de la Imprenta Nacional hace del conocimiento que toda publicación en el Diario Ofi cial se procesa por transcripción directa y fi el del original, por consiguiente la institución no se hace responsable por transcripciones cuyos originales lleguen en forma ilegible y/o defectuosa y son de exclusiva responsabilidad de la persona o institución que los presentó. (Arts. 21, 22 y 23 Reglamento de la Imprenta Nacional). S U M A R I O Pág. Pág. Reformas a los estatutos de la Asociación de Desarrollo ORGANO EJECUTIVO Comunal Fuerza Espiritual y Acuerdo No. 160, emitido por la Alcaldía Municipal de Santa Rosa Guachipilín, aprobándolas. 25-29 MINISTERIO DE EDUCACION CONSULTA RAMO DE EDUCACIÓN SECCION CARTELES OFICIALES Acuerdo No. 15-0748.- Equivalencia de estudios a favor de Velky Yoliveth Degrandes Rodríguez. ................................. 4 LEGAL PARADE PRIMERA PUBLICACION MINISTERIO DE MEDIO AMBIENTE Y Declaratoria de Herencia RECURSOS NATURALES Cartel No. 1203.- Emilia Quintana de Mineros y otro (1 30 RAMO DE MEDIO AMBIENTE Y RECURSOS vez) ........................................................................................... NATURALES SOLO DE SEGUNDA PUBLICACION Acuerdo No. 107.- Se concede plazo a la Dirección VALIDEZ General de Ciudadanía y Territorio, para que cumpla con ciertos Aceptación de Herencia requerimientos. ........................................................................... 4 Cartel No. 1187.- Mauricia Salgado de Gómez y otro (3 alt.) ........................................................................................... 30 ORGANO JUDICIAL Cartel No. 1188.- Beatriz de Jesús González Girón (3 OFICIALTIENE alt.) ........................................................................................... 30 CORTE SUPREMA DE JUSTICIA Cartel No. -

Fact Book 2012 2012 Fact Book III Contents

Fact Book 2012 2012 Fact Book III Contents Shanghai Securities Market.......................................................1 Historical Review .........................................................................................................................................1 Securities Products ......................................................................................................................................1 2011 Market Review ....................................................................5 Overview ....................................................................................................................................................5 Securities Issuance and Listing ......................................................................................................................5 Introduction of New Products ........................................................................................................................6 Pledge-style Bond Repo ...............................................................................................................................6 Securities Repo ...........................................................................................................................................6 Major Events in the Securities Market 2011 ....................................................................................................7 Market Highlights ........................................................................................................................................10 -

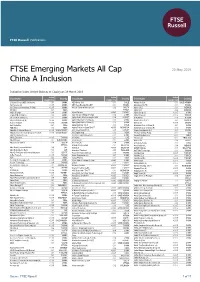

FTSE Emerging Markets All Cap China a Inclusion

FTSE Russell Publications FTSE Emerging Markets All Cap 20 May 2019 China A Inclusion Indicative Index Weight Data as at Closing on 29 March 2019 Index Index Index Constituent Country Constituent Country Constituent Country weight (%) weight (%) weight (%) 21Vianet Group (ADS) (N Shares) 0.01 CHINA AES Gener S.A. 0.01 CHILE Almarai Co Ltd 0.01 SAUDI ARABIA 360 Security (A) <0.005 CHINA AES Tiete Energia SA UNIT 0.01 BRAZIL Alpargatas SA PN 0.01 BRAZIL 361 Degrees International (P Chip) <0.005 CHINA African Rainbow Minerals Ltd 0.02 SOUTH Alpek S.A.B. 0.01 MEXICO 3M India 0.01 INDIA AFRICA Alpha Bank 0.04 GREECE 3SBio (P Chip) 0.04 CHINA Afyon Cimento <0.005 TURKEY Alpha Group (A) <0.005 CHINA 51job ADR (N Shares) 0.03 CHINA Agile Group Holdings (P Chip) 0.04 CHINA Alpha Networks <0.005 TAIWAN 58.com ADS (N Shares) 0.12 CHINA Agility Public Warehousing Co KSC 0.04 KUWAIT ALROSA ao 0.06 RUSSIA 5I5j Holding Group (A) <0.005 CHINA Agricultural Bank of China (A) 0.06 CHINA Alsea S.A.B. de C.V. 0.02 MEXICO A.G.V. Products <0.005 TAIWAN Agricultural Bank of China (H) 0.26 CHINA Altek Corp <0.005 TAIWAN Aarti Industries 0.01 INDIA Aguas Andinas S.A. A 0.03 CHILE Aluminum Corp of China (A) 0.01 CHINA ABB India 0.02 INDIA Agung Podomoro Land Tbk PT <0.005 INDONESIA Aluminum Corp of China (H) 0.03 CHINA Abdullah Al Othaim Markets <0.005 SAUDI ARABIA Ahli United Bank B.S.C. -

2020 China Car(おもて)

FOURIN entered its 31th year of operation in 2011. We sincerely appreciate your continued support over this time. China Automotive Industry Order Form for China Automotive Industy 2011 Yearbook □ Please send me hard copies of China Automotive Industy 2011 Yearbook - Automotive Parts - for - Automotive Parts - 120,000JPY (1,463USD)* each including shipping. 20201111 Yearbook ………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………… □ Please send me printable type PDF access licenses** of Moving from Growth to Maturity Stage in China, Electrification, China Automotive Industy 2011 Yearbook - Automotive Parts - for 120,000JPY (1,463USD)* each. Lightweighting as well as Cost Competitiveness Needed for Auto Parts Makers ………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………… ■Size: A4, 259 pages+CD ■Publication Date: June 29, 2011 ■Price: 120,000 JPY (free shipping but VAT for Japan orders) □ Please send me sets of China Automotive Industy 2011 Yearbook - Automotive Parts - in print and license printable type PDF access for 144,000JPY (1,756USD)* each including shipping. Invaluable Intelligence and Data to Support Any Automotive Business in China ………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………………… Please send me view-only type PDF access licenses** of □ ◆Identifies the direction of the Chinese automotive industry based on analysis of growth strategies of China's central and China Automotive -

Future International Business Strategy of Chinese Automotive Manufacturers: a Case Study on Their Overseas Operations in the Russian Market

Annals of Business Administrative Science 9 (2010) 13–32 Online ISSN 1347-4456 Print ISSN 1347-4464 Available at www.gbrc.jp ©2010 Global Business Research Center Future International Business Strategy of Chinese Automotive Manufacturers: A Case Study on Their Overseas Operations in the Russian Market Zejian LI Abstract: Since 1955, when new China began to reconstruct its automotive industry, and for a long time after, Chinese car exports consisted mainly of commercial automobile products (chassis and finished vehicles, etc.) which were exported in small quantities by state-owned manufacturers. Since 2000, however, with the emergence of independent automobile manufacturers, the number of vehicles exported has increased rapidly, and the makeup of exports has shifted gradually from a focus on commercial vehicles to a focus on passenger vehicles. With regard to overseas expansion, manufacturers’ market access strategy has led to the rapid transition from parts trade to local knock-down manufacturing. However, despite the rapid progress of foreign expansion, problems have arisen due to insufficient risk management know-how with regard to foreign expansion on the part of independent Chinese manufacturers, and the fact that their experience acquired from domestic markets is not applicable to overseas markets. For these reasons, following a period of prosperous overseas expansion, some Chinese automobile manufacturers have been forced to withdraw from one market or have chosen to switch to another market. This entire process, from rapid prosperity -

References China Map Page 14 References China Overview Page 15

References Germany | Europe | America | Asia | China The analysis specialist for powertrain Content of the brochure References Germany Map page 3 References Germany Overview page 4 References Europe Map page 6 References Europe Overview page 8 References America Map page 10 References America Overview page 11 References Asia Map page 12 References Asia Overview page 13 References China Map page 14 References China Overview page 15 Imprint: Reproduction, copying, inclusion in online magazines and the Internet, including copies of any kind only after prior written consent of REILHOFER KG. © REILHOFER KG, Edition 2019 2 REILHOFER KG - The analysis specialist for powertrain www.rhf.de | [email protected] References Germany Hamburg Bremen Berlin Wolfsburg Hannover Osnabrück Leipzig Köln Erfurt Dresden Chemnitz Frankfurt Mainz Nürnberg Saarbrücken Stuttgart Passau München References - Germany | Europe | America | Asia | China 3 References Germany AGCO POWER AMG APL APS Aston Martin Marktoberdorf Aff alterbach Landau Stuttgart Cologne Atesteo AUDI Autovision (ZFM) AVL Bentley Wolfsburg | Alsdorf Ingolstadt | Neckarsulm Wolfsburg Bietigheim-Bissingen Wolfsburg BMTS Technology BMW BMW Motorrad BorgWarner Turbo Bosch Engineering Stuttgart Munich | Dingolfi ng | Landshut Munich Kirchheimbolanden Stuttgart BoschRexroth Bugatti Claas Continental Daimler Horb Wolfsburg Paderborn Roding | Nürnberg | Berlin Mannheim Danfoss Deutz DeVeTec Dirk Schumann ElringKlinger AG Neumünster Cologne Saarbrücken Hilgert Dettingen FEV FKFS Ford Fuchs Schmierstoff e Getrag