TOWARDS a THEORY of SERVICE INNOVATION: an Inductive Case Study Approach to Evaluating the Uniqueness of Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

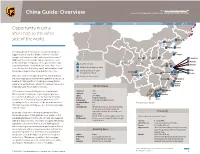

China Guide: Overview Or Call UPS International Customer Service at 1-800-782-7892

Visit ups.com/international China Guide: Overview or call UPS International Customer Service at 1-800-782-7892. GMT+ 5.5 GMT+ 6 GMT+ 7 GMT+ 8 GMT+ 8.5 Opportunity is just a short hop to the other Shenyang side of the world. Beijing Tianjin Dalian In today’s global economy, no country represents a bigger opportunity than China. Home to 1.3 billion Qingdao people and numerous cities with populations over 5 Xi’an Zhengzhou Changzhou million, China is the world’s largest exporter, as well Nantong as the third-largest importer of U.S. goods. While large Key UPS Air Hubs CHINA Nanjing Kunshan corporations have established a presence here, it is a Hefei Multiple UPS Package Facilities lesser known fact that many small- and medium-sized Shanghai American enterprises are already active here, too. UPS Air and Ocean Freight Wuxi Chengdu Hangzhou Ningbo Forwarding Locations Wuhan Suzhou Chongqing Shaoxing Have you considered expansion to the China market, UPS Aircraft Connections but new languages and unknown regulations have been Jiaxing Wenzhou a barrier to taking action? Thinking you need global Fuzhou experience and a global network to make an impression Quanzhou Xiamen internationally? No problem. Use ours. UPS in China Dongguan Guangzhou Huizhou UPS is one of the world’s largest customs brokers. Established: 1988 Foshan Employees: 6,000+ We know the ins and outs of getting your products Jiangmen Shenzhen Flights: 200+ weekly to customers in China because we have been doing Zhongshan Air Hubs: Shenzhen and Shanghai Zhuhai business there for nearly 30 years. More than 225 Delivery Fleet: 864 package vans, trailers and trucks operating facilities, two state-of-the-art hubs and over Operating Facilities: 225+ *Principal locations displayed 200 flights weekly can help you get closer to a growing Cities: 300+ customer base. -

Ups Annual Report 2012

from: Moscow, Russia 129 to: Sydney, Australia to: London, 2000 United Kingdom N1 0AB UPS ANNUAL REPORT 2012 from: UPS Zhengzhou, China 2012 from: 450000 Guadalajara, Mexico ANNUAL REPORT 44150 to: Halifax, Canada B3H 0A2 from: Louisville, USA 40215 55 Glenlake Parkway, NE Atlanta, GA 30328-3474 www.ups.com © 2013 United Parcel Service of America, Inc. UPS, the UPS brandmark, and the color brown are trademarks of United Parcel Service of America, Inc. All rights reserved. 8851_CVRc4.indd 1 3/6/13 12:39 PM QUQQUICKUI K FINANCIAL INVESTOR INFORMATION HIGHLIGHTS 2012 2011 2010 FACTSFAACACTS Annual Meeting UPS Shareowner Services Revenue $54,127 $53,105 $49,545 Our annual meeting of shareowners will be held at 8 a.m. Convenient access 24 hours a day, seven days a week. on May 2, 2013 at the Hotel DuPont, 11th and Market Operating expenses 52,784 47,025 43,904 Street, Wilmington, DE. Shareowners of record as of Class A Common Shareowners Net income 807 3,804 3,338 March 15, 2013 are entitled to vote at the meeting. www.cpushareownerservices.com 888-663-8325 Adjusted net income1 4,389 4,311 3,495 Investor Relations Class B Common Shareowners Diluted earnings per share 0.83 3.84 3.33 You can contact our Investor Relations Department at: www.cpushareownerservices.com 1907 1 800-758-4674 YEAR FOUNDED Adjusted diluted earnings per share 4.53 4.35 3.48 UPS Dividends declared per share 2.28 2.08 1.88 55 Glenlake Parkway NE Calls from outside the United States: 201-680-6612 399, Atlanta, GA 30328-3474 TDD for hearing impaired: 800-231-5469 2.5 MILLION Assets 38,863 34,701 33,597 800-877-1503 or 404-828-6059 TDD for non-U.S. -

Service Guide LATIN AMERICA and the CARIBBEAN Effective January 1, 2008 TABLE of CONTENTS 1

Service Guide LATIN AMERICA AND THE CARIBBEAN Effective January 1, 2008 TABLE OF CONTENTS 1 Table of Contents Service Portfolio Services ...............................................2 New Services UPS Returns®............................................3 UPS PaperlessSM Invoice ..................................4 UPS Broker of ChoiceSM....................................5 Additional Services UPS Trade DirectSM .......................................6 Customs Brokerage ......................................6 Saturday Delivery .......................................6 Extended Areas .........................................6 Address Correction.........................................6 UPS Exchange CollectSM...................................6 UPS World EaseSM........................................6 Technology Services UPS TradeAbilityTM........................................7 Quantum View NotifySM....................................7 UPS Billing Data and Billing Analysis Tool ...................7 UPS Internet ShippingTM...................................7 UPS WorldShip® .........................................7 My UPS................................................7 UPS Online® Tools .......................................7 UPS Packaging Packaging, Use, Features and Dimensions...................8 How to Prepare Your Shipments Packaging Guidelines ....................................9 The UPS International Air Waybill.........................10 Multiple-Package Shipments.............................10 Commercial Invoice ....................................11 -

United Parcel Service

United Parcel Service By Michael Vida Carmela Miele Salvatore Samà 1 of 34 St. John’s University Undergraduate Student Managed Investment Fund United Parcel Service, Inc. (UPS) $58.40 Date: April 14, 2003 Type of Report: Recommendation & Analysis Recommendation: Limit order to buy 175 shares at $55.00 Market order to buy 175 shares Industry: Transportation - Air Delivery, Freight & Parcel Services Analysts: Michael Vida - [email protected] Carmela Miele – [email protected] Salvatore Samà – [email protected] Share Data Price - $58.40 Fundamentals Date – April 14, 2003 P/E (12/02): 20.2 Target Price - $60.35 P/E (12/03E): 26.46 52 Week Price Range - $53.00 - $67.10 Book Value/Share: $11.09 Market Capitalization - $ 64.644 Billion Price/Book Value: 5.167 Shares Outstanding – 1.12 Billion Dividend Yield: 1.46% Revenue - $31.272 Billion Proj. LT EPS Growth Rate: 14% ROE 2002: 26.10% Earnings Per Share and Projections FY Ending Full Year Consensus Est. 12/01A 2.13 12/02A 2.84 12/03E 2.29 Avg=2.33 (yahoo) 12/04E 2.67 Avg=2.67 (yahoo) 12/05E 2.94 N/A 2 of 34 Executive Summary We are recommending the purchase of 350 shares of UPS, currently trading on the NYSE at $57.30. United Parcel Services has one of the most extensive global ground and air networks for transportation. The largest transportation company, UPS, has been outperforming S&P by 30%. UPS is not solely a transportation company; they also act as consultants for the logistics of major companies in 130 countries. -

UPS Rate and Service Guide

UPS Rate and Service Guide 2011 Retail Rates For Customers Located in Alaska and Hawaii Logistics is the most powerful force in business today Discover the new logistics Logistics. It’s about getting things where they need to be, exactly when they need to be there, and doing it as efficiently as possible. But today’s logistics can offer much more than that. It’s a strategic way to add value to your business. It makes running your business easier. It lets you serve your customers better. And it can help you grow. It’s the new logistics. What the new logistics can do for you The new logistics is more than just getting things to the right place at the right time at the right cost. It’s about using the movement of goods as a competitive advantage. It’s a whole new way of thinking. And a powerful force for growing your business. What the new logistics can do for the earth The new logistics means efficiency. And efficiency means moving shipments using the least amount of resources. Because we manage our own network responsibly, UPS can offer you more ways to make greener transportation decisions. Access to resources through UPS visit ups.com® In a logistics-driven world, UPS is better suited to help your business 1-800-Pick-UPS® succeed than any other company. You don’t need a large warehouse, distribution center or global network to access this new logistics. You just need UPS. We have more than 400,000 dedicated employees, more than a century of logistics experience and a hard-won reputation for enabling some of the globe’s largest and most technologically advanced supply chains. -

(Austria) Logistic Gmbh Belgium / België / Be

Austria / Österreich United Parcel Service Speditionsgesellschaft m.b.h. UPS SCS (Austria) Logistic GmbH Belgium / België / Belgique United Parcel Service Belgium NV UPS SCS (Belgium) NV UPS Capital Versicherungsvermittlung GmbH, Belgian Branch UPS Europe SPRL Bulgaria / България UPS Bulgaria EOOD Czech Republic / United Parcel Service Czech Republic, s.r.o. Česká republika UPS SCS (Czech Republic) s.r.o. Denmark / Danmark U.P.S. Danmark A/S UPS SCS (Denmark) ApS Finland / Suomi United Parcel Service Finland Oy UPS SCS (Finland) Oy France United Parcel Service France SNC UPS SCS (France) SAS UPS Capital Versicherungsvermittlung GmbH, France Branch UPS Logistics Group SAS Germany / Deutschland United Parcel Service Deutschland S.à r.l. & Co. OHG UPS SCS GmbH & Co. OHG UPS SCS (Services) GmbH United Parcel Service LLC & Co. OHG UPS Capital Versicherungsvermittlung GmbH Fritz Companies Deutschland GmbH UPS Logistics Group International GmbH UPS Transport Services GmbH Greece / Ελλάδα UPS of Greece, Inc. Hungary / Magyarország UPS SCS (Hungary) Szállítmányozási Korlátolt Felelosségu Társaság UPS Healthcare Hungary Zrt. UPS Hungary Forwarding Limited Liability Company Ireland / Éire United Parcel Service of Ireland Ltd UPS (SCS) Ireland Ltd United Parcel Service CSTC Ireland Ltd Italy / Italia United Parcel Service Italia S.R.L. UPS SCS (Italy) S.R.L. UPS Capital Versicherungsvermittlung GmbH, Italian Branch UPS Healthcare Italia S.R.L. Luxembourg / Lëtzebuerg United Parcel Service Luxembourg S.à r.l. United Parcel Service Deutschland S.à r.l. UPS Worldwide Services S.à r.l. Netherlands / Nederland United Parcel Service Nederland BV UPS SCS (Nederland) B.V. UPS Logistics Group International B.V. Norway / Norge UPS Norway AS Poland / Polska UPS Polska sp. -

Conference Papers-Web Ed-Through 2010 7/2010 Update

T:\Website\Conference Papers-Web Ed-through 2010 7/2010 update A B C D E AUTHOR, LAST AUTHOR, FIRM YEAR TITLE OF PAPER NAME FIRST NAME 1 2 Anderson, Esq. John A. Anderson and Yamada, PC 2010 Limitations on a Carrier's Recovery of Collection Charges pdf. Beckwith, Esq. Dirk H. Foster, Swift, Collins & 2010 A Motor Carrier's Ten Best Practices Regarding Investigating and Claim Review pdf. 3 Smith, P.C. Blubaugh Marc S. Benesch, Friedlander, 2010 Loss and Damage Claims Best Practices: The 3PLs Perspective pdf. 4 Coplan & Aronoff LLP 5 Brown Michael S. Avalon Risk Management 2010 Cargo Loss - Risk Management and Insurance 6 Cammarano, Esq. Dennis A. Cammarano & Sirna, LLP 2010 U.S. Supreme Court Case of: K-Line & Union Pacific v. Regal-Beloit Corp. pdf. 7 Carey, CCP Cindy nVision Global 2010 Shippers Best Practices Regarding Preparing and Filing Claims pdf. Downs Jordan The Garden Distribution 2010 Transportation and Logistics Contracts - Best Practices pdf. Group Of Central Garden 8 and Pet Hillenbrand, Esq. Hyman DeOrchis, Hillenbrand & 2010 Everything You Wanted to Know About Third Party Intermediaries, But Were Afraid to Ask 9 O'Brien, LLP pdf. Lopez-Baum Estella Expeditors International of 2010 Customs Trade Partnership Against Terrorism (CTPAT) pdf. 10 Washington Inc. Mazaroli, Esq. David L. Law Offices of David 2010 The COGSA "Customary Freight Unit" Limitation and its Effect on Shippers of Special Use 11 Mazaroli Vehicles, Heavy Equipment and Bulk Cargoes pdf. Payne Martha Benesch Friedlander Coplan 2010 Transportation and Logistics Contracts - Key Elements pdf. 12 & Aronoff LLP 13 Regan Mike TranzAct Technologies, Inc. -

UPS Asia Pacific Fact Sheet

UPS ASIA PACIFIC REGION FACTSHEET FOUNDED 28 August 1907, in Seattle, Washington, USA ESTABLISHED IN ASIA PACIFIC 1988 WORLD HEADQUARTERS Atlanta, Ga., USA ASIA PACIFIC HEADQUARTERS Singapore UPS ASIA PACIFIC PRESIDENT Ross McCullough WORLD WIDE WEB ADDRESS www.ups.com UPS ASIA PACIFIC REGION OFFICE UPS House 22 Changi South Avenue 2 Singapore 486064 GLOBAL VOLUME & REVENUE 2019 REVENUE US$74 billion 2019 DELIVERY VOLUME 5.5 billion packages and documents DAILY GLOBAL DELIVERY VOLUME 21.9 million packages and documents DAILY U.S. AIR VOLUME 3.5 million packages and documents DAILY INTERNATIONAL VOLUME 3.2 million packages and documents EMPLOYEES 13,092 in Asia Pacific; 528,000 globally ASIA PACIFIC AREAS SERVED 41 countries & territories ASIA PACIFIC POINTS OF ACCESS More than 2,979 points of access including UPS Express, MBEs (Mail Box Etc.), customer centers, authorized shipping outlets, lockers and alliances OPERATING FACILITIES 254 (admin offices, package centers, hubs, gateway offices, distribution centers and warehouses, healthcare facilities, active and inactive CL sites) ASIA PACIFIC DELIVERY FLEET 1,676 (package vans, trucks, trailers, motorcycles and alternative fuel vehicles) WEEKLY FLIGHTS INTRA-ASIA PACIFIC 168 INTERNATIONAL 144 AIRPORTS SERVED INTRA-ASIA PACIFIC 17 (Shanghai – PVG; Shenzhen – SZX; Zhengzhou – CGO; Hong Kong – HKG; Penang – PEN; Kuala Lumpur – KUL; Clark – CRK; Cebu – CEB; Osaka – KIX; Tokyo – NRT; Incheon – ICN; Singapore – SIN; Jakarta – CGK; Taipei – TPE; Bangkok – BKK; Sydney – SYD; and Guam – GUM;) INTERNATIONAL -

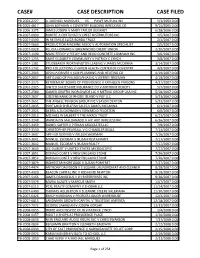

Case# Case Description Case Filed

CASE# CASE DESCRIPTION CASE FILED PB-2003-2227 A. MICHAEL MARQUES VS PAWT MUTUAL INS 5/1/2003 0:00 PB-2005-4817 JOHN BOYAJIAN V COVENTRY BUILDING WRECKING CO 9/15/2005 0:00 PB-2006-3375 JAMES JOSEPH V MARY TAYLOR DEVANEY 6/28/2006 0:00 PB-2007-0090 ROBERT A FORTUNATI V CREST DISTRIBUTORS INC 1/5/2007 0:00 PB-2007-0590 IN RE EMILIE LUIZA BORDA TRUST 2/1/2007 0:00 PB-2007-0663 PRODUCTION MACHINE ASSOC V AUTOMATION SPECIALIST 2/5/2007 0:00 PB-2007-0928 FELICIA HOWARD V GREENWOOD CREDIT UNION 2/20/2007 0:00 PB-2007-1190 MARC FEELEY V FEELEY AND REGO CONCRETE COMPANY INC 3/6/2007 0:00 PB-2007-1255 SAINT ELIZABETH COMMUNITY V PATRICK C LYNCH 3/8/2007 0:00 PB-2007-1381 STUDEBAKER WORTHINGTON LEASING V JAMES MCCANNA 3/14/2007 0:00 PB-2007-1742 PRO COLLECTIONS V HAVEN HEALTH CENTER OF COVENTRY 4/9/2007 0:00 PB-2007-2043 JOSHUA DRIVER V KLM PLUMBING AND HEATING CO 4/19/2007 0:00 PB-2007-2057 ART GUILD OF PHILADELPHIA INC V JEFFREY FREEMAN 4/19/2007 0:00 PB-2007-2175 RETIREMENT BOARD OF PROVIDENCE V KATHLEEN PARSONS 4/27/2007 0:00 PB-2007-2325 UNITED STATES FIRE INSURANCE CO V ANTHONY ROSCITI 5/7/2007 0:00 PB-2007-2580 GAMER GRAFFIX WORLDWIDE LLC V METINO GROUP USA INC 5/18/2007 0:00 PB-2007-2637 CITIZENS BANK OF RHODE ISLAND V PGF LLC 5/23/2007 0:00 PB-2007-2651 THE ANGELL PENSION GROUP INC V JASON DENTON 5/23/2007 0:00 PB-2007-2835 PORTLAND SHELLFISH SALES V JAMES MCCANNA 6/1/2007 0:00 PB-2007-2925 DEBRA A ZUCKERMAN V EDWARD D FELDSTEIN 6/6/2007 0:00 PB-2007-3015 MICHAEL W JALBERT V THE MKRCK TRUST 6/13/2007 0:00 PB-2007-3248 WANDALYN MALDANADO -

2021 UPS® Rate & Service Guide

2021 UPS® Rate & Service Guide Alaska & Hawaii Rates Updated July 11, 2021 Essential Contacts Support UPS Customer Service WorldShip® Technical Support ups.com ups.com/worldshipsupport 1-800-PICK-UPS® (1-800-742-5877) 1-888-553-1118 1-800-877-1548 En Español 1-800-782-7892 International UPS Package Design and Test Lab 1-800-811-1648 Billing 1-877-877-7229 1-800-554-9964 Hazardous Materials UPS CampusShip® Support 1-800-833-0056 Hearing Impaired – TTY/TDD Help Desk: 1-877-289-6418 (United States) [email protected] ups.com/upsemail/input International Shipping ups.com/international 1-800-782-7892 Zone Charts View or download at ups.com/rates Freight Services UPS offers multiple options for shipments over 150 pounds. For more information on these services, go to pages 2-4. Air Freight Services UPS Trade Direct® ups.com/north-americanairfreight Trade Direct ups.com/internationalairfreight 1-800-742-5727 1-800-443-6379 UPS Worldwide Express Freight® Services Ocean Freight Services UPS Worldwide Express Freight at ups.com ups.com/oceanfreight 1-800-782-7892 1-800-443-6379 UPS Express Critical® Express Shipping 1-800-714-8779 UPS Solutions Visit ups.com/services to view the full portfolio of UPS services. The UPS Store® UPS Mail Innovations® theupsstore.com ups.com/mailinnovations 1-800-789-4623 1-800-500-2224 UPS Capital® UPS Supply Chain Solutions® upscapital.com ups.com/supplychainsolutions 1-877-263-8772 1-800-742-5727 Parcel Pro® parcelpro.com 1-888-683-2300 Stay on top of the latest UPS news, announcements and critical updates via e-mail at ups.com/subscribe. -

Handbook for Finnish Startups for Entering Chinese Market

Handbook for Finnish Start-ups REVIEW 338/2017 REVIEW for Entering Chinese Market Riikka Koponen, Maggie Li and Tero Kosonen, B&B Advisors Shanghai Tekes Report 1/2015 Helsinki 2015 2 Riikka Koponen, Maggie Li and Tero Kosonen, B&B Advisors Shanghai Handbook for Finnish Start-ups for Entering Chinese Market Tekes Review 338/2017 Helsinki 2017 3 Tekes – the Finnish Funding Agency for Innovation Tekes is the main public funding organisation for research, development and innovation in Finland. Tekes funds wide-ranging innovation activities in research communities, industry and service sectors and especially promotes cooperative and risk-intensive projects. Tekes’ current strategy puts strong emphasis on growth seeking SMEs. B&B Advisors Shanghai B&B Advisors Shanghai is a Finnish boutique-sized management-consulting firm with offices in Helsinki, Shanghai and Hong Kong. B&B Advisors Shanghai provides Nordic companies with strategy and market entry-related advisory services as well as project and interim management in China. www.bietbi.com Copyright Tekes 2017. All rights reserved. This publication includes materials protected under copyright law, the copyright for which is held by Tekes or a third party. The materials appearing in publications may not be used for commercial purposes. The contents of publications are the opinion of the writers and do not represent the official position of Tekes. Tekes bears no responsibility for any possible damages arising from their use. The original source must be mentioned when quoting from the materials. ISSN 1797-7339 ISBN 978-952-457-630-7 Cover photo: B&B Advisors Shanghai Page layout: DTPage Oy 4 Forewords China has seen great economic development during the last decades and its economy is already the second biggest economy in the world (only after US). -

We Simplify Freight Shipping. There’S More to UPS Than Just Transporting Small Packages All Over the Planet

We simplify freight shipping. There’s more to UPS than just transporting small packages all over the planet. In fact, we’re equally proficient at moving really big things on pallets and in containers. If you’re looking to grow your business in unfamiliar countries, take a closer look at UPS® Global Freight Forwarding. You might be surprised to learn we’re the world’s sixth largest1 freight forwarder. But please don’t think we only work for huge companies. Every day, we help businesses of all sizes confidently cross new borders. 1Armstrong & Associates and Air Cargo News, 6/14/19 2 Table of Contents 4 Air freight 8 Ocean freight 12 Multimodal freight 3 Air Freight 4 Air Freight If it has an airport, we’ll get your shipment there. If you’re using air freight, it’s critical. Your shipment needs to get where it needs to be, when it needs to be there. On time, without doubt. We get it. It’s our job to move your goods, expeditiously and cost-effectively. Whether it’s on our own aircraft or the next flight out, you can rest assured your freight will always fly the most efficient way possible.Because it’s not the logo on the plane that matters most to us; it’s the logo on the cargo. 5 Air Freight At a glance Service to 14,000+ Operations in 220+ origins and 140+ countries destinations countries served and territories Service to 300+ air and ocean 600+ operating airports facilities worldwide We move everything from life-saving vaccines to fidget spinners 6 Air Freight There are more ways to deliver your airfreight than just our airplanes.