Designing Banknote Identity DNB Occasional Studies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

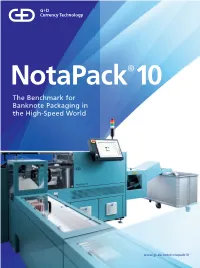

The Benchmark for Banknote Packaging in the High-Speed World

NotaPack®10 The Benchmark for Banknote Packaging in the High-Speed World www.gi-de.com/notapack10 2 NotaPack® 10 3 Concentrated packaging power NotaPack 10 is the leading banknote PHENOMENAL SECURITY MODULAR, COMPACT, FLEXIBLE FULLY AUTOMATIC – INCREASED PRODUCTIVITY – packaging system worldwide for cash Three main factors drive a high level With a high level of product modularity FULLY INTEGRATED INCREASED EFFICIENCY of security: First, intelligent features and optimum flexibility as a result of The G+D High-Speed World is character- NotaPack 10 packages up to 10 bundles centers and banknote printing works, that safeguard the unpackaged bank- over 30 different modules, NotaPack 10 ized by the perfect integration of every of 500 or 1,000 banknotes per minute – engineered in particular for the de- note bundle right up until it is fully can fulfill all key customer requirements. single element, so it is no surprise that quickly, reliably, and to a consistently manding requirements of the industry. shrink-wrapped. These include optical It also offers integration of up to five NotaPack 10 is designed for perfect high level of quality. The system’s energy It is the flawless packaging solution bundle inspection and advanced access BPS systems, and an extremely compact alignment and compatibility with BPS consumption is very low in comparison protection facilitated by continuous design that is suitable for very confined systems and G+D software. Thus, the to other systems. These considerations for the BPS M3, M5, M7, and X9 conveyor covers with locks and log file spaces (taking up floor space of just ideally alligned end-to-end process make the NotaPack 10 a highly efficient, High-Speed Systems, simultaneously writing (p. -

DNB Occasional Studies Vol.8/No.4 (2010)

Occasional Studies Banknote design for retailers and public DNB Occasional Studies Vol.8/No.4 (2010) Hans de Heij Central bank and prudential supervisor of financial institutions ©2010 De Ne der land sche Bank NV Author: Hans de Heij e-mail: [email protected] Aim of the Occasional Studies is to disseminate thinking on policy and analytical issues in areas relevant to the Bank. Views expressed are those of the individual authors and do not necessarily reflect official positions of De Ne der land sche Bank. Editorial Committee Jakob de Haan (chairman), Eelco van den Berg (secretary), Hans Brits, Pim Claassen, Maria Demertzis, Peter van Els, Jan Willem van den End, Maarten Gelderman and Bram Scholten. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any means, electronic, mechanical, photocopy, recording or otherwise, without the prior written permission of De Ne der land sche Bank. Subscription orders for DNB Occasional Studies and requests for specimen copies should be sent to: De Ne der land sche Bank NV Communications P.O. Box 98 1000 AB Amsterdam The Netherlands Internet: www.dnb.nl Occasional Studies Vol.8/No.4 (2010) Hans de Heij Banknote design for retailers and public Banknote design for retailers and public Abstract Two stakeholders of banknote design are discussed, retailers and the general public. A retailer on average receives around 120 banknotes a day. A security check should be effected in less than two seconds and avoid discussion with the client. -

Frequently Asked Questions Coins and Notes July 2020

Frequently Asked Questions Coins and Notes July 2020 A. Currency Issuance 1. Under what authority does the Bangko Sentral ng Pilipinas (BSP) issue currency? The BSP is the sole government institution mandated by law to issue notes and coins for circulation in the Philippines. In Particular, Section 50 of Republic Act (R.A) No. 7653, otherwise known as The New Central Bank Act, as amended by Republic Act No. 11211, stipulates that the BSP shall have the sole power and authority to issue currency within the territory of the Philippines. It also issues legal tender commemorative notes and coins. 2. How does the BSP determine the volume/value of notes and coins to be issued annually? The annual volume/value of currency to be issue is projected based on currency demand that is estimated from a set of economic indicators which generally measure the country’s economic activity. Other variables considered in estimating currency order include: required currency reserves, unfit notes for replacement, and beginning inventory balance. The total amount of banknotes and coins that the BSP may issue should not exceed the total assets of the BSP. 3. How is currency issued to the public? Based on forecast of currency demand, denominational order of banknotes and coins is submitted to the Currency Production Sub-Sector (CPSS) for production of banknotes and coins. The CPSS delivers new BSP banknotes and coins to the Cash Department (CD) and the Regional Operations Sub-Sector (ROSS). In turn, CD services withdrawals of notes and coins of banks in the regions through its 22 Regional Offices/Branches. -

Selected Quality Metrics for Digital Passport Photographs Vom

Selected Quality Metrics for Digital Passport Photographs Vom Fachbereich Informatik der Technischen Universität Darmstadt genehmigte Dissertation Zur Erlangung des akademischen Grades Doktor-Ingenieurs (Dr.-Ing.) von Oriana Yuridia González Castillo aus Cuernavaca, Morelos Mexiko Referenten der Arbeit: Prof. Dr. José L. Encarnação, Technische Universität Darmstadt Prof. Dr. Stephen Wolthusen, Royal Holloway University of London Tag der Einreichung: 26.10.2007 Tag der mündliche Prüfung: 12.12.2007 Hochschulkennziffer D17 Acknowledgements This work was developed thanks to the facilities provided by the Fraunhofer-Institute for Com- puter Graphics Darmstadt (Fraunhofer IGD), the founds provided for the Consejo Nacional de Ciencia y Tecnología (CONACyT) México and the Deutscher Akademischer Austausch Dienst (DAAD) Germany. The development of this thesis in Germany has been one of the best experiences in my life. I learned many things which I could not have learned in any other country. This thesis rep- resents the culmination of the biggest dream I ever had. I want to thank all the people who supported me to make it possible: Stephanie Buechl, Dr. Volker Roth, Dr. Christoph Busch, Prof. José L. Encarnação, Dr. Stephen Wolthusen, Dr. Martin Schmucker, Dr. Henning Daum, Dr. Ullrich Pinsdorf, Dipl. Ing. Alexander Nouak and all the colleagues of the de- partment A8 from Fraunhofer IGD in Darmstadt. I also want to thank to: Elfriede Fitschen, Elke Frank, Sabine Bartsch, Doris Müller, Barbara Merten, Carola Eichel and my friends Ana, Adriana, Francisco, Chetna, Sebastian, Jaime, Sonja, Mariza, Erica and Roberto C. My family in Mexico has played a very important role in the development of my career. -

2 Euro Kibris 2008

2 euro kibris 2008 click here to download We offer the lowest price online for the Cyprus 2 euros coin. The coin depicst a cruciform idol from the Chalcolithic period ( BC). [eur]. Jul 10, As from 1 February , only euro banknotes and coins may be The Cypriot 2 euro coin edge inscription Image of Cyprus 2 euros coin. Detailed information about the coin 2 Euro, Cyprus, with pictures and collection Lettering: ΚΥΠΡΟΣ KIBRIS Engraver: Tatiana Sotiropoulou, Erik Maell. Cypriot euro coins feature three separate designs for the three series of coins. Cyprus has been In and , the Mint of Finland was chosen to mint the coins (except the €2 1 Cypriot euro design; 2 Circulating Mintage quantities; 3 Identifying marks; 4 Design National Identifier, "ΚΥΠΡΟΣ (Kypros) and KIBRIS". Worth - Cyprus 2 euro in the coin catalog at www.doorway.ru Edge description, '2 EYPΩ 2 EURO 2 EYPΩ 2 EURO' Obverse, KIBRIS / ΚΥΠΡΟΣ. Find 2 euro kibris from a vast selection of Coins. Get great deals #e Zypern Kursmünzensatz Euro-Set Cyprus * Kibris 1 Cent bis 2 Euro. EUR Find great deals for Cyprus 2 Euro, Shop with confidence on eBay!. Find great deals for Cyprus Euro, Shop with 2 Euro Coin Cyprus Gem Uncirculated Cyprus 2 Euro Cents~Double Ram~Free Shipping. Text picture side: ΚΥΠΡΟΣ KIBRIS (CYPRUS) Text value side: 2 EURO. Design, Picture side: Tatiana Sotiropoulou, Erik Maell Value side: Luc Luycx. www.doorway.ru is a complete online catalog of values for euro coins with daily updated market prices for your Click here to access Cyprus 2 Cent Coin 1 cent, 2 cent, 5 cent, Cyprus, подробнее. -

France À Fric: the CFA Zone in Africa and Neocolonialism

France à fric: the CFA zone in Africa and neocolonialism Ian Taylor Date of deposit 18 04 2019 Document version Author’s accepted manuscript Access rights Copyright © Global South Ltd. This work is made available online in accordance with the publisher’s policies. This is the author created, accepted version manuscript following peer review and may differ slightly from the final published version. Citation for Taylor, I. C. (2019). France à fric: the CFA Zone in Africa and published version neocolonialism. Third World Quarterly, Latest Articles. Link to published https://doi.org/10.1080/01436597.2019.1585183 version Full metadata for this item is available in St Andrews Research Repository at: https://research-repository.st-andrews.ac.uk/ FRANCE À FRIC: THE CFA ZONE IN AFRICA AND NEOCOLONIALISM Over fifty years after 1960’s “Year of Africa,” most of Francophone Africa continues to be embedded in a set of associations that fit very well with Kwame Nkrumah’s description of neocolonialism, where postcolonial states are de jure independent but in reality constrained through their economic systems so that policy is directed from outside. This article scrutinizes the functioning of the CFA, considering the role the currency has in persistent underdevelopment in most of Francophone Africa. In doing so, the article identifies the CFA as the most blatant example of functioning neocolonialism in Africa today and a critical device that promotes dependency in large parts of the continent. Mainstream analyses of the technical aspects of the CFA have generally focused on the exchange rate and other related matters. However, while important, the real importance of the CFA franc should not be seen as purely economic, but also political. -

ID Document and Banknote Production: the Technology of Trust

YEAR 19 / AUGUST 2015 / ISSUE 65 INFOSECURA ID document and banknote production: The technology of trust A magazine for the security printing industry worldwide, published four times a year by Intergraf in Brussels and mailed to named members of the security printing community, such as security printers, their suppliers, banknote issuing, government and postal www.securityprinters.orgwww.securityprinters.org / 1 authorities as well as police forces in more than 150 countries. www.intergraf.eu EDITORIAL / AUGUST 2015 / INFOSECURA Contents Trust is our business: 3 spread the word Fighting document fraud he security printing industry is forever fighting against threats. Threats from counterfeiting mainly, and conse- 5 Tquently the industry spends millions to develop ever more Identify: the next generation fiendishly difficult security features, which come often very close to the unreachable ideal of uncounterfeitable. As the very low 7 number of counterfeits compared to the number of banknotes in existence shows, these features work. Do they work because Strong market growth in secure elements they are technically so advanced that no counterfeiter in his/her right mind would attempt to produce a credible copy? Or do they work because the really 8 clever counterfeiters and money-conmen have found easier pickings? Possibly The EU’s new digital strategy a bit of both. At the last Security Printers Conference by Intergraf, a document examiner 9 from Interpol showed your correspondent a counterfeit Euro note that had Birth certificates: the weakest link been drawn by hand. It was almost perfect and it was also almost charming in its naivety. The counterfeiter could have made more money selling his hand- 11 iwork as a work of art than passing it off as a banknote. -

Acrylic Business Card Holder

Hello – thanks for stopping by! If you’re writing an article, or reviewing our products, you’ve come to the right place. To make life easier, we’ve collated all our most commonly requested facts, figures and high res images for you to browse, download and quote from. If you’re still after more info, or some different images or format, please do get in touch – we’ll do everything we can to help. MOO is a new kind of printing business. The internet, smartphones, tablets - everyone’s online all the time (including us!) But that doesn’t mean that we’ve stopped enjoying the feel of something beautiful and tangible in our hands. In an increasingly digital world, MOO makes life a little less virtual. Why? Because we love to print. MOO makes life a little less virtual. MOO was born from a passion for beautiful, high-quality printed products and a love of great design – for everyone. Founded in 2004, we aimed to disrupt the $640 billion global print industry by combining the values of professional design with the accessibility and reach of the web. Printing has been around for centuries, and we’re certainly not the first printer to go digital. But since the launch of moo.com on 19th September 2006, we’ve worked hard to set the standard for digital print. How? With consistently remarkable new products that combine great design and uncompromising high standards. MOO is a bit different to other printers. We invented a unique, patented technology called ‘Printfinity’ which allows customers to have a different image on every single Business Card, MiniCard, Postcard, Greeting Card or Sticker in a pack. -

C 62 Official Journal

ISSN 1977-091X Official Journal C 62 of the European Union Volume 57 English edition Information and Notices 4 March 2014 Notice No Contents Page II Information INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES European Commission 2014/C 62/01 Non-opposition to a notified concentration (Case COMP/M.7138 — ThyssenKrupp/Acciai Speciali Terni/Outokumpu VDM) ( 1) . 1 2014/C 62/02 Non-opposition to a notified concentration (Case COMP/M.7052 — Lloyds Development Capital/ PostNL/TNT Post UK) ( 1) . 2 2014/C 62/03 Non-opposition to a notified concentration (Case COMP/M.7157 — BPCE/GIMV/Veolia Transport Belgium) ( 1) . 2 2014/C 62/04 Non-opposition to a notified concentration (Case COMP/M.7168 — Lukoil/ISAB/ISAB Energy/ISAB Energy Services) ( 1) . 3 Price: 1 EN EUR 3 ( ) Text with EEA relevance (Continued overleaf) Notice No Contents (continued) Page IV Notices NOTICES FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES Council 2014/C 62/05 Council conclusions — Efficient and innovative education and training to invest in skills — Supporting the 2014 European Semester . 4 European Commission 2014/C 62/06 Interest rate applied by the European Central Bank to its main refinancing operations: 0,25 % on 1 March 2014 — Euro exchange rates . 7 2014/C 62/07 New national sides of euro circulation coins . 8 2014/C 62/08 New national side of euro coins intended for circulation . 9 EN 4.3.2014 EN Official Journal of the European Union C 62/1 II (Information) INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES EUROPEAN COMMISSION Non-opposition to a notified concentration (Case COMP/M.7138 — ThyssenKrupp/Acciai Speciali Terni/Outokumpu VDM) (Text with EEA relevance) (2014/C 62/01) On 12 February 2014, the Commission decided not to oppose the above notified concentration and to declare it compatible with the common market. -

THE ISLANDS of TAHITI the Big Influencers in the South Pacific Ocean: French Polynesia

Special Report This supplement is printed and This report was produced distributed by the Los Angeles Times in partnership with Media Group. It does not involve the editorial staff of Los Angeles Times. One World Media. 2019 TAHITI COME DISCOVER THE TREASURES: Tahiti is one of the most coveted leisure destinations in the world! Find the Mana: in search of the Polynesian Soul also for business THE ISLANDS OF TAHITI The big influencers in the South Pacific Ocean: French Polynesia ocated in the center of the “Another very real asset is our people”, Southern Pacific Ocean, Tahiti adds President Fritch, “The liveliness of our is the largest island of the people and our deep cultural roots make Windward group of French this country one of a kind, with men and Polynesia. Featuring world women eager to be producers, or partners, renowned black sand beaches or workers”. and clear blue seas, it has long been the One of the most difficult challenges Lcultural, economic and political center of the the country faces today has to do with country, as well as a hotspot for international modernization. In a global economy where tourism. technology plays an important role, many Having previously been a French colony, developing countries are struggling to keep today French Polynesia is considered France’s up with the pace. “Digital networks have only Country Abroad, entitling the territory become as important to countries as are to have more independence, with their own roads, ports and airports”, says President President and complete control over their Fritch, “This is why we are improving our economy and currency, the CPF Franc. -

ANNUAL REPORT 2014 in Charts, the Dots Indicate the Actual Data, and the Lines Reflect the Smoothing Approximation of the Data

ISSN 1407–1800 LATVIJAS BANKA: ANNUAL REPORT 2014 In Charts, the dots indicate the actual data, and the lines reflect the smoothing approximation of the data. The smoothing approximation of the daily data is more distinguished than the curve of the actual data. Details may not add because of rounding-off. – no transactions or no outstanding amounts in the period. x no data available or no computation of indicators possible. 0 the indicator is below 0.5 but over 0, or the result of the computation of the indicator is 0. © Latvijas Banka, 2015 The source is to be indicated when reproduced. Photos: Ieva Lūka and Andris Tenass The cut-off date is 27 April 2015. ISSN 1407–1800 Latvijas Banka K. Valdemāra iela 2A, Riga, LV-1050 Tel.: +371 67022300 Fax: +371 67022420 http://www.bank.lv [email protected] CONTENTS Foreword of the Governor 5 3 Statements of Vision, Mission and Values of Latvijas Banka 8 Economic Environment 9 Global and Euro Area Economic Environment 10 Currency and Financial Markets 10 Real Sector 12 Latvia's Economic Environment 14 Inflation and Prices 14 Gross Domestic Product 15 Labour Market 18 Foreign Trade, Balance of Payments and External Debt 19 Fiscal Developments 21 Credit Institution Developments 23 Money Supply 24 Lending and Deposit Rates 28 Foreign Exchange and Interbank Market 30 Securities Market 33 LATVIJAS BANKA: ANNUAL REPORT 2014 REPORT ANNUAL BANKA: LATVIJAS Operations and Activities of Latvijas Banka 35 Legal Framework and Functions. Latvijas Banka in the Eurosystem and Institutions of the European Union 36 Development, -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic