Asset Tracing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Texas Constructive Trust and Its Peculiar Requirements

Digital Commons at St. Mary's University Faculty Articles School of Law Faculty Scholarship Spring 2018 The Texas Constructive Trust and Its Peculiar Requirements David Dittfurth St. Mary's University School of Law, [email protected] Follow this and additional works at: https://commons.stmarytx.edu/facarticles Part of the Estates and Trusts Commons Recommended Citation David Dittfurth, The Texas Constructive Trust and Its Peculiar Requirements, 50 Tex. Tech L. Rev. 447 (2018). This Article is brought to you for free and open access by the School of Law Faculty Scholarship at Digital Commons at St. Mary's University. It has been accepted for inclusion in Faculty Articles by an authorized administrator of Digital Commons at St. Mary's University. For more information, please contact [email protected]. THE TEXAS CONSTRUCTIVE TRUST AND ITS PECULIAR REQUIREMENTS David Dittfurth" I. INTRODUCTION ........................................ 447 II. THESIS .............................................. 448 III. CONSTRUCTIVE TRUST MECHANICS ........................ 451 A . JudicialR em edy ........................................................................ 451 B. Statutory Rem edies ................................................................... 452 IV. THE THREE-ELEMENT RULE ........................................................... 454 A. KCM Financial, LLC v. Bradshaw...................454 B . K insel v. L indsey ...................................................................... 458 V. THE FUNCTION OF WRONGDOING.................................................. -

The Restitution Revival and the Ghosts of Equity

The Restitution Revival and the Ghosts of Equity Caprice L. Roberts∗ Abstract A restitution revival is underway. Restitution and unjust enrichment theory, born in the United States, fell out of favor here while surging in Commonwealth countries and beyond. The American Law Institute’s (ALI) Restatement (Third) of Restitution & Unjust Enrichment streamlines the law of unjust enrichment in a language the modern American lawyer can understand, but it may encounter unintended problems from the law-equity distinction. Restitution is often misinterpreted as always equitable given its focus on fairness. This blurs decision making on the constitutional right to a jury trial, which "preserves" the right to a jury in federal and state cases for "suits at common law" satisfying specified dollar amounts. Restitution originated in law, equity, and sometimes both. The Restatement notably attempts to untangle restitution from the law-equity labels, as well as natural justice roots. It explicitly eschews equity’s irreparable injury prerequisite, which historically commanded that no equitable remedy would lie if an adequate legal remedy existed. Can restitution law resist hearing equity’s call from the grave? Will it avoid the pitfalls of the Supreme Court’s recent injunction cases that return to historical, equitable principles and reanimate equity’s irreparable injury rule? Losing anachronistic, procedural remedy barriers is welcome, but ∗ Professor of Law, West Virginia University College of Law; Visiting Professor of Law, The Catholic University of America Columbus School of Law. Washington & Lee University School of Law, J.D.; Rhodes College, B.A. Sincere thanks to Catholic University for supporting this research and to the following conferences for opportunities to present this work: the American Association of Law Schools, the Sixth Annual International Conference on Contracts at Stetson University College of Law, and the Restitution Rollout Symposium at Washington and Lee University School of Law. -

Beyond Unconscionability: the Case for Using "Knowing Assent" As the Basis for Analyzing Unbargained-For Terms in Standard Form Contracts

Beyond Unconscionability: The Case for Using "Knowing Assent" as the Basis for Analyzing Unbargained-for Terms in Standard Form Contracts Edith R. Warkentinet I. INTRODUCTION People who sign standard form contracts' rarely read them.2 Coun- sel for one party (or one industry) generally prepare standard form con- tracts for repetitive use in consecutive transactions.3 The party who has t Professor of Law, Western State University College of Law, Fullerton, California. The author thanks Western State for its generous research support, Western State colleague Professor Phil Merkel for his willingness to read this on two different occasions and his terrifically helpful com- ments, Whittier Law School Professor Patricia Leary for her insightful comments, and Professor Andrea Funk for help with early drafts. 1. Friedrich Kessler, in a pioneering work on contracts of adhesion, described the origins of standard form contracts: "The development of large scale enterprise with its mass production and mass distribution made a new type of contract inevitable-the standardized mass contract. A stan- dardized contract, once its contents have been formulated by a business firm, is used in every bar- gain dealing with the same product or service .... " Friedrich Kessler, Contracts of Adhesion- Some Thoughts About Freedom of Contract, 43 COLUM. L. REV. 628, 631-32 (1943). 2. Professor Woodward offers an excellent explanation: Real assent to any given term in a form contract, including a merger clause, depends on how "rational" it is for the non-drafter (consumer and non-consumer alike) to attempt to understand what is in the form. This, in turn, is primarily a function of two observable facts: (1) the complexity and obscurity of the term in question and (2) the size of the un- derlying transaction. -

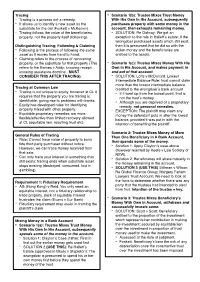

Tracing Is a Process Not a Remedy

Tracing - Scenario 1(b): Trustee Mixes Trust Money - Tracing is a process not a remedy. With His Own In His Account, subsequently - It allows us to identify a new asset as the purchases property with some money in the substitute for the old (Foskett v McKeown). account, then exhausts remaining money. - Tracing follows the value of the beneficiaries - SOLUTION: Re Oatway: We get an property, not the property itself (following). exception to the rule in Hallett’s estate: if the wrongdoer purchased assets which still exist, Distinguishing Tracing; Following & Claiming then it is presumed that he did so with the - Following is the process of following the same stolen money and the beneficiaries are asset as it moves from hand to hand. entitled to the assets. - Claiming refers to the process of recovering property, or the substitute for that property (This - Scenario 1(c): Trustee Mixes Money With His refers to the Barnes v Addy; knowing receipt, Own In His Account, and makes payment in knowing assistance doctrine - MUST and out of that account. CONSIDER THIS AFTER TRACING). - SOLUTION: Lofts v McDonald: Lowest Intermediate Balance Rule: trust cannot claim more than the lowest intermediate balance Tracing at Common Law - credited to the wrongdoer’s bank account Tracing is not unique to equity, however at CL it - If it went up from the lowest point, that is requires that the property you are tracing is not the trust’s money. identifiable, giving rise to problems with banks. - - Although you are deprived of a proprietary Equity has developed rules for identifying remedy, not personal remedies. -

Supreme Court of the United States ————

No. 19-508 IN THE Supreme Court of the United States ———— AMG CAPITAL MANAGEMENT, LLC, ET AL., Petitioners, v. FEDERAL TRADE COMMISSION, Respondent. ———— On Writ of Certiorari to the United States Court of Appeals for the Ninth Circuit ———— REPLY BRIEF FOR PETITIONERS ———— PAUL C. RAY JEFFREY A. LAMKEN PAUL C. RAY, CHTD Counsel of Record 8670 West Cheyenne Ave. MICHAEL G. PATTILLO, JR. Suite 120 SARAH J. NEWMAN Las Vegas, NV 89129 MOLOLAMKEN LLP (702) 823-2292 The Watergate, Suite 500 [email protected] 600 New Hampshire Ave., N.W. Washington, D.C. 20037 (202) 556-2000 [email protected] Counsel for Petitioners (Additional Counsel Listed on Inside Cover) WILSON-EPES PRINTING CO., INC. – (202) 789-0096 – WASHINGTON, D.C. 20002 JENNIFER E. FISCHELL MOLOLAMKEN LLP 430 Park Ave. New York, NY 10022 (212) 607-8160 MATTHEW J. FISHER MOLOLAMKEN LLP 300 N. LaSalle St. Chicago, IL 60654 (312) 450-6700 Counsel for Petitioners TABLE OF CONTENTS Page Introduction ................................................................ 1 Argument .................................................................... 3 I. Section 13(b) Does Not Authorize Monetary Relief .............................................. 3 A. The Term “Permanent Injunction” Does Not Encompass Retrospective Monetary Relief Like Restitution .......... 3 B. Equity Courts’ Ancillary Jurisdiction Does Not Expand § 13(b)’s Scope ........................................... 7 1. Equity’s Power To Award “Complete Relief” Cannot Expand the Commission’s § 13(b) Authority ................................. 8 2. Early Patent and Copyright Cases Do Not Support Expanding § 13(b) ............................... 12 C. The Commission’s Reading of § 13(b) Defies the FTC Act’s Structure and History .............................. 14 D. Precedent Requires Adhering to § 13(b)’s Text ............................................. 20 E. Policy Arguments Are Properly Addressed to Congress ........................... -

Asset Tracing in the British Virgin Islands

Article Asset Tracing in the British Virgin Islands In this article, we will discuss some of the tools available to a party in the British Virgin Islands to seek to recover property, or proceeds of property, which have been misappropriated. It is not surprising that in some cases, the identity of the wrongdoer or the whereabouts of the misappropriated property is unknown. Against that background, it is worth noting that while a BVI, and whether there has been any past judgment which company incorporated in the BVI is required to maintain may shed light on assets held by the company. In addition, certain records at the office of its registered agent (such as upon application the BVI Land Registry can provide certain its memorandum and articles of association, register of details regarding the owner of BVI land or real estate. directors, register of members, minutes of members’ and However, this requires the applicant to first be able to directors’ meetings and copies of resolutions), there is no identify the location or owner of the land. A party may also right for the public to inspect such records. Indeed, obtain certain information regarding vessels registered under confidentiality of corporate documents and information is a BVI flag from the BVI Ship Registry. one of the key attractions of incorporating a company in the BVI. BVI companies are not generally required to maintain or What is “tracing”? file statutory accounts, or meet any particular set of international accounting standards. Under section 98 of the Tracing consists of a series of rules developed by equity to BVI Business Companies Act 2004, all that a company is deal with situations where assets have been required to maintain are records “sufficient to show and misappropriated and the wrongdoer is not in a position to explain the company’s transactions” and which “will, at any compensate, or money compensation is not adequate. -

Asset Tracing and Recovery Reassessed

Asset tracing and recovery reassessed Nicole Sandells QC Miles Harris 4 New Square Professional Liability & Regulatory Conference 4 February 2020 This material was provided for the 4 New Square Professional Liability & Regulatory Conference on 4 February 2020. It was not intended for use and must not be relied upon in relation to any particular matter and does not constitute legal advice. It has now been provided without responsibility by its authors. 4 NEW SQUARE T: +44 (0) 207 822 2000 LINCOLN’S INN F: +44 (0) 207 822 2001 LONDON WC2A 3RJ DX: LDE 1041 WWW.4NEWSQUARE.COM E: [email protected] Nicole Sandells QC Call: 1994 Silk: 2018 Nicole's practice in recent years has focused heavily on financial and property law, civil fraud, restitution, trusts, probate and equitable remedies alongside Chambers' mainstream professional indemnity work. She has significant experience of unjust enrichment, subrogation, breach of trust and fiduciary duty claims. She is never happier than when finding novel answers to tricky problems. Nicole is described as ‘a mega-brain, with encyclopaedic legal knowledge and the ability to cut through complex legal issues with ease’ and 'a master tactician who is exceptionally bright and has a fantastic ability to condense significant evidential information' (Legal 500). Apparently, she is also “exceptionally bright and a ferocious advocate. She gives tactical advice and is a pleasure to work with. Clients speak extremely highly of her.” “If you want someone to think outside of the box and really come up with an innovative position, then she’s an excellent choice.” – Chambers & Partners, 2020 Professional Negligence. -

PATRICK DURKIN V. MTOWN CONSTRUCTION, LLC

03/13/2018 IN THE COURT OF APPEALS OF TENNESSEE AT JACKSON Assigned on Briefs February 2, 2018 PATRICK DURKIN v. MTOWN CONSTRUCTION, LLC Direct Appeal from the Circuit Court for Shelby County No. CT-004623-16 Rhynette N. Hurd, Judge No. W2017-01269-COA-R3-CV This appeal involves a homeowner’s lawsuit against a construction company for breach of contract and negligence. After a bench trial, the trial court entered judgment for the homeowner for $135,383.93 and denied a counterclaim filed by the construction company for the balance of the contract price. The construction company appeals, arguing that the trial court erred in its calculation of damages and in denying the counterclaim. We affirm in part, reverse in part, and remand for further proceedings. Tenn. R. App. P. 3 Appeal as of Right; Judgment of the Circuit Court Affirmed in part, Reversed in part, and Remanded BRANDON O. GIBSON, J., delivered the opinion of the court, in which CHARLES D. SUSANO and RICHARD H. DINKINS, JJ., joined. Christopher M. Myatt, Memphis, Tennessee, for the appellant, MTown Construction, LLC. Lewis Clayton Culpepper, III, Memphis, Tennessee, for the appellee, Patrick Durkin. OPINION I. FACTS & PROCEDURAL HISTORY Patrick Durkin purchased a home in a historic neighborhood in Memphis in 2015. In 2016, Mr. Durkin entered into a written contract with MTown Construction, LLC, for the replacement of his roof. The work began on August 25, 2016. After workers removed about three quarters of the existing shingles, rain began falling. The rain quickly developed into a thunderstorm and “a complete downpour.” MTown workers attempted to cover the exposed roof with tarps, but the tarps contained holes and did not adequately protect the home. -

A Commonwealth of Perspective on Restitutionary Disgorgement for Breach of Contract

A Commonwealth of Perspective on Restitutionary Disgorgement for Breach of Contract Caprice L. Roberts Table of Contents I. Introduction: Contractual Disgorgement Remedy as Watershed.....................................................................................946 II. Section 39 of the Pending American Restatement of Restitution ....................................................................................950 III. Comparative Roots & Flaws of Section 39’s Proposed Disgorgement Remedy .................................................................953 A. Blake’s Resonance and Other Signposts of Commonwealth Support ........................................................954 B. Section 39’s Adoption of Blake’s Remedial Theory but with Narrow Application .................................................961 C. Lessons of Blake & Practical Flaws of Section 39.................965 1. Section 39’s Potential May Be Lost for Its Cumbersome Nature........................................................965 2. Section 39 Asserts Its Narrowness, but to What End?......................................................................966 IV. Intellectual Godparents to Section 39...........................................967 Professor of Law, West Virginia University. The author is indebted to Andrew Kull for graciously accepting criticism of the pending American Restatement provision on disgorgement, providing substantive feedback, and provoking my continued interest in assisting with the artful navigation of drafting this important contractual -

Principles of Tracing

Principles of Tracing Presented at Trial Lawyers Association of B.C. – Making Equity Work in Your Practice June 10, 2021 Dan Parlow Partner, Kornfeld LLP I. Introduction ............................................................................................................................ 1 II. Tracing ancillary to other causes of action ................................................................................ 2 A. Constructive trusts .................................................................................................................... 2 B. Express or implied trusts ........................................................................................................... 3 C. Equitable liens, mortgages and other charges .......................................................................... 4 D. Fraudulent conveyances and preferences ................................................................................ 5 III. When tracing is possible .......................................................................................................... 6 IV. Tracing by competing claimants of properties fraudulently conveyed ....................................... 7 V. Competing claims to a common fund or property ..................................................................... 9 VI. Extending remedy to assets not directly traceable .................................................................. 14 VII. Adequacy of pleadings .......................................................................................................... -

Thomas, Et Al. V. Othman, Et

IN THE COURT OF APPEALS FIRST APPELLATE DISTRICT OF OHIO HAMILTON COUNTY, OHIO RICHARD THOMAS, : APPEAL NO. C-160827 TRIAL NO. A-1601001 and : GAIL THOMAS, : O P I N I O N. Plaintiffs-Appellants, : vs. : AKRAM OTHMAN, : and : MARK WOEHLER, : Defendants-Appellees. : Civil Appeal From: Hamilton County Court of Common Pleas Judgment Appealed from is: Affirmed Date of Judgment Entry on Appeal: November 8, 2017 William Flax, for Plaintiffs-Appellants, James R. Hartke, for Defendant-Appellee Akram Othman, George M. Parker, for Defendant-Appellee Mark Woehler. OHIO FIRST DISTRICT COURT OF APPEALS CUNNINGHAM, Presiding Judge. {¶1} Plaintiffs-appellants Richard and Gail Thomas appeal from the judgment of the Hamilton County Court of Common Pleas granting the motion of defendants-appellees Akram Othman and Mark Woehler to dismiss the amended complaint for failure to state a claim upon which relief could be granted, pursuant to Civ.R. 12(B)(6). For the reasons that follow, we affirm. I. Background Facts and Procedure {¶2} This appeal arises from the Thomases’ efforts to recover from Othman and Woehler a portion of the retirement funds the Thomases lost after investing them in a Ponzi scheme operated by Glen Galemmo. According to the allegations in the amended complaint, Galemmo was convicted of securities fraud in the case United States v. Galemmo, Case No. 1:13-CR-00141, for operating a “complex,” multi-year “Ponzi scheme.” The Thomases, Othman, and Woehler were all investors in the scheme, and are all members of the plaintiff class of “Net Losers” investors— investors who lost more than their principal investment—in several civil class-action lawsuits which were referenced in the Thomases’ complaint. -

Unconscionability As a Sword: the Case for an Affirmative Cause of Action

Unconscionability as a Sword: The Case for an Affirmative Cause of Action Brady Williams* Consumers are drowning in a sea of one-sided fine print. To combat contractual overreach, consumers need an arsenal of effective remedies. To that end, the doctrine of unconscionability provides a crucial defense against the inequities of rigid contract enforcement. However, the prevailing view that unconscionability operates merely as a “shield” and not a “sword” leaves countless victims of oppressive contracts unable to assert the doctrine as an affirmative claim. This crippling interpretation betrays unconscionability’s equitable roots and absolves merchants who have already obtained their ill-gotten gains. But this need not be so. Using California consumer credit law as a backdrop, this Note argues that the doctrine of unconscionability must be recrafted into an offensive sword that provides affirmative relief to victims of unconscionable contracts. While some consumers may already assert unconscionability under California’s Consumers Legal Remedies Act, courts have narrowly construed the Act to exempt many forms of consumer credit. As a result, thousands of debtors have remained powerless to challenge their credit terms as unconscionable unless first sued by a creditor. However, this Note explains how a recent landmark ruling by the California Supreme Court has confirmed a novel legal theory that broadly empowers consumers—including debtors—to assert unconscionability under the State’s Unfair Competition Law. Finally, this Note argues that unconscionability’s historical roots in courts of equity—as well as its treatment by the DOI: https://doi.org/10.15779/Z382B8VC3W Copyright © 2019 California Law Review, Inc. California Law Review, Inc.