Published by ENPA November 2009 1 EXMOOR NATIONAL PARK

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

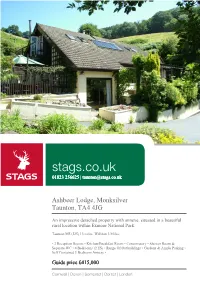

Stags.Co.Uk 01823 256625 | [email protected]

stags.co.uk 01823 256625 | [email protected] Ashbeer Lodge, Monksilver Taunton, TA4 4JG An impressive detached property with annexe, situated in a beautiful rural location within Exmoor National Park. Taunton/M5 (J25) 13 miles. Williton 3 Miles. • 2 Reception Rooms • Kitchen/Breakfast Room • Conservatory • Shower Room & Separate WC • 4 Bedrooms (2 ES) • Range Of Outbuildings • Gardens & Ample Parking • Self Contained 1 Bedroom Annexe • Guide price £415,000 Cornwall | Devon | Somerset | Dorset | London Ashbeer Lodge, Monksilver, Taunton, TA4 4JG Situation appointed family home. The accommodation is Ashbeer Lodge occupies a beautiful rural location flexible and gives the ability to utilise rooms for a within the Exmoor National Park. There are variety of uses. It is currently arranged to provide superb views from the property and the a sitting room, dining room, kitchen/breakfast surrounding countryside. The popular village of room, two ground floor bedrooms and two further Monksilver is considered by many to be one of bedrooms on the first floor. the most attractive villages in West Somerset and Accommodation has an ancient church and popular inn. A sitting room with an open fireplace and door Monksilver is located at the foot of the Brendon leads through to the dining room which inturn Hills, just within the Exmoor National Park leads through to the kitchen/breakfast room, boundary. A large range of facilities are available which is fitted with a range of modern units and in the rural town of Williton, which is about three LPG fired Rayburn providing cooking, central miles, and includes stores, supermarkets and heating and hot water. -

Nettlecombe Court Slope and Old Weather Station Field: National Vegetation Classification 2019

Nettlecombe Court Slope and Old Weather Station Field: National Vegetation Classification 2019 First published July 2021 Natural England Research Report NERR099 www.gov.uk/natural-england Nettlecombe NVC Final Report Natural England Research Report NERR099 Natural England Research Report NERR099 Nettlecombe Court Slope and Old Weather Station Field: National Vegetation Classification 2019 A.McLay July 2021 This report is published by Natural England under the Open Government Licence - OGLv3.0 for public sector information. You are encouraged to use, and reuse, information subject to certain conditions. For details of the licence visit Copyright. Natural England photographs are only available for non-commercial purposes. If any other information such as maps or data cannot be used commercially this will be made clear within the report. ISBN: 978-1-78354-770-8 © Natural England 2021 Nettlecombe Court Slope and Old Weather Station Field: National Vegetation Classification 2019 Natural England Research Report NERR099 Project details This report should be cited as: McLay, A. 2021. Nettlecombe Court Slope and Old Weather Station Field: National Vegetation Classification 2019 Natural England Research Report NERR099. Natural England. Natural England Project manager Mike Pearce Author A.McLay Keywords Nettlecombe Park, grassland survey, grassland fungi, SSSI Further information This report can be downloaded from the Natural England Access to Evidence Catalogue: http://publications.naturalengland.org.uk/ . For information on Natural England publications -

Deer Hunting with Dogs on the Quantock Hills in Somerset 2018/19 a Report by Somerset Wildlife Crime and Hounds Off

Deer Hunting With Dogs On The Quantock Hills In Somerset 2018/19 A Report by Somerset Wildlife Crime and Hounds Off HOUNDS OFF Protecting You From Hunt Trespass 1. Introduction 2 2. Background 3-4 3. Quantock Stag Hounds Fixture List 2018/19 5-6 4. National Trust 7-10 5. Forestry Commission 11-12 6. Other Landowners 13-14 7. Firearms 15-18 8. Biosecurity 19-20 9. Policing 21-24 10. Anti Social Behaviour, Threats & Assaults 25-26 11. Tracks & Rights Of Way 27-28 12. Road Safety 29-30 13. Cruelty Of Deer Hunting With Dogs 31-34 14. Public Outreach 35-36 15. How You Can Help This Campaign 37 16. Conclusions 38 17. From the Heart 39-40 Deer Hunting With Dogs On The Quantock Hills In Somerset 2018/19 A Report by Somerset Wildlife Crime and Hounds Off Closing in for the kill, 11/04/19. 1 Deer Hunting With Dogs On The Quantock Hills In Somerset 2018/19 A Report by Somerset Wildlife Crime and Hounds Off 1. Introduction 1.1 In response to requests from local residents, in August 2018 we (Somerset Wildlife Crime and Hounds Off) began a focused campaign to shine a light on modern day deer hunting with dogs. (1) 1.2 Throughout the 2018/19 hunting season the Quantock Stag Hounds (QSH) chased red deer with pairs of dogs plus the eyes, ears, binoculars, mobile phones and two-way radios of their supporters on horseback, motorbikes, quadbikes, four-wheel drives and on foot. 1.3 Deer were killed by running them to exhaustion and then shooting from close range. -

Exmoor Bars & Pubs

22 23 21 28 26 24 27 Bus: 309/310 25 13 15 Bus: 28/198/WSR 10 Lynton 6 36 14 11 20 2 18 1 38 Porlock 12 Bus: 309/310 Bus: 10 34 35 33 Minehead 32 47 Dunster Watchet Blackmoor Gate Bus: 28/198/WSR 5 44 41 Wheddon Cross 39 Simonsbath 19 Exford 29 16 Bratton Fleming 17 Bus: 198 46 48 45 37 Exmoor Brayford 4 40 42 Bars & 3 43 8 9 30 31 Dulverton Pubs 7 Bus: 25/198/398 49 Design: Edible Exmoor | www.edibleexmoor.co.uk 1. Barbrook Exmoor Manor Hotel & 14. Dunster Stags Head Inn 27. Lynton The Sandrock 43. Upton Lowtrow Cross Inn Beggars Roost Inn 15. Dunster Yarn Market Hotel 28. Lynton Bay Valley Of Rocks Hotel 44. Wheddon Cross Rest & Be Thankful Inn 2. Brendon The Staghunters Inn 16. Exford Crown Hotel 29. Monksilver Notley Arms Inn 45. Winsford The Royal Oak 30. Molland The London Inn 46. Withypool Royal Oak 3. Brompton Regis The George Inn 17. Exford Exmoor White Horse Inn 31. Molland Blackcock 47. Wooton Courtenay Dunkery Beacon Country Badgers Holt 18. Heddons Mouth The Hunters Inn 4. Bridgetown 32. Parracombe The Fox & Goose House Hotel. 5. Challacombe The Black Venus Inn 19. Luxborough Royal Oak Inn 33. Porlock The Castle 48. Yarde Down The Poltimore Arms 6. Countisbury The Blue Ball Inn 20. Lynbridge Cottage Inn Nartnapa Thai 34. Porlock The Royal Oak 49. Yeo Mill Jubilee Inn 7. Dulverton The Bridge Inn Kitchen, Thai Restaurant 35. Porlock The Ship Inn (Top Ship) Buses pass locations in Red. -

Topic Paper 1: Brief Assessment of Settlement Strategy Options January 2020

Local Plan 2040 - Issues and Options - Topic Paper 1 January 2020 LOCAL PLAN 2040 Topic Paper 1: Brief Assessment of Settlement Strategy Options January 2020 Prepared by: Stuart Todd BA (Hons), Dip.TRP, MRTPI Director, Stuart Todd Associates Ltd. 26th September, 2019 Local Plan 2040 - Issues and Options - Topic Paper 1 January 2020 This page is left intentionally blank Local Plan 2040 - Issues and Options - Topic Paper 1 January 2020 Contents 1. Introduction and Brief ................................................................................................................................................................................................................................................................. 2 2. Method ........................................................................................................................................................................................................................................................................................ 2 Assumptions and Caveats ................................................................................................................................................................................................................................................................. 3 3. National Policy and Reasons for Consideration of Options ....................................................................................................................................................................................................... -

Social Care and Support for Adults the Somerset Directory 2016/17

Social Care and Support for Adults The Somerset Directory 2016/17 Sunset at Berrow The comprehensive guide to choosing and paying for care and support Community support • care at home • care homes • specialist care For adults of working age, older people who have disabilities, mental health conditions, a sensory loss or general frailty. Publications Also available electronically at www.carechoices.co.uk and in spoken word through Browsealoud In association with www.carechoices.co.uk www.somerset.gov.uk Untitled-1 1 19/04/2016 10:55 Contents Welcome from Somerset County Council 4 How can Somerset County Council help you? 45-47 Regions covered by this Directory 4 Needs assessments 45 How can this Directory help? 5 Care eligibility 46 What is the difference between care and support? 5 Reablement 46 Where do I start? 5-8 Occupational therapy assessment 47 Help and advice 6 Paying for care 47-53 Independent advice and support 6 Financial eligibility 47 Wellbeing 7 Paying for home care 48 Writing your support plan 8 Paying for care homes 50 Help for carers 9-11 Third party payments 50 Compass Carers – the carers’ support service for What happens to your home? 51 Somerset 9 Running out of money 51 Carers’ assessments 9 NHS Continuing Healthcare 52 Carers’ information, support and counselling 10 Support for people who lack capacity 52 Health and wellbeing 11-13 Specialist care 53-55 Staying safe from falls 12 Dementia care 53 The Silver Line 13 Residential dementia care checklist 54 Mental health 55 Support in the community 13-23 Learning disability -

'Off-The-Beaten Track' Sightseeing Tour of Central Exmoor

‘Off-the-Beaten Track’ Sightseeing Tour of Central Exmoor Central Tour of Sightseeing Track’ ‘Off-the-Beaten B G F C E D A N H L M I J K G Places of interest along the route Overlay of route This map is intended as a guide only. © Exmoor National Park Authority Circular drive around central Exmoor This drive through the beautiful scenery of Exmoor, is designed to give you an ‘off-the-beaten-track’ sightseeing tour with plenty to do along the way. It includes small single-track roads which have passing places and a picturesque toll road. The information starts at Porlock, but you can pick up the route anywhere along it, depending on where you are staying. Places of interest are listed and numbered in the order you reach them going anti-clockwise around the route, which is the recommended direction to follow. Remember to take your binoculars with you, as you have a good chance of seeing red deer herds on this route, as well as Exmoor ponies. Distance: about 36 miles Duration, including stops: all day. Please note: This route is not suitable for larger vehicles. Main towns and villages visited Porlock, Porlock Weir, Oare, Brendon, Rockford, Simonsbath, Exford, Stoke Pero, Cloutsham, Horner. Places of interest along the way A. Porlock – Doverhay Manor Museum, St Dubricius church, Greencombe Gardens B. Porlock Weir (off route) – harbour, boat museum, Exmoor Glass, Porlock Marsh, Culbone church C. Toll road through ancient woodlands D. Oare church (Lorna Doone story) E. Malmsmead – Doone valley, tea rooms, old pack horse bridge, walks F. -

Minutes of a Meeting Held at 7Pm on Monday 16Th September 2019 at Washford Memorial Hall

OLD CLEEVE PARISH COUNCIL Minutes of a Meeting held at 7pm on Monday 16th September 2019 At Washford Memorial Hall Agenda Item Action Present Present: Cllr Williams, (Chair), Cllr Gannon (Vice-Chair), Cllr Duncan, Cllr Smith, Cllr Searle, Cllr Webb, Cllr Binding, Cllr Johnson-Smith from 7.05, Cllr Duncuff-Hoad from 7.05, Cllr Baker from 7.20pm In Attendance: Cllr Lawrence, Cllr Kravis from 7.45pm Also in attendance – Mrs S. Penny 807/0919 Apologies: Apologies and Cllr Eggar, Cllr Hunt, Cllr Pilkington, Cllr Lillis, Cllr Gaskin Declarations of Declarations of Interest: Interest Cllr Gannon – planning application 3/26/19/019 Cllr Smith – Cleeve Park and Blue Anchor Toilets Cllr Williams – Blue Anchor Toilets 808/0919 Minutes of the meeting of August 19th 2019 to be approved: Minutes of the Proposed: Cllr Searle Seconded: Cllr Duncan last meeting – It was resolved unanimously that the minutes of the meeting held on Monday 19th August 2019 be accepted as a true and accurate record. 809/0919 Co-option of Councillor: Councillor An application had been received for the Casual Vacancy from Stephanie Penny. Vacancy Following a presentation by Mrs Penny it was proposed to co-opt Mrs Penny to the Council Proposed: Cllr Webb Seconded: Cllr Smith resolved unanimously 810/0919 The Chair summarised activities undertaken since the August 2019 meeting: Chairs Report • An article was submitted to the Parish magazine which included the following items: o Article 4 Cleeve Park o Calling in planning applications o Salt & grit provision o Hedgerows overhanging -

January-February 2021

Page 1 Issue No. 127 Village News January - February 2021 Monkton Heathfield, West Monkton and Bathpool Getting Up-Close and Personal with a Wooly Mamoth See Page 8 Contents: Useful Numbers/Regular Bookings - Page 2 Somerset Birds - Page 3 Broomsquires - Page 4 & 5 South Quantock Benefice - Page 6 Bishop Peter/Bathpool Chapel/100 Club - Page 7 School News - Page 8 Oak Partnership/Gardening Corner - Page 9 Find out more about Carrion Crows Parish Council - Pages 10 & 11 See Page 3 WI Walks - Page 12 Sports Pitches - Page 13 Happy New Year Memories of Hestercombe - Page 14 from Hestercombe Cont/Village Hall - Page 15 all of us at the Village News WM&CF Film Club/Blood Donations/Debt Help/Walking Football - Page 16 Taunton Scrubbers/And Finally - Page 24 Publication in the Village News does not imply an endorsement. The Editors cannot be held responsible for any errors or omissions. The information contained within this publication is published in good faith. Volunteers deliver this publication to homes in West Monkton, Monkton Heathfield, Bathpool, Gotton and Goosenford. Copy deadline for March - April 2021 is 1st February 2021 Page 2 Useful Names and Telephone Numbers Regular Events at West Monkton Village Hall Monkton Heathfield, TA2 8NE Rector: Rev. Mary Styles - 01823 451189 The Vicarage, Kingston St Mary, TA2 8HW Slimming World Associate Vicar half-time: Rev Jim Cox - 01823 333377 Mondays 09:00 - 11:00 Churchwarden: Hazel Adams - 01823 443027 Phoenix Camera Club P.C.C Secretary: Samm Barge - 07976415337 Mondays 19:00 - 22:00 P.C.C -

South West River Basin District Flood Risk Management Plan 2015 to 2021 Habitats Regulation Assessment

South West river basin district Flood Risk Management Plan 2015 to 2021 Habitats Regulation Assessment March 2016 Executive summary The Flood Risk Management Plan (FRMP) for the South West River Basin District (RBD) provides an overview of the range of flood risks from different sources across the 9 catchments of the RBD. The RBD catchments are defined in the River Basin Management Plan (RBMP) and based on the natural configuration of bodies of water (rivers, estuaries, lakes etc.). The FRMP provides a range of objectives and programmes of measures identified to address risks from all flood sources. These are drawn from the many risk management authority plans already in place but also include a range of further strategic developments for the FRMP ‘cycle’ period of 2015 to 2021. The total numbers of measures for the South West RBD FRMP are reported under the following types of flood management action: Types of flood management measures % of RBD measures Prevention – e.g. land use policy, relocating people at risk etc. 21 % Protection – e.g. various forms of asset or property-based protection 54% Preparedness – e.g. awareness raising, forecasting and warnings 21% Recovery and review – e.g. the ‘after care’ from flood events 1% Other – any actions not able to be categorised yet 3% The purpose of the HRA is to report on the likely effects of the FRMP on the network of sites that are internationally designated for nature conservation (European sites), and the HRA has been carried out at the level of detail of the plan. Many measures do not have any expected physical effects on the ground, and have been screened out of consideration including most of the measures under the categories of Prevention, Preparedness, Recovery and Review. -

Der Europäischen Gemeinschaften Nr

26 . 3 . 84 Amtsblatt der Europäischen Gemeinschaften Nr . L 82 / 67 RICHTLINIE DES RATES vom 28 . Februar 1984 betreffend das Gemeinschaftsverzeichnis der benachteiligten landwirtschaftlichen Gebiete im Sinne der Richtlinie 75 /268 / EWG ( Vereinigtes Königreich ) ( 84 / 169 / EWG ) DER RAT DER EUROPAISCHEN GEMEINSCHAFTEN — Folgende Indexzahlen über schwach ertragsfähige Böden gemäß Artikel 3 Absatz 4 Buchstabe a ) der Richtlinie 75 / 268 / EWG wurden bei der Bestimmung gestützt auf den Vertrag zur Gründung der Euro jeder der betreffenden Zonen zugrunde gelegt : über päischen Wirtschaftsgemeinschaft , 70 % liegender Anteil des Grünlandes an der landwirt schaftlichen Nutzfläche , Besatzdichte unter 1 Groß vieheinheit ( GVE ) je Hektar Futterfläche und nicht über gestützt auf die Richtlinie 75 / 268 / EWG des Rates vom 65 % des nationalen Durchschnitts liegende Pachten . 28 . April 1975 über die Landwirtschaft in Berggebieten und in bestimmten benachteiligten Gebieten ( J ), zuletzt geändert durch die Richtlinie 82 / 786 / EWG ( 2 ), insbe Die deutlich hinter dem Durchschnitt zurückbleibenden sondere auf Artikel 2 Absatz 2 , Wirtschaftsergebnisse der Betriebe im Sinne von Arti kel 3 Absatz 4 Buchstabe b ) der Richtlinie 75 / 268 / EWG wurden durch die Tatsache belegt , daß das auf Vorschlag der Kommission , Arbeitseinkommen 80 % des nationalen Durchschnitts nicht übersteigt . nach Stellungnahme des Europäischen Parlaments ( 3 ), Zur Feststellung der in Artikel 3 Absatz 4 Buchstabe c ) der Richtlinie 75 / 268 / EWG genannten geringen Bevöl in Erwägung nachstehender Gründe : kerungsdichte wurde die Tatsache zugrunde gelegt, daß die Bevölkerungsdichte unter Ausschluß der Bevölke In der Richtlinie 75 / 276 / EWG ( 4 ) werden die Gebiete rung von Städten und Industriegebieten nicht über 55 Einwohner je qkm liegt ; die entsprechenden Durch des Vereinigten Königreichs bezeichnet , die in dem schnittszahlen für das Vereinigte Königreich und die Gemeinschaftsverzeichnis der benachteiligten Gebiete Gemeinschaft liegen bei 229 beziehungsweise 163 . -

WS SHLAA 2020 Appendix E Developable Sites

WEST SOMERSET STRATEGIC HOUSING LAND AVAILABILITY ASSESSMENT Developable Sites Appendix E Please note: All the sites submitted in between 2016 and 2020 were subjected to a full site assessment as outlined in the Stage 2 of the Methodology, this determined whether the site was deemed deliverable, developable or non-developable. The assessment sheets are included alongside a location map for each deliverable and developable site in the following chapters. Any sites that were carried forward to this 2020 publication from the previous SHLAA have not been reassessed in such detail as they were subject to a similar process when they were first submitted. Their assessment tables have been updated to take account of the latest definitions of deliverable and developable in the February 2019 NPPF and reflect any relevant information update provided by the landowner. SHLAA Criteria 2019 2015 Address Suitable Size (ha) & 2020 SHLAA Site Ref. Site Ref. Capacity Status (No. of dwellings) MHD2 MIN23 land at rear and to the west of Chestnut Way, Yes 2.75 Developable Alcombe, Minehead TA24 6EB Planning & Sustainability Criteria Location Access & Retail Health Social & Education Comments Public Transport Outside No direct access Post Office: Surgery – V. Hall: 0.5M/0.8Km - adjoins existing built-up Greenfield to the public road 400m 0.9M/1.5Km 1st School 0.9M/1.5Km area of settlement system Super-mkt: Hospital – Mid. School 0.5M/0.8Km - possible restrictive 400m 1.4M/2.2Km WS College 0.7M/1.1Km covenants None - southern part within bat foraging zone (see HRA) - access issues to road network - part of strategic site allocation SHLAA Criteria 2019 2015 Address Suitable Size (ha) & 2020 SHLAA Site Ref.