Our Response to the Infrastructure Commission for Scotland's Initial

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

3 Radio and Audio Content 3 3.1 Recent Developments in Scotland

3 Radio and audio content 3 3.1 Recent developments in Scotland Real Radio Scotland has been rebranded as Heart In February 2014 Capital Scotland was sold to the Irish media holding company, Communicorp. It was sold as part of eight stations divested by Global Radio to satisfy the UK regulatory authorities following the acquisition, two years ago, of GMG Radio from Guardian Media Group. Under a brand licensing agreement, Communicorp has rebranded the 'Real' stations under the 'Heart' franchise and plans to relaunch the 'Smooth' stations following the reintroduction of local programming. Therefore, Real Radio Scotland was rebranded as Heart Scotland in May 2014. XFM Scotland was re-launched by its owners, Global Radio, in March 2014. 3.2 Radio station availability Five new community radio stations are available to listeners in Scotland Scotland’s community radio industry has continued to grow. There are now 23 community stations on air, out of the 31 licences that have been awarded in Scotland. New to air in 2013/14 were East Coast FM, Irvine Beat FM, Crystal Radio, and K107 FM. Irvine Beat FM has received funding from the Lottery Awards for All fund to build a training studio. Nevis Radio, which serves Fort William and the surrounding areas, was originally licensed as a commercial radio service, but having chosen to become a community radio service it was awarded this licence instead, on application. The remaining eight of the most recent round of licence awards are preparing to launch. A licensee has two years from the date of the licence award in which to launch a service. -

Account Manager – Capital Scotland We're Looking for an Experienced Media Sales Professional Who Is Passionate, Ambitious An

Account Manager – Capital Scotland We’re looking for an experienced media sales professional who is passionate, ambitious and thrives in a competitive sales environment. You’ll be results focussed and have our clients and their goals at the heart of everything you do. Your mission is to sell amazing ideas to new and existing clients at Capital Scotland. You’ll know the local market and be able to successfully identify revenue opportunities to grow and retain client business and deliver target expectations. Including: • Source opportunities and generate appointments to win new business in your local market. • Maintain and develop new and existing client relationships. • Build relationships with clients to understand their business goals. • Explore the freshest ways of working across our broad range of products. • Create innovative ideas to deliver results and grow your client’s business. • Think and do things differently, ensuring we stand out in the industry and above our competition. • Work across multi-disciplined teams to efficiently deliver results for our clients. • Present creative pitches in a dynamic and engaging way • Deliver against agreed revenue targets, call rates, activity levels and standards of performance. Your Experience You will need to be smart, bold, and engaging and be able to display our company values in the work you do with Bravery, Integrity and Passion. You will: • Be target and goal driven. • Have experience in creating and selling advertising and marketing services. • Have a creative and solution focussed outlook – with examples to back this up. • Know the very best ways to develop new business. • Be confident with delivering pitches and presentations using the latest technology. -

Scottish Government

Tuesday 26 May 2020 SCOTTISH GOVERNMENT Constitution and External Affairs Mark Griffin (Central Scotland) (Scottish Labour): To ask the Scottish Government how many times the Cabinet has met since the World Health Organization declared the COVID-19 outbreak as a pandemic on 11 March 2020; on what dates these meetings took place, and how many were held in a (a) partly- and (b) fully-remote manner. (S5W-28945) Michael Russell: Since the World Health Organization declared the COVID-19 outbreak as a pandemic on 11 March 2020, the Scottish Cabinet has met 11 times, up to and including 19 May. The dates of these 11 meetings are as follows. From 24 March onwards, all of these meetings have been held by teleconference, with a minimum number of Ministers and supporting officials attending in person, while observing the required strict physical distancing and hygiene requirements. Cabinet meetings held between 11 March and 19 May: 17 March 24 March 31 March 7 April 14 April 21 April 28 April 5 May 10 May 12 May 19 May Finlay Carson (Galloway and West Dumfries) (Scottish Conservative and Unionist Party): To ask the Scottish Government what the monthly expenditure has been by publishing companies acting on its behalf on COVID-19 advertising since March 2020 in each Parliamentary region, also broken down by (a) newspaper advertising and (b) broadcasting outlets, including (i) radio and (ii) television. (S5W-29009) Kate Forbes: Month Media Folio Name Supplier Full Name March April May Name ITV DIGITAL 9,385 35,806 37,598 82,788 ASTUS UK LTD 9,385 35,806 -

Global-GMG Merger Inquiry: Appendices and Glossary

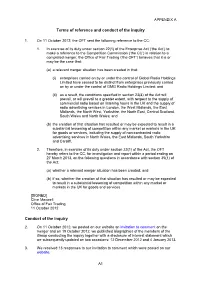

APPENDIX A Terms of reference and conduct of the inquiry 1. On 11 October 2012, the OFT sent the following reference to the CC: 1. In exercise of its duty under section 22(1) of the Enterprise Act (‘the Act’) to make a reference to the Competition Commission (‘the CC’) in relation to a completed merger, the Office of Fair Trading (‘the OFT’) believes that it is or may be the case that: (a) a relevant merger situation has been created in that: (i) enterprises carried on by or under the control of Global Radio Holdings Limited have ceased to be distinct from enterprises previously carried on by or under the control of GMG Radio Holdings Limited; and (ii) as a result, the conditions specified in section 23(4) of the Act will prevail, or will prevail to a greater extent, with respect to the supply of commercial radio based on listening hours in the UK and the supply of radio advertising services in London, the West Midlands, the East Midlands, the North West, Yorkshire, the North East, Central Scotland, South Wales and North Wales; and (b) the creation of that situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods or services, including the supply of non-contracted radio advertising services in North Wales, the East Midlands, South Yorkshire and Cardiff. 2. Therefore, in exercise of its duty under section 22(1) of the Act, the OFT hereby refers to the CC, for investigation and report within a period ending on 27 March 2013, on the following questions in accordance with section 35(1) of the Act: (a) whether a relevant merger situation has been created; and (b) if so, whether the creation of that situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods and services. -

“Reaching 79% of Commercial Radio's Weekly Listeners…” National Coverage

2019 GTN UK is the British division of Global Traffic Network; the leading provider of custom traffic reports to commercial radio and television stations. GTN has similar operations in Australia, Brazil and Canada. GTN is the largest Independent radio network in the UK We offer advertisers access to over 240 radio stations across the country, covering every major conurbation with a solus opportunity enabling your brand to stand out with up to 48% higher ad recall than that of a standard ad break. With both a Traffic & Travel offering, as well as an Entertainment News package, we reach over 28 million adults each week, 80% of all commercial radio’s listeners, during peak listening times only, 0530- 0000. Are your brands global? So are we. Talk to us about a global partnership. Source: Clark Chapman research 2017 RADIO “REACHING 79% OF COMMERCIAL RADIO’S WEEKLY LISTENERS…” NATIONAL COVERAGE 240 radio stations across the UK covering all major conurbations REACH & FREQUENCY Reaching 28 million adults each week, 620 ratings. That’s 79% of commercial radio’s weekly listening. HIGHER ENGAGEMENT With 48% higher ad recall this is the stand-out your brand needs, directly next to “appointment-to-listen” content. BREAKFAST, MORNING, AFTERNOON, DRIVE All advertising is positioned within key radio listening times for maximum reach. 48% HIGHER AD RECALL THAN THAT OF A STANDARD AD BREAK Source: Clark Chapman research NATIONAL/DIGITAL LONDON NORTH EAST Absolute Radio Absolute Radio Capital North East Absolute Radio 70s Kiss Classic FM (North) Absolute -

Domain Station ID Station UDC Performance Date

Total Per Performance No of Days DomainStation IDStation UDC Minute Date in Period Rate Radio BR ONE BBC RADIO 1 B0001Census 91£ 8.15 Radio BR TWO BBC RADIO 2 B0002Census 91£ 21.62 Radio BR1EXT BBC RADIO 1XTRA B0106Census 91£ 1.90 Radio BRASIA BBC RADIO ASIAN NETWORK B0064Census 91£ 1.80 Radio BRBEDS BBC THREE COUNTIES RADIO B0065Census 91£ 1.59 Radio BRBERK BBC RADIO BERKSHIRE B0103Census 91£ 1.52 Radio BRBRIS BBC RADIO BRISTOL B0066Census 91£ 1.52 Radio BRCAMB BBC RADIO CAMBRIDGESHIRE B0067Census 91£ 1.55 Radio BRCLEV BBC RADIO TEES B0068Census 91£ 1.53 Radio BRCMRUBBC RADIO CYMRU B0011Census 91£ 1.60 Radio BRCORN BBC RADIO CORNWALL B0069Census 91£ 1.59 Radio BRCOVN BBC RADIO COVENTRY B0070Census 91£ 1.49 Radio BRCUMB BBC RADIO CUMBRIA B0071Census 91£ 1.53 Radio BRCYMMBBC RADIO CYMRU 2 B0114Census 91£ 1.60 Radio BRDEVN BBC RADIO DEVON B0072Census 91£ 1.65 Radio BRDOR BBC DORSET B0115Census 91£ 1.57 Radio BRDRBY BBC RADIO DERBY B0073Census 91£ 1.57 Radio BRESSX BBC ESSEX B0074Census 91£ 1.61 Radio BRFIVE BBC RADIO 5 B0005Census 91£ 5.07 Radio BRFOUR BBC RADIO 4 B0004Census 91£ 14.87 Radio BRFOYL BBC RADIO FOYLE B0019Census 91£ 1.74 Radio BRGLOS BBC RADIO GLOUCESTERSHIRE B0075Census 91£ 1.49 Radio BRGUER BBC RADIO GUERNSEY B0076Census 91£ 1.45 Radio BRHRWC BBC HEREFORD AND WORCESTER B0077Census 91£ 1.52 Radio BRHUMB BBC RADIO HUMBERSIDE B0078Census 91£ 1.56 Radio BRJERS BBC RADIO JERSEY B0079Census 91£ 1.47 Radio BRKENT BBC RADIO KENT B0080Census 91£ 1.63 Radio BRLANC BBC RADIO LANCASHIRE B0081Census 91£ 1.56 Radio BRLEED BBC RADIO LEEDS -

Independent Radio (Alphabetical Order) Frequency Finder

Independent Radio (Alphabetical order) Frequency Finder Commercial and community radio stations are listed together in alphabetical order. National, local and multi-city stations A ABSOLUTE RADIO CLASSIC ROCK are listed together as there is no longer a clear distinction Format: Classic Rock Hits Broadcaster: Bauer between them. ABBEY 104 London area, Surrey, W Kent, Herts, Luton (Mx 3) DABm 11B For maps and transmitter details see: Mixed Format Community Swansea, Neath Port Talbot and Carmarthenshire DABm 12A • Digital Multiplexes Sherborne, Dorset FM 104.7 Shropshire, Wolverhampton, Black Country b DABm 11B • FM Transmitters by Region Birmingham area, West Midlands, SE Staffs a DABm 11C • AM Transmitters by Region ABC Coventry and Warwickshire DABm 12D FM and AM transmitter details are also included in the Mixed Format Community Stoke-on-Trent, West Staffordshire, South Cheshire DABm 12D frequency-order lists. Portadown, County Down FM 100.2 South Yorkshire, North Notts, Chesterfield DABm 11C Leeds and Wakefield Districts DABm 12D Most stations broadcast 24 hours. Bradford, Calderdale and Kirklees Districts DABm 11B Stations will often put separate adverts, and sometimes news ABSOLUTE RADIO East Yorkshire and North Lincolnshire DABm 10D and information, on different DAB multiplexes or FM/AM Format: Rock Music Tees Valley and County Durham DABm 11B transmitters carrying the same programmes. These are not Broadcaster: Bauer Tyne and Wear, North Durham, Northumberland DABm 11C listed separately. England, Wales and Northern Ireland (D1 Mux) DABm 11D Greater Manchester and North East Cheshire DABm 12C Local stations owned by the same broadcaster often share Scotland (D1 Mux) DABm 12A Central and East Lancashire DABm 12A overnight, evening and weekend, programming. -

THE VOICE of UK COMMERCIAL Annual Review 2011

Annual Review 2011 THE VOICE OF UK COMMERCIAL Contents 03 CHAIRMAN’S REVIEW 04 CEO’S REVIEW RADIO 06 12 18 REVENUE DIGITAL ORGANISATION 10 14 AUDIENCE INFLUENCE RadioCentre | Annual Review 2011 01 // 2011 has been a year where radio has continued to buck the trend and confound its critics as the only traditional medium to grow revenue. // 02 RadioCentre | Annual Review 2011 Chairman’s Review Welcome to the RadioCentre Review of An industry-wide marketing campaign was When I meet with my colleagues on the 2011. The last twelve months have been an launched by the RAB under the umbrella RadioCentre board each quarter, we are impressive year for commercial radio, with theme of Britain Loves Radio, with a mindful of the importance of all these continuing record audiences and strong national advertising campaign helping to services and the need to balance both the revenue growth, especially against the deliver this message. differing priorities of different members, and recessionary backdrop for all businesses. work for a secure and prosperous future for RAB also tackled the historic challenge of a the sector. I hope that 2012 proves It has been a year where radio has lack of creativity in radio advertising, with successful for you and for everyone involved continued to buck the trend and confound an important partnership with D&AD, the in our industry. its critics, as the only traditional medium to membership organisation which represents grow revenue. And if the forecasts are to be excellence in the creative, design and believed there could be more good news in advertising communities. -

Bauer Radio Total Portfolio

1 2 BAUER RADIO TOTAL PORTFOLIO RAJAR Q4 2012 3 BAUER RADIO TOTAL PORTFOLIO ■ 13.3m listeners ■ Our Place Portfolio stations are No.1 in 21 out of 21 markets ■ Smash Hits, The Hits & Heat are all in the top 10 digital stations ■ Average age 38 Source: RAJAR, Bauer Radio Total Portfolio TSA, 6 Months PE Dec 12 4 LISTENER PROFILE 4 ■ 46% of listeners are male, 54% are female BAUER RADIO TOTAL PORTFOLIO REACHES ■ 51% of listeners are ABC1, 49% C2DE 13,279,000 ADULTS 15+ EVERY WEEK ■ 76% of listeners are Main Shoppers ■ Has a commercial Share of 25.0% Source: RAJAR, Bauer Radio Total Portfolio TSA, 6 Months PE Dec 12 5 REACH BY AGE BREAK 5 WEEKLY REACH (000) 3,488 2,965 2,345 2,383 2,098 15-24 25-34 35-44 45-54 55+ Source: RAJAR, Bauer Radio Total Portfolio TSA, 6 Months PE Dec 12 6 THIS IS A FULLSCREEN PICTURE CHART 7 THIS IS A FULLSCREEN PICTURE CHART 8 THIS IS A FULLSCREEN PICTURE CHART 9 THE BAUER PLACE PORTFOLIO ■ 8.7m listeners ■ No.1 in 21 out of 21 markets ■ 18% higher reach than our nearest competitor ■ 41% more listening hours ■ Average age 42 Source: RAJAR, Bauer Place Portfolio TSA, 6 Months PE Dec 12 10 BAUER PLACE PORTFOLIO REACH Bauer Place Portfolio reaches 8.7 million adults across the UK ■ Heart FM (UK): 7.4 million ■ Capital FM (UK): 6.8 Million ■ Classic FM: 5.4 Million ■ Total Smooth Radio UK: 3.8 Million ■ talkSPORT: 3.0 Million ■ Total Absolute Radio Network: 3.1 Million Source: RAJAR, Bauer Place Portfolio TSA, 6 Months PE Dec 12 11 AND WE CONNECT WITH THEM FOR 11 LONGER Bauer Place Portfolio has average hours of 8.3 ■ Heart FM (UK): 6.9 hours ■ Capital FM (UK): 5.9 hours ■ Classic FM: 6.7 hours ■ Total Smooth Radio UK: 8.0 hours ■ talkSPORT: 6.4 hours ■ Total Absolute Radio Network: 6.9 hours Source: RAJAR, Bauer Place Portfolio TSA, 6 Months PE Ded 12 12 MADE UP OF THE BEST LOCAL BRANDS 12 13 13 FEEL INFORMED BAUER PLACE PORTFOLIO + 40% FEEL INVOLVED BAUER PLACE PORTFOLIO + 30% FEEL CONNECTED BAUER PLACE PORTFOLIO + 32% VS. -

QUARTERLY SUMMARY of RADIO LISTENING Survey Period Ending 5Th April 2015

QUARTERLY SUMMARY OF RADIO LISTENING Survey Period Ending 5th April 2015 PART 1 - UNITED KINGDOM (INCLUDING CHANNEL ISLANDS AND ISLE OF MAN) Adults aged 15 and over: population 53,502,000 Survey Weekly Reach Average Hours Total Hours Share in Period '000 % per head per listener '000 TSA % All Radio Q 47799 89 19.0 21.3 1017509 100.0 All BBC Radio Q 34872 65 10.4 15.9 553852 54.4 All BBC Radio 15-44 Q 14583 57 6.3 11.0 160045 40.5 All BBC Radio 45+ Q 20290 73 14.1 19.4 393807 63.2 All BBC Network Radio1 Q 31671 59 8.9 15.1 476849 46.9 BBC Local Radio Q 8816 16 1.4 8.7 77003 7.6 All Commercial Radio Q 33916 63 8.1 12.8 435496 42.8 All Commercial Radio 15-44 Q 17802 70 8.6 12.4 220112 55.8 All Commercial Radio 45+ Q 16115 58 7.7 13.4 215384 34.6 All National Commercial1 Q 17137 32 2.7 8.4 144545 14.2 All Local Commercial (National TSA) Q 26763 50 5.4 10.9 290951 28.6 Other Radio Q 3688 7 0.5 7.6 28161 2.8 Source: RAJAR/Ipsos MORI/RSMB 1 See note on back cover. For survey periods and other definitions please see back cover. Embargoed until 00.01 am Enquiries to: RAJAR, 6th floor, 55 New Oxford St, London WC1A 1BS 21st May 2015 Telephone: 020 7395 0630 Facsimile: 020 7395 0631 e mail: [email protected] Internet: www.rajar.co.uk ©Rajar 2015. -

Global Radio / Real and Smooth Limited REGIONAL ANALYSIS For

SLAUGHTER AND MAY Global Radio / Real and Smooth Limited REGIONAL ANALYSIS For each of the 7 SLC regions identified by the CC, Global has assessed the scale of the SLC and the customer benefits which will be lost through a divestment of any of the parties’ core stations (i.e. Smooth, Real, Capital and Heart). Global has quantified both the maximum likely scale of the SLC in each region and the customer benefit likely to be lost through divestment of core stations (to the extent this can be quantified). As a result of this analysis, Global has evidenced that any divestment of a core station would not be proportionate or reasonably justified in any of the 7 SLC areas. We comment on each of the 7 SLC areas in turn. Error! Unknown document property name. 2 1. EAST MIDLANDS Executive Summary 1.1 The scale of the SLC in the East Midlands is trivial. Based on the CC’s Provisional Findings, the revenues affected by the merger in the East Midlands are £[]. 1.2 While not accepting that any SLC found by the CC would lead to an increase in price, Global considers that any such increase would be small (not greater than 5%) given that the parties are not close competitors in the East Midlands and that Orion is a much closer competitor to both Capital and Smooth than they are to each other. A 5% price increase on the affected revenues in the East Midlands would imply the harm from the SLC is £[]. 1.3 Any harm from the SLC is substantially outweighed by the advertiser discounts that will be lost as a result of the divestment of Smooth East Midlands (£[]) which comprise: (i) Lost network discounts of £[]for contracted advertisers; and (ii) Lost single-region multi-brand discounts of £[] for non-contracted advertisers. -

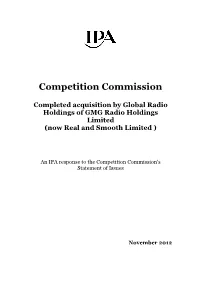

IPA Submission

Competition Commission Completed acquisition by Global Radio Holdings of GMG Radio Holdings Limited (now Real and Smooth Limited ) An IPA response to the Competition Commission's Statement of Issues November 2012 Competition Commission: Completed acquisition by Global Radio Holdings of GMG Radio Holdings Limited (now Real and Smooth Limited ) This paper responds to the Competition Commission's statement of issues with regard to the above. I About the IPA The Institute of Practitioners in Advertising is the trade body and professional institute for UK advertising, media and marketing communications agencies. Our 240 corporate members, who are based throughout the country, handle over 80% of the UK’s advertising agency business with an estimated value of £16.1 billion in 2011 (Source: Advertising Association 2012), on behalf of many tens of thousands of their client companies and organisations. As the Competition Commission will be aware, the IPA is vitally concerned regarding any consolidation in the media marketplace, which could potentially affect the ability of our members to buy airtime/space fairly and effectively on behalf of their clients. It is therefore with this in mind that the following observations are made. II. Background The Competition Commission will already have seen the IPA's submission to the OFT on this issue and will therefore be aware that we have viewed the acquisition in question with mixed feelings. On the plus side, the move might be seen to enable Commercial Radio, as a whole, to compete more effectively for