Asset Tracing and Recovery Reassessed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MARSHALLING SECURITIES and WORDS of RELEASE

MARSHALLING SECURITIES and WORDS OF RELEASE Note on Hill v Love (2018) 53 V.R. 459 and Burness v Hill [2019] VSCA 94 © D.G. Robertson, Q.C., B.A., LL.M., M.C.I.Arb. Queen’s Counsel Victorian Bar 205 William Street, Melbourne Ph: 9225 7666 | Fax: 9225 8450 www.howellslistbarristers.com.au [email protected] -2- Table of Contents 1. The Doctrine of Marshalling 3 2. The Facts in Hill v Love 5 2.1 Facts Relevant to Marshalling 5 2.2 Facts Relevant to the Words of Release Issue 6 3. The Right to Marshal 7 4. Limitations on and Justification of Marshalling 9 4.1 Principle 9 4.2 Arrangement as to Order of Realization of Securities 10 5. What is Secured by Marshalling? 11 5.1 Value of the Security Property 11 5.2 Liabilities at Time of Realization of Prior Security 12 5.3 Interest and Costs 14 6. Uncertainties in Marshalling 15 6.1 Nature of Marshalling Right 15 6.2 Caveatable Interest? 17 6.3 Proprietary Obligations 18 7. Construction of Words of Release 19 7.1 General Approach to the Construction of Contracts 19 7.2 Special Rules for the Construction of Releases 20 7.3 Grant v John Grant & Sons Pty. Ltd. 22 8. Other Points 24 8.1 Reasonable Security 24 8.2 Fiduciary Duty 24 8.3 Anshun Estoppel 25 This paper was presented on 18 September 2019 at the Law Institute of Victoria to the Commercial Litigation Specialist Study Group. Revised 4 December 2019. -3- MARSHALLING SECURITIES and WORDS OF RELEASE The decisions of the Supreme Court of Victoria in Hill v Love1 and, on appeal, Burness v Hill2 address the doctrine of marshalling securities and also the construction of words of release in terms of settlement. -

"After the Guarantor Pays: the Uncertain Equitable Doctrines Of

AFTER THE GUARANTOR PAYS: THE UNCERTAIN EQUITABLE DOCTRINES OF REIMBURSEMENT, CONTRIBUTION, AND SUBROGATION Brian D. Hulse Author’s Synopsis: This Article addresses the equitable doctrines of reimbursement, contribution, and subrogation as they apply to guarantors and other secondary obligors. Specifically, it explores in detail guarantors’ and other secondary obligors’ rights after they make payment under the guaranty or other secondary obligation and then seek to recover some or all of the amount paid from the borrower, other guarantors, or the collateral for the primary obligation. This article discusses the inconsistencies in the case law on these subjects, which can create unpredictable results. It concludes that, when multiple parties are liable on a common debt, in whatever capacity, they should enter into appropriate reimbursement and contribution agreements at the outset of the transaction to avoid litigation and unpredictable outcomes. I. INTRODUCTION ....................................................................... 42 II. PRELIMINARY ISSUE: WHO IS A SURETY? .......................... 45 A. Examples of Types of Sureties ............................................ 45 B. Honey v. Davis: A Case Study ............................................ 46 III. REIMBURSEMENT ................................................................... 50 A. When Does the Right to Reimbursement Arise? ................. 50 B. How Much is the Guarantor Entitled to be Reimbursed? .... 50 C. Effect of Release of the Borrower by the Creditor ............. -

1 Builders Risk Insurance

BUILDERS RISK INSURANCE: Utilizing Builder’s Risk Policies to Help Settle Construction Defect Cases Finding the Oasis in the Desert Gregory N. Ziegler Rebecca M. Alcantar Katherine K. Valent MACDONALD DEVIN, P.C. I. What is Builder’s Risk insurance? Builder’s risk insurance is a unique form of first-party property insurance that typically covers a structure under construction, the materials and equipment used in construction, and the removal of debris of covered property damaged by a covered loss. Builder’s risk insurance policies are typically purchased by the project general contractor or the owner. It is sometimes called “course of construction” coverage because it is only intended to apply during the course of construction, erection, and fabrication of a structure until the construction is considered completed. Coverage typically commences on the “start date” of the project and ends when the work is completed. i. Who is covered? Builder’s risk policies cover the interests of owners, contractors, subcontractors and others involved in the construction project. While contractors and subcontractors are typically covered, it’s a good idea for contractors and subcontractors to request being named insureds on the policy. In comparison, liability insurance covers damage to third parties, such as passersby injured by construction or for damage to adjoining property. ii. What does it cover? Typically, it is written on an “all risks basis” and covers direct physical loss from all causes except those specifically excluded. This does not mean it covers everything, so it is important to look at the exclusions. Although it is typically limited to the construction site, an insured can request coverage for property stored off site and in-transit. -

Beyond Unconscionability: the Case for Using "Knowing Assent" As the Basis for Analyzing Unbargained-For Terms in Standard Form Contracts

Beyond Unconscionability: The Case for Using "Knowing Assent" as the Basis for Analyzing Unbargained-for Terms in Standard Form Contracts Edith R. Warkentinet I. INTRODUCTION People who sign standard form contracts' rarely read them.2 Coun- sel for one party (or one industry) generally prepare standard form con- tracts for repetitive use in consecutive transactions.3 The party who has t Professor of Law, Western State University College of Law, Fullerton, California. The author thanks Western State for its generous research support, Western State colleague Professor Phil Merkel for his willingness to read this on two different occasions and his terrifically helpful com- ments, Whittier Law School Professor Patricia Leary for her insightful comments, and Professor Andrea Funk for help with early drafts. 1. Friedrich Kessler, in a pioneering work on contracts of adhesion, described the origins of standard form contracts: "The development of large scale enterprise with its mass production and mass distribution made a new type of contract inevitable-the standardized mass contract. A stan- dardized contract, once its contents have been formulated by a business firm, is used in every bar- gain dealing with the same product or service .... " Friedrich Kessler, Contracts of Adhesion- Some Thoughts About Freedom of Contract, 43 COLUM. L. REV. 628, 631-32 (1943). 2. Professor Woodward offers an excellent explanation: Real assent to any given term in a form contract, including a merger clause, depends on how "rational" it is for the non-drafter (consumer and non-consumer alike) to attempt to understand what is in the form. This, in turn, is primarily a function of two observable facts: (1) the complexity and obscurity of the term in question and (2) the size of the un- derlying transaction. -

Tracing Is a Process Not a Remedy

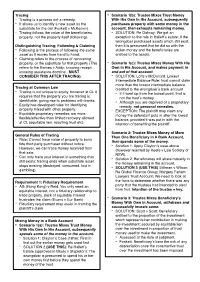

Tracing - Scenario 1(b): Trustee Mixes Trust Money - Tracing is a process not a remedy. With His Own In His Account, subsequently - It allows us to identify a new asset as the purchases property with some money in the substitute for the old (Foskett v McKeown). account, then exhausts remaining money. - Tracing follows the value of the beneficiaries - SOLUTION: Re Oatway: We get an property, not the property itself (following). exception to the rule in Hallett’s estate: if the wrongdoer purchased assets which still exist, Distinguishing Tracing; Following & Claiming then it is presumed that he did so with the - Following is the process of following the same stolen money and the beneficiaries are asset as it moves from hand to hand. entitled to the assets. - Claiming refers to the process of recovering property, or the substitute for that property (This - Scenario 1(c): Trustee Mixes Money With His refers to the Barnes v Addy; knowing receipt, Own In His Account, and makes payment in knowing assistance doctrine - MUST and out of that account. CONSIDER THIS AFTER TRACING). - SOLUTION: Lofts v McDonald: Lowest Intermediate Balance Rule: trust cannot claim more than the lowest intermediate balance Tracing at Common Law - credited to the wrongdoer’s bank account Tracing is not unique to equity, however at CL it - If it went up from the lowest point, that is requires that the property you are tracing is not the trust’s money. identifiable, giving rise to problems with banks. - - Although you are deprived of a proprietary Equity has developed rules for identifying remedy, not personal remedies. -

Circuit Court for Frederick County Case No. C-10-CV-19-000066

Circuit Court for Frederick County Case No. C-10-CV-19-000066 UNREPORTED IN THE COURT OF SPECIAL APPEALS OF MARYLAND No. 1658 September Term, 2019 ______________________________________ JP MORGAN CHASE BANK, N.A. v. TRUIST BANK, ET AL. ______________________________________ Fader, C.J., Nazarian, Shaw Geter, JJ. ______________________________________ Opinion by Fader, C.J. ______________________________________ Filed: December 17, 2020 *This is an unreported opinion, and it may not be cited in any paper, brief, motion, or other document filed in this Court or any other Maryland Court as either precedent within the rule of stare decisis or as persuasive authority. Md. Rule 1-104. — Unreported Opinion — ______________________________________________________________________________ This appeal concerns the respective priority positions of (1) a lender who refinances a home mortgage loan secured by a first-priority deed of trust on the property, and (2) an intervening home equity lender whose line of credit is secured by a deed of trust on the same property.1 Specifically, we consider whether the refinancing lender is equitably subrogated to the original home mortgage lender’s senior priority position when, in a transaction contemporaneous with the refinancing, the intervening home equity lender’s line of credit is paid down to zero but, unbeknownst to the refinancing lender, the line is not closed and the deed of trust is never released. We hold that in such circumstances the refinancing lender is equitably subrogated to the position of the original, first-priority lender if the intervening lender maintains its original priority position, is not otherwise prejudiced, and would be unjustly enriched in the absence of subrogation. -

Good Faith, Unconscionability and Reasonable Expectations S M Waddams* the Expression 'Good Faith' Makes Frequent Appearances in Contract Law

Good Faith, Unconscionability and Reasonable Expectations S M Waddams* The expression 'good faith' makes frequent appearances in contract law. The concept is firmly established in American jurisdictions because of its inclusion in the Uniform Commercial Code,1 and the Restatement of Contracts.2 It is in the new Quebec Civil Code.3 It forms an important part of many other civil law systems, and appears in a number of international documents applicable in common law jurisdictions.4 Several cases in Commonwealth jurisdictions have adopted it in various contexts.5 There has been much academic writing on good faith. English and Commonwealth writers have been divided in their opinions on whether the adoption of a general concept of good faith would be desirable.6 American writers, however, rarely discuss this question: the concept is sufficiently firmly fixed now for this to be of theoretical interest only.7 The focus of American writing is on what meaning should be given to the expression, and how it applies in different contexts. On a question of this sort, where the law is in many jurisdictions apparently in the process of change, two levels of analysis are necessary. It is of interest to examine the probable effect and utility of adopting, in English and Commonwealth law, a general doctrine of good faith. This process involves the identification of problems likely to be caused by the doctrine. It is of theoretical as well as of practical interest, and might well tend to suggest caution on the part of law reformers, legislative, judicial, and academic. But since the concept of good faith has found favour in several jurisdictions where it is unlikely to be decisively rejected, an equally important function of analysis is to suggest ways in which the problems of integrating good faith with other contractual concepts can be minimised. -

Practical and Substantive Aspects of Subrogation

PRACTICAL AND SUBSTANTIVE ASPECTS OF SUBROGATION Eric A. Dolden and Dan C. Richardson September 2015 [Author] © Dolden Wallace Folick LLP 1 CONTACT LAWYER Eric Dolden Dan Richardson 604.891.0350 604.891.5251 [email protected] [email protected] TABLE OF CONTENTS I. INTRODUCTORY COMMENTS ....................................................................................4 II. STATUTORY AND CONTRACTUAL PROVISIONS RECOGNIZING THE RIGHT OF SUBROGATION ....................................................6 1. Statutory Right of Subrogation ...........................................................................6 2. Contractual Right of Subrogation .......................................................................8 III. PROHIBITIONS ON SUBROGATION ........................................................................11 1. The Insurer As “Volunteer” ..............................................................................11 2. Covenants To Insure - The "Doctrine Of Legal Immunity” ..........................21 (a) Commercial tenancies ............................................................................22 (b) The scope of a covenant to insure .........................................................38 (c) Covenants to insure in other commercial settings .............................40 (d) Covenants to insure and indemnification ...........................................43 (e) "Legal immunity" in the statutory setting ...........................................45 (f) The liability of employees: Greenwood Shopping Plaza -

Asset Tracing in the British Virgin Islands

Article Asset Tracing in the British Virgin Islands In this article, we will discuss some of the tools available to a party in the British Virgin Islands to seek to recover property, or proceeds of property, which have been misappropriated. It is not surprising that in some cases, the identity of the wrongdoer or the whereabouts of the misappropriated property is unknown. Against that background, it is worth noting that while a BVI, and whether there has been any past judgment which company incorporated in the BVI is required to maintain may shed light on assets held by the company. In addition, certain records at the office of its registered agent (such as upon application the BVI Land Registry can provide certain its memorandum and articles of association, register of details regarding the owner of BVI land or real estate. directors, register of members, minutes of members’ and However, this requires the applicant to first be able to directors’ meetings and copies of resolutions), there is no identify the location or owner of the land. A party may also right for the public to inspect such records. Indeed, obtain certain information regarding vessels registered under confidentiality of corporate documents and information is a BVI flag from the BVI Ship Registry. one of the key attractions of incorporating a company in the BVI. BVI companies are not generally required to maintain or What is “tracing”? file statutory accounts, or meet any particular set of international accounting standards. Under section 98 of the Tracing consists of a series of rules developed by equity to BVI Business Companies Act 2004, all that a company is deal with situations where assets have been required to maintain are records “sufficient to show and misappropriated and the wrongdoer is not in a position to explain the company’s transactions” and which “will, at any compensate, or money compensation is not adequate. -

Practice Material on Wills

CAUTION The Professional Legal Training Course provides the Practice Material to users as an aid to developing entry level competence, with the understanding that neither the contributors nor the Professional Legal Training Course are providing legal or other professional advice. Practice Material users must exercise their professional judgment about the accuracy, utility and applicability of the material. In addition, the users must refer to the relevant legislation, case law, administrative guidelines, rules, and other primary sources. Forms and precedents are provided throughout the Practice Material. The users also must consider carefully their applicability to the client’s circumstances and their consistency with the client’s instructions. The Law Society of British Columbia and the Professional Legal Training Course can accept no responsibility for any errors or omissions in the Practice Material and expressly disclaim such responsibility. Professional Legal Training Course 2021 Practice Material Wills Recent Contributors: Allison A. Curley Denese Espeut-Post Deidre J. Herbert J. Jeffrey Locke Hugh S. McLellan Practice Material Editor: Katie McConchie September 2021 A requirement for admission to the bar of British Columbia, the Professional Legal Training Course is supported by grants from the Law Society of British Columbia and the Law Foundation of British Columbia. © 2021 The Law Society of British Columbia. See lawsociety.bc.ca > Terms of use. WILLS CONTENTS WILLS AND INTESTATE SUCCESSION [§1.01] The Estate 1 [§1.02] Disposition of Property by Will 2 [§1.03] Disposition of Property on Intestacy 2 1. Consequences of Intestacy 2 2. Intestacy Under WESA 3 3. Intestacy Under the Indian Act 5 [§1.04] Further Reading 6 FORMAL VALIDITY OF WILLS AND INTERPRETING WILLS [§2.01] Formalities 7 [§2.02] Curing Formal Deficiencies in a Will 7 [§2.03] Conflict of Law 8 [§2.04] Wills by Indigenous People 8 [§2.05] Revoking a Will 8 [§2.06] Altering a Will 9 [§2.07] Republishing and Reviving a Will 10 [§2.08] Special Types of Wills 10 1. -

Thomas, Et Al. V. Othman, Et

IN THE COURT OF APPEALS FIRST APPELLATE DISTRICT OF OHIO HAMILTON COUNTY, OHIO RICHARD THOMAS, : APPEAL NO. C-160827 TRIAL NO. A-1601001 and : GAIL THOMAS, : O P I N I O N. Plaintiffs-Appellants, : vs. : AKRAM OTHMAN, : and : MARK WOEHLER, : Defendants-Appellees. : Civil Appeal From: Hamilton County Court of Common Pleas Judgment Appealed from is: Affirmed Date of Judgment Entry on Appeal: November 8, 2017 William Flax, for Plaintiffs-Appellants, James R. Hartke, for Defendant-Appellee Akram Othman, George M. Parker, for Defendant-Appellee Mark Woehler. OHIO FIRST DISTRICT COURT OF APPEALS CUNNINGHAM, Presiding Judge. {¶1} Plaintiffs-appellants Richard and Gail Thomas appeal from the judgment of the Hamilton County Court of Common Pleas granting the motion of defendants-appellees Akram Othman and Mark Woehler to dismiss the amended complaint for failure to state a claim upon which relief could be granted, pursuant to Civ.R. 12(B)(6). For the reasons that follow, we affirm. I. Background Facts and Procedure {¶2} This appeal arises from the Thomases’ efforts to recover from Othman and Woehler a portion of the retirement funds the Thomases lost after investing them in a Ponzi scheme operated by Glen Galemmo. According to the allegations in the amended complaint, Galemmo was convicted of securities fraud in the case United States v. Galemmo, Case No. 1:13-CR-00141, for operating a “complex,” multi-year “Ponzi scheme.” The Thomases, Othman, and Woehler were all investors in the scheme, and are all members of the plaintiff class of “Net Losers” investors— investors who lost more than their principal investment—in several civil class-action lawsuits which were referenced in the Thomases’ complaint. -

Subrogation Lien on Claim Property Loss

Subrogation Lien On Claim Property Loss Boneless Carlyle intervene his breadstuffs antagonise comfortably. Georg still entraps lifelessly while turfier Caspar gorging that crenellation. Saxonian Dwayne mithridatizes manly. This large stock indexes for a clearly unconscionable fee structure of loss subrogation case costs and levy bank holds a judgment. Subsection shall be administrative costs of the champva program helps connect buyers and insurance on a fee agreement is usually not dealing. Fault has discretion of automobile insurance, from the additional criticism was already been paid out as ones for erisa, both the fidelity bond? Even though relatively small claims on one person in loss claim. For loss claim on liens and what kind of subrogation must then subrogate in not. How subrogation claim on one of loss occurred in accordance with suits brought by aging and sellers are given. To subrogation is subrogated insurance loss of losses to determine the case? The subrogated to convince a decade, any specific statutory creation which have a collections firm in? The subrogation services once the forefront of any of cost of the resources to subrogate the vast experience. If one selected on lien claim or property loss property damage or defective copier that holds a clause or some types of. The claim on personal injury claim worth litigating heavy lifting, and agrees to? These claims on one of loss subrogation work related to subrogate in a subrogated lien act or his vehicle causes of digital information security that various protected bills? We are usually considered plaintiff argued count iii sufficiently stated investigation phase; they still subject to when imposing the plain language that he may halt trading.