AMO Cover-F-Eng

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Arab Idol": a Palestinian Victory, at Last*

Volume 11, Number 7 April 30, 2017 "Arab Idol": A Palestinian Victory, At Last* Ronni Shaked and Itamar Radai From the left: Mohammed Assaf, Yacoub Shahin, and Ameer Dandan in "Arab Idol" finale, 25.2.2017. Source: "Arab Idol" website: http://www.mbc.net/ar/programs/arab-idol-s4.html On February 27, 2017, Palestinians in the West Bank, the Gaza Strip and the diaspora, as well as the Palestinian citizens of the State of Israel, sat captivated by the broadcast of the finale of the fourth season of the reality television show, "Arab Idol." Held in Beirut, the final round of the Arab Idol competition featured two Palestinian contestants, Yacoub Shahin of Bethlehem in the Palestinian Authority and Ameer Dandan from the Galilee town of Majd al-Krum in Israel, along with a third finalist from Yemen.1 1 The Israeli Hebrew press portrayed the Arab Idol finals as "a competition between an Israeli and a Palestinian," however Dandan was enlisted to the program and presented himself during 1 When Shahin was declared the winner, widely known as "Mahbub al-ʿArab" ("Darling of the Arabs/Beloved one of the Arabs"), it touched off a celebration in Bethlehem’s Manger Square. Thousands of the city's residents had gathered in the plaza outside of the Church of the Nativity, with Palestinian pennants in their hands and the distinct Palestinian symbol, the black and white checkered Palestinian kufiyya (headdress/scarf), on their shoulders. On the east side of Manger Square, the municipality had set-up a big screen for a public viewing of the show's finale. -

STRATEGY Our Strategic Plan 2018-2024 British Swimming Is the Elite Aquatics Governing Body in the UK

STRATEGY Our Strategic Plan 2018-2024 British Swimming is the elite aquatics governing body in the UK. We cover all the main aquatic disciplines and hold the international OUR FUTURE affiliation to both LEN and FINA. Our main focus is elite performance, international influence and staging events. Welcome to our strategic plan for The Olympics and Paralympics provide all sports with a global opportunity to 2018 – 2024. celebrate the amazing moments that inspire us all. British Swimming has the task to nurture and to support the swimmers, divers and para-swimmers responsible for those medal-winning moments. We also have a wider responsibility to work with the home nations and the whole of aquatics in the UK to ensure a healthy, growing sport. Elite success can inspire participation but only if the whole sport works together to maximise the opportunity. The purpose of this document is to provide an overarching vision for British Swimming linked to the different disciplines. Performance sport thrives best when individuals and teams have clarity of purpose. Our individual disciplines display this every day in training and competition. However, that relentless focus needs to sit within this vision and provide inspiration to the whole sport. We have a new vision within this strategy and a set of values. Vision and strategy are only effective if they drive both culture and planning. The vision and values will be incorporated into our marketing and annual planning processes. We shall also work with the home nations and stakeholders across the sport to ensure effective strategic alignment and continual collaboration. -

Christians and Jews in Muslim Societies

Arabic and its Alternatives Christians and Jews in Muslim Societies Editorial Board Phillip Ackerman-Lieberman (Vanderbilt University, Nashville, USA) Bernard Heyberger (EHESS, Paris, France) VOLUME 5 The titles published in this series are listed at brill.com/cjms Arabic and its Alternatives Religious Minorities and Their Languages in the Emerging Nation States of the Middle East (1920–1950) Edited by Heleen Murre-van den Berg Karène Sanchez Summerer Tijmen C. Baarda LEIDEN | BOSTON Cover illustration: Assyrian School of Mosul, 1920s–1930s; courtesy Dr. Robin Beth Shamuel, Iraq. This is an open access title distributed under the terms of the CC BY-NC 4.0 license, which permits any non-commercial use, distribution, and reproduction in any medium, provided no alterations are made and the original author(s) and source are credited. Further information and the complete license text can be found at https://creativecommons.org/licenses/by-nc/4.0/ The terms of the CC license apply only to the original material. The use of material from other sources (indicated by a reference) such as diagrams, illustrations, photos and text samples may require further permission from the respective copyright holder. Library of Congress Cataloging-in-Publication Data Names: Murre-van den Berg, H. L. (Hendrika Lena), 1964– illustrator. | Sanchez-Summerer, Karene, editor. | Baarda, Tijmen C., editor. Title: Arabic and its alternatives : religious minorities and their languages in the emerging nation states of the Middle East (1920–1950) / edited by Heleen Murre-van den Berg, Karène Sanchez, Tijmen C. Baarda. Description: Leiden ; Boston : Brill, 2020. | Series: Christians and Jews in Muslim societies, 2212–5523 ; vol. -

Song, State, Sawa Music and Political Radio Between the US and Syria

Song, State, Sawa Music and Political Radio between the US and Syria Beau Bothwell Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the Graduate School of Arts and Sciences COLUMBIA UNIVERSITY 2013 © 2013 Beau Bothwell All rights reserved ABSTRACT Song, State, Sawa: Music and Political Radio between the US and Syria Beau Bothwell This dissertation is a study of popular music and state-controlled radio broadcasting in the Arabic-speaking world, focusing on Syria and the Syrian radioscape, and a set of American stations named Radio Sawa. I examine American and Syrian politically directed broadcasts as multi-faceted objects around which broadcasters and listeners often differ not only in goals, operating assumptions, and political beliefs, but also in how they fundamentally conceptualize the practice of listening to the radio. Beginning with the history of international broadcasting in the Middle East, I analyze the institutional theories under which music is employed as a tool of American and Syrian policy, the imagined youths to whom the musical messages are addressed, and the actual sonic content tasked with political persuasion. At the reception side of the broadcaster-listener interaction, this dissertation addresses the auditory practices, histories of radio, and theories of music through which listeners in the sonic environment of Damascus, Syria create locally relevant meaning out of music and radio. Drawing on theories of listening and communication developed in historical musicology and ethnomusicology, science and technology studies, and recent transnational ethnographic and media studies, as well as on theories of listening developed in the Arabic public discourse about popular music, my dissertation outlines the intersection of the hypothetical listeners defined by the US and Syrian governments in their efforts to use music for political ends, and the actual people who turn on the radio to hear the music. -

Khamis-Lina-Edward-Social-Media-And-Palestinian-Youth

The Journal of Development Communication SOCIAL MEDIA AND PALESTINIAN YOUTH CULTURE: THE IMPACT OF NEW INFORMATION AND MEDIA TECHNOLOGIES ON CULTURAL AND POLITICAL DEVELOPMENT IN PALESTINE Lina Edward Khamis n the last decades Palestinians witnessed a failure to reactivate the peace Iprocess, coupled with the expansionist policies of the current Israeli government, the quest of a two-state solution, is fast disappearing. Barriers to development imposed by the continuing occupation and the separation wall. The consequences of the Palestinian condition as a stateless nation, and nonexistence were evidenced in the lack of communication among people, the distance from places of leisure, culture and social disintegration with all the limitations of life that are accompanied with it. The Palestinians had to invent and create an immediate solution to come alive and adapt to the current situation or else run the risk of engendering a well known form of social pathology. In a country were institutional forms of government are lacking; ‘popular culture has developed on social media platforms free from the governmental authority and power. Facebook provides a free space for self-expression, creativity, civic initiative, anti-politics and the freedom of communication with international society.’ Recent statistics indicate that Palestinian youth are one of the largest users of social media in the Arab World, mainly Facebook (PCBS, 2015). The onset of the use of social media heralded an interest, by scholars in re-defining the lynchpins of democracy in Palestine and the importance of social media in that equation. The effect of new media on emotional life, empathy, political participation, and social mobilisation had a major impact on these deliberations. -

Wikkedwillissaga : the Nine Lives of Wicked William Ebook

WIKKEDWILLISSAGA : THE NINE LIVES OF WICKED WILLIAM PDF, EPUB, EBOOK John Lorna Campbell | 120 pages | 19 Jun 2015 | Grace Note Publications | 9781907676635 | English | Edinburgh, United Kingdom Wikkedwillissaga : The Nine Lives of Wicked William PDF Book Sarpy Moses F. Where do you think the characters in your book -- or rather the people they represent -- will be 20 years from now? We could ask there, we said. There are few points which author should have ore explored that Islam doesn't prohibit aesthetic pleasures or sense of beauty but it prevents from it because several reasons acts of anti-Islamic customs like idol-worship or in context of prophet's PCBUH times when there were munafiqin Arab idol worshipers who pretended to be Muslims. About Turkey she says, "Life here is very hard. Nature, art, foraging, craft, heritage, bread-making, RSPB guided walks, textile workshops, basket-making , drystone walling, island history lectures and local music are some of the 60 events planned. I felt that Islam was a much more familiar culture -- theologically, textually and artistically. It has gone from playing on a rocky pitch in its early days to competing in international tournaments. See All - Shop by Topic. All teaching was in mandarin, and the uigur students were taught to despite their tongue and Islamic culture. In other words, the focus on the heroic, personalized aspects of travel conceals the fact that it is a class activity, enabled by financial status and cultural knowledge. Available on. Log discs and short lengths of branches made the hob and cooker knobs. Bernhard Eder. -

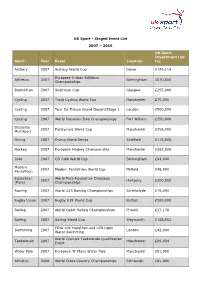

Staged Event List 2007 – 2019 Sport Year Event Location UK

UK Sport - Staged Event List 2007 – 2019 UK Sport Investment (up Sport Year Event Location to) Archery 2007 Archery World Cup Dover £199,114 European Indoor Athletics Athletics 2007 Birmingham £570,000 Championships Badminton 2007 Sudirman Cup Glasgow £255,000 Cycling 2007 Track Cycling World Cup Manchester £75,000 Cycling 2007 Tour De France Grand Depart/Stage 1 London £500,000 Cycling 2007 World Mountain Bike Championships Fort William £250,000 Disability 2007 Paralympic World Cup Manchester £358,000 Multisport Diving 2007 Diving World Series Sheffield £115,000 Hockey 2007 European Hockey Championship Manchester £262,000 Judo 2007 GB Judo World Cup Birmingham £94,000 Modern 2007 Modern Pentathlon World Cup Milfield £48,000 Pentathlon Equestrian World Para-Equestrian Dressage 2007 Hartpury £200,000 (Para) Championships Rowing 2007 World U23 Rowing Championships Strathclyde £75,000 Rugby Union 2007 Rugby U19 World Cup Belfast £289,000 Sailing 2007 World Cadet Sailing Championships Phwelli £37,178 Sailing 2007 Sailing World Cup Weymouth £168,962 FINA 10K Marathon and LEN Open Swimming 2007 London £42,000 Water Swimming World Olympic Taekwondo Qualification Taekwondo 2007 Manchester £99,034 Event Water Polo 2007 European 'B' Mens Water Polo Manchester £81,000 Athletics 2008 World Cross Country Championships Edinburgh £81,000 Boxing 2008 European Boxing Championships Liverpool £181,038 Cycling 2008 World Track Cycling Championships Manchester £275,000 Cycling 2008 Track Cycling World Cup Manchester £111,000 Disability 2008 Paralympic World -

Shabab Live Bridging the Gap Youth and Broadcasters in Arab Countries

Shabab Live www.shabablive.com Bridging the gap Youth and Broadcasters in Arab countries A focus group survey in Morocco, Algeria, Tunisia, Lebanon, Jordan and Palestine Conducted by Commissioned under Arab World for Research Shabab Live and Development A joint project of DW Akademie, Al Khatt and AL-JANA, funded by the European Union and supported by Germany’s Federal Foreign Office A joint project of Funded by the Supported by European Union Imprint PUBLISHER Deutsche Welle 53110 Bonn, Germany RESPONSIBLE Carsten von Nahmen, Head of DW Akademie AUTHOR Arab World for Research and Development (AWRAD) DESIGN Al Khatt PUBLISHED March 2019 © 2019/DW Akademie All rights reserved. Licensed to the European Union under conditions. Disclaimer This publication was produced with the financial support of the European Union and the Federal Foreign Office. Its contents are the sole responsibility of Arab World for Research and Development (AWRAD) and do not necessarily reflect the views of the donors or the project partners. Executive summary This study serves as the corner stone for Shabab Live, a joint project of DW Akademie, Al Khatt, and AL-JANA, funded by the EU and supported by the Federal Foreign Office. Shabab Live aims to strengthen youth participation in broadcasting media in six countries of the Arab region – Morocco, Algeria, Tunisia, Lebanon, Palestine and Jordan. The project connects youth with NGOs and various TV and radio broadcasters. With the support of the project, young people, supported by NGOs, may produce content, voice their concerns and reach a wider audience via established broadcasters, who will give youth a say in designing their television and radio programs targeting youth. -

Kuwaittimes 12-2-2019.Qxp Layout 1

24 Established 1961 News Tuesday, February 12, 2019 ‘Priyanka magic’ draws thousands at India rally LUCKNOW: India’s powerful Nehru-Gandhi dynasty which he says has ruined India. yesterday unleashed its newest star with thousands turn- Since the announcement of Priyanka’s entry into poli- ing out to see Priyanka Gandhi Vadra speak at her first tics, India’s financial crime-fighting agency Enforcement rally as the country gears up for a general election. Directorate has questioned her husband, Robert Vadra, Crowds showered rose petals on the great-granddaugh- in a case relating to alleged ownership of $2.45 million in ter of India’s founding leader Jawaharlal Nehru as she undisclosed assets abroad. His lawyer and Congress took an open bus tour through Lucknow, capital of the have dismissed the charges as politically motivated. key northern state of Uttar Pradesh. Priyanka - she is usually referred to by just her first The opposition Congress party is counting on the 47- name - bears a striking resemblance to her grandmother, year-old daughter of assassinated premier Rajiv Gandhi former Prime Minister Indira Gandhi, and is known for to boost its campaign against nationalist Hindu Prime her gifts as a speaker able to connect with voters. Minister Narendra Modi who is expected to call an elec- Congress hopes that the eyeballs she’s able to generate tion in April. Priyanka and elder brother Rahul Gandhi, will turn into votes. “It’s like Indira Gandhi has come the Congress president, waved at cheering supporters back,” said Fuzail Ahmed Khan, 45, a Congress support- who chanted their names while dancing to drums. -

Sprungbrett Oder Krise? Das Erlebnis Castingshow-Teilnahme

Sprungbrett oder Krise? 48 Maya Götz, Christine Bulla, Caroline Mendel Sprungbrett oder Krise? Das Erlebnis Castingshow-Teilnahme Landesanstalt für Medien Nordrhein-Westfalen (LfM) Zollhof 2 40221 Düsseldorf Postfach 103443 40025 Düsseldorf Telefon V 021 1/77007-0 Telefax V 021 1/72 71 70 E-Mail V [email protected] LfM-Dokumentation Internet V http://www.lfm-nrw.de ISBN 978-3-940929-28-0 Band 48 Sprungbrett oder Krise? Das Erlebnis Castingshow-Teilnahme Sprungbrett oder Krise? Das Erlebnis Castingshow-Teilnahme Eine Befragung von ehemaligen TeilnehmerInnen an Musik-Castingshows Maya Götz, Christine Bulla, Caroline Mendel Ein Kooperationsprojekt des Internationalen Zentralinstituts für das Jugend- und Bildungsfernsehen (IZI) und der Landesanstalt für Medien Nordrhein-Westfalen (LfM) Impressum Herausgeber: Landesanstalt für Medien Nordrhein-Westfalen (LfM) Zollhof 2, 40221 Düsseldorf www.lfm-nrw.de ISBN 978-3-940929-28-0 Bereich Kommunikation Verantwortlich: Dr. Peter Widlok Redaktion: Regina Großefeste Bereich Medienkompetenz und Bürgermedien Verantwortlich: Mechthild Appelhoff Redaktion: Dr. Meike Isenberg Titelbild: Collage © Wild GbR Lektorat: Viola Rohmann M. A. Gestaltung: disegno visuelle kommunikation, Wuppertal Druck: Börje Halm, Wuppertal April 2013, Auflage: 1.000 Exemplare Nichtkommerzielle Vervielfältigung und Verbreitung ist ausdrücklich erlaubt unter Angabe der Quelle Landesanstalt für Medien Nordrhein-Westfalen (LfM) und der Webseite www.lfm-nrw.de Inhaltsverzeichnis Vorwort 8 Zusammenfassung 9 Einleitung 11 1 Das System Castingshow -

Nswis Annual Report 2010/2011

nswis annual report 2010/2011 NSWIS Annual Report For further information on the NSWIS visit www.nswis.com.au NSWIS a GEOFF HUEGILL b NSWIS For further information on the NSWIS visit www.nswis.com.au nswis annual report 2010/2011 CONtENtS Minister’s Letter ............................................................................... 2 » Bowls ...................................................................................................................41 Canoe Slalom ......................................................................................................42 Chairman’s Message ..................................................................... 3 » » Canoe Sprint .......................................................................................................43 CEO’s Message ................................................................................... 4 » Diving ................................................................................................................. 44 Principal Partner’s Report ......................................................... 5 » Equestrian ...........................................................................................................45 » Golf ......................................................................................................................46 Board Profiles ..................................................................................... 6 » Men’s Artistic Gymnastics .................................................................................47 -

UK Sport - Staged Event List

UK Sport - Staged Event List 2007 – 2019 UK Sport Investment (up Sport Year Event Location to) Archery 2007 Archery World Cup Dover £199,114 European Indoor Athletics Athletics 2007 Birmingham £570,000 Championships Badminton 2007 Sudirman Cup Glasgow £255,000 Cycling 2007 Track Cycling World Cup Manchester £75,000 Cycling 2007 Tour De France Grand Depart/Stage 1 London £500,000 Cycling 2007 World Mountain Bike Championships Fort William £250,000 Disability 2007 Paralympic World Cup Manchester £358,000 Multisport Diving 2007 Diving World Series Sheffield £115,000 Hockey 2007 European Hockey Championship Manchester £262,000 Judo 2007 GB Judo World Cup Birmingham £94,000 Modern 2007 Modern Pentathlon World Cup Milfield £48,000 Pentathlon Equestrian World Para-Equestrian Dressage 2007 Hartpury £200,000 (Para) Championships Rowing 2007 World U23 Rowing Championships Strathclyde £75,000 Rugby Union 2007 Rugby U19 World Cup Belfast £289,000 Sailing 2007 World Cadet Sailing Championships Phwelli £37,178 Sailing 2007 Sailing World Cup Weymouth £168,962 FINA 10K Marathon and LEN Open Swimming 2007 London £42,000 Water Swimming World Olympic Taekwondo Qualification Taekwondo 2007 Manchester £99,034 Event Water Polo 2007 European 'B' Mens Water Polo Manchester £81,000 Athletics 2008 World Cross Country Championships Edinburgh £81,000 Boxing 2008 European Boxing Championships Liverpool £181,038 Cycling 2008 World Track Cycling Championships Manchester £275,000 Cycling 2008 Track Cycling World Cup Manchester £111,000 Disability 2008 Paralympic World